On June 20, 2026, three clues originally belonging to different worlds converged at the same coordinates: the tense air pressure over the Strait of Hormuz, an unusually heavy LINK deposit within the Meituan circle, and the covert war between Washington and state bankers regarding “dollar-pegged token yields.” Trump issued a 60-day ultimatum to Iran, emphasizing the passage of around 700 ships through this critical oil channel and warning that if Tehran did not compromise within the deadline, the U.S. could take action to ensure that oil here “would no longer flow out.” This threat instantly raised global energy risk premium expectations in market sentiment. At the same time, the fear and greed index in the crypto market rose from a lower position to 23, appearing to recover slightly but firmly remaining in the “extreme fear” range. In this atmosphere where everyone wanted to withdraw, a wallet viewed as a non-circulating supply source transferred approximately 18.375 million LINK to Binance, estimated at about 144.93 million USD based on a single price, which the market instinctively interpreted as potential selling pressure or at least a liquidity preparation move, further casting a shadow over the already fragile risk appetite for altcoins. Far from the frontline, the American State Bankers Association meeting highlighted “dollar-pegged token yields” as a key topic for communication with senators. Traditional banks were concerned that deposits and funds were being continuously drained by on-chain yield products, beginning to increase their negotiations with legislators. This means that in the future, the yield and compliance structure between dollar cash, bank deposits, and on-chain dollar assets might be redrawn. The threat of a blockade in Hormuz raises energy and safe-haven pricing, while the entry of LINK whales stirs on-chain and market sentiment, with the regulatory battle over on-chain dollar yields determining how long funds are willing to keep which part firmly in the crypto world. These three clues are working together to push funds down from high-beta speculative positions, forcing them to reallocate between “continuing to bet on risk” and “retrenching to dollar-pegged, high-liquidity assets.”

Hormuz Tension: Oil and Safe-Haven Premium

Trump marked the clock—60 days for Iran, coupled with the threat that “oil from Hormuz may no longer flow out,” essentially added an option premium directly onto global energy and geopolitical risk premiums. The Strait of Hormuz itself is one of the most important oil transport chokepoints in the world; any notion of “blockade” would be translated by the market into scenarios of rising future oil prices, hindered transportation, or even supply shocks. Even though U.S. envoy Witkoff and Iranian Foreign Minister Araghchi planned to meet in Switzerland, signaling that diplomatic channels remain open, the uncertain meeting time leaves this premium in a state of “cannot confirm, must pay first.”

In such a highly uncertain environment, asset ranking can quickly reorder: historically, global allocations often first cut exposure to high-volatility assets, shifting chips towards cash, short-duration government bonds, and energy and commodity-related positions, effectively adding “sandbags” to the portfolio. The problem is that current BTC and ETH are seen more as high-beta risk assets in the eyes of mainstream funds, rather than safe-haven tools alongside gold and government bonds—especially when the fear and greed index is still at 23 in that “extreme fear” zone. Any additional geopolitical noise only strengthens the instinctive reaction of “reduce positions first, then discuss narratives.” The result is that the longer Hormuz remains tense, the more shadow is cast over global risk premiums, while crypto positions are more likely to be categorized as risk assets that need to be discounted and compressed.

Fear Index Rises: BTC is No Longer Treated as Gold

The fear and greed index rose from a previous low of about 14 to 23, looking “a bit better,” but remains classified in the extreme fear range. This index itself is a composite reading crafted from multiple signals such as volatility, trading volume, and social sentiment, with 23 indicating that the market is collectively in a defensive posture: not asking “how much higher can it go,” but calculating “how much longer can it withstand.” In this emotional phase, historically common patterns include simultaneous deleveraging on-chain and off-chain, raising margin ratios, and increased liquidations of futures long positions, first cutting off leveraged legs before discussing any grand narratives. The result is that BTC and ETH's positions on investors' asset sheets are closer to a basket of highly leveraged tech stocks rather than “systematic insurance policies” that can be benchmarked against gold or government bonds; what is prioritized is “whether it can be quickly liquidated,” rather than “whether it can hedge macro risks.”

The trading structure during extreme fear phases thus becomes highly homogenized: selling off high-beta altcoins and long-term high-risk exposition, squaring leveraged longs, and reallocating risk budgets toward dollar cash, government bonds, and dollar-pegged tokens. BTC and ETH in this process are more often “chips being sold off” rather than “safe assets being held tightly,” serving as both a highly liquid escape route and a source of cash for covering losses elsewhere. Passive sell-offs on the spot side and proactive reductions on the derivatives side overlap, directly suppressing any imaginative space for bulls regarding price rebounds. At this point, the market question has shifted from “will geopolitical risk elevate BTC's long-term value” to “under the premise that the fear index remains at 23, who is willing to use new dollars to acquire assets that are collectively treated as risk assets?” The latter is the core variable that truly determines the upcoming price elasticity and flow of funds.

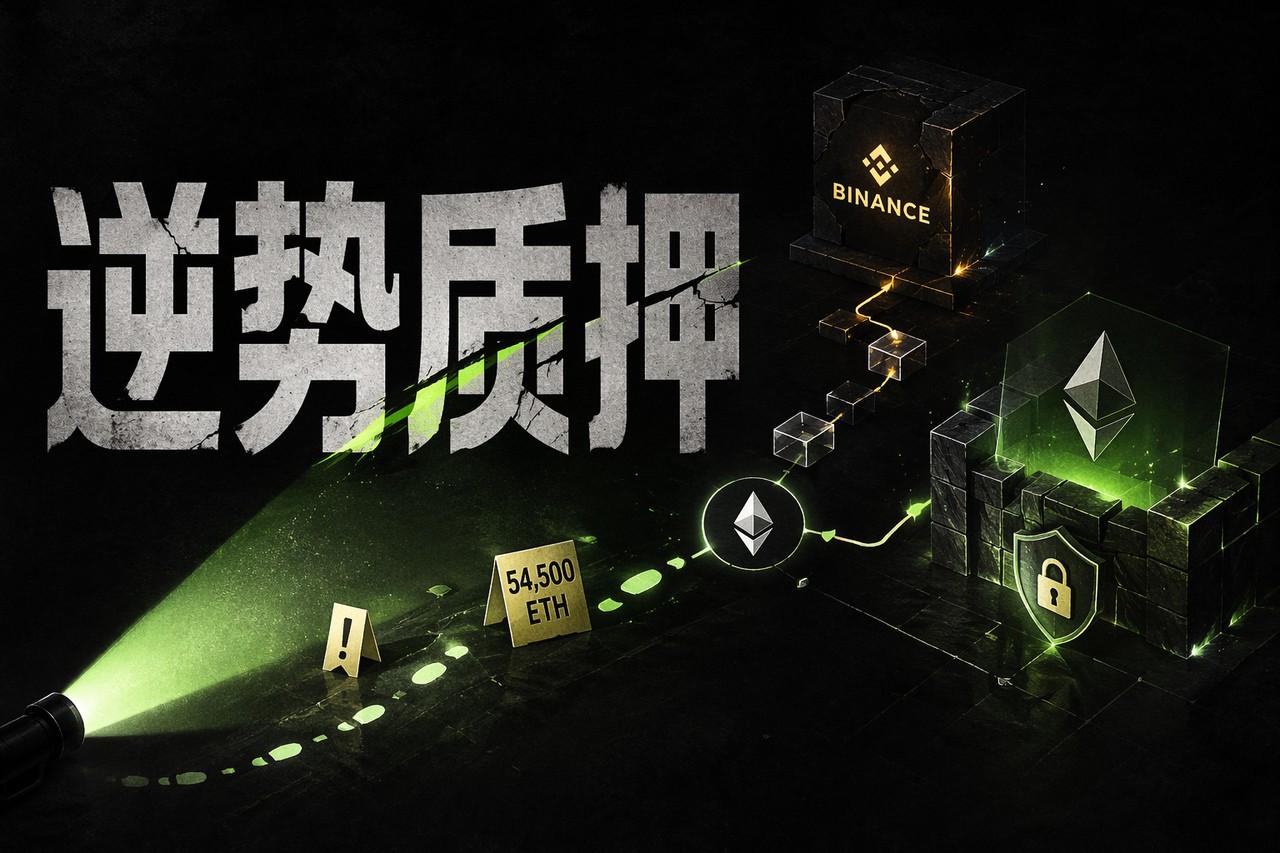

LINK 144 Million USD Deposited to Binance: Shadow of Selling Pressure Looms

Just as the fear index remained at 23 and funds were generally retracting, on-chain data delivered another blow to the market: a wallet widely viewed by the community as a “non-circulating supply source” transferred about 18.375 million LINK to Binance, estimated at nearly 144.93 million USD based on a single price source. Such an address is usually regarded as a long-term chip pool or “cold storage.” Once chips are pushed towards a centralized exchange, in traders’ experience, the implicit meaning defaults to two options—either preparing to sell or readying the chips for conditions to sell at any time. The problem is that up to now, public information has neither revealed the true use of this batch of LINK nor confirmed whether it has already been actively dumped or is lying in some newly created account waiting for instructions. However, in an extremely defensive emotional environment, the distinction between “not sold yet” and “preparing to sell” is deliberately blurred in terms of pricing, and that large deposit record on the chart is first understood as a layer of quantifiable overhead selling pressure.

The panic sentiment and geopolitical tensions combined not only trigger a repricing of LINK itself but also lead to an overall discount on the “large-cap altcoin” asset category. Usually, assets of LINK's size and depth represent a liquidity premium—institutions can hedge, leverage, and use it as on-chain collateral; but when the market suddenly realizes there is a chip equivalent to 144 million USD that could anytime be dumped into the same depth pool, this “liquidity that can exit at any moment” advantage instantly rewrites into “liquidity being able to be exited before you.” Market makers widen spreads, quantitative trading reduces relevant baskets ahead of time, and holders, to hedge against potential slippage, not only sell LINK itself but also simultaneously cut a basket of high-beta tokens, even pulling back some risk exposure to BTC and ETH. The valuation anchor of the entire crypto sector is forced to shift downward. Under this narrative, as long as the direction of this batch of LINK remains uncertain, funds will default to rearranging positions under the “worst scenario,” pushing more chips toward the dollar and dollar-pegged assets, while labeling high-volatility assets, including LINK, with a liquidity discount.

Stablecoin Yields Become the Focus: Wall Street Eyes the Spread

As funds retract from high-beta tokens and shrink into dollars, another battlefield quietly forms on Wall Street: According to Fox Business reporters citing insider sources, the State Bankers Association across the U.S. has recently listed “stablecoin yields” as a key topic for communication with senators. Traditional banks no longer see on-chain dollar assets as fringe toys but as competitors that could rob them of spreads—they are worried about deposits and short-term funds being siphoned off to dollar-pegged tokens or on-chain yield products that can generate returns. This anxiety over “deposit loss” has escalated from worries of individual banks to an industry consensus.

If legislation and regulation ultimately provide clear “pricing” for these yields—what type of yield is legal, how to disclose it, and how to tax it—fund allocation formulas will be rewritten: part will remain in bank demand and term deposits, part will pursue Treasury ETF yields, and another part will flow into on-chain dollar assets and DeFi yield pools within a compliant framework. Currently, although there are no public bill texts or timelines, as long as the market perceives a signal of “being included in a framework,” historical experience often indicates that institutions tend to increase their stakes in compliant, dollar-pegged assets, raising their weight in crypto portfolios. Amidst the hysteresis of rising Hormuz risk premiums, extreme fear still gripping the fear index, and the emotions suppressed by the entry of LINK whales, this yield spread battle will only amplify in one direction: high liquidity, dollar-pegged assets with clear compliance prospects will become the "new cash" for defensive positions, while BTC, ETH, and altcoins are further marginalized in risk budgets, only finding reasons to remain in the portfolio with lower valuations and smaller positions.

Trading Tactics Interwoven with Geopolitics and Regulation

Tying this round of clues together, the U.S.-Iran game over Hormuz raises energy and conflict premiums. The crypto fear and greed index, while recovering from lower levels, still sits at 23 in the “extreme fear” range, compounded by the concentrated entry of approximately 144.93 million LINK and the U.S. game over “stablecoin yields,” leads funds to a consistent answer: reduce risk, shorten duration, and align towards dollars and high liquidity assets. Under such combined shocks, the pricing of BTC and ETH resembles that of high-beta tech assets—thrown out first when extreme events occur, with only a chance to retell the “hedging” and “core allocation of digital assets” story after conflicts clarify and emotions repair; altcoins are more passive, with high-beta narratives and long-term visions difficult to secure risk budgets during overlapping periods of panic and regulatory uncertainty. Whether there are real selling pressures and whether they can maintain liquidity and compliance expectations become the key thresholds for their short-term survival in portfolios. The upcoming trading tactics must center on a few mainlines: first, the situation in Hormuz is the overall switch oppressing all risk assets; second, whether the crypto fear index can continue to rise from the extreme fear range will determine if overall positions can leverage again; third, whether LINK’s non-circulating wallets continue transferring to exchanges or reverse flowing back directly affects altcoin sentiment; and fourth, the speed of U.S. policy advancement surrounding “stablecoin yields” will reshape the yield structure between dollar-pegged assets and spot crypto. The direction of these mainlines will determine whether funds ultimately retreat to dollar yields in the long term or are willing to pay a higher risk premium for BTC, ETH, and certain altcoins.

Join our community to discuss and grow stronger together!

AiCoin exclusive Hyperliquid benefits: https://app.hyperliquid.xyz/join/AICOIN88

AiCoin exclusive Aster benefits: https://www.asterdex.com/zh-CN/referral/9C50e2

On-chain Telegram community: https://t.me/AiCoinWhaleData

On-chain community: https://www.aicoin.com/link/chat?cid=N6OVMor5g

AiCoin on-chain Twitter: https://x.com/aicoinwhaledata

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。