Summary

- The total market value of the global storage sector has seen explosive growth, with the three giants Samsung Electronics, SK Hynix, and Micron Technology all surpassing a market capitalization of one trillion dollars.

- As the demand for AI large model training and inference continues to grow, there’s a significant increase in data center requirements for high bandwidth memory HBM, DDR5, enterprise-grade SSDs, and other storage products in terms of demand intensity and value.

- Micron Technology recently officially entered the trillion-dollar market cap club, becoming one of the most watched revaluations in the AI storage industry chain. According to StockAnalysis data, as of June 3, 2026, Micron's market value is about 1.17 trillion dollars.

- The core reason for the rise in the storage sector this round is not merely a rebound in the traditional DRAM cycle, but rather the market starting to reprice AI servers, high bandwidth memory HBM, long-term supply agreements (LTA), and the structural value amid tight supply and demand in the storage industry.

- Gate officially launched stock trading, allowing users to directly trade mainstream securities markets' stocks and ETF assets using USDT on the platform. The stock contract section has launched perpetual contracts, supporting USDT settlement and 1-20 times leverage two-way trading. Gate has also introduced leveraged ETF tokens to provide investors with stock long exposure.

- Micron's trillion-dollar market value is not solely a result of a single performance cycle but is a reflection of the reevaluation of AI storage value, upgrades in HBM products, long-term agreement mechanisms, and improvements in industry supply and demand.

Storage Sector Driven by AI

In the past, the storage industry was often seen as a typical cyclical sector, with corporate profits highly dependent on supply-demand fluctuations and price elasticity. However, in the AI era, storage is gradually upgrading from a supporting component in general hardware to a key resource in computing infrastructure.

Large model training and inference not only require stronger GPUs and interconnect capabilities but also need storage systems with higher bandwidth, larger capacity, and lower latency. Whether it's HBM on the GPU side or DDR5 and enterprise-grade SSDs on the server side, their importance is significantly increasing. For cloud vendors and data center clients, storage is no longer just a cost item; it is a key variable influencing model training efficiency, inference throughput, and overall deployment costs.

The changes brought about by the expansion of AI applications are not just an increase in storage chip shipments but, more importantly, a rise in the proportion of high-end products. HBM has higher bandwidth, higher integration, and higher added value compared to ordinary DRAM; enterprise-grade SSDs have also benefited from the increased loads at data centers. As product portfolios shift towards high performance, the revenue structure, profit margin structure, and valuation framework of leading manufacturers may also change.

Unlike the traditional logic of "price increase leads to production expansion," high-end storage products like HBM are constrained by manufacturing processes, yield rates, advanced packaging, and client certification rhythms, so supply release is relatively limited. Meanwhile, core clients are more inclined to lock in production capacity and partial prices through long-term supply agreements, which enhance the revenue visibility and bargaining power of leading manufacturers compared to the past, allowing this round of prosperity to exhibit more pronounced structural characteristics.

Micron Technology, Inc. (NASDAQ: MU) was established in 1978 and is headquartered in Boise, Idaho, USA. It is a leading global supplier of semiconductor memory and storage solutions. The company primarily designs, manufactures, and sells DRAM, NAND Flash, NOR Flash, high bandwidth memory HBM, SSDs, and storage products for data centers, mobile devices, automotive, industrial, and consumer electronics. Using it as a research case is not to focus the article on a single stock but because Micron reflects the evolutionary direction of the AI storage sector in its product lineage, customer structure, performance elasticity, and market pricing.

Micron Technology

In the global storage chip industry, Micron is ranked with Samsung Electronics and SK Hynix as a major DRAM supplier and is also an important player in the global NAND market. As the demand for large model training and inference continues to grow, the demand for high bandwidth memory HBM, high-capacity DDR5, and enterprise-grade SSDs is rapidly increasing in AI servers. Storage chips are no longer just supporting components in general computing devices but are gradually becoming one of the key bottlenecks in AI computing infrastructure. Especially in GPU clusters, the performance in terms of bandwidth, capacity, and power consumption of HBM directly impacts the performance release of AI chips; thus, Micron is being re-included as a core supplier in the AI semiconductor industrial chain. This report views Micron Technology as an important representative company in the AI storage industry chain and will analyze its trillion-dollar market capitalization breakthrough, long-term agreements, HBM growth, valuation reconstruction, and Gate stock-related trading support.

Fundamental Analysis and Investment Logic

According to Gate market data, as of June 3, 2026, Micron Technology's stock price is $1,056. Based on approximately 1.1 billion diluted shares, the company's total market capitalization is about $1.17 trillion. Over the past year, Micron Technology (MU) has displayed a clear upward fluctuation trend, ultimately accelerating its breakthrough. The stock price started from about $110, gradually strengthened alongside expectations for AI storage demand and climbed steadily to over $400; after experiencing a phase adjustment, it once again entered a major upward wave driven by the explosion in demand for HBM and AI data centers, soaring significantly from May to June, reaching a high of $1,076, an increase of more than 8 times from the one-year low. Over the past year, Micron's stock price increased from around $110 to about $1,056, a cumulative increase of over 800%, with the company's market value simultaneously breaking through $1 trillion, reflecting the market's continued reevaluation of the demand for AI storage and the prospects for HBM business.

In terms of business structure, Micron currently focuses on four main application areas: first, data centers and cloud computing, including AI servers, enterprise servers, and networking devices; second, mobile terminals, including smartphones and tablets; third, storage business, including enterprise and client SSDs; fourth, embedded business, including automotive, industrial, and consumer electronics applications. With the continuous expansion of capital expenditures for AI data centers, the storage demand related to data centers is becoming the fastest-growing and highest profit elastic business direction for Micron.

Micron's recent market value breakthrough of one trillion dollars is not simply due to a rebound in the traditional storage cycle but rather stems from the market's revaluation of its strategic value in the AI infrastructure industrial chain. The FY2026 Q2 performance shows that the company's revenue, gross margin, EPS, and free cash flow have all set records, validating the profit inflection point driven by AI demand, industry supply constraints, and upgrades in high-end storage products.

In the AI Era, Storage Upgrades from Supporting Components to Strategic Assets

In traditional computing architectures, storage chips are typically viewed as supporting components outside the CPU and GPU, with industry pricing mainly influenced by cyclical supply and demand. However, in the AI era, especially after the continuous expansion of large model training and inference, memory bandwidth, capacity, and energy efficiency have become key bottlenecks for the performance release of AI systems.

Micron clearly stated in the FY2026 Q2 performance announcement that the record performance in Q2 reflects the “strategic value of storage in the AI era.” Company CEO Sanjay Mehrotra indicated that storage has become a strategic asset for customers in the AI era. This signifies that Micron's management has repositioned the company from a traditional storage supplier to a core player in AI computing infrastructure.

The rapid growth of demand for HBM, high capacity DRAM, DDR5, and enterprise-grade SSDs in AI servers has significantly increased the value of storage products in the server BOM. As GPU cluster scales expand, customers are not only focusing on chip computing capabilities but also increasingly concerned about the stability of storage supply, performance matching, and controllable deployment costs. This change brings Micron stronger bargaining power and higher profit elasticity.

FY2026 Q2 Performance Validates Demand Strength

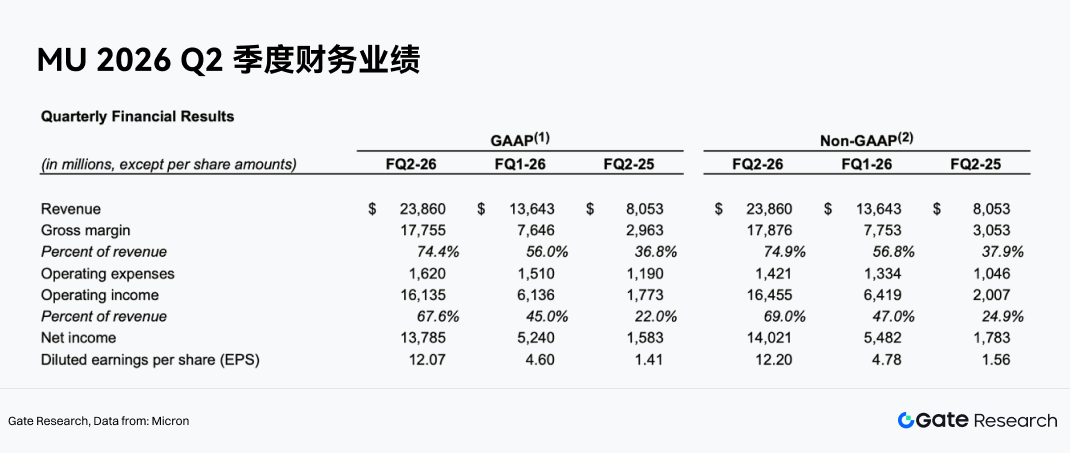

Micron's FY2026 Q2 revenue reached $23.86 billion, a significant increase from the previous quarter's $13.64 billion, and also well above the $8.05 billion from the same period last year. The company’s Non-GAAP net profit reached $14.02 billion, Non-GAAP EPS was $12.20, operating cash flow reached $11.90 billion, and adjusted free cash flow reached $6.90 billion.

More importantly, profit quality is also improving synchronously. FY2026 Q2 Non-GAAP gross margin reached 74.9%, significantly higher than the previous quarter's 56.8% and last year's 37.9%; Non-GAAP operating profit margin reached 69.0%, compared to 47.0% last quarter and 24.9% a year earlier.

This indicates that Micron is not merely relying on revenue growth to drive profits but has achieved a leap in profit margins under the combined improvements in product pricing, product structure, and cost efficiency. For a storage company, increasing gross margins from the 30%-40% range to over 70% means that the supply-demand relationship and the company’s product mix have undergone significant changes.

Data Center and Cloud Business Become Core of Growth

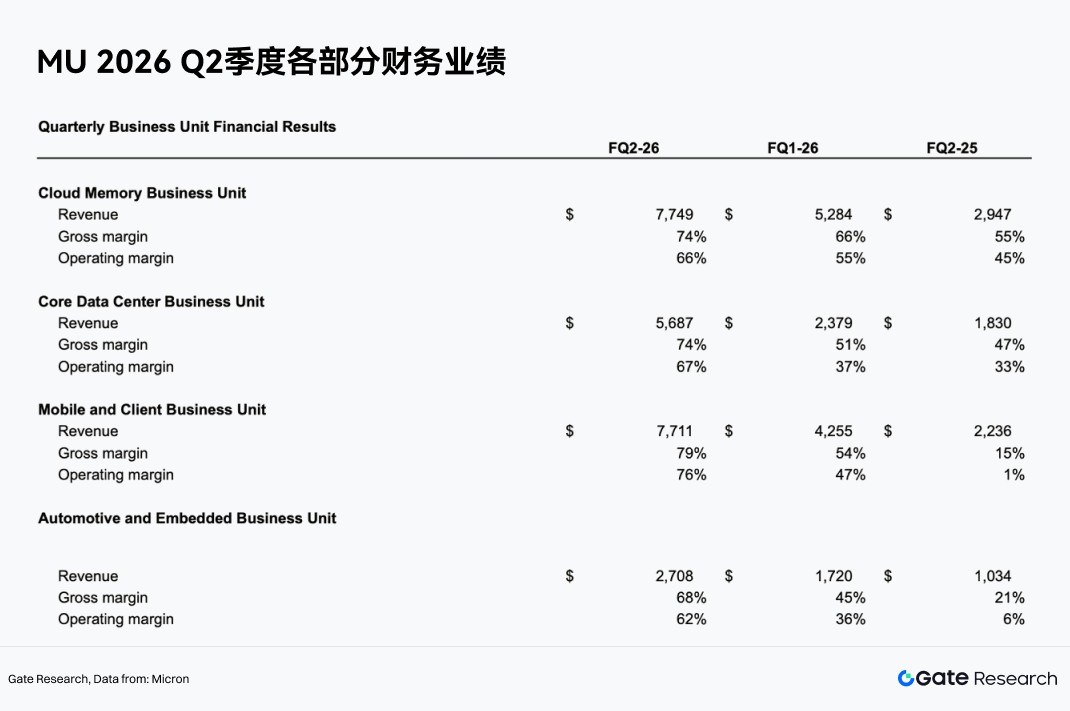

From a business unit perspective, Micron's FY2026 Q2 growth is highly concentrated in AI and data center-related directions.

The Cloud Memory Business Unit's revenue reached $7.749 billion with a gross margin of 74% and an operating profit margin of 66%. The Core Data Center Business Unit's revenue reached $5.687 billion with a gross margin of 74% and an operating profit margin of 67%. These two business units combined accounted for over $13.4 billion in revenue, becoming the company’s most important growth engine.

This shows that Micron's business focus is shifting from traditional consumer electronics cycles like PCs and mobile phones to cloud computing, AI servers, and data centers. Compared to consumer electronics, AI data center customers have characteristics such as large capital expenditure scales, high product performance requirements, and strong continuity of supply, making it easier to form high-end product premiums and long-term supply relationships.

HBM and High-End DRAM Drive Product Structure Upgrade

The most obvious product direction benefiting Micron is HBM and high-end DRAM. HBM is a key storage product in AI GPUs and accelerators, featuring high bandwidth, high capacity, and high energy efficiency, with price per GB and gross margin both exceeding that of ordinary DRAM.

UBS predicts that Micron's HBM ASP will grow by about 50% year-on-year by 2027, continuously driving the expansion of HBM revenue. As AI chip platforms iterate, demand for HBM capacity and bandwidth is expected to increase, allowing Micron to achieve a higher proportion of revenue through HBM3E, subsequent HBM products, and advanced packaging capabilities.

The significance of the product structure upgrade is that Micron is no longer just following industry DRAM average price fluctuations but is gaining stronger pricing power through high-end products. With the increase in the proportion of HBM, the company's overall gross margin and profit stability will also improve.

Industry Supply Tightness Strengthens Price Elasticity

Micron’s strong performance in FY2026 Q2 also comes from industry supply tightness. The performance is driven by a combination of a strong demand environment, tight industry supply, and the company’s execution ability. Some institutions expect that the DRAM industry's supply shortage will continue at least until the second quarter of 2028, and NAND supply shortages will last until the fourth quarter of 2027. In a constrained supply environment, DRAM and NAND prices have sustained support, and Micron's revenue and margins are likely to remain high.

More importantly, this cycle is different from the past. In the past, storage manufacturers often rapidly expanded production after price increases, ultimately leading to oversupply and price drops. However, the demand growth rate for high-end memory in AI servers is rapid, and HBM capacity expansion is constrained by technological, yield, advanced packaging, and client certification cycles, making it challenging for supply to quickly catch up with demand.

Long-Term Supply Agreements (LTA) Enhance Profit Visibility

LTA, which stands for Long-Term Agreement, refers to long-term supply agreements. In the semiconductor storage industry, LTA typically refers to the advance arrangements made between suppliers and core clients regarding future supply, including procurement quantities, delivery cycles, product specifications, and in some cases, price frameworks. In the past, procurement agreements in the storage industry were more inclined toward "locking volume but not price." Clients committed to a certain procurement volume ahead of time, providing suppliers with partial demand visibility, but prices would still fluctuate rapidly according to DRAM and NAND market supply and demand. Therefore, when the industry enters a downturn, substantial price declines would directly impact the revenue and profit of storage manufacturers like Micron, Samsung, and SK Hynix.

LTA is another key logic for Micron's valuation reassessment. The new type of LTA not only locks in procurement volume but also partially locks in prices, with terms lasting up to 3-5 years. This is different from past agreements that solely locked in volume. For Micron, the value of LTA lies in increasing revenue visibility, reducing price volatility, and improving cross-cycle profitability. For cloud vendors and AI clients, LTA can ensure future storage supply and partly lock in costs, avoiding passive absorption of higher prices during supply constraints. If LTAs are implemented on a large scale, Micron’s business model will gradually shift from that of a traditional cyclical commodity company toward one that possesses long-term orders, stable cash flow, and stronger customer loyalty as a semiconductor supplier.

Profit and Cash Flow Support Valuation Reconstruction

Micron's adjusted free cash flow reached $6.9 billion in FY2026 Q2, and the company's board approved a 30% increase in the quarterly dividend. This indicates that not only has the company’s profitability significantly improved, but the quality of its cash flow has also noticeably enhanced. In capital markets, stable and substantial free cash flow often supports higher valuations. Micron's past low valuation was primarily due to market concerns about the sustainability of its profits; however, now, if AI demand, LTA, and the upgrades in HBM product structure collectively reduce cyclical fluctuations, Micron qualifies to transition from traditional storage cycle stock valuations to valuations reflective of core AI semiconductor assets.

Gate Stock Investment Products

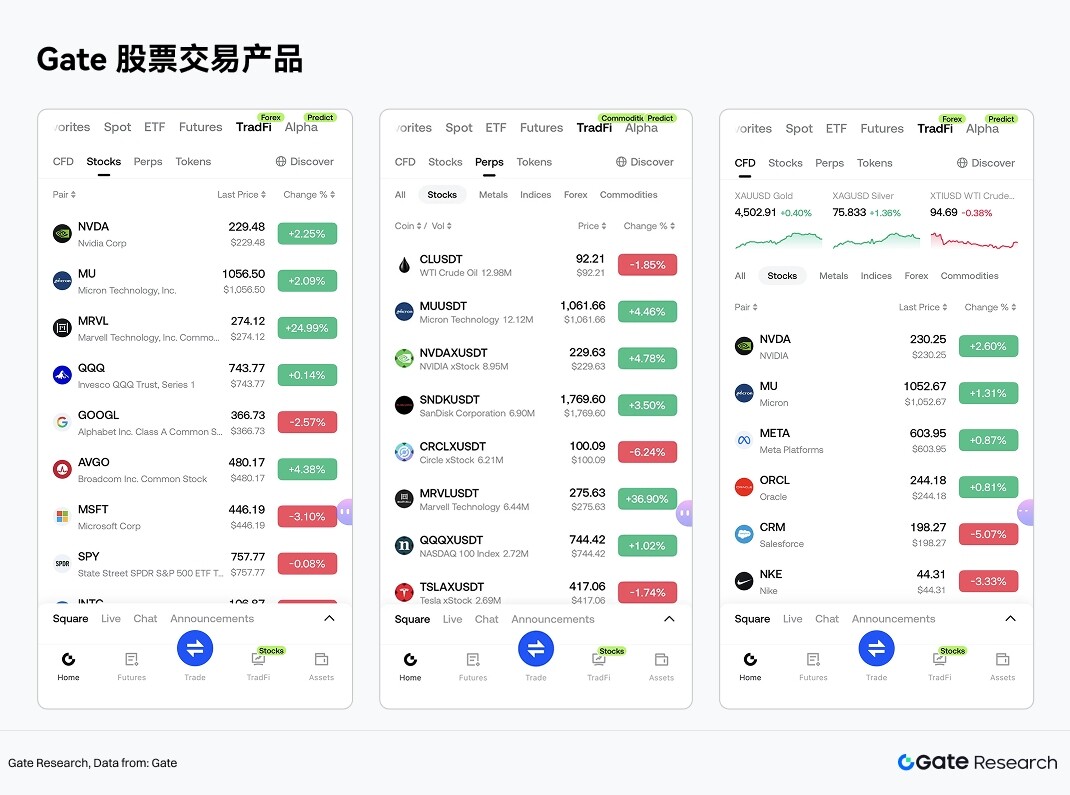

The most watched American stock targets in the storage sector. Gate has also supported US stock-related trading services in the TradFi sector, allowing users to participate in trading assets such as stocks and ETFs in the mainstream securities market using USDT through a unified account system.

Unlike the common stock tokenization or RWA mapping models in the market, Gate's stock services emphasize market access capabilities and compliant trading systems. Gate stocks are offered through compliant brokerage connections, providing users with stock and ETF trading services, not on-chain mapped assets or tokenized stock derivatives. Users can complete the buying, holding, and selling of stock assets through their Gate accounts, and related holdings, P&L, cash flows, and corporate action information can be viewed and managed uniformly within the account.

In terms of the coverage of targets, Gate stocks currently support over 10,000 stocks and ETFs, covering mainstream securities trading markets and liquidity networks such as NYSE, Nasdaq, NYSE Arca, NYSE American, and BATS. Currently, Gate stocks support intraday trading and will gradually expand to 24/7 trading in the future, providing global users with a more flexible entry point for US stock asset allocation.

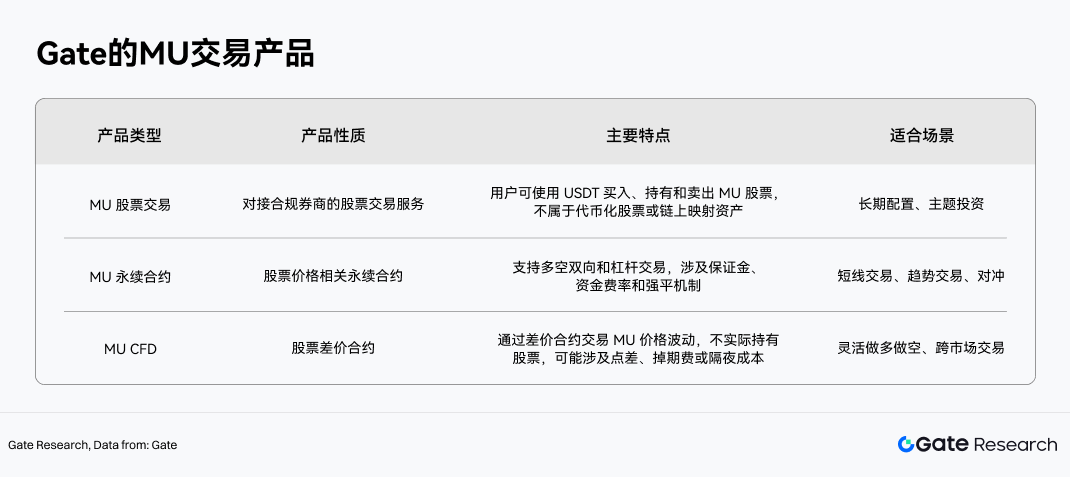

In terms of product structure, Gate TradFi has trading tools related to stocks divided into three categories, taking the MU trading product as an example:

Among them, Gate stock spot trading and the traditional CFD system operate independently. Stock trading does not involve funding rates in perpetual contracts, nor does it involve position costs such as swaps or overnight fees that may exist in CFD products, making it more suitable for users who wish to hold US stock assets for the long term. In contrast, perpetual contracts and CFDs are more oriented toward trading tools, suitable for directional trading or risk management regarding Micron's short to medium-term price fluctuations.

Relying on a unified crypto asset account system, Gate further bridges digital asset trading and stock investment scenarios. After completing KYC and meeting the access requirements in their respective regions, users can access stock sections in the TradFi segment of the Gate App to view market data and participate in trading after conducting stablecoin transfers via the trading or asset pages. This means that the application scenario for USDT is extending from crypto asset trading to global stock asset allocation.

From an industry trend perspective, Gate's launch of stock trading services provides users with a unified trading entry for digital assets and traditional financial assets. For users focused on the AI semiconductor theme, the launch of real stocks, perpetual contracts, and CFDs allows for more flexible asset allocation and trading management around storage, AI, HBM, and the semiconductor cycle on the same platform.

Risk Warning

From a sector research perspective, future judgments regarding the prosperity of the storage industry and company quality can focus on four dimensions: first, whether capital expenditures by AI server and cloud vendors continue to expand; second, the penetration rate and ASP changes of high-end categories like HBM, DDR5, and enterprise-grade SSDs; third, the supply discipline and expansion rhythm of leading manufacturers like Samsung, SK Hynix, and Micron; fourth, whether long-term supply agreements, client certification, and advanced packaging capabilities continue to strengthen industry barriers.

This implies that the storage sector can no longer be fully understood through the past single “price cyclical stock” framework. For researchers, a more reasonable analytical approach is to consider it as a semiconductor sub-sector where “cyclical attributes still exist, but the weight of structural upgrades continues to increase”; Micron’s case provides a highly recognizable sample for observing this transition.

Furthermore, although LTAs help stabilize part of the income, uncertainties still exist regarding their price-locking ratios, execution periods, and client commitments, which may not completely eliminate industry fluctuations. Micron's stock price and market capitalization have risen significantly, and the market has high expectations for the AI storage super cycle and valuation reconstruction; if performance fails to meet these expectations, stock price volatility may intensify.

References

- Gate, https://www.gate.com/

- Micron, https://investors.micron.com/node/50256/pdf

- UBS, https://research.ibb.ubs.com/openaccess/compliance/79529_1_new.html

Gate Research Institute is a comprehensive blockchain and cryptocurrency research platform that provides readers with in-depth content, including technical analysis, hot insights, market reviews, industry studies, trend forecasting, and macroeconomic policy analysis.

Disclaimer

Investing in the cryptocurrency market involves high risks. Users are advised to conduct independent research and fully understand the nature of assets and products purchased before making any investment decisions. Gate does not assume liability for any losses or damages resulting from such investment decisions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。