Crypto neobanking is moving from card distribution to account ownership.

The card economics are limited: interchange is often ~2% and the broader merchant-fee pool gets split across the payment stack. Margins are thin after rewards, chargebacks, and processing costs.

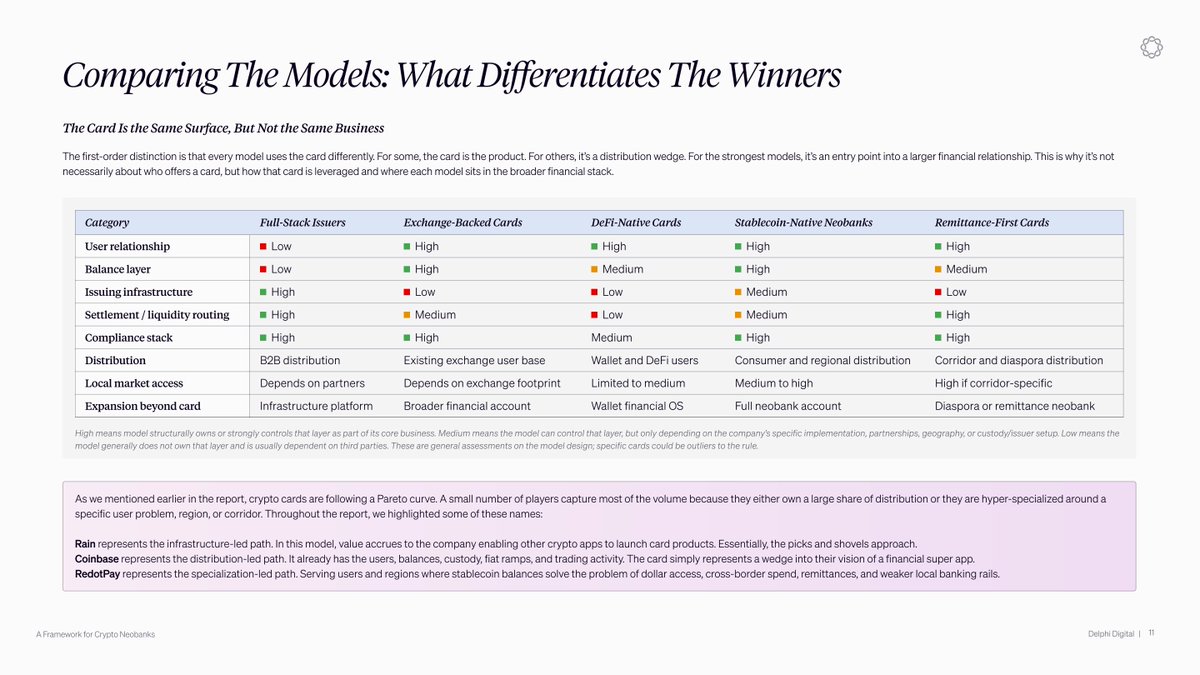

Rain processed $2.42B in card volume without owning the consumer front end. It controls issuance through Visa's principal member program, captures a bulk of interchange, and powers other companies' cards from the backend.

The other side is the account layer. Exchanges like Coinbase already hold user balances, custody, and trading activity. Exchange-backed cards keep users from cashing out and moving back to a bank. This can be a retention strategy that keeps activity within the ecosystem.

Plasma One treats the account as the product and the card as one feature inside it. It layers transfers, local on/off-ramps, and global card spend around the balance.

Specialization wins when it owns a corridor. Felix Pago has processed over $5B across Latin American remittance flows because legacy rails are too expensive, slow, or inaccessible.

The business underneath the card determines who survives.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。