The Douyin creator "Li Yien" has found his traffic password. Before commenting on the stock market every day, he always shouts a slogan, "Still that saying, time will prove the optical modules and computing power." After shouting for more than a year, the likes on a single video have risen from two or three thousand to forty or fifty thousand, and netizens flocking to the comments section only ask one question: now that they are "standing in the light," is it too late.

The three words that connect the anxiety of netizens are "Yi Zhongtian." It is not the scholar from the Lecture Hall, but a nickname given by A-shares to three leading companies in optical modules: New Yisong, Zhongji Xuchuang, and Tianfu Communication, each taking one word. Starting from the low point in April 2025, New Yisong has increased by 16 times, Zhongji Xuchuang by 17 times, and Tianfu Communication by 10 times. Those who bought in early have made a fortune.

But as the story reached June 2026, the plot took a turn. On June 5, "Yi Zhongtian" collectively plunged, with Zhongji Xuchuang dropping nearly 8% in a single day. On June 11, New Yisong's price almost hit the daily limit, and the CPO concept began to adjust. The people rushing to escape and those flocking to bottom-fish completed their handover amidst huge trading volumes.

The story of wealth creation has been told to death. The real question that no one has answered seriously is another: if you could only choose one of the three, which one is the most valuable? In this article, we will not discuss "whether you can still get on the bus," but only deconstruct one question: among Yi Zhongtian, whose cost performance is the highest.

No one in this round of optical module market looks at the current price-to-earnings ratio anymore.

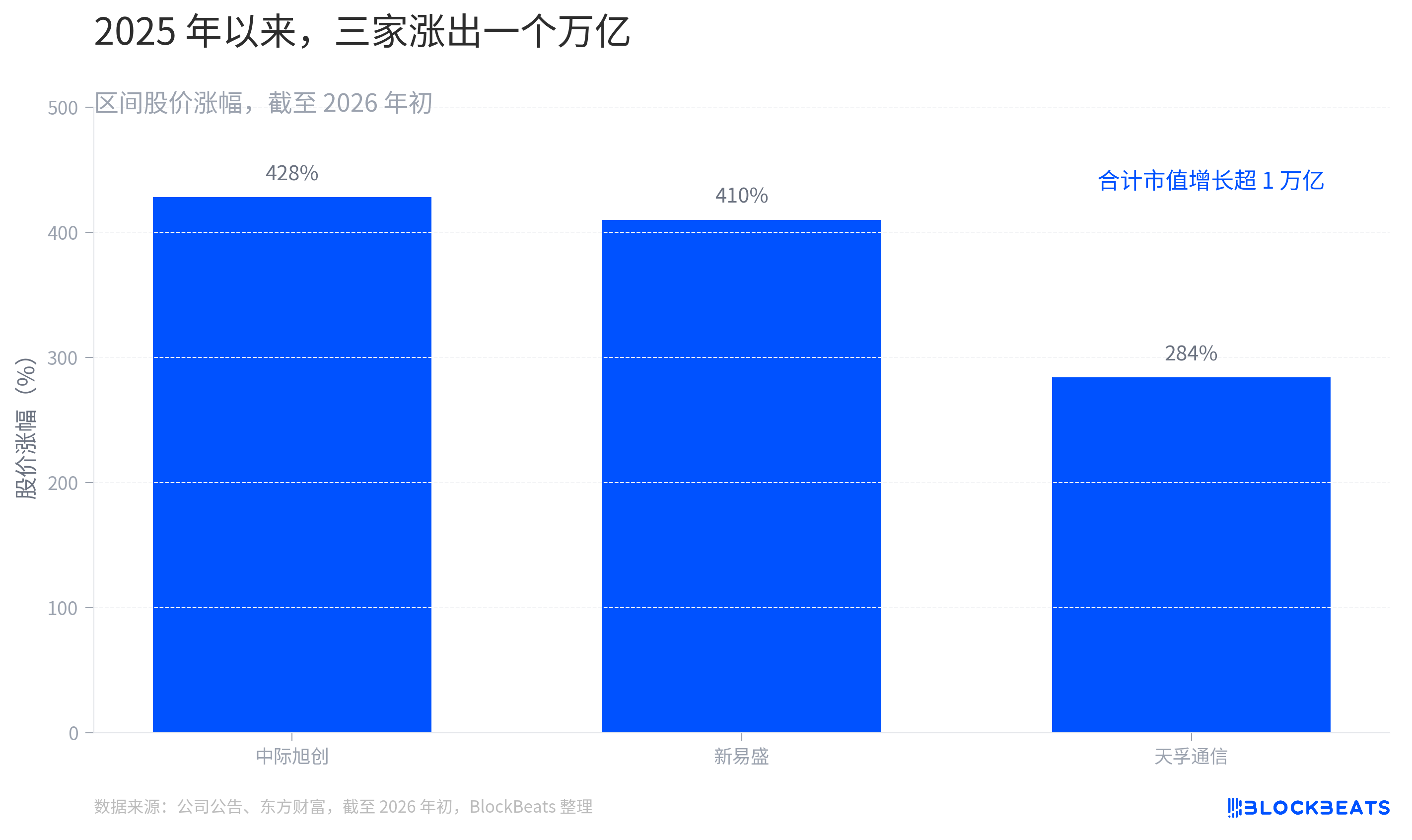

The reason is simple: when a company's profits are still growing at triple-digit speeds, calculating the price-to-earnings ratio based on the profits from the past twelve months produces a meaningless number. The anchor of market pricing has shifted from "how much is earned this year" to "how much can be earned in 2026 and 2027." As of early 2026, the stock price increases since 2025 for the three companies were Zhongji Xuchuang at 428%, New Yisong at 410%, and Tianfu Communication at 284%, with a total market capitalization increase of over one trillion yuan. This one trillion is not buying the present, but the expectations for the next two to three years.

Therefore, "cost performance" here does not mean "which stock price is lower," but needs to be measured with three metrics. The first metric is PEG, which is the dynamic price-to-earnings ratio divided by the growth rate, measuring "how much you are paying for the same growth." The second metric is profit quality, measuring how clean the earnings are and how high the gross margin is. The third metric is certainty's premium/discount, measuring how much the market is willing to pay extra for "stability" and how much to deduct for "uncertainty."

Using these three metrics, the three companies provide three completely different answers. One is the king of cost performance in numbers, one is expensive but stable certainty, and one is the most expensive certainty.

New Yisong: the king of cost performance in numbers, but being cheap has its reasons.

First, let's look at the one that is numerically the cheapest.

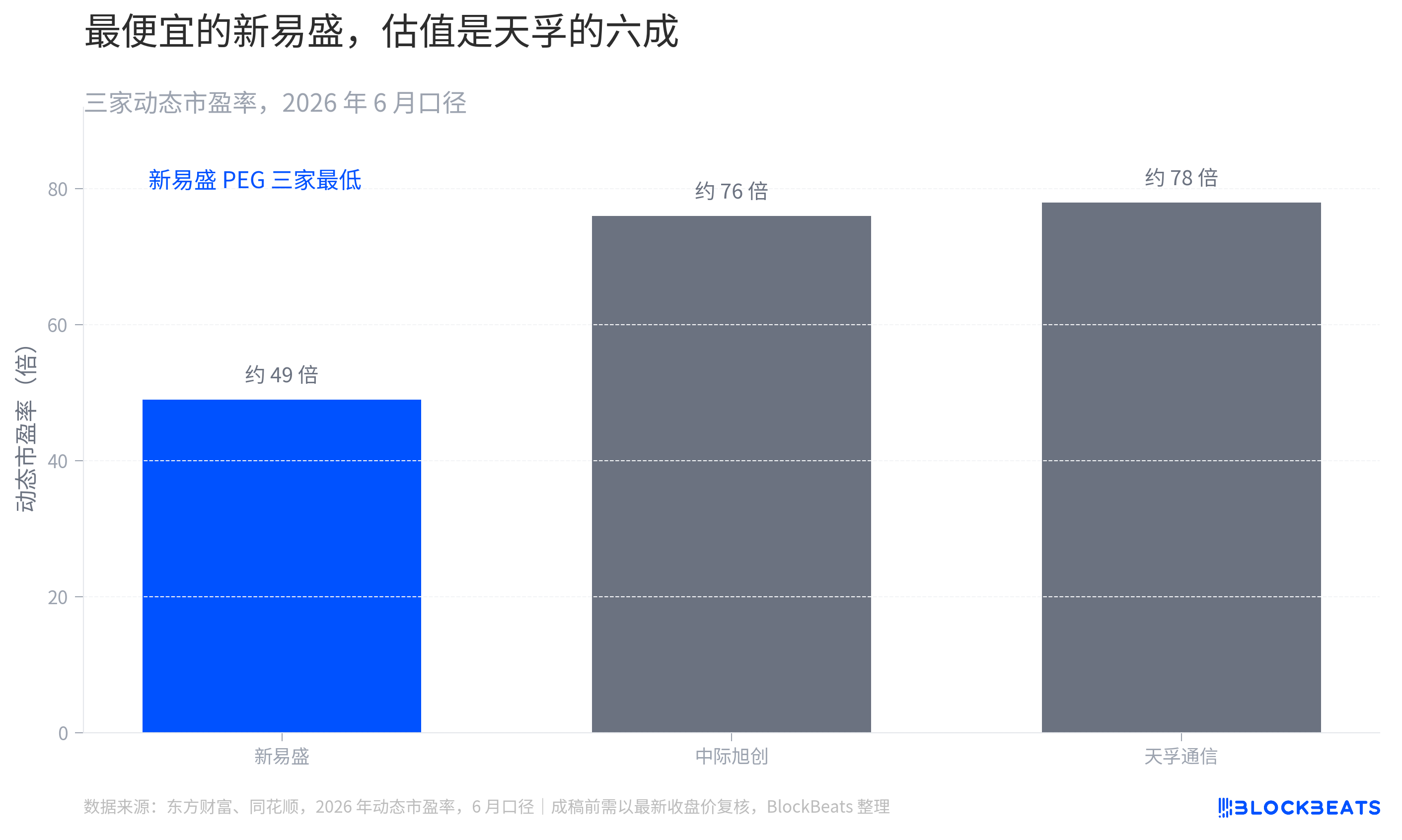

By PEG calculation, New Yisong is the most cost-effective among the three. Its net profit attributable to the parent in 2025 is expected to grow nearly 2.5 times year-on-year, significantly higher than the 89.5% to 128% growth of Zhongji Xuchuang during the same period. In the fourth quarter, its net profit grew +39% quarter-on-quarter, and the 1.6T product was released early. Such rapid growth comes with the lowest valuation. Based on the consensus expected net profit for 2026, its dynamic price-to-earnings ratio is only about 22.8 times, with a corresponding PEG of about 0.30, the lowest among the three. For the same unit of growth, you pay the least for New Yisong.

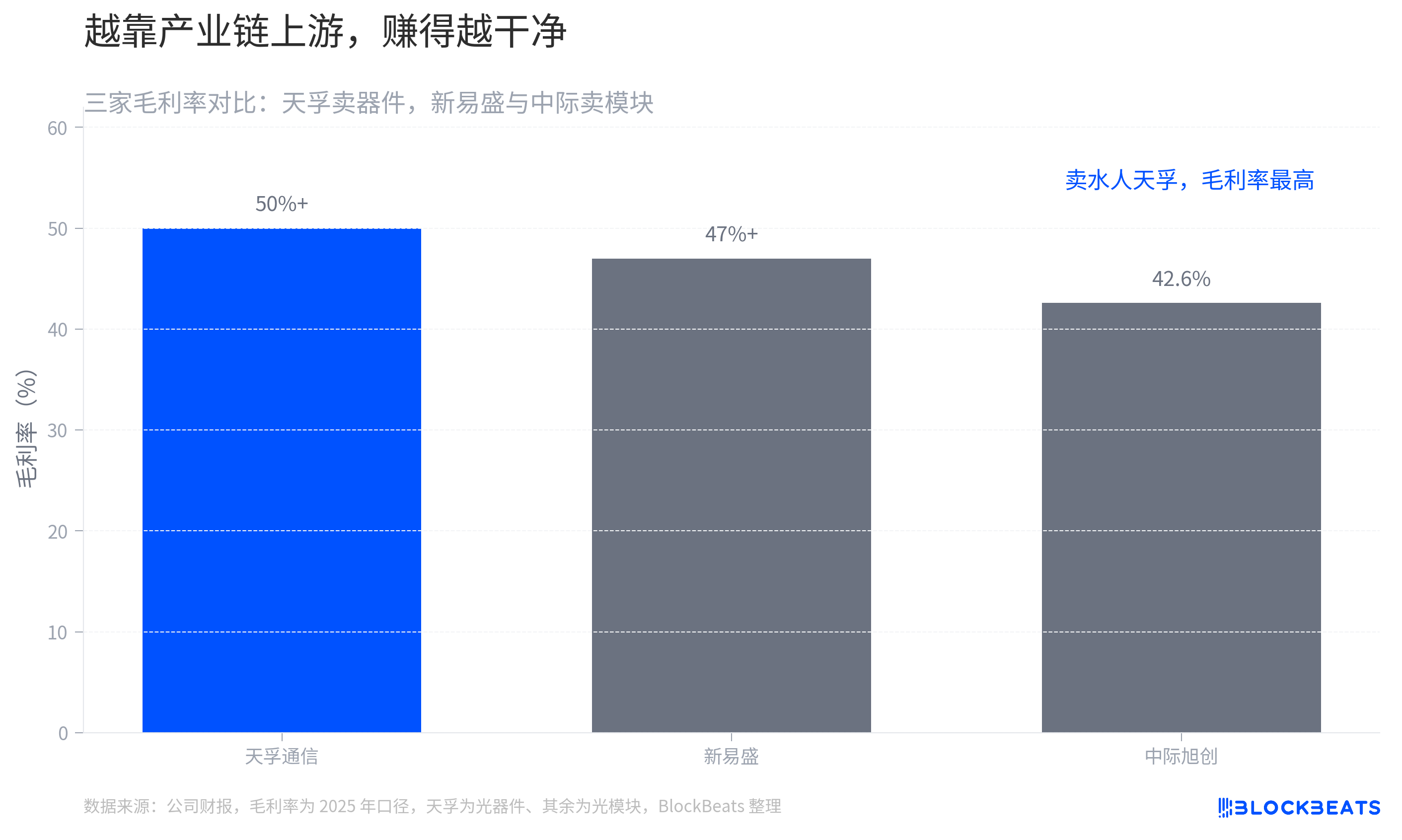

Not only is it cheap, but the money it earns is also the "cleanest." In its 2025 performance, New Yisong's non-recurring gains and losses are only 33 million yuan, with a gross margin above 47%, relying on cost advantages from vertical integration. On this profit quality metric, it even outperformed the larger Zhongji Xuchuang.

At this point in the story, New Yisong seems like an underestimated dark horse by the market. But this is precisely where one should not stop at the surface. Its cheapness indicates a discount, not a windfall.

The market does not arbitrarily discount a high-growth company. The real risk factors that are depressing New Yisong include a high customer concentration, with its performance highly dependent on a few large customers. The overseas revenue proportion reaches 78%, directly exposed to risks from tariffs and trade restrictions. Most importantly, can the "dark horse" maintain its explosive growth? In terms of long-term technology narrative and forward planning, its story is not as solid as that of Zhongji Xuchuang. The low price-to-earnings ratio given by the market essentially discounts "sustainability."

This discount is being partially restored. By 2026, New Yisong's stock price has risen over 79% and it is planning to go public in Hong Kong. Funds are using their feet to vote, pulling it from being "an untrusted dark horse" to "a revalued leader." It is cheap, but the discount is narrowing.

As for the expensive one, where is its stability?

Zhongji Xuchuang: expensive certainty.

The cost performance of Zhongji Xuchuang does not lie in its cheapness, but in its certainty.

Understanding this is straightforward by looking at a comparison. In the first quarter of 2026, Zhongji Xuchuang's revenue was 19.496 billion yuan, with a net profit of 5.735 billion yuan. Just one quarter's net profit exceeds its total for the entire year of 2024. During the same period, its gross margin for optical communication transceiver modules improved from 34.65% in 2024 to 42.61%, an increase of nearly 8 percentage points. Scale is increasing, and the efficiency of profit-making is also increasing, which is the stance of a leader.

Supporting this certainty are market share and technological gap. Zhongji Xuchuang secured more than half of NVIDIA's procurement of 800G optical modules. For the 1.6T generation, it is expected to capture 50% to 60% of the market share due to its first-mover advantage by completing NVIDIA verification first. During last year's third-quarter earnings call, the company's executives made the rhythm clear: "In the third quarter of this year, key customers will start to deploy 1.6T and continue to increase orders... It is expected that from 2026 to 2027, other key customers will also deploy 1.6T on a large scale." To capture these orders, the company is preparing chips and expanding capacity, laying out on both domestic and overseas fronts.

The cost of this is that it is the most expensive. Zhongji Xuchuang's rolling price-to-earnings ratio once reached 73 to 74 times, more than 40% higher than that of New Yisong. What you are paying for is a premium of "leading barriers + technological leadership." This premium is suitable for those who value certainty more and can afford to pay a higher price.

However, certainty does not mean the absence of risks, and its risks are more prone to "black swan" nature. On June 8, 2026 (US time), Zhongji Xuchuang was placed on the "1260H List" by the U.S. Department of Defense. The company urgently responded, stating that this designation does not conform to objective facts, as the company is neither a military enterprise nor a military-civil integration enterprise, and it has not had a substantial impact on operations, with orders, production, and supply chains all normal. However, for a company with an overseas revenue proportion reaching 86.8%, geopolitical issues are the real sword hanging over its head. It may not affect the fundamentals, but it could cut the valuation on any trading day.

Having dissected the two module manufacturers, there remains Tianfu, which does not belong to the same table at all.

Tianfu Communication: the most expensive certainty, betting on the next-generation architecture.

What makes Tianfu Communication special? It does not sell modules; it sells "water."

An analogy using an industry chain will be the most intuitive. If Zhongji Xuchuang and New Yisong are the restaurants directly facing the diners, Tianfu Communication is the supplier to those restaurants. It sells optical engines and optical devices, the core components, to downstream optical module manufacturers, who assemble them into complete modules for shipment. It does not directly take orders from cloud vendors, but every high-end optical module contains its products.

Being situated upstream allows it to maintain the highest gross margin among the three, consistently above 50%, and the competitive landscape is the clearest. More importantly, it has hit on a highly certain long slope: the CPO/NPO architecture. Institutions estimate that in the value chain of a high-configured 51.2T switch, the combined potential value of Tianfu Communication in the FAU, precision lenses, and optical engine packaging phases could reach the scale of $7,000 to $10,000.

In comparison to the several dozen dollars of component value in the traditional pluggable era, this represents a complete simultaneous increase in quantity and price. Regardless of which module solution downstream cloud vendors ultimately choose, as long as data centers continue to evolve towards more efficient and energy-saving architectures, the position of the "water seller" is secure.

It sounds beautiful. However, Tianfu's problems are hidden within the phrase "water seller." It boasts the least elasticity, the highest valuation, and is the most likely to miss expectations.

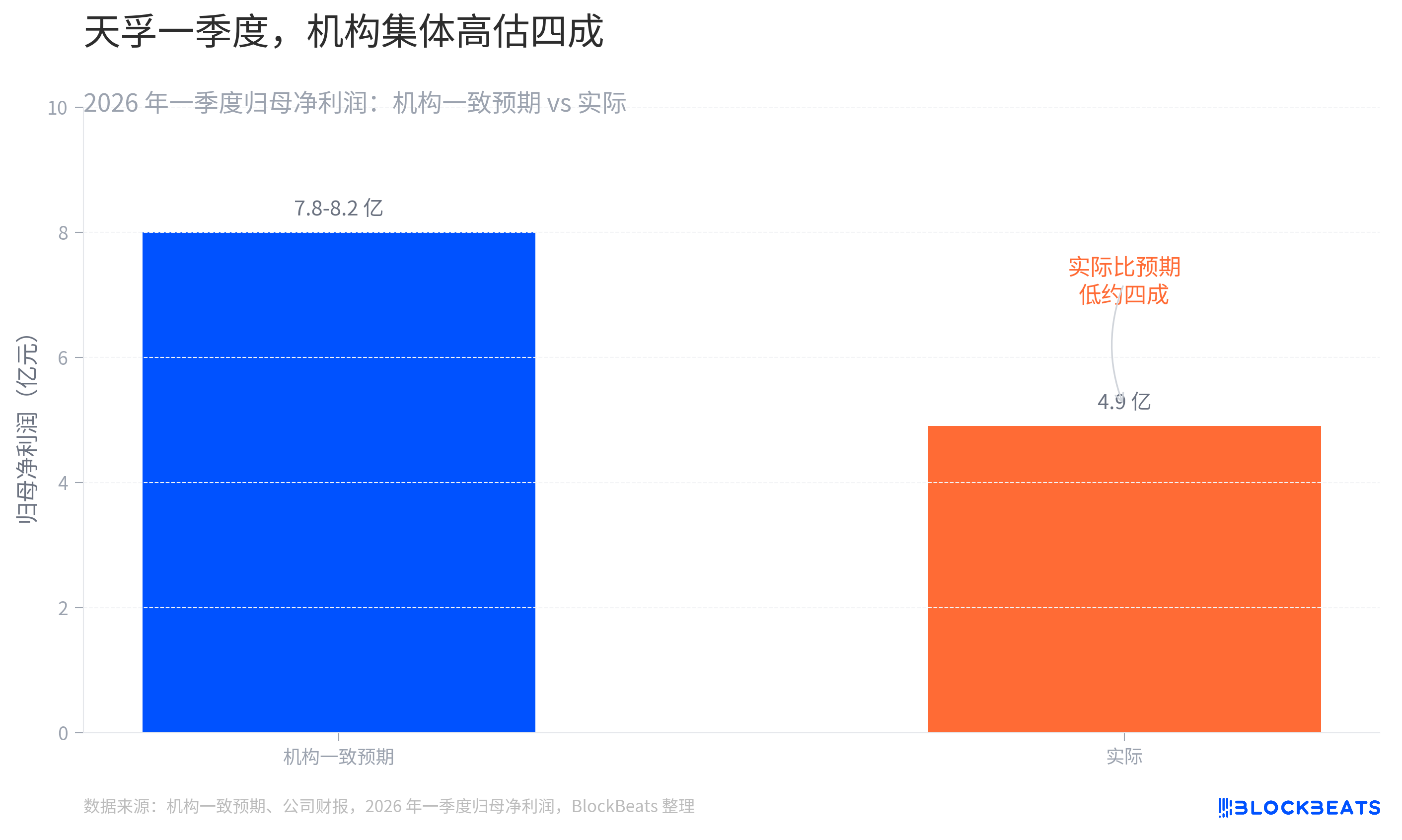

The low elasticity is due to its growth being a stream, not a pulse. Zhongji Xuchuang and New Yisong directly benefit from the pulse-like explosion of AI capital expenditures, resulting in huge performance elasticity. Tianfu's growth is steady but gradual. The high valuation reflects the market's anticipation of this certainty sky-high. By February 10, 2026, its rolling price-to-earnings ratio was about 122 times, far higher than the other two. The ease of missing expectations was vividly demonstrated in the first quarter of 2026. Institutions unanimously expected its net profit for that quarter to be between 780 million and 820 million, but it was only 490 million. The massive gap was the result of institutions applying the pulse logic of module manufacturers to a component company.

This precisely reminds everyone who wants to rank "Yi Zhongtian": Tianfu and the other two are not on the same table. Using the pricing logic of selling complete machines to make judgments about a seller of engines is a misunderstanding in itself.

At this point, we have dissected the three companies. However, the issue of "cost performance" carries a hidden variable that everyone has overlooked.

The profit pool is not in their hands at all.

Returning to that card table, let's ask a tougher question: the money made from Yi Zhongtian, is it really "good money"?

The essence of optical modules is system integration. It involves procuring optical chips, electronic chips, and optical devices, then assembling them into a complete module using packaging technology. The barrier does not lie in the assembly itself. The true profit pool and moat are concentrated at both ends of the industry chain: upstream laser chips and switching chips. The process that Chinese manufacturers dominate is the assembly process in the middle.

Hence, many people’s remarks about "Zhongji crushing Lumentum and Coherent" must be viewed in two layers. It holds true in module market share. Zhongji Xuchuang indeed has pressed these two traditional American manufacturers down. However, in terms of profit quality, it’s a different story.

Lumentum and Coherent guard precisely the upstream. They hedge the risk of supply shortages through vertically integrated laser chip supply, and the advantages of InP and GaAs platforms in high-power applications still genuinely exist. Moreover, these two are not handily defeated fallen soldiers, but upstream players that are rapidly bouncing back. In Q1 of the 2026 fiscal year, Lumentum's revenue grew by 58% year-on-year, with a gross margin increasing from 28% to 34%.

Coherent managed to achieve a quarterly revenue of $1.81 billion during the same period, with a year-on-year growth of 21%. The data center and communication business accounted for 75% of total revenue, with year-on-year growth exceeding 40%. Its non-GAAP gross margin reached 39.6%.

What's even more striking is that in this round of trillion valuations for Yi Zhongtian, the bet is on the transition of the CPO architecture. However, CPO is inseparable from CW light sources and InP substrates, which happen to be American companies' stronghold. Coherent is doubling its InP production capacity, and its factory in Sherman, Texas, is the most advanced InP production line globally, specifically scaling production of CW lasers for solutions including NVIDIA CPO.

The more Yi Zhongtian bets on architectural upgrades, the more it is expanding the territory for upstream American chip manufacturers. Therefore, what Yi Zhongtian earns is money from assembly and devices, while Coherent and Lumentum earn the money from chips. The latter is thinner, slower, yet more enduring.

This is also why everyone is linking "Yuanjie high-power lasers" with "Yi Zhongtian." Yuanjie Technology represents the efforts of domestic laser chips climbing upstream in the industry chain. Its 100G EML has passed customer verification in 2025 and is entering mass production in 2026, with the CW 100mW high-power light source also achieving bulk delivery, resulting in a year-on-year revenue growth of over three times in the first quarter. If this layer can truly break through at the critical points of EML and high-power laser chips, then Yi Zhongtian's moat will extend from assembly to chips, and the binding will become truly robust. If it cannot climb up, no matter how high the cost performance, it will only earn a hard-earned income.

This is the true hidden variable that measures the long-term cost performance of the three companies: whether the Chinese optical module industry can seize the profit pool from upstream.

Whether time will prove the optical modules and computing power remains unknown. But at least, those standing in the light should first clarify which beam they are standing in.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。