TL;DR

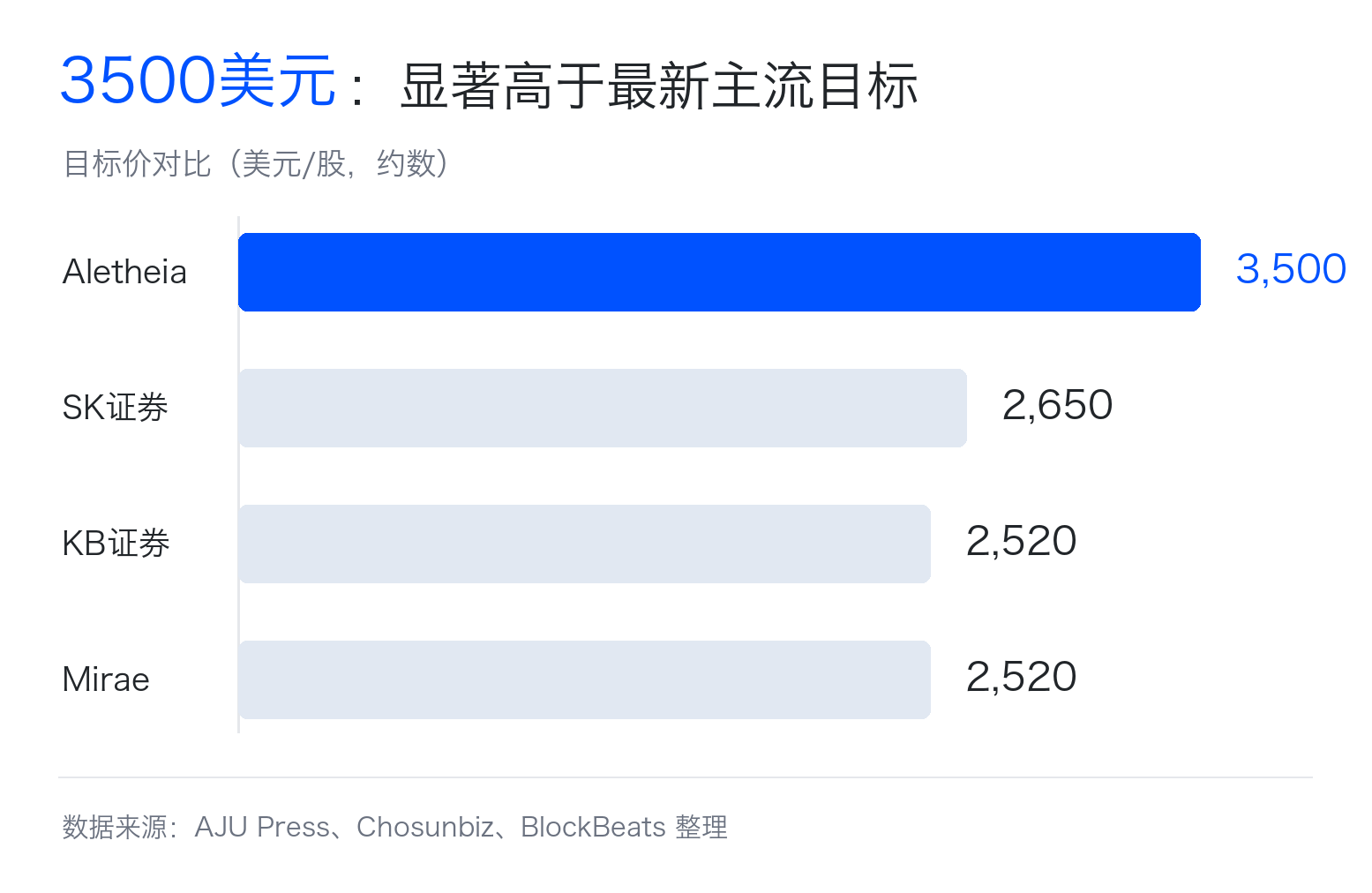

- Aletheia Capital raised the target price for SK Hynix to approximately $3,500, significantly higher than the target range of about $2,000 to $2,520 set by several mainstream institutions.

- The core of this pricing divergence is whether the market is willing to believe that the shortage of HBM, the increase in DRAM prices, and the improvement in free cash flow can continue until 2027.

- Related targets: SK Hynix, Samsung Electronics, Micron, NVIDIA supply chain.

Aletheia Capital released a report today raising the target price for SK Hynix to approximately $3,500, placing it significantly above the target ranges set by mainstream institutions.

Aletheia Capital is an independent research and investment consulting firm based in Hong Kong, targeting institutional investors and covering segments such as Asian technology hardware; in contrast, publicly reported target prices from SK Securities are around $2,000, and from Mirae Asset and KB Securities about $2,520.

The truly aggressive aspect of the $3,500 target price is not just its optimism compared to mainstream institutions, but rather its requirement that the market believes three things will happen simultaneously: HBM (High Bandwidth Memory for AI chips) will continue to be in short supply, regular DRAM prices will keep increasing, and the demand for AI servers will sustain the memory boom and free cash flow until 2027.

The market has already acknowledged that SK Hynix should be revalued, with the divergence lying in how far the revaluation can go; most mainstream institutions still retain a cyclical industry discount, while $3,500 continues to pull out an optimistic tail scenario after revaluation.

The divergence lies in the profit base for 2027

The $3,500 price can easily be misread as a simple valuation issue: just give SK Hynix a multiple of 10 times its 2027 profits or free cash flow, and the stock price can continue to rise. The difficulty does not lie in the multiple itself but in how much the company will actually earn by 2027 and how much cash it can retain.

Memory company's profits are highly volatile. During upturns, prices increase, inventories are sold off, and profit margins expand rapidly. During downturns, new capacity is released, customers cancel orders, and prices fall, potentially leading to a quick decline in profits. This is also why the market has long given memory companies lower valuation multiples.

Even with SK Hynix currently posting strong profits, the 12-month forward P/E ratio mentioned in public reports is still in the single digits. The market does not fail to see AI; instead, it worries that this upswing will ultimately still be priced according to cyclical peaks.

The aggressive target price circulated by Aletheia challenges this cyclical discount. According to public reports, it bets that AI hardware demand will continue to push up HBM and DRAM prices, that SK Hynix's free cash flow in 2027 will significantly exceed current expectations, and thus can be repriced with a higher base.

The problem is that the $3,500 price requires multiple variables to stand on the favorable side simultaneously: HBM prices must remain strong, regular DRAM prices must not be dragged down by new capacity, SK Hynix must maintain its leading share, capital expenditures must not consume too much cash, and the market must still be willing to give cyclical stocks a no-low multiple. Any one of these links falling short of expectations will turn the target price from structural revaluation into high boom extrapolation.

HBM transmits shortages to regular memory

HBM can change SK Hynix's pricing logic, as it is not just a small upgrade from regular memory, but a core component next to AI accelerator cards. No matter how fast AI chips compute, if data cannot be fed in, overall performance will also be bottlenecked. The role of HBM is to provide a higher bandwidth data channel for GPUs or AI accelerators.

Regular investors can understand it as: the GPU is the engine, HBM is the high-speed fuel supply system. The stronger the engine, the higher the requirements for the fuel supply system. In the past, the market first looked at NVIDIA GPUs when trading AI hardware. Now the market is increasingly aware that whether GPUs can be shipped and whether AI servers can scale also depends on HBM supply.

The supply of HBM cannot be simply expanded by slightly modifying regular DRAM production lines. It requires more complex stacking, packaging, and customer certification, and consumes more wafer area and advanced packaging resources. Producing an equal capacity of HBM often takes up more capacity resources than standard DRAM.

This impact will also spread to regular memory. When manufacturers divert more resources to make HBM, the supply of DRAM used in servers, PCs, and mobile phones will tighten, and the average selling price of DRAM may also rise.

This is the core mechanism that can explain the approximately $3,500 target price. If HBM is just a fast-growing small product, it can only boost a part of SK Hynix's revenue. If HBM simultaneously squeezes the supply of regular DRAM and raises the entire memory price curve, it will become a magnifier for the company's overall profit margin and cash flow.

However, the shortage of HBM can only prolong the cycle, not eliminate it. Samsung and Micron are catching up, and SK Hynix itself will also expand production; new wafer fabs and packaging capacity will ultimately reflect on the supply side. The core of the controversy is not whether there is a shortage, but how long the shortage can last and how strong the prices can remain.

SK Hynix benefits directly from supply chain premiums

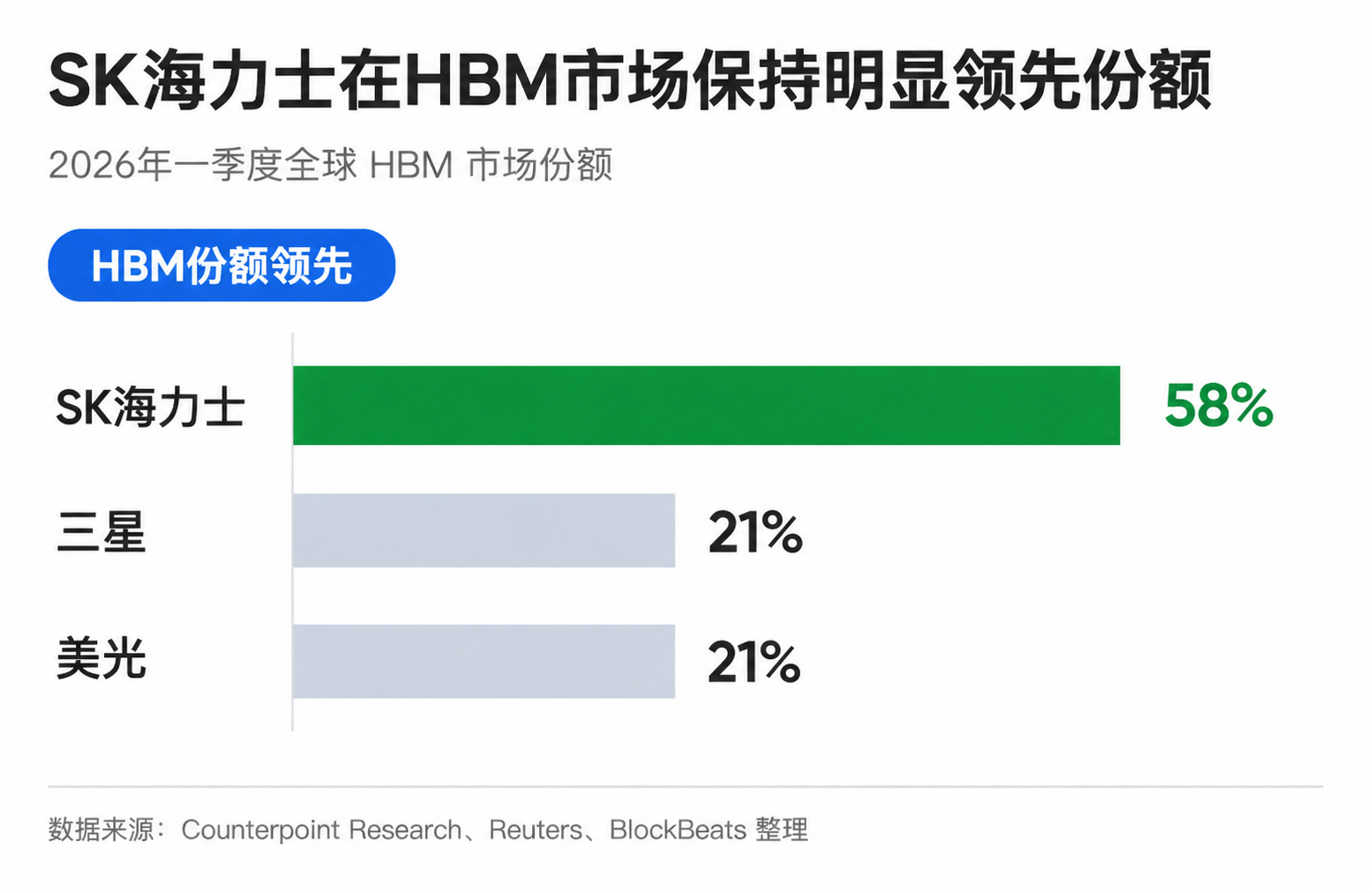

SK Hynix has become the core of this revaluation, not only because it is a memory company but also because it is the fastest runner in HBM. According to Reuters' report on Counterpoint data, SK Hynix held about 58% of the global HBM market share in Q1 2026, while Samsung and Micron each accounted for about 21%. Reuters has also referred to it as an important supplier in NVIDIA's HBM supply chain.

This lead is very valuable in the semiconductor supply chain. AI chip manufacturers choose HBM not only based on price but also on performance, yield, stability, and certification progress. The sooner they pass customer certification, the easier it will be to enter the collaboration window for the next generation of products. The sooner they secure orders, the easier it will be to gain the initiative in capacity planning and price negotiations.

This is also why the visibility of supply and demand for 2026 is receiving attention. According to a Reuters report in 2025, SK Hynix has completed discussions for 2026 HBM supply with key customers. Multiple industry reports also indicate that the HBM shortage may continue into 2027. For investors, the performance in 2026 is at least not completely supported by the story.

The benefits for SK Hynix are not limited to HBM revenue itself. Because HBM occupies more capacity, the supply of regular DRAM is squeezed, and traditional memory business may also benefit from price increases. AI demand first enters the financial statements through HBM and subsequently affects the entire DRAM price through capacity redistribution.

This explains why institutional target prices are continually revised upward. Even if they do not accept the extreme scenario of $3,500, the target price range of approximately $2,000 to $2,520 also indicates that mainstream institutions are already recalculating SK Hynix's profit elasticity for 2026 to 2027. The difference is that most still retain the appropriate cyclical industry discount and have not directly extrapolated the shortage after 2027 into a new normal.

A doubling in price requires three conditions to be met

The $3,500 target price circulated by Aletheia essentially bets on continuing strong demand, tight supply, and cash flow exceeding expectations. Over the past two years, cloud companies and AI firms have massively procured GPUs, driving explosive demand for HBM; the next thing the market needs to watch is whether inference, enterprise AI, and custom ASICs can continue to expand memory consumption, so that demand is not limited to training clusters.

On the supply side, it cannot loosen too quickly either. The tightness in 2026 is relatively easy to understand, as capacity, packaging, and customer certification all have lags; by 2027, new capacity and new products from Samsung, SK Hynix, and Micron will gradually enter the market. If the new supply outpaces expectations, the price increase for HBM may narrow, and regular DRAM will also face renewed pressure.

Ultimately, it still comes down to cash flow. When the memory industry is in an upturn, companies often increase capital expenditures to expand production, upgrade processes, and lay out advanced packaging. Profit growth does not necessarily remain fully on the books; if SK Hynix needs to invest more to maintain its lead, the free cash flow base that the $3,500 target price relies on will be weakened.

Therefore, this target price is better seen as an optimistic scenario rather than a validated market consensus. 2027 is the real observation window: as long as HBM prices, average DRAM prices, supply rhythms, and free cash flow continue to stand on the favorable side, the market will believe that AI is raising the profit center of the memory industry; if prices first soften, supply arrives early, and cash flow is consumed by capital expenditures, the approximately $3,500 will turn from a revaluation anchor into an emotional peak.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。