Original Author: Jia Liu

Will copper become another type of gold in this era?

In the past two years, the market has understood AI infrastructure as a chip story. NVIDIA’s GPUs, TSMC's production capacity, HBM yield rates, and CoWoS packaging bottlenecks have dominated almost all discussions surrounding silicon. However, AI data centers cannot simply run by buying GPUs and plugging them in. They also require grid access, transformers, bus ducts, cables, liquid cooling systems, fiber optic interconnections, and a significant amount of metal.

In the previous article titled The "Great Famine" Moment of Fiber Optics and Copper in the AI Era, we briefly discussed one thing: the demand for AI is shifting from chips to fiber optics and copper.

This article will delve deeper into the changing narrative of copper this year. Why does the market feel that copper is increasingly resembling gold? Why are macro funds beginning to buy copper? Why are mining companies and commodity traders saying, "there is not enough copper"? Why is it no longer just the industrial metal used to gauge economic cycles?

Dr. Copper is no longer just a reflection of the manufacturing cycle

In English financial markets, there is an old saying called Dr. Copper, which Chinese financial media sometimes translates as "Copper Doctor." The name implies that copper prices act like an economic doctor, capable of diagnosing the global economy’s ups and downs in advance.

This is because copper prices are intertwined with manufacturing. When there is significant construction in China's real estate sector, manufacturing stock replenishment occurs, and the demand for household appliances, cars, cables, and pipes rises, copper prices increase. As the cycle declines, copper mirrors this drop. Essentially, copper prices are a reflection of China's real estate, global manufacturing, and trade cycles.

However, today copper's demand has new influencing factors: AI data centers, grid expansion, new energy vehicles, energy storage, military industry, and re-industrialization are all increasing structural demand for copper.

Wherever electricity is needed, copper is indispensable.

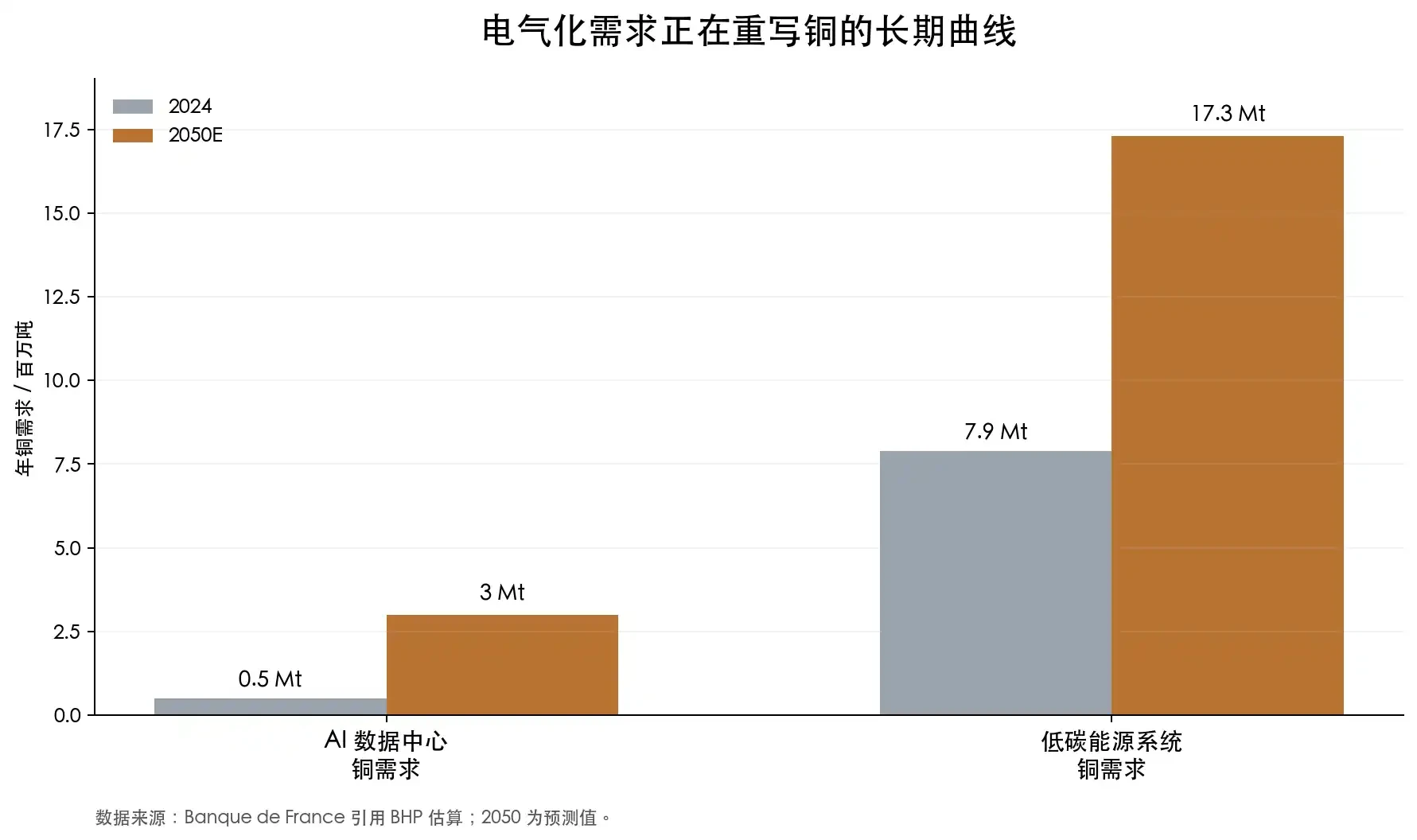

The Banque de France, in an analysis about AI data centers and the copper market, quoted an estimate from BHP: AI data center copper demand could grow from about 500,000 tons in 2024 to approximately 3 million tons by 2050. During the same period, the demand for copper in low-carbon energy systems could rise from 7.9 million tons to 17.3 million tons. The article also cited a specific case: Microsoft's Chicago data center construction consumed 2,177 tons of copper.

Looking at this number alone, it is not particularly large in the global copper market. But the point is not about how much copper a specific data center uses; rather, the demand for AI data centers is not a singular need but an entire set of electric power infrastructure requirements. The denser the GPUs, the higher the power of the cabinets, the more data centers resemble high-energy-consuming factories. Factories need electricity, and for electricity, they require grids, transformers, cables, busbars, switchgear, and cooling systems.

Of course, not all stories about copper can be simply attributed to AI.

Richard Holtum, CEO of global commodity trading giant Trafigura, pointed out at the 2025 LME Week that while data centers and defense are indeed hot, the majority of copper demand in the next decade will still come from traditional infrastructure, construction, urbanization, and consumer goods. He also noted that back in the day, copper used for air conditioning still exceeded that for data centers.

This viewpoint provides us with a new perspective: the increase in copper demand is not solely supported by AI as a single factor; rather, its demand is expanding across almost all electricity-related scenarios.

The biggest bullish logic for copper is that it cannot be mined quickly

Many people's first impression of copper is "industrial metal," believing that as long as prices rise, more mining will occur, and supplies will naturally increase. However, the reality is different.

Large copper mines take about a decade or more from discovery, exploration, resource confirmation, feasibility studies, financing, permissions, construction to operation. The IEA’s report shows that new copper projects take an average of about 17 years to go from discovery to production. This means that if the market suddenly realizes in 2026 that there is not enough copper, new large-scale supplies may not materialize by 2028 or 2029—most supplies would have to wait until the 2030s.

Robert Friedland, founder and co-executive chairman of Canadian mining company Ivanhoe Mines, repeatedly emphasizes this point. He is one of the world's most famous copper bulls, owning the world-class copper project Kamoa-Kakula in the Democratic Republic of Congo. His expression has always been quite aggressive: the world has not yet realized how much copper it actually needs. Over the past decade, the globe has not prepared enough new copper mines for the electrification era.

This is not just his judgment. Data from the IEA also supports this direction.

Since 1991, the average grade of global copper mines has declined by about 40%. A decline in grade means that in the past, one ton of ore yielded more copper; now more ore must be extracted, more electricity used, more water consumed, and more waste rock handled to obtain the same ton of copper. The IEA also noted that only 5% of the copper deposits discovered in the past 35 years appeared in the last decade. With fewer new discoveries and depleting grades in existing mines, longer project construction cycles, and increasing capital expenditures, the IEA estimates that, based on the current project pipeline, the copper market could face a 30% supply gap by 2035.

Therefore, copper is not an asset that exhibits the normal cycle of "supply immediately comes online after a price increase." Copper mining projects increasingly resemble large infrastructure projects: searching for mines, obtaining permits, managing community relations, addressing water resources, facing environmental reviews, and enduring changes in resource country taxation policies.

Chile, Peru, the Democratic Republic of Congo, Zambia, Indonesia, and Mongolia are all places with significant copper resources but also have various forms of political, tax, community, or operational risks. The more strategic copper is, the more motivating it is for resource countries to increase their shares; the higher the copper price, the easier it is for mining companies to face tax increases and renegotiate deals.

The smelting side is also showing stress.

After copper concentrates enter smelters, they are processed into refined copper. The fees charged by smelters to mines for processing and refining, known in the industry as TC/RC, represent treatment charge and refining charge. Normally, when concentrate supplies are abundant, smelters have strong bargaining power, resulting in high TC/RC; when concentrates are tight, smelters scramble for raw materials, leading to a drop in TC/RC.

In 2026, one unusual point is that while copper prices reached new highs, smelting processing fees dropped to historic lows. The IEA states that the annual TC/RC benchmark for 2026 fell to zero dollars per ton, while spot TC/RC has been negative since 2024.

This is more crucial than simply looking at exchange inventories because the bottleneck for copper is not only in refined copper products but also in mines and concentrates. If upstream raw materials are tight, having more smelting capacity does not help. China has significantly expanded its copper smelting capacity over the past twenty years, with the IEA stating that China accounted for over 90% of the global copper smelting capacity growth since 2005, and by 2025 it will account for about half of global copper smelting output. With strong midstream capacity and tight upstream mines, the vulnerabilities in the supply chain are magnified.

The scarcity of gold comes from reserves, extraction costs, and monetary attributes. Copper is certainly not gold, but as its new supply slows, resources become more concentrated, and its strategic attributes strengthen, it starts to possess a sense of scarcity similar to gold.

Why macro funds have begun to favor copper

Copper used to primarily belong to commodity traders and mining analysts. Now, it increasingly attracts macro funds.

For example, Stanley Druckenmiller, one of America's most well-known macro investors, previously managed the Quantum Fund with Soros and later founded Duquesne Family Office. His characteristic is to focus on large cycles and heavily invest in high-conviction trades, so the market pays close attention to his views on AI, the dollar, bonds, and commodities.

Recently, in an interview with Morgan Stanley, he mentioned that his portfolio had been primarily driven by AI in the past few years but has now shifted towards a more macro and geopolitical positioning. He mentioned holding copper, being bearish on the dollar, and also holding gold as a geopolitical hedge.

His logic is: if the dollar weakens, commodities priced in dollars will benefit. With an expanding fiscal deficit, continued government spending, and rising geopolitical risks, there is buying demand for gold; in the same environment, the return of electricity, military, AI data centers, energy systems, and manufacturing will also increase demand for physical assets, with copper sitting at the intersection of these directions.

Druckenmiller represents the perspective of macro funds, while the commodity trading circle has even more aggressive expressions.

Pierre Andurand is one of the most typical examples. He is a well-known European commodity hedge fund manager who started in energy trading, co-founded BlueGold Capital, and later established Andurand Capital. In an interview with the Financial Times, he made very aggressive predictions: copper prices could surge to $40,000 per ton in the coming years.

Jeff Currie’s perspective is also noteworthy. He served as the global head of commodities research at Goldman Sachs for a long time and later joined Carlyle, becoming one of the most influential figures in Wall Street commodity research. He has long posited that "copper is the new oil," meaning that in the era of energy transition, copper could play a foundational role similar to that of oil in the era of old energy. In 2024, he again referred to copper as one of his highest conviction trades.

Data also shows that funds are flowing in.

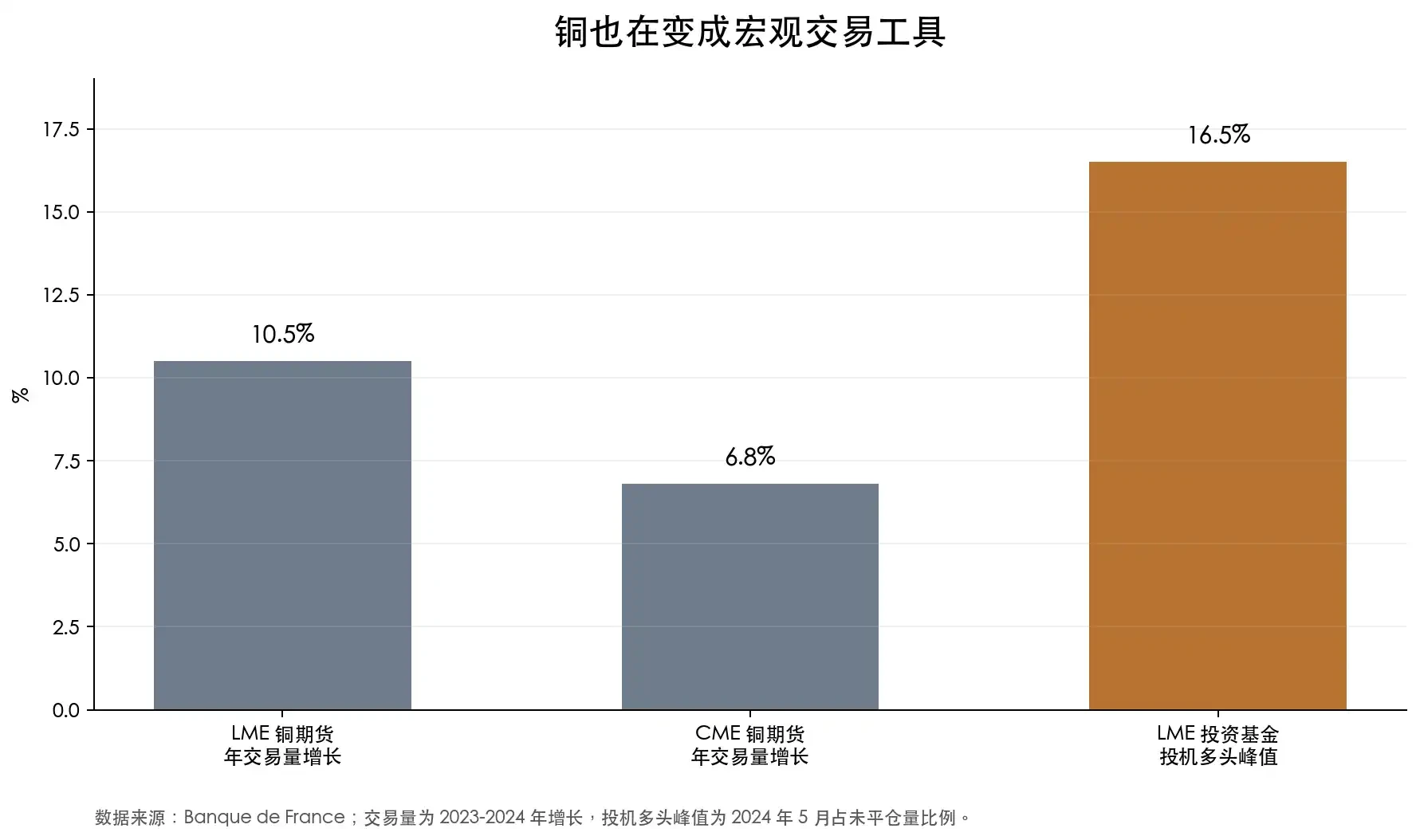

The Banque de France mentioned that from 2023 to 2024, the annual trading volume of LME copper futures increased by 10.5%, and the annual trading volume of CME copper futures rose by 6.8%; within LME copper futures, speculative long positions held by investment funds reached an open interest of 16.5% in May 2024. This is not merely simple physical replenishment but indicates that financial capital is treating copper as a macro trading tool.

Copper mining stocks: The leverage of copper

In a bull market for gold, gold stocks typically amplify price fluctuations. In a copper bull market, copper mining stocks exhibit a similar amplification property.

Rising copper prices create cost pressures for end-users, but for mining companies that already have capacity, it might lead to margin expansion. For instance, if copper prices rise from $9,000 to $12,000 per ton, and the cash costs for the mining company do not increase accordingly, a large part of the additional $3,000 will directly enter the profit statement. For this reason, copper mining stocks inherently possess operational leverage. When copper prices rise, mining company profits may increase even more; when copper prices fall, profits will also contract more quickly.

The market has already traded this leverage over the past two years.

Taking A-shares as an example, from June 2024 to June 2026, Luoyang Molybdenum is the most typical high-elasticity sample. Its core highlight is the copper-cobalt assets in the Democratic Republic of Congo, especially Tenke Fungurume and KFM. Based on adjusted closing prices, Luoyang Molybdenum's range increase over these two years is approximately 129%, peaking at nearly 260%. This is not the performance of a typical cyclical stock but rather the market re-pricing overseas copper mining resources.

Companies like Jiangxi Copper, Tongling Nonferrous, and Yunnan Copper more clearly reflect the combined volatility of copper prices and smelting attributes. Jiangxi Copper has had a range increase of about 82%, peaking over 200%; Tongling Nonferrous has had a range increase of about 77%, peaking at approximately 159%; Yunnan Copper had a range increase of only about 29%, but its peak increase also exceeded 130%.

These stocks all showcase another side of copper mining stocks: when the market is favorable, the elasticity is substantial; when the market pulls back, the retraction can also be severe.

Looking at retraction from peak values shows this volatility more intuitively. Yunnan Copper retracted about 45% from peak values, Jiangxi Copper retracted about 41%, and Luoyang Molybdenum, Northern Copper, and Zijin Mining also each had retractions of over 30%. Copper mining stocks are not copper prices themselves, but the result of copper prices, costs, inventory, TC/RC, project progress, resource country risks, and equity market sentiment all interacting together.

In the U.S. stock market, the most representative copper mining stock is Freeport-McMoRan, with the ticker FCX. It is one of America’s core copper producers and owns assets including Morenci in the U.S., Cerro Verde in Peru, and Grasberg in Indonesia. For global funds, FCX is one of the most commonly used U.S. stocks for gaining exposure to copper prices. MarketWatch data indicates that FCX hit a 52-week high of $72.09 on June 2, 2026, but dropped 9.07% on June 5, retracting over 12% from its peak within just a few days.

Southern Copper, ticker SCCO, is another high-quality copper mining stock representative. Its assets are primarily in Peru and Mexico, have high copper exposure, and strong profitability. Earlier this year, IBD noted that SCCO had once risen 55% within the year, creating a historical high. Compared to FCX, SCCO resembles higher purity, better profitability copper mining assets, but it also cannot escape risks associated with copper prices and resource countries.

If investors do not want to bet on a single company, they can also look at copper mining ETFs, such as the Global X Copper Miners ETF, which tracks global copper mining companies.

However, copper mining stocks are far more complex than copper itself.

The value of a mining company depends not only on copper prices but also on mine quality, cash costs, lifespan of reserves, capital expenditures, the country in which it operates, tax policies, labor relations, environmental permits, transportation conditions, and management execution capability. Copper prices can elevate the valuations of an entire sector, yet significant differentiation among companies will ultimately emerge.

Resource country risks are especially critical. Many high-quality copper mines are located in Chile, Peru, the Democratic Republic of Congo, Zambia, Mongolia, and Indonesia. Good resource endowments do not equate to stable shareholder returns. The more valuable copper becomes, the more governments will recalibrate their share; the larger the project, the more complicated issues become in managing communities, environmental concerns, water usage, and infrastructure.

Cost inflation can also erode profits. When copper prices rise, energy, equipment, labor, steel, and financing costs often increase simultaneously. A project that appears attractive might ultimately leave little profit for shareholders due to overruns in capital expenditure, production delays, or permit obstacles.

Early-stage copper mining companies have higher risks. They focus on future reserves and yields, but every step from resource estimation to extractable reserves, from feasibility to financing, from permitting to construction can potentially fail. The long-term logic around copper holds true, but that does not guarantee every copper mining stock will realize it.

Thus, copper mining stocks are better understood as leveraged expressions of copper price logic rather than simple substitutes for copper prices themselves. They can provide higher elasticity, but they can also cause larger drawdowns. What is truly worth studying are companies with low costs, long lifespans, clear expansion pathways, sound balance sheets, and controllable political risks.

This is also part of the "goldenization" of copper: the logic of copper's scarcity is not limited to the spot and futures markets; it is being re-packaged by the stock market, ETFs, and speculative funds. Rising copper prices represent one layer of trading, while rising copper mining stocks represent another layer of trading. The former reflects the commodity itself, while the latter reflects how much imagination the market is willing to pay for this long-term scarcity.

The "goldenization" of copper has only just begun

This world needs more electricity, and more electricity means more copper.

Of course, copper will not truly become gold. It does not possess the pure monetary attributes of gold, nor can it escape economic cycles. Global economic slowdowns, weakening manufacturing, and risk asset cooling will all suppress copper prices. Copper will continue to fluctuate, and may even experience severe volatility.

But the change lies in the fact that the underlying logic of copper has shifted from the past.

Historically, significant drops in copper prices often occurred during periods of weakening demand coupled with oversupply. Today’s supply side is not as loose. With aging mines, declining grades, extended permitting cycles, smelters scrambling for raw materials, and resource countries redistributing benefits, these factors make it increasingly difficult to treat copper as just an ordinary cyclical commodity.

It may still be an industrial metal, but it is no longer merely a reflection of the industrial cycle.

The "goldenization" of copper has only just begun.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。