This week in the global market, the main focus is on Japan's interest rate hike and the Federal Reserve meeting. For risk assets, this week is destined not to be gentle.

Three months ago, Wall Street was still discussing when to cut interest rates. Waller had just taken office, and the market was willing to give the new chairman a chance; inflation was declining, employment was easing, and a rate cut seemed just a matter of time. But that's the fickle nature of the financial world; the script everyone had anticipated was never used.

In May, the CPI rose 4.2% year-on-year and 0.5% month-on-month, with energy prices up 3.9% month-on-month, while core CPI remained near 2.9% year-on-year. Employment didn’t give the Federal Reserve an immediate reason to pivot dovish either, with 172,000 non-farm jobs added in May and the unemployment rate holding at 4.3%. This means the Federal Reserve is currently facing an awkward combination: inflation is rising again, employment is not showing a significant collapse, AI-related investments continue to support economic resilience, the reasons for rate cuts are diminishing, but the conditions for rate hikes are slowly accumulating.

Meanwhile, the Bank of Japan will hold a policy meeting on June 15-16, and the market has almost priced in a 25 basis point rate hike as the base case. Polymarket's odds for the "Bank of Japan Decision in June" show a probability of about 98.3% for a 25bp hike, only about 1.45% for no change, and about 0.55% for a hike of more than 50bp.

Many people should still remember that previous rate hikes in Japan have had a significant impact on the overall financial market. This week, facing Japan's rate hike on Tuesday and the Federal Reserve's FOMC meeting on Thursday, will the market decline?

Waller's "Debut," Federal Reserve Rate Hike Probability Increases

Let's first look at the Federal Reserve's side.

The possibility of a rate cut seems to have been mostly closed off. Polymarket's pricing shows a probability of about 70.35% for "no rate cuts in 2026," approximately 2.35% for "rate cuts before July," and only about 23% for "rate cuts before December." Seventy percent are betting there won't be a cut this year. In the year-end interest rate corridor, maintaining a 3.75% upper limit has a probability of about 37%, 4.00% about 32.5%, 4.25% about 11.25%, and 4.50% and above about 3.35%, with a total of about 47% for over 4.00%.

The market consensus regarding Waller is that during his debut at this week's FOMC meeting, it is very unlikely he will initiate a rate hike. The risks of a rate hike are primarily concentrated in the third quarter and beyond. Several Polymarket odds clearly illustrate this consensus:

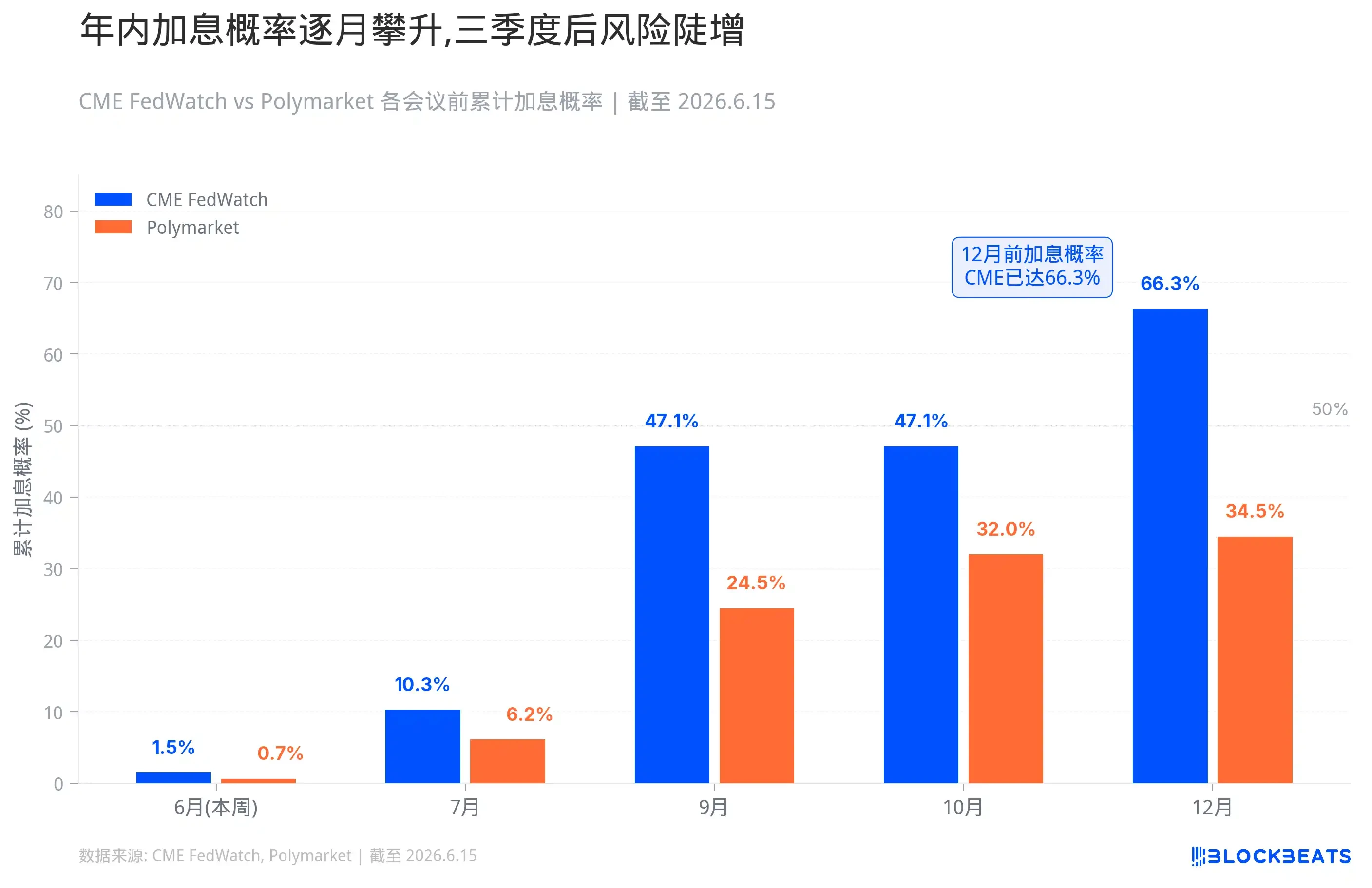

"Fed rate hike in 2026?" shows a probability of about 34.5% for a hike anytime in 2026; "Fed rate hike by...?" shows approximately 0.65% before June, about 6.15% before July, about 24.5% before September, and about 32% before October; in "Fed Decision in July," a 25bp hike in July has a probability of about 3.15%, more than 50bp about 0.3%, and no change about 93.5%; in "What will the Fed rate be at the end of 2026?" the probability of the year-end rate cap at 3.75% is about 37%, 4.00% about 32.5%, 4.25% about 11.25%, and 4.50% and above about 3.35%.

Looking at the more specific probabilities and data, the probability of a rate hike before July 29 is about 10.3%, before October 28 about 47.1%, and before December 9 about 66.3%. Polymarket is even more conservative, showing 34.5% for "Fed rate hike in 2026," about 24.5% before September, and about 32% before October. The probabilities for this month have CME FedWatch showing a 98.5% probability for no change, and Polymarket showing 99.55%.

The U.S. is very likely to remain on hold this week, but "not taking action" and "not tightening" are two different matters.

If Waller acknowledges in the press conference that inflation risks have resumed overshadowing growth concerns, and if the dot plot shifts the 2026 interest rate midpoint from a cutting direction to flat or even up, and if the wording suggesting a "bias towards rate cuts" is removed, the market will tighten on its own in response to the Federal Reserve.

The first to react will be short-term U.S. Treasuries. The yield on 2-year and 1-year notes will directly follow the Federal Reserve's path; once the market shifts from "rate cuts later" to "possible rate hikes later," short-term yields will rise. The dollar will also be supported, as a strong dollar is itself a form of global tightening.

In U.S. equities, high-valuation growth stocks and long-duration AI assets are the most sensitive. The higher the interest rates, the less valuable future cash flows become, financing costs increase, and the market becomes increasingly unwilling to pay a premium for stories that haven’t yet materialized. Logic for small-cap stocks, micro-cap stocks, and unprofitable tech stocks is even more fragile; these companies rely on cheap money, and once cash isn’t cheap anymore, valuations will collapse first.

If a real tail event occurs, and with the 98.5% "no change" pricing, if the Federal Reserve directly hikes rates, the impact will be very severe. Short-term rates will spike, the dollar will surge, and leveraged positions will be forced to reduce risk. It’s not guaranteed to happen, but the meaning of such probability is that if it does occur, no one will have time to react.

After all, the importance of Waller's "debut" has been amplified by the market, and another significant factor is that he may change the Federal Reserve's communication style. Long-time watchers of the Federal Reserve, like Timiraos, have made it very clear: for Waller, symbolic adjustments such as the dot plot, statement wording, and the timing of press conferences can be quickly made, but truly changing the Federal Reserve's communication system requires long-term persuasion and internal collaboration. This week's meeting may be the first step.

Across the Pacific, Japan's Rate Hike "Curse"

Let's look at Japan; the Bank of Japan will hold a meeting on June 15-16, with Polymarket giving a 98.3% probability for a 25 basis point rate hike. If implemented, the policy rate will rise from 0.75% to 1%, the highest since 1995.

The logic that has forced Japan to this point is quite straightforward. Middle Eastern conflicts have driven up oil prices; Japan is a typical energy importer, and the weak yen has further amplified import costs. Wages are rising, service prices are increasing, and inflation expectations are starting to loosen. If low interest rates continue, the market will question whether the Bank of Japan even cares about inflation anymore.

The rate hike itself is not in suspense, but a significant concern is that over the past few years, a large amount of global funds have been converted from low-yielding yen into dollars or other high-yield assets, purchasing U.S. Treasuries, stocks, and credit, with some indirectly entering higher volatility risk assets. This structure is built on one premise: that Japanese interest rates are low enough, yen financing is cheap enough, and the central bank is slow enough. In other words, if the market believes that the normalization of Japanese interest rates is continuous, the carry trade will become fragile, yen shorts will be squeezed, and global leveraged funds will begin to contract.

The market's fear of Japan's rate hike is not unfounded. Over the past two decades, every time the Bank of Japan has attempted to raise rates from near zero, global markets have nearly always encountered issues.

The first instance was in August 2000. The Bank of Japan raised rates from zero to 0.25%, coinciding perfectly with the peak of the U.S. internet bubble. Within three months after the rate hike, the Nasdaq dropped 35%. The Japanese economy couldn't withstand it either, quickly slipping back into recession, forcing the Bank of Japan to lower rates back to zero in 2001.

The second instance was from 2006 to 2007. The Bank of Japan raised rates to 0.5% in two steps, the first in July 2006 and the second in February 2007. This timeline almost perfectly corresponds to the period of brewing for the U.S. subprime mortgage crisis. In the summer of 2007, the U.S. subprime crisis began to explode, and in 2008 Lehman collapsed, triggering a global financial crisis. The Bank of Japan was once again forced to lower rates back to zero.

The third instance occurred on July 31, 2024. The Bank of Japan raised rates from 0% to 0.25%, a very small increment, but the market reacted extremely. On August 5, the Nikkei 225 plummeted 12.4% in a single day, marking the largest drop since the Black Monday of 1987. The Korean KOSPI triggered a circuit breaker, and the Nasdaq and S&P 500 dropped 3.4% and 3%, respectively. The VIX volatility index spiked above 65. The transmission mechanism of that crash was clear: the Bank of Japan's rate hike triggered a sharp rise in the yen, forcing the liquidation of carry trades financed by yen to buy overseas assets, leading to collective sell-offs and a stampede. To meet margin calls, fund managers even sold off "safe-haven assets" like gold and BTC. Under the liquidity crisis, all assets’ correlations approached 1. The market's horrific state that day is still fresh in my memory.

Therefore, what matters more is what kind of hints the Japanese government will provide at tomorrow's press conference: how high will the rates actually rise?

U.S. Stocks, U.S. Treasuries, Bitcoin—Who is Most at Risk This Week?

As previously mentioned, the performance of global markets during the last three rate hike cycles by the Bank of Japan mostly saw declines.

However, the Bank of Japan's rate hike itself does not necessarily lead to a crash; crashes generally happen when other fragile leverage is present. For instance, in 2000 and 2007, it coincided with larger bubbles in other countries. August 2024 faced an unexpected situation where the market was too heavily positioned to react in time. Subsequent times, the market had preparation, and there were no incidents.

This time, the 25 basis points are already priced into the market at 98.3%, leaving almost no room for surprises. According to experiences from December 2024 and January 2025, the rate hike itself will likely be smoothly digested. However, there are two additional variables this time.

The first concern is that Governor Ueda has been hospitalized due to a liver condition and is expected to miss this meeting and the following press conference. According to public reports, Deputy Governor Ishi is expected to act as meeting chairman, while Deputy Governor Uchida will host the post-meeting press conference. This arrangement will likely not change the direction of the rate hike. However, the market is not as familiar with Uchida's communication style compared to Ueda, and the volatility in interpreting statements could be amplified. A statement of "future decisions will depend on data" versus "there is still room for interest rate normalization" may seem similar, but for traders, they convey entirely different signals.

The second concern is that both the Bank of Japan and the Federal Reserve have meetings in the same week. The Bank of Japan's decision and the FOMC meeting are only a day apart. If the Bank of Japan raises rates and the market reacts calmly, but the next day, Waller is hawkish in his press conference, that two-layer pressure will compound. Conversely, if the Bank of Japan's rate hike causes the market to become tense, and then Waller adds fuel to the fire, short-term sentiment may overreact. The scheduling of two central banks' announcements back-to-back inherently amplifies volatility.

Let’s analyze each asset one by one:

U.S. Treasuries are likely to be the first to respond this week. Short-term yields will directly follow the Federal Reserve’s path, with 2-year and 1-year notes being the most sensitive. If Waller's press conference is hawkish and the dot plot shifts upward, short-term yields will rise, reflecting a re-pricing of the market for "later rate cuts" or even "rate hikes within the year." The long-term situation is more complex; the 10-year yield may not rise in tandem. If the market begins to worry about high rates harming the economy, the yield curve may further flatten or deepen its inversion. On the Japanese side, if Uchida hints at continued rate hikes, Japanese government bond yields will also rise, and any marginal loosening of Japan's substantial $1.13 trillion U.S. Treasury position could further affect the U.S. Treasury market's supply and demand.

The dollar is likely to be supported. A hawkish Federal Reserve stance will push up expected yields on dollar-denominated assets, strengthening the DXY. A rate hike from the Bank of Japan should theoretically benefit the yen and harm the dollar, but the actual direction will depend on the statements: if the Bank of Japan hikes and then signals dovish, the yen may not only not rise but actually fall, potentially strengthening the dollar index. With both central banks meeting in the same week, the relative movements of the dollar and yen will be very sensitive, and FX market volatility will likely increase. Asian currencies and emerging market currencies will be under pressure; a strong dollar itself is a form of global tightening that will draw liquidity away from overseas dollar markets.

In U.S. stocks, differentiation will be very pronounced. High-valuation growth stocks, long-duration AI assets, small-cap stocks, micro-cap stocks, and unprofitable tech stocks are the most vulnerable. The higher the interest rates, the less valuable future cash flows become; financing becomes more expensive, and the market becomes increasingly unwilling to pay a premium for stories that remain unfulfilled. The Russell 2000 and companies relying on cheap capital will bear the brunt. The reaction of bank stocks may be more complicated; short-term interest margins may benefit, but if the curve continues to invert and credit risks rise, it may not be a good thing. Defensive stocks will hold up relatively well, but utility stocks and REITs, considered "bond-like assets", will also have their valuations compressed by high rates. The S&P 500 closed last Friday around 7382 points, and the Nikkei 225 around 66078 points; if both central banks lean hawkish this week, U.S. stocks and Japanese stocks will face pressure, particularly indices with significant tech weighting.

The situation for Japanese stocks is somewhat special. A rate hike by the Bank of Japan is indeed bad news for Japanese export companies, as a stronger yen will erode overseas profits. However, if the scale and pace of the hike are within expectations, Japanese stocks may not necessarily crash, as experiences from December 2024 and January 2025 suggest. The real risk lies in the post-meeting communication; if Uchida implies that normalization will continue, the Nikkei may initially drop before reassessing.

Gold will be pulled by two forces. Rising real rates and a stronger dollar typically weigh on gold, but if the reasons behind the rate hike are energy shocks, geopolitical risks, and uncontrolled inflation, demand for safe havens may support gold prices. This week, gold is likely to experience high-level fluctuations, with direction depending on whether the market is more afraid of rising rates or uncontrolled inflation. Crude oil is more impacted by supply-demand dynamics and geopolitical factors; conflicts with Iran continue to brew, and if the rate hike stems from oil price increases pushing up inflation, oil prices may not immediately fall. However, if the market starts trading on expectations of slowing demand, industrial metals and oil may face downward pressure.

Credit bonds and real estate are slower variables, but the direction is clear. High-yield spreads will widen, financing costs will rise, and sensitive assets like commercial real estate, REITs, and mortgage-sensitive assets will be under pressure. Emerging markets with high exposure to dollar-denominated debt will also find it more challenging, as capital outflow pressures will increase.

The crypto market is also under pressure in this macro backdrop. BTC is currently around $65,000, down from $72,000 in early June; after the CPI announcement, it dropped to about $61,500 and has only just rebounded in the past few days. This price level itself is unstable; when it fell below $62,000 on June 5, over $1.5 billion in long positions were liquidated, and there was a net outflow of $2.7 billion from Bitcoin spot ETFs in one week. Although prices have rebounded somewhat, the position structure is not healthy. BTC carries some macro asset attributes, and while it may not necessarily collapse with rising rates, it is also hard to strengthen independently. ETH, SOL, altcoins, meme coins, and small-cap coins are even more fragile; these assets thrive on liquidity spillover and risk appetite, and once the market begins to reassess the attractiveness of returns from cash, short-term bonds, and money market funds, high beta assets will be the first to be cut. Funding rates in the derivatives market have already declined, and on-chain risk appetite has cooled, with an earlier occurrence in early June.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。