Currently, basically, the four major investment banks in the United States have unanimously set the tone, optimistic about the future growth of MLCC. Morgan Stanley's recent major research report has a core conclusion in one sentence: This round of supply and demand tightness for MLCC is the strongest in history, without exception! 🔥

Let me break it down simply and see what JP Morgan has to say:

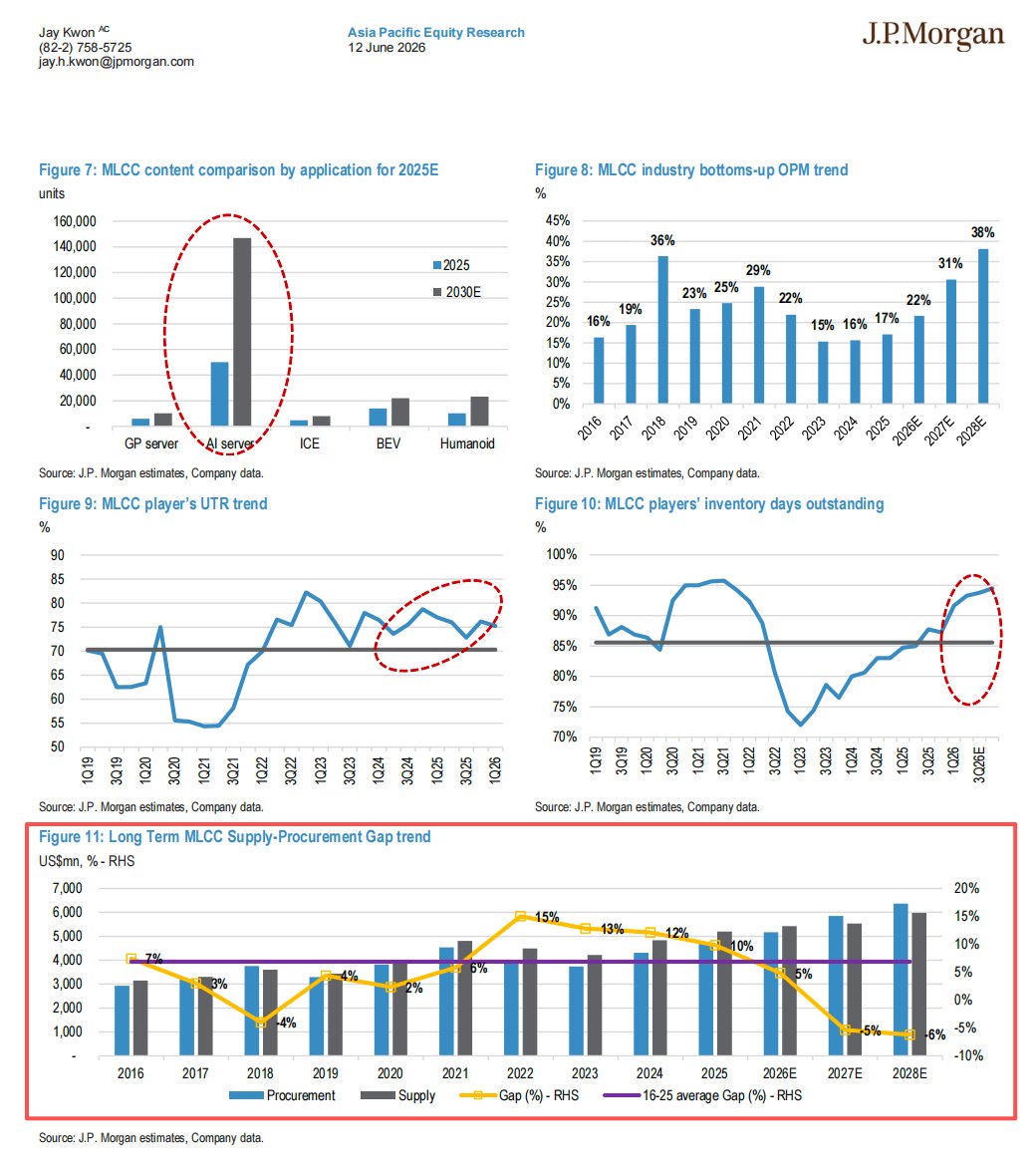

📊 How exaggerated is the supply-demand gap?

• 2025-2028 cycle: from 10% surplus → 2028 6% shortage → shortage further widens later.

• This level of tension is even fiercer than the passive components supercycle of 2017-18.

• JP Morgan predicts a growth potential of up to 50% ASP (similar to the increase during the 2016-18 cycle).

• Industry OPM will rise from 36% in 2018 to 38% in 2028.

💡 Why is it so tight? Two core drivers:

1️⃣ Explosive growth in AI server TAM, the MLCC usage per server is several times that of traditional servers

2️⃣ Capacity bottlenecks are severely underestimated, which is crucial!

JP Morgan points out a fact overlooked by the market: MLCC capacity cannot only be looked at from the perspective of nominal capacity growth (approximately 10% annualized over the past decade), but must consider effective capacity.

What does this mean?

• AI servers require ultra-high specification MLCC (such as 1005-47uF ultra-high capacitance)

• The yield for these high-spec products is lower, power consumption is higher, and assembly difficulty is greater

• Resulting in actual output being far below theoretical capacity

• Capacity losses are accelerating, and the impact over the next three years will be tenfold that of the past five years

It's like you run a factory; the equipment is full, but if the yield for high-end products is only 70%, the actual marketable products are reduced by 30%. The market hasn't fully priced this bottleneck!

📈 The market has already reacted:

• MLCC suppliers have risen 268% YTD in 2026 (the overall market is only +16%), so JP Morgan believes there is still room for valuation

• Current market capitalization is $354 billion, PE for 2026-2028 are 61x/40x/30x respectively

• Considering that the AI ecosystem transformation is still in its early stages, the consensus profit forecast may lag

🎯 JP Morgan's investment recommendation:

More favorable on Japanese/Taiwanese targets rather than Korean

• Japan: Murata, TDK, Taiyo Yuden

• Taiwan: Yageo, Walsin Technology

• Korean targets are relatively less attractive in valuation

My own view, since I personally hold Murata, US stock code: #MRAAY, I have studied it more recently. This round of the MLCC cycle is essentially the hardware dividend of AI infrastructure construction. It may be another strong and certain sector after storage!

When everyone is focused on chip stocks like Nvidia and AMD, MLCC, as the "capillaries" of servers, might have greater demand elasticity and less supply elasticity (long capacity expansion cycle, slow yield ramp-up).

Moreover, this sector is boring enough, with low attention, which may easily yield alpha. You see, it has risen 268% YTD in 2026, how many people have noticed it?

Now the four major manufacturers (Yageo, Walsin Technology, Unimicron, Taiyo Yuden) all say at the shareholder meetings "the longest shortage period in history," and JP Morgan has come out to endorse this trend; it is already very clear.

DYOR🙏

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。