Introduction: Why Cryptocurrency ETFs are Entering 2.0 from HYPE ETF

Since the approval of the U.S. spot Bitcoin ETFs in 2024, cryptocurrency ETFs have become an important gateway for traditional funds entering the digital asset market. From BTC, ETH to SOL, XRP, and recently the HYPE ETF launched around Hyperliquid, ETFs are gradually expanding from purely tracking token prices to staking yields, protocol growth, index allocation, and active management strategies. The competitive logic of cryptocurrency ETFs is also shifting from "providing asset exposure" to "providing yields and strategies."

Recently, 21Shares and Bitwise have launched HYPE-related ETFs, which include products that hold spot assets and attempt to obtain on-chain yields, as well as strategy products that offer double leveraged exposure. While all appear to revolve around HYPE, they correspond to completely different risk-return structures behind the scenes. This raises a new question: when ETFs start packaging staking yields, protocol economics, and investment strategies, what exactly are investors purchasing—the tokens themselves or a financial product redesigned by the issuer?

1. From BTC to HYPE: Why are Cryptocurrency ETFs Becoming More Complex?

In the U.S. market, cryptocurrency ETFs can be divided into four stages. Prior to this, there were physical-backed crypto ETPs globally, but the approval of the U.S. futures ETFs opened a local regulatory path.

The first stage is futures indirect exposure: On October 19, 2021, ProShares BITO was listed as the first Bitcoin futures ETF in the U.S. BITO does not directly hold BTC but tracks BTC through CME Bitcoin futures. It solves regulatory and custodial barriers but introduces rolling costs, futures spot basis, and tracking errors.

The second stage is direct spot holding: In January 2024, asset management firms such as BlackRock, Fidelity, ARK 21Shares, and Bitwise launched BTC spot ETFs; in July of the same year, ETH spot ETFs also officially entered the U.S. market. Compared to futures ETFs, spot ETFs directly hold the underlying assets, with net values closer to spot prices, shifting the competitive focus from "whether they can be approved" to fees, liquidity, custodial capabilities, and tracking efficiency.

The third stage is asset expansion: After BTC and ETH, the boundaries for ETFs started to expand significantly. From the end of 2024 to 2026, issuers gradually extended their product applications and strategies to assets such as SOL, XRP, HYPE, SUI, DOGE, and DOT. Crypto ETFs are no longer solely focused on the most mainstream assets but are starting to cover more public chains, protocols, and tokens with high market attention.

The fourth stage is yield and strategy expansion: We are currently in this stage, with staking ETFs for SOL, staking ETFs for HYPE, 2x Long HYPE ETFs, and crypto index ETFs, corresponding respectively to staking rewards, multiple exposures, multi-asset portfolios, and yield enhancement needs. Furthermore, crypto ETFs have also begun to enter the active management stage. For example, the 21Shares Active Crypto ETF (TKNS) no longer passively tracks a single token or a fixed index but dynamically adjusts the allocation of crypto assets and related tools based on market conditions, valuations, liquidity, and risk changes.

This evolution has a clear business rationale. BTC and ETH spot ETFs have formed a concentrated pattern at the top, and later entrants can hardly compete based solely on homogeneous products; they can only vie for funds through fees, staking yields, leverage, active management, or new targets. At the same time, PoS tokens can generate staking yields, and protocol tokens may be related to transaction fees, repurchases, and ecological incentives; if an ETF only tracks price, it will forgo some on-chain functions. The entrance of cryptocurrency ETFs into 2.0 essentially indicates that the traditional asset management industry has started to fully apply mature strategies such as indices, leverage, active management, and yield enhancement to crypto assets.

2. What are ETFs Actually Packaging: From Price Exposure to Asset Management Tools

The evolution of crypto ETFs from BTC futures ETFs to HYPE ETFs is not just the expansion of underlying assets, but also the expansion of product functions and sources of returns. When ETFs no longer only track prices, what exactly do they package?

2.1 Single Token Spot ETFs: Lowering the Holding Barrier but Losing On-Chain Functions

Single token spot ETFs are the most direct products. The fund holds the underlying tokens, and investors hold ETF shares to gain price exposure through the fund's net value. It solves issues such as wallet management, private key security, custody, compliance, and tax processing.

However, ETF holders typically cannot freely use their assets like direct token holders. Investors cannot transfer BTC from the ETF to personal wallets, nor can they directly use ETH, SOL, or HYPE to participate in DeFi, governance, payments, and on-chain applications. Fund shares represent a right in the securities market and do not equate to direct control over on-chain assets.

2.2 Staking ETFs: Incorporating On-Chain Yields into Funds but Introducing New Intermediary Risks

Staking ETFs attempt to compensate for the on-chain yield lost by spot ETFs. Taking 21Shares' THYP as an example, the fund tracks the price of HYPE and can stake part of its holdings for additional rewards. As of June 10, 2026, THYP's AUM is approximately $61.85 million, with a management fee of 0.30%. Bitwise's BHYP plans to internally stake the HYPE held by the fund through Bitwise Onchain Solutions. The potential staking rewards belong to the fund and are not directly distributed to investors, and staking rewards are not guaranteed.

Staking ETFs seem to be merely "spot ETFs plus yields," but they actually increase multiple layers of risk. The fund must select validators or staking service providers, process asset locking and un-staking cycles, and ensure the staked assets can meet ETF redemption demands. If a validator goes offline, misbehaves, or suffers slashing, the fund's assets may be damaged; if a large number of investors redeem while assets are still locked, the fund may also face liquidity mismatches.

2.3 Leveraged ETFs: Not Packaging Long-Term Assets but Daily Trading Strategies

Leveraged ETFs are fundamentally different from spot ETFs. The goal of the 21Shares 2x Long HYPE ETF (TXXH) is to achieve twice the daily price performance of HYPE, not twice the long-term cumulative return. The fund primarily gains leveraged exposure through swaps, futures, and options, does not directly hold HYPE, and does not pursue more than double returns beyond a single trading day. As of June 12, 2026, TXXH's AUM is approximately $6.16 million, with a management fee of 1.89%, significantly higher than THYP.

In a unidirectional rising market, compounding may amplify returns; in a highly volatile and fluctuating market, frequent rebalancing can create volatility drag. Even if HYPE returns to the starting point after a period, TXXH may still incur significant losses due to the daily path of gains and losses. Therefore, leveraged ETFs are not "more aggressive long-term HYPE investments," but strategy tools aimed at short-term traders.

2.4 Protocol Asset ETFs: Business Growth Affects Tokens but Without Equity

The most significant meaning of HYPE ETFs is that they allow traditional investors to begin engaging with protocol-based assets. The value narrative of HYPE is closely related to Hyperliquid's trading volume, transaction fees, repurchases, staking, and ecosystem expansion. Compared to BTC, it is more like an on-chain economic system with business metrics. Traditional analysts can observe Hyperliquid's trading volume, revenue, market share, repurchase amounts, user growth, and the HyperEVM ecosystem to assess HYPE's potential value.

However, protocol tokens are still not stocks. HYPE holders do not possess legal claims to Hyperliquid's cash flows, repurchase mechanisms can change, and rights to governance and information differ from those of corporate shareholders. Investing in THYP is not a direct investment in Hyperliquid. This constitutes an important boundary of ETF 2.0: ETFs can package protocol economics as price exposure in a securities account but cannot automatically convert tokens into equity.

2.5 Actively Managed ETFs: From Selecting Tokens to Selecting Strategies

Active management is the direction in which crypto ETFs are further complicating. TKNS does not track a fixed single asset but is managed by a team selecting and adjusting crypto assets and related investment tools based on market conditions. As of June 12, 2026, TKNS's AUM is approximately $207,000, with a management fee of 1.05%, and daily trading volume of only about $138.

Active management is theoretically suitable for the rapidly changing crypto market with significant asset variance, but it also transfers risk to the manager's abilities. The current small asset scale of TKNS indicates that the presence of the product does not equate to market acceptance of actively managed crypto ETFs.

3. After the Explosion of ETFs: Why Will Winners Take Most of the Funds?

The reality of cryptocurrency ETFs 2.0 is not that products and funds grow uniformly, but that products expand rapidly while funds continue to concentrate. As more issuers enter the market, crypto ETFs are gradually transitioning from the early product innovation stage to the stage of scale competition.

3.1 Cryptocurrency ETFs are Rapidly Expanding

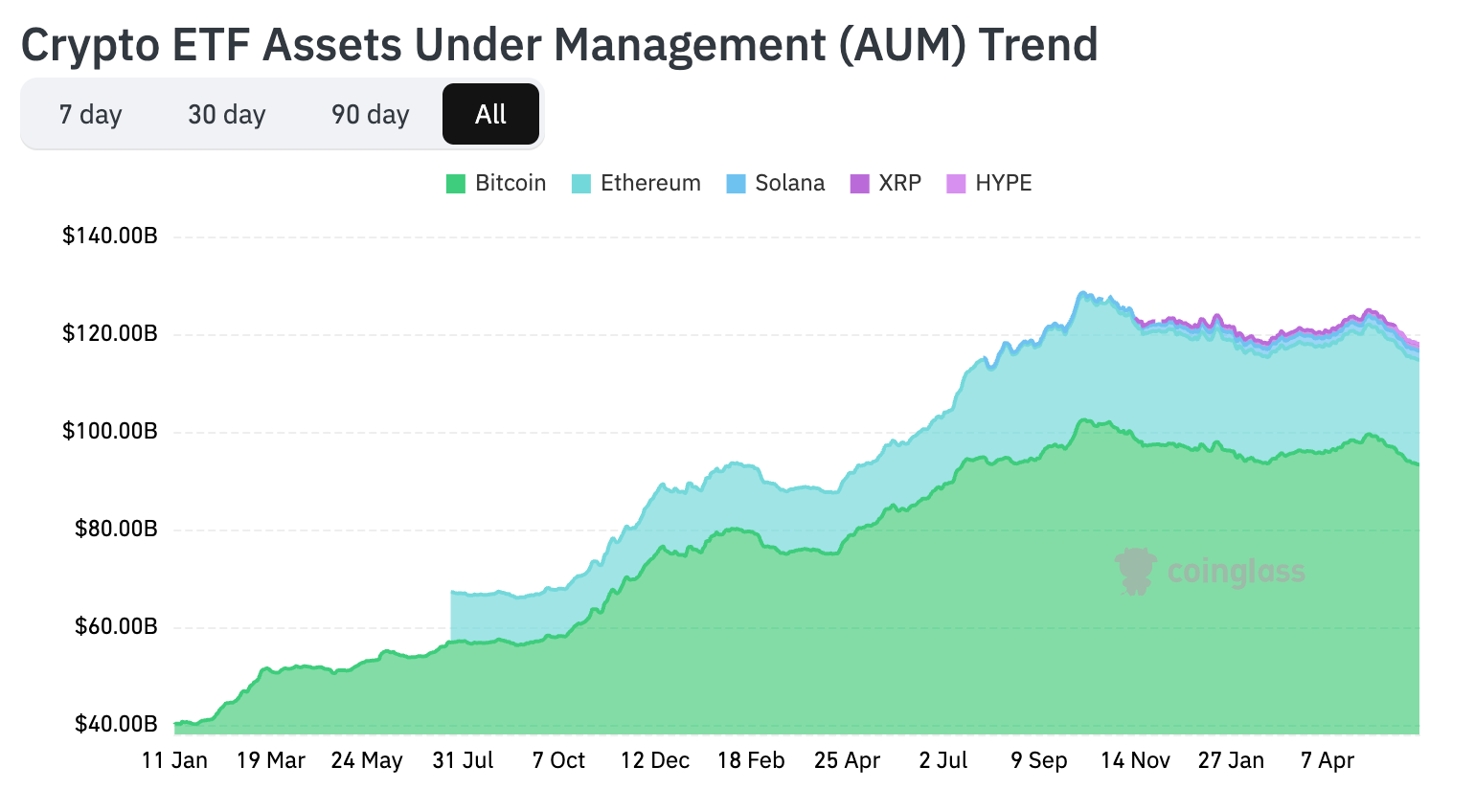

Since the approval of spot Bitcoin ETFs in the U.S. in 2024, the cryptocurrency ETF market has entered a period of rapid expansion. According to data cited by The Wall Street Journal from Morningstar Direct, asset management institutions have launched approximately 130 new crypto ETFs, with around 155 digital asset ETFs in the application or preparation stages. As of June 12, 2026, the total assets under management of 32 cryptocurrency ETFs tracked by CoinGlass reached $118.072 billion, covering 11 issuing institutions. Its AUM trend chart shows that since the U.S. spot Bitcoin ETFs were listed in January 2024, the total market size quickly grew from less than $40 billion, briefly approaching $130 billion. Although there has been a cumulative net outflow of approximately $5.487 billion from cryptocurrency ETFs over the past month, total AUM remains above $100 billion, indicating that cryptocurrency ETFs have gradually evolved from relying on short-term capital inflows to innovative products with a stable asset base.

Source: https://www.coinglass.com/etf

Product types have also undergone significant changes. In addition to BTC and ETH spot ETFs, the market has seen ETFs covering crypto assets like SOL, XRP, and HYPE, as well as innovations including staking ETFs, leveraged ETFs, actively managed ETFs, and index ETFs. ETFs are evolving from purely price tracking tools to comprehensive investment vehicles covering yields, strategies, and protocol growth.

3.2 The Matthew Effect in the ETF Industry

ETFs are fundamentally a market with strong network effects, where the growth in the number of products does not lead to an even distribution of funds. For investors, the core competitiveness of ETFs comes not merely from the underlying assets but from liquidity, trading depth, and transaction costs. The larger an ETF, the more likely it has higher trading volumes and more active market maker participation, leading to tighter bid-ask spreads and lower trading friction.

This advantage creates a positive feedback loop:

The larger the size, the better the liquidity;

The better the liquidity, the lower the bid-ask spread;

The lower the bid-ask spread, the easier it is to attract institutional fund allocations;

More fund inflows further enhance size and liquidity.

Currently, the combined AUM of Bitcoin ETFs and Ethereum ETFs accounts for about 97% of the total market size; while SOL, XRP, and HYPE ETFs have extended product boundaries to more crypto assets, their combined AUM still accounts for less than 3%. This means that the cryptocurrency ETF market is undergoing two simultaneous changes: rapid expansion in product numbers and underlying asset range, while funds remain highly concentrated in BTC and ETH. At the same time, funds continue to concentrate in ETF products from a few leading asset managers, while smaller ETFs find it increasingly difficult to attract attention and fund inflows. For institutional investors, liquidity is often more important than product innovation. Even if several ETFs offer similar asset exposures, funds often preferentially flow to the most actively traded and largest products.

3.3 The “Winner Takes All” Characteristic of Traditional ETFs

This phenomenon is not unique to cryptocurrency ETFs but is a long-standing rule in the ETF industry. For instance, in the U.S. stock index ETF market, the SPDR S&P 500 ETF (SPY), Vanguard S&P 500 ETF (VOO), and iShares Core S&P 500 ETF (IVV) have long dominated the majority of S&P 500 index ETF assets. Despite a plethora of products tracking the same index in the market, funds ultimately concentrate in a few top ETFs with the best liquidity and largest sizes. This is because, for institutional funds, scale, liquidity, and trading efficiency often outweigh the slight differences in fees. Therefore, the ETF industry inherently exhibits a “winner takes all” characteristic.

Cryptocurrency ETFs are replicating this developmental path. From BTC spot ETFs to HYPE ETFs, product innovation is certainly important, but the factors determining long-term winners are likely still asset scale and fund liquidity.

3.4 Cryptocurrency ETFs May Enter a Phase of Elimination

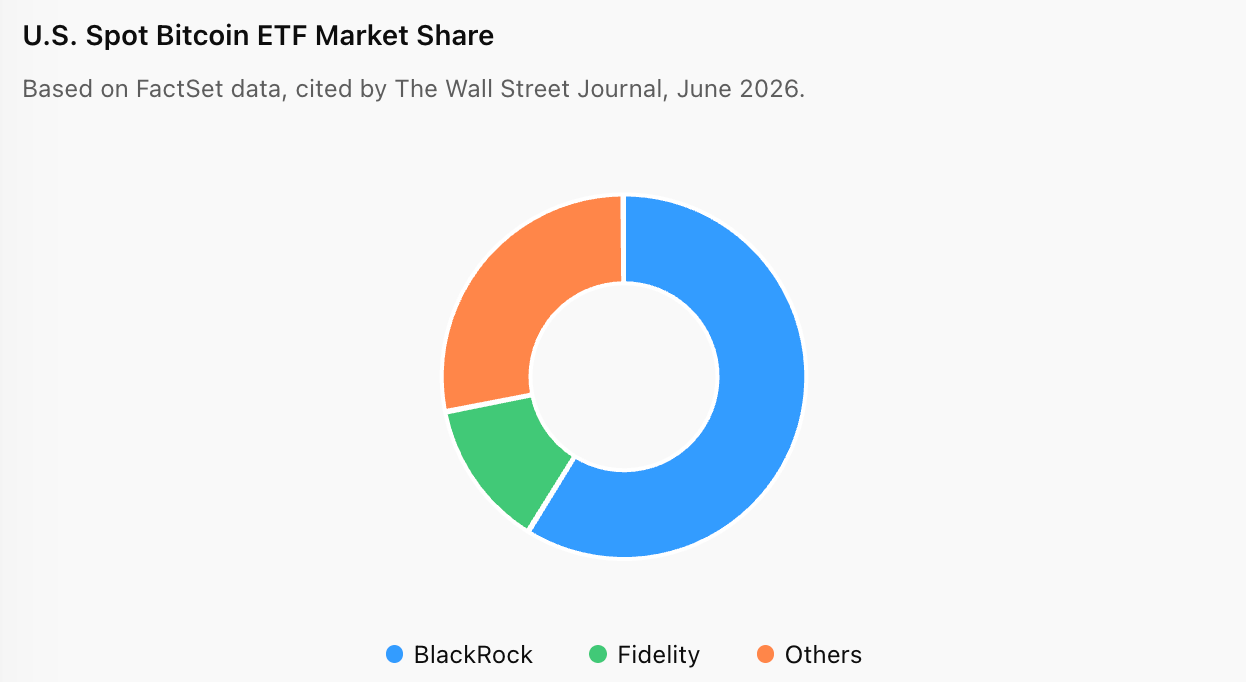

FactSet data shows that in the U.S. spot Bitcoin ETF market, BlackRock’s IBIT occupies nearly 60% of market share, Fidelity’s FBTC accounts for about 13%, with these two institutions controlling approximately 72% of the asset scale.

This highly concentrated market structure means that a large number of newly issued products will face increasingly fierce competition. It is widely believed in the industry that an ETF typically needs to reach an asset management scale (AUM) of about $25 million to $100 million to cover operating costs such as issuance, custody, compliance, auditing, and market-making, while also ensuring a sustainable economic foundation for long-term operation. For products with smaller scales and inactive trading, if they cannot continuously attract fund inflows, they may face risks of liquidation or closure in the future. As more homogeneous products flood into the market, the cryptocurrency ETF industry may gradually evolve from an "issuance race" to an "elimination phase."

4. The Four Structural Contradictions of ETF 2.0

The significance of cryptocurrency ETF 2.0 lies not only in the increase of product quantity and expansion of asset range but also in how it is reshaping the way investors engage with crypto assets. From spot ETFs to staking ETFs, protocol-based ETFs, and actively managed ETFs, crypto assets are gradually being integrated into the traditional financial system. However, this integration is not a simple benefit, as it is accompanied by a series of new structural contradictions.

4.1 ETFs Make Crypto Assets Easier to Buy but Harder to Participate in On-Chain Economics

The greatest value of ETFs lies in lowering barriers to entry. Investors can gain exposure to crypto assets through securities accounts, retirement accounts, or traditional advisory platforms without managing wallets, private keys, gas fees, or on-chain security risks. For many traditional investors, purchasing BTC ETFs, ETH ETFs, or THYP is far more convenient than directly holding the underlying assets.

However, this convenience is built on the abandonment of on-chain participatory rights. When investors purchase ETFs, they receive price exposure, not full usage rights of the underlying assets. Whether it’s BTC ETFs, ETH ETFs, or future products holding HYPE, investors typically cannot participate in protocol governance, claim airdrops, use DeFi protocols, or engage in other on-chain interactions.

In other words, ETFs make it easier for investors to access crypto assets but also distance them from on-chain economies. This creates a natural tension for a crypto industry that emphasizes open participation and self-custody.

4.2 ETFs Bring Yields into Securities Accounts but Increase Intermediary Layers

The emergence of staking ETFs is one of the most important innovative directions of ETF 2.0. Taking THYP, BHYP, and SOL Staking ETFs as examples, issuers attempt to incorporate on-chain staking yields into the fund returns, allowing traditional investors to earn returns similar to on-chain holders without managing wallets and validating nodes. From an investor's perspective, this undoubtedly enhances capital efficiency. Previously, investors could only gain from price increases, but now they can also share part of the on-chain yields.

However, obtaining these yields is not without cost. In the on-chain world, users can autonomously choose validators, determine staking ratios, and bear corresponding risks; whereas, under the ETF structure, key decisions regarding asset custody, validator selection, operational management, and risk control are made by the issuer.

This means that yields are retained, but control is centralized. Investors gain a simpler experience but also become more dependent on the decision-making abilities of fund managers, custodians, and validator operators. As the scale of staking ETFs expands, the concentration of validator rights among a few institutions may become a new industry issue.

4.3 ETFs Make Protocol Values Easier to Price but Cannot Resolve Equity Absence

The rise of protocol-based ETFs poses a new question for the market: how can traditional capital markets invest in crypto protocols?

Taking Hyperliquid as an example, the value of the HYPE token is closely related to protocol trading volume, revenue, and ecosystem development. With the advent of products like THYP and BHYP, traditional investors can allocate HYPE through ETFs and share in the potential benefits of protocol growth. From this perspective, ETFs do lower the barriers for traditional capital to engage with crypto protocols and make protocol value easier to price in traditional markets.

However, a fundamental issue persists. Unlike stocks, protocol tokens typically do not represent equity and do not grant holders legal claims to protocol cash flows. Even if an ETF holds a large amount of HYPE, its investors still receive only the returns from changes in token prices, not equity in the business sense.

As a result, ETFs can securitize protocol values but cannot securitize protocol ownership. This is the most essential difference between protocol-based ETFs and traditional stock ETFs. They can help traditional capital markets understand and allocate crypto protocols, but cannot fully replicate the equity structure of stock markets.

4.4 ETFs Promote Industry Maturity but May Weaken Crypto's Native Attributes

From a broader perspective, ETFs are driving the crypto industry into an asset management era. In the past, investments in crypto assets emphasized self-custody and on-chain participation. Investors needed to manage wallets, sign transactions, participate in governance, and interact directly with protocols. Today, more and more investors are obtaining exposure through ETFs. In the future, with the development of actively managed ETFs, index ETFs, yield enhancement ETFs, and multi-asset strategy ETFs, investors may even stop caring about which chain the underlying assets operate on or what technical architecture they employ, focusing solely on fund performance and risk-return characteristics.

The investment logic is changing: previously, it was about buying BTC and holding BTC; now, it's about buying BTC ETFs; and in the future, it might be about purchasing a basket of crypto strategy ETFs. This trend helps attract more traditional capital into the market, enhancing industry liquidity and maturity, but it may also weaken the long-emphasized native attributes of the crypto industry.

Essence-wise, ETF 2.0 is pushing crypto assets closer to traditional financial assets, and this reflects the long-standing contradiction between financialization and decentralization. ETFs may become a bridge connecting these two worlds, but they are also redefining crypto assets' initial value propositions.

5. Outlook: Cryptocurrency ETFs are Entering Asset Management Era

The development of cryptocurrency ETFs has shifted from the regulatory phase of "can they be approved" to the asset management phase of "how to compete." If ETF 1.0 solved the issue of how traditional investors could gain exposure to crypto assets, then ETF 2.0 is answering another question: how will crypto assets be incorporated into the global asset management system.

5.1 Competition Will Shift from Asset Expansion to Fund Competition

Over the past two years, the core competition in cryptocurrency ETFs has been asset expansion. The market has completed the transition from BTC to ETH, and then to assets like SOL, XRP, HYPE. Issuers are competing for the market opportunities of "first approved" and "first listed."

However, as the number of products rapidly grows, the focus of future competition will gradually shift from asset expansion to fund contention. For the ETF industry, what truly matters is not the number of products, but the assets under management (AUM). Liquidity, trading depth, brand influence, and institutional channel capabilities will eventually be reflected in the scale of funds. Institutions with stronger issuance capabilities, broader distribution networks, and higher market acceptance are more likely to continuously attract capital inflows.

According to the development experience of the traditional ETF market, leading products often capture the majority of funds, while numerous homogeneous products struggle to break the scale bottleneck. The cryptocurrency ETF market is likely to develop along a similar path, with the core measure of industry competition transitioning from "number of issuances" to "AUM rankings."

5.2 Yield and Strategy Products Will Become Mainstream

As spot ETFs gradually mature, merely offering price exposure may become increasingly difficult to form a differentiated competitive advantage. In the future, yield and strategy products are likely to become the main direction of industry innovation.

On one hand, staking ETFs are expected to further expand. By incorporating on-chain yields into fund returns, issuers can provide additional sources of yield beyond price increases. The market may see more staking ETFs based on SOL, HYPE, and other PoS networks in the future.

On the other hand, strategy-based products will also continue to diversify. Actively managed ETFs, index ETFs, leveraged ETFs, and yield enhancement ETFs are bringing mature investment frameworks from traditional asset management into the crypto market. The focus for investors will no longer merely be "which assets to buy," but "what strategies to adopt."

This change means that the competitive logic of crypto ETFs will gradually shift from underlying asset competition to asset management capabilities competition.

5.3 Cryptocurrency Assets are Being Repackaged as Traditional Financial Products

From a longer-term perspective, the development of cryptocurrency ETFs is essentially part of the financialization process of crypto assets. BTC ETFs are packaged as digital gold; ETH ETFs are packaged as exposures to smart contract infrastructure; THYP and BHYP offer exposure to Hyperliquid's protocol growth and potential staking yields; TKNS is closer to actively managed funds in the traditional asset management industry.

For increasing numbers of traditional investors, they don't necessarily need to understand wallets, private keys, gas fees, or on-chain interactions, nor do they need to directly hold underlying tokens. Through ETFs, they can gain exposure to corresponding assets, yields, or strategy. This means that the investment barrier is lowering, but the distance between investors and the on-chain world is gradually increasing.

In the future crypto market, there may be two existing systems: one is the ETF, fund, and asset management product system targeting institutions and traditional investors; the other is the on-chain protocols and decentralized finance system targeting native users. ETFs will become an important bridge connecting these two worlds.

Conclusion

The significance of ETF 2.0 is not just the emergence of more cryptocurrency ETFs, but the re-packaging and re-pricing of crypto assets, gradually integrating them into the global asset management system.

From BTC spot ETFs to HYPE staking ETFs, and then to actively managed and strategy-based products, what investors are purchasing is no longer just the tokens themselves, but a set of financial products that have been screened, packaged, and managed for risks.

The crypto market is undergoing a transformation from "on-chain assets" to "configurable assets," and although ETFs may not change blockchain itself, they are changing the way global capital allocates crypto assets.

About Us

Hotcoin Research, as the core research institute of Hotcoin Exchange, is committed to turning professional analysis into your practical tools. Through "Weekly Insights" and "In-Depth Research Reports," we dissect market dynamics for you; with the help of the exclusive column “Hotcoin Selection” (AI + expert dual screening), we pinpoint potential assets and reduce trial-and-error costs. Every week, our researchers will also meet you through live broadcasts to interpret hot topics and predict trends. We believe that with warm companionship and professional guidance, more investors can navigate the cycles and seize the value opportunities in Web3.

Risk Warning

The cryptocurrency market is highly volatile, and investments inherently carry risks. We strongly advise investors to invest only after fully understanding these risks and conducting investments under a strict risk management framework to ensure fund safety.

Website: https://www.hotcoin.com/zh_CN/learn/index/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。