The problem with Oracle is not that there is no AI story, but that this story has become expensive enough.

After the US stock market closes on June 10, Oracle will release the FY2026 Q4 financial report. The market currently expects Q4 revenue to be around $19.1 billion, with an adjusted EPS of about $1.96. In the previous quarter, Oracle provided a Q4 guidance of total revenue growth of 19%—21% year-over-year, total cloud revenue growth of 46%—50%, and a non-GAAP EPS of $1.96—$2.00.

Looking at these figures, Oracle is still firmly positioned within the AI cloud narrative.

Meanwhile, over the past year, OCI, AI cloud orders, large customer contracts, data center expansions, and the market speculation surrounding customers like OpenAI, Meta, and NVIDIA have repositioned Oracle from being a traditional database and enterprise software company into the trading framework of AI infrastructure.

However, this financial report is one where the market really wants to see not whether Oracle has an AI story, but rather the AI cloud orders are substantial, but are these orders worth the high capital expenditures needed from Oracle?

1. From the data, Oracle has already placed itself at the AI cloud table

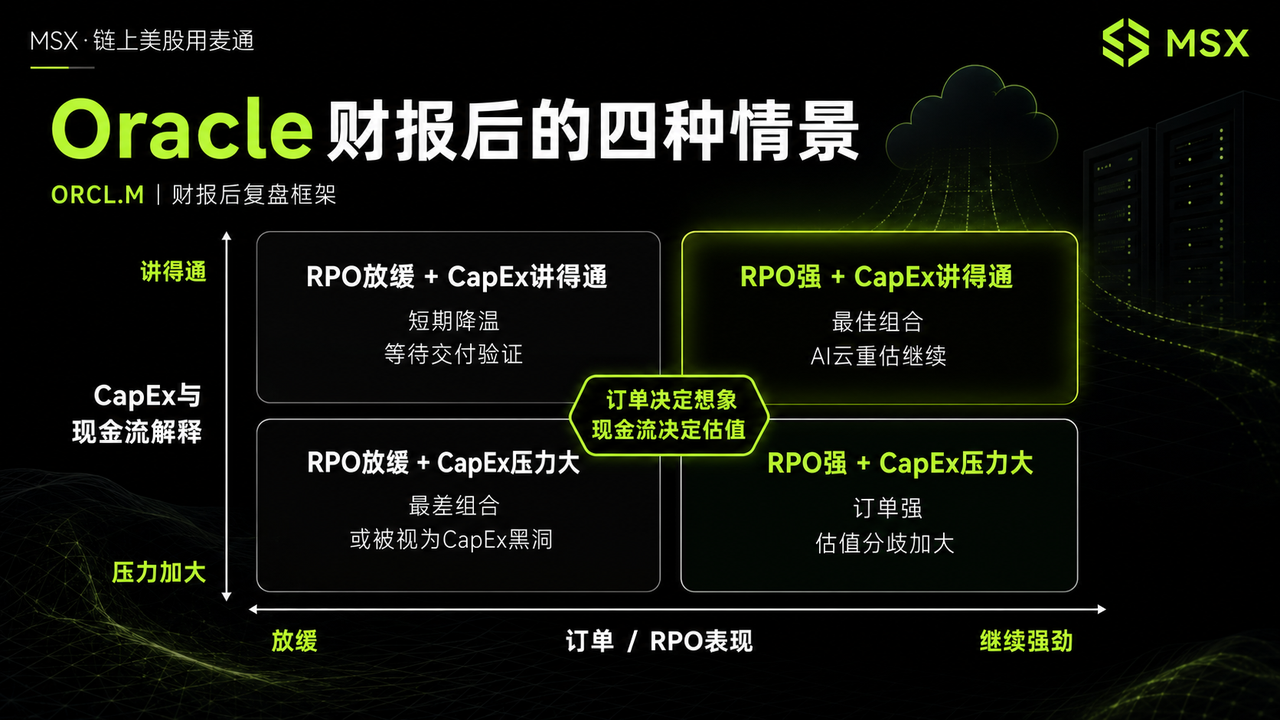

The most shocking data from Oracle last quarter was undoubtedly the RPO reaching $553 billion, a year-over-year increase of 325%.

RPO can be simply understood as the scale of contracts that the company has signed but has not yet recognized as revenue. For cloud computing companies, the larger the RPO, the higher the visibility of future revenue, overall reflecting the demand climate and CPU capacity commitments concentratedly.

This is also why after Oracle disclosed its RPO last quarter, the market quickly regarded it as one of the core targets in the AI cloud infrastructure space.

However, it should be noted that RPO is not profit, nor is it cash flow that arrives immediately; it is more like a huge order book—while thicker orders do indicate stronger demand, investors will continue to inquire about three more practical questions: When will these orders be delivered? How much needs to be paid upfront before delivery? Is the gross margin and cash recovery speed sufficient after delivery?

That is the central disagreement for Oracle now.

- Bulls believe that the $553 billion RPO indicates that AI cloud demand is real, long-term, and already secured by large clients, and Oracle is becoming an important capacity provider during times of tight AI computing supply;

- Bears worry that if these orders depend heavily on substantial data center investment, GPU procurement, power resources, and long-term financing to fulfill, then the higher the RPO, the greater the potential short-term free cash flow and balance sheet pressure may be;

Therefore, Oracle's RPO itself is not the problem.

The real issue is how quickly RPO can be converted into revenue and what margins and cash flow quality will convert it into shareholder value.

This is also the first core point of interest in this financial report: whether RPO continues to expand and whether management can provide a clearer delivery rhythm for orders. If RPO continues to reach new highs, it indicates that large AI cloud contracts are still flowing in, and Oracle's visibility of future revenue will continue to improve; however, if the growth rate of RPO significantly slows down, the market may worry that the peak of AI cloud orders is passing.

Orders are the starting point of a story, but not the endpoint.

For the current Oracle, the market has already recognized it has gained a ticket to the AI cloud; what remains to be seen is whether it can convert the ticket into real revenue, profits, and cash flow.

2. The story is expensive: CapEx pressures behind OCI growth

Oracle's past core label was databases and enterprise software.

But now, the market is more attentive to OCI, which stands for Oracle Cloud Infrastructure.

In the last quarter, Oracle provided guidance of total cloud revenue growth for Q4 to be 46%—50% year-over-year. If this time cloud revenue approaches or even exceeds the upper limit of guidance, it indicates that AI cloud demand remains strong, and the growth trajectory of OCI has not yet noticeably sloweddown; however, if cloud revenue falls below expectations, the market will begin to worry: while RPO is significant, the order conversion and delivery rhythm might not be as swift as imagined.

This is also the biggest difference between AI cloud and traditional software.

Traditional software companies have lower marginal costs, making revenue growth easier to convert into profits; however, AI cloud infrastructure is not a light asset business; it requires building data centers in advance, procuring GPUs, and securing power, land, cooling, networking, and operational capabilities.

Orders can be signed quickly, but data centers will not be built overnight, GPUs will not arrive automatically, and power capacity is not always accessible.

Therefore, Oracle's biggest bottleneck now may not be whether there is demand, but whether there is enough capacity to meet that demand.

This is also why the market has become more discerning regarding Oracle.

If it were a pure software company, new revenue could typically deliver higher incremental profit margins; however, as Oracle is increasingly being priced by the market as an AI cloud infrastructure company, it must accept a different set of evaluation standards: capital expenditure intensity, asset turnover efficiency, depreciation pressure, financing costs, free cash flow, and long-term investment returns.

In other words, Oracle is not simply upgrading from a "software company" to an "AI company"; it is more like transitioning from a high cash flow enterprise software company to one that simultaneously has software business and heavy asset AI cloud business. The valuation logic has changed, and the market will naturally reprice.

This is also one of the key reasons for the pressure on Oracle's stock price over the past period; the market does not deny the demand for AI cloud, but is concerned about whether Oracle will bear excessively heavy capital expenditure pressures to chase orders.

Thus, in this financial report, management must answer several questions:

- How much higher should future CapEx go?

- Is the speed of data center construction keeping up with orders?

- Are the gross margins of AI cloud contracts good enough?

- When will free cash flow improve?

- Are the financing costs and balance sheet pressures manageable?

These questions are more important than mere income and EPS. Because Oracle's current transaction focus has shifted from "are there AI orders" to "can these AI orders bring sufficient capital returns."

If management merely continues to emphasize strong orders, it may already be insufficient. What the market really wants to hear is how quickly Oracle can turn these orders into measurable cloud capacity, and whether this cloud capacity can ultimately convert into high-quality cash flow.

3. Is it an AI cloud dark horse or a CapEx black hole?

This Oracle financial report is essentially an exam on AI cloud capital returns.

From a data perspective, the market will first pay attention to whether Q4 revenue and EPS meet expectations. The market anticipates revenue of about $19.1 billion and EPS of approximately $1.96, if it merely approaches expectations, it may not be enough to change the market's concerns over CapEx; if it significantly exceeds expectations, especially if cloud revenue and profit quality perform well together, it will provide stronger support for the stock price.

Next, cloud revenue should be near or exceed the guidance upper limit. Last quarter, Oracle provided a Q4 total cloud revenue guidance of 46%—50% year-over-year growth. This is a key indicator to determine whether OCI continues to accelerate. If cloud revenue approaches or even exceeds the upper limit, it indicates that AI cloud demand is still being fulfilled; if it falls short of expectations, the market will reassess the delivery rhythm of RPO.

The third point is whether RPO continues to expand. If RPO continues to reach new highs, it indicates that large AI cloud contracts are still flowing in, and Oracle's future revenue visibility will continue to improve; but if the growth rate of RPO significantly slows, the market may worry that the peak of AI cloud orders is passing.

The fourth point is whether the FY2027 revenue guidance can be strengthened. The market is now highly focused on Oracle's revenue visibility for the upcoming year. If management can further strengthen the growth and delivery rhythm of AI cloud, Oracle's AI cloud logic will be steadier; conversely, if future growth guidance is not strong enough, the market may believe that current valuations have already reflected too many optimistic expectations.

Finally, and most importantly, is the CapEx and cash flow metric. Oracle must prove that the current high investment is not simply in pursuit of the AI trend, but capable of yielding higher future revenues, better profit margins, and more stable cash flow.

If management can clarify the CapEx rhythm, data center delivery, customer demand, financing arrangements, and paths for improving free cash flow, the market's concerns about Oracle will ease; however, if these issues remain vague, the stock price may continue to fluctuate around the contradiction of "growth" and "burning money."

This is also the current largest disagreement regarding Oracle.

Bulls believe that it is becoming a capacity provider in the AI cloud era. Against the backdrop of tight supply in AI computing, those who can provide stable, scalable cloud capacity will secure large customer orders and long-term revenue visibility; Oracle's advantage lies in its enterprise client base, its product mix of database and cloud services, as well as obtaining a sufficiently large order book during the burst of AI cloud demand.

From this perspective, Oracle is no longer just a traditional software company but an important link in the AI infrastructure chain.

But bears are concerned that it is exchanging increasing capital expenditures for growth. AI cloud is not a light asset business. Data centers may face delays, power and GPU supplies may be constrained, depreciation and financing costs may rise, and free cash flow may remain under pressure. Once order deliveries fail to meet expectations or gross margins fall below market projections, Oracle's AI cloud story may turn from "high growth" to "high investment, low return."

Both sides have their reasoning.

Oracle's bullish logic is based on the premise that AI cloud demand is real, RPO is extremely strong, OCI's growth is rapid, and large customer orders grant the company long-term revenue visibility; whereas the bearish logic holds that the heavy asset nature of the AI cloud is altering the company's financial structure, requiring the market to reassess its cash flow quality and capital return capability.

This financial report from Oracle is not a proof of the AI story, but rather a proof of capital expenditure returns.

If RPO continues to expand, cloud revenue maintains high growth, management strengthens future revenue visibility, and clarifies CapEx, cash flow, and financing arrangements sufficiently, then Oracle's AI cloud story can continue.

However, if growth remains primarily at the order level, while delivery, cash flow, and capital expenditure pressures do not ease, the market will also continue to question whether this is an AI cloud dark horse or a CapEx black hole?

In short, it just needs to prove that these orders are worth spending this much money.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。