Capital is betting on card issuance, compliance, clearing and settlement, and corporate APIs, and the dividends of stablecoin payments are shifting from "cards" to "infrastructure."

Written by: Farmer Frank

Li Lin has made another investment.

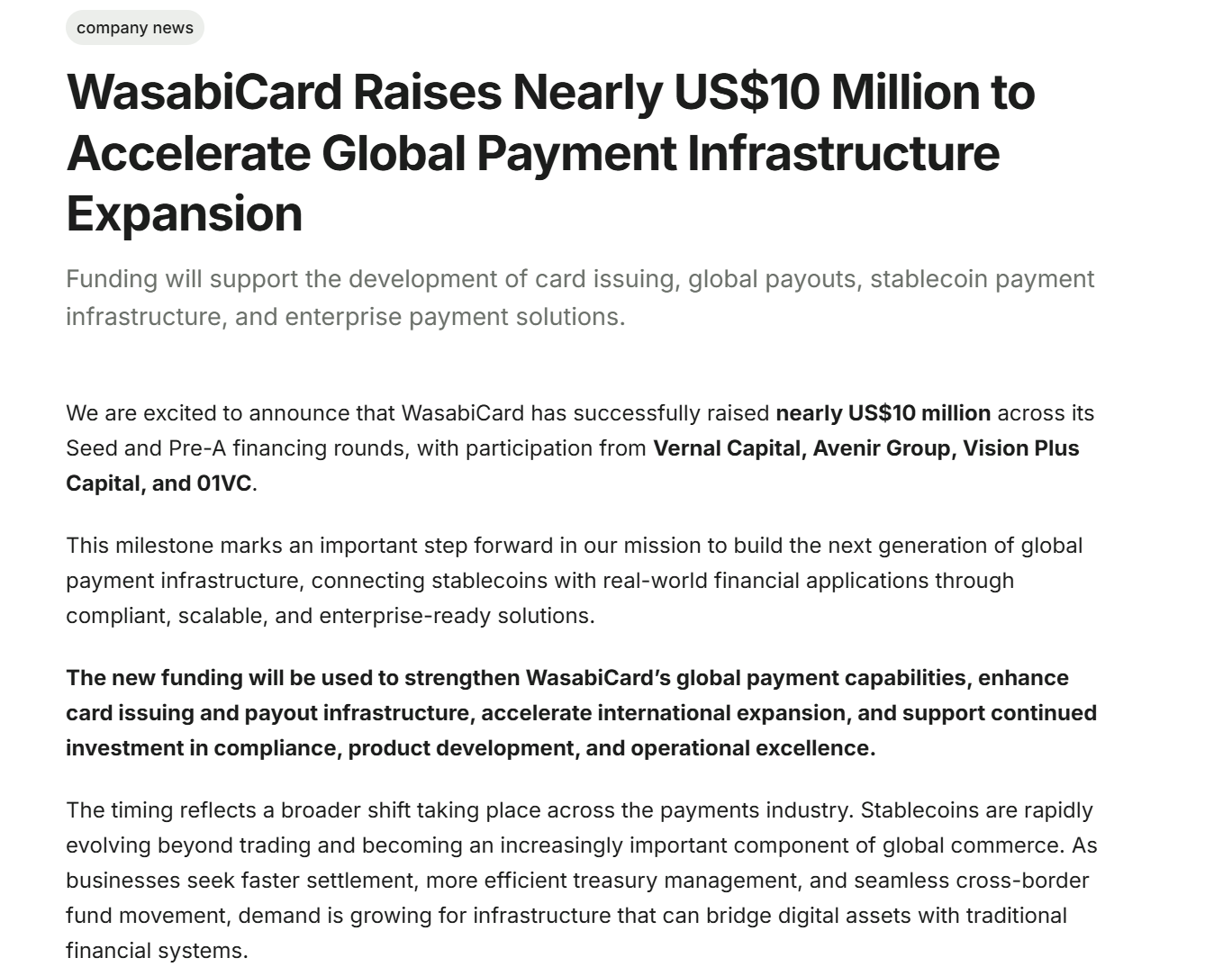

On June 3, 2026, the global stablecoin payment infrastructure platform WasabiCard completed its Pre-A round financing, bringing its total funding to nearly $10 million, including previous early rounds. Investors include Vernal Capital, Avenir Group, Vision Plus Capital, and 01VC—among them, Avenir Group is Li Lin's family office.

Interestingly, almost simultaneously, another news swept through the community: Fiat24 has suspended new account applications in mainland China, while several familiar crypto payment card services for Chinese users, such as SafePal and Bitget Wallet, have partnerships with Fiat24 regarding issuance capabilities.

On one side, capital is pouring into an "invisible" payment infrastructure company, while on the other side, underlying service providers are directly affected by policy adjustments, impacting some front-end card products. Viewed together at the same point in time, this provides an opportunity to reassess the stablecoin payment landscape.

Behind this opportunity is a rapidly growing real demand.

1. The Decline of U Cards: It's Not the Demand That's Declining, But the Model

According to Fireblocks' "State of Stablecoins 2025" report, among the surveyed institutions, 49% are already using stablecoins in payment scenarios, while another 41% are in testing or planning stages, indicating that nearly 90% of institutions are engaging with stablecoin payments in some way.

Demand is increasing, but the ways to meet that demand are changing.

It is well known that the form of stablecoin payments most discussed in the Chinese market over the past few years has been the "U Card": users transfer stablecoins like USDT and USDC into card products and use them for online subscriptions, purchases, or offline payments, which is the easiest for everyone to understand and accept.

However, U cards are just the visible front end to users.

Behind a card, the real complexity lies in card issuance qualifications, card organization partnerships, KYC/AML, risk control systems, stablecoin to fiat currency exchanges, clearing and settlement networks, merchant channels, and cross-border payment capabilities. What users often remember are brands targeted at them, such as RedotPay, KAST, and Crypto.com, whereas institutions like WasabiCard are not well known.

In fact, thanks to infrastructure companies like WasabiCard, today, issuing a card alone is not a difficult task.

Project parties can completely outsource the stablecoin acceptance, credit allocation, card issuance, and consumption channels to third-party service providers, needing only to brand and complete the front-end launch. In a sense, this is also a key reason why U card products have quickly spread in recent years.

Therefore, Fiat24 tightening account openings is just a prelude.

The real issue is that the rapidly spreading C-end U cards over the past few years essentially embody a "light front-end, heavy external dependencies" model, outsourcing the most difficult aspects while retaining mainly branding, customer acquisition, and that layer of user interface. While this addresses the issue of "spending U," it fails to resolve the question of "how to operate this business long-term, stably, and compliantly."

Over the past year, the contraction or even exit of several front-end card products has repeatedly demonstrated that relying solely on front-end experience cannot sustain a payment business that can withstand market cycles.

This point is crucial.

U card products can be copied, subsidies can be followed, and users will quickly migrate with rates, risk control, and availability, but what is truly hard to replicate is back-end capability:

Can stable card issuance and acquisition partnerships be maintained across multiple markets;

Can different jurisdictions' identity verification and anti-money laundering requirements be managed;

Can funds and information flows be maintained precisely across stablecoin top-ups, fiat exchanges, card usage, and merchant settlements;

Can a sufficiently mature risk control system be established regarding abnormal transactions, high-risk addresses, chargebacks, refunds, freezes, and compliance reviews;

This is also the starting point for institutions like Avenir Group to invest in WasabiCard—what institutions are focusing on may not be just another crypto card product, but a stablecoin payment business that is transitioning from "cards" to "infrastructure."

2. Why Avenir Group Invested in WasabiCard

In recent years, the crypto market has not lacked grand narratives.

From DeFi, NFT, GameFi to public chains, L2, restaking, and AI + Crypto, industry cycles are often driven by asset prices, token expectations, and liquidity expansions. However, payments have always been a somewhat different business: they aren’t as glamorous, and it’s challenging to create extreme valuation imaginations in a short time. Yet, they are much closer to real-world transaction needs.

As long as transactions occur, every specific aspect—payment, currency exchange, card issuance, settlement, acquiring, and cross-border transfers—has the potential to generate income.

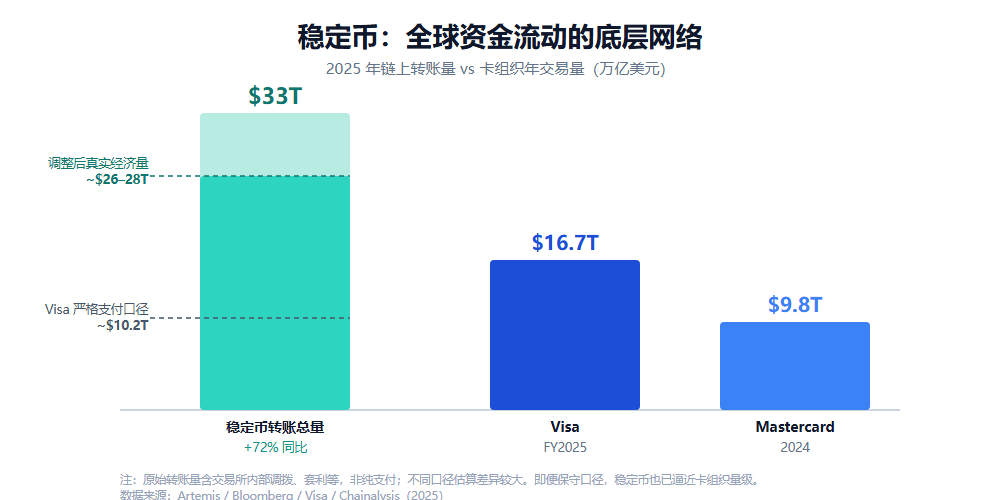

The scale of this business can no longer be ignored. According to Artemis data, by 2025, the global on-chain transfer volume of stablecoins will reach $33 trillion, a 72% year-on-year increase, surpassing the combined total of Visa and Mastercard. Even excluding internal allocations, arbitrage, and other non-payment purposes, its real economic volume is approaching that of traditional card organizations.

Regardless of whether these funds correspond to transactions, allocations, or settlements, it means stablecoins have become a vital underlying network for global capital flows. However, because of this, a chain-based USDT/USDC transfer must turn into usable payments for businesses, salaries that employees receive, settlements that merchants accept, or balances that users can spend, requiring a whole set of off-chain financial infrastructure for support.

This is the opportunity for companies like WasabiCard.

They engage in the essential yet somewhat "dirty work" of connecting card organizations and issuance resources, building corporate APIs, handling financial settlements, managing risk control and compliance, and supporting enterprise clients in embedding stablecoin payment capabilities into their workflows. Such tasks may not attract immediate market attention like issuing a token, but once validated, they could create stronger reusability.

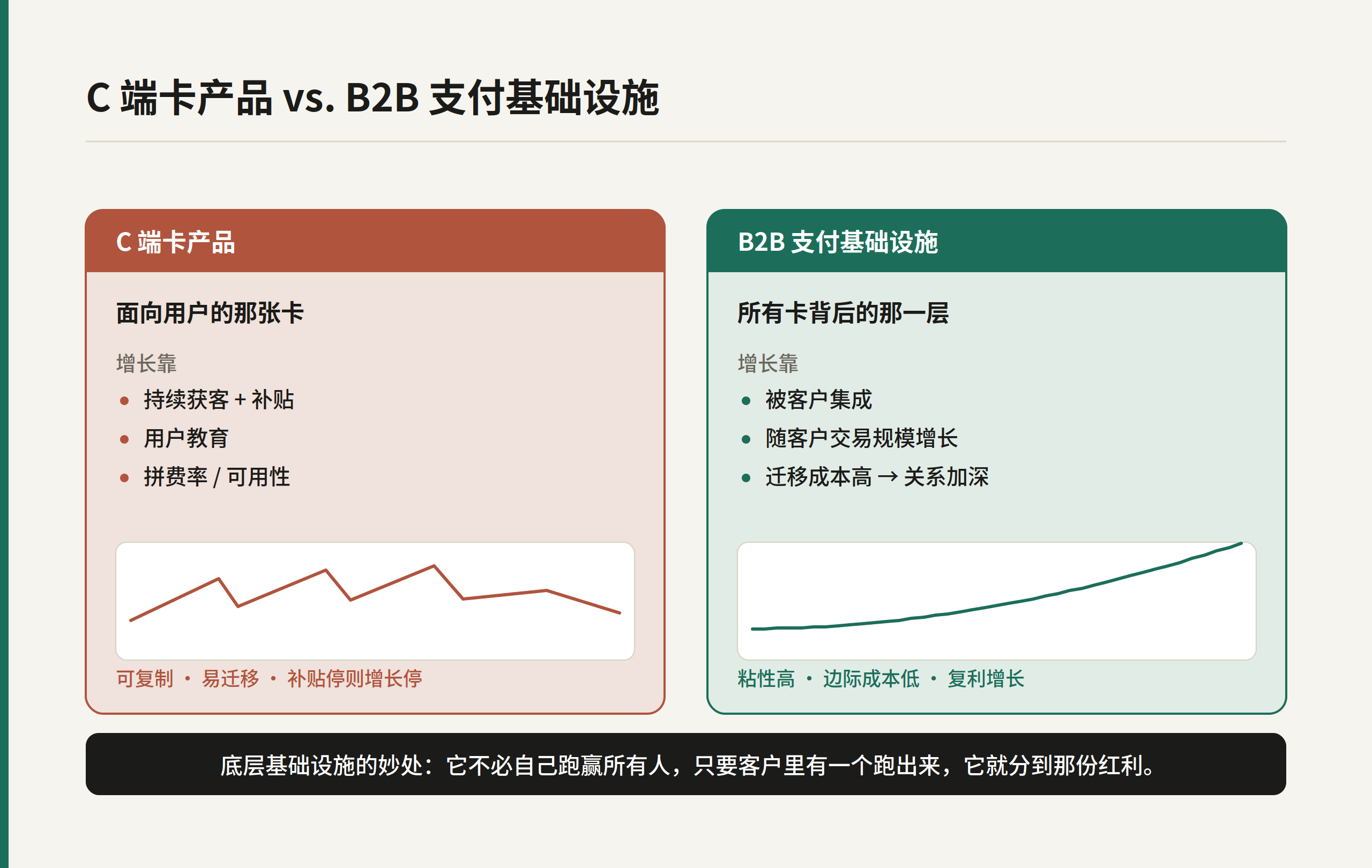

Because from a business model perspective, B2B infrastructure and C-end card products are inherently two different businesses.

C-end card products require continuous customer acquisition, ongoing subsidies, and continuous user education, and they face user comparisons regarding rates, usability, and brand trust. Once B2B payment infrastructure is integrated by exchanges, wallets, payment companies, and overseas enterprises, it has the opportunity to continually benefit as the client’s transaction volume grows—while the former is trapped in the acquisition cycle, the latter can more readily achieve compounding returns.

More importantly, once a project integrates a particular payment API into its business, the migration costs increase, and the partnership is more likely to deepen over transaction volumes, settlement amounts, and business scale. This is the brilliance of underlying infrastructure: it doesn’t need to outperform everyone; as long as any customer succeeds or scales, it can share in the growth dividends.

Breaking this down explains why capital is more willing to focus on the underlying layer:

Payments are one of the easiest scenarios for stablecoins to generate real cash flow; compared to the Web3 narrative that still relies on token cycles and liquidity expectations, it aligns more with the real transaction needs, forming a business model that is less dependent on market sentiment and more driven by transaction flows and network scale;

Service providers like WasabiCard already possess business and compliance foundations, accumulating reusable capabilities through B-end customer relationships and highly compliant systems. For investors, "already integrated" is far more valuable than "planned to integrate";

Capital is not purchasing a singular product, but a set of scalable infrastructure, and its growth can "ride" on customer growth rather than needing to reacquire customers with each transaction;

For investment institutions, the ceiling of a singular U card product depends on how many C-end users it can secure and how often these users actively consume; whereas the imagination of a stablecoin payment infrastructure depends on how many enterprise clients it can serve, how many payment scenarios it encompasses, and whether it can become a general capability layer behind more front-end products.

From this perspective, Avenir Group's investment in WasabiCard should be viewed not so much as a form of "authoritative endorsement" but more like a keen instinct of a seasoned crypto player making a directional bet on stablecoin payment infrastructure.

Where it points may be more significant than the investment itself.

3. It's Not About Scale, But Position: What are the Barriers on the B-end?

Of course, this doesn't mean that the infrastructure model is inherently more likely to succeed. In stablecoin payments, the C-end cards and B-end infrastructure are two distinct tracks, and comparing absolute scales is meaningless; the key lies in positioning.

First, take a look at the benchmark of the C-end track, RedotPay, which currently has over 6 million users, covers more than 100 countries, with an annual transaction volume of about $10 billion and an annual revenue exceeding $150 million. In 2025, it cumulatively raised $194 million, with a valuation exceeding $1 billion.

It almost represents the ceiling for what U cards can achieve—yet interestingly, even for such a champion, card BINs previously had to rely on licensed entities like Reap, compliance needed connections with Fireblocks and Sumsub, and cross-border payouts required integration with Circle's network.

In other words, the leading card also stands atop a layer of underlying infrastructure.

Now consider the "graduate" of the B-end track, BVNK, which processes over $30 billion in annual payments, covers more than 130 countries, holds licenses in places including MiCA, and was eventually acquired by Mastercard for up to $1.8 billion, making it the largest stablecoin infrastructure acquisition to date.

It illustrates another possible endpoint for this track: rather than capturing C-end users, it achieves depth in underlying capabilities, continuously refining compliance, culminating in being absorbed into a global network by a giant.

WasabiCard also participates in this track. As of this round of financing, it has disclosed that it has served over 500 enterprises globally, issued over 500,000 cards, processed transactions exceeding $1 billion, and completed integrations with multiple chains including Avalanche, Arbitrum, and BNB Chain. Recently, it also joined Circle's partner program.

It aggregates card issuance, APIs, settlement, and payment capabilities into a single interface, focusing on localized strategies in collaboration with major banks globally, positioning itself as an infrastructure company capable of "one-click" global white-label card issuance, APIs, clearance, settlement, and payment capabilities. This localization strategy allows WasabiCard to leverage local banking capabilities to compliantly issue cards to local users; at the same time, as its enterprise clients, they need only integrate the API once to achieve global card issuance at a click.

More crucially, from publicly available information, WasabiCard's focus is not solely on consumer card issuance, but on continually expanding global card issuance resources, enterprise payment APIs, global fund distributions (payout), multi-chain asset integrations, and compliance system construction. This signifies that it offers not merely a singular payment product, but a suite of underlying payment capabilities that can be invoked by various platforms and business scenarios.

So, what exactly is the moat of this capability?

The Fireblocks report provides a useful reference: when banks and payment institutions select stablecoin infrastructure suppliers, 41% prioritize "quick and reliable fund distributions (payout)", and 34% emphasize compliance. In short, payout and compliance are the two most valued factors when enterprises make selections, which cannot be substituted by merely issuing a card.

For B-end representatives like WasabiCard, this also means needing to prove not just the ability to issue cards, but the capacity to become the stablecoin payment operating system behind different enterprise clients, serving a broader array of internet enterprises and cross-border business scenarios.

4. PayFi: A Moment When the "Underlying" Is Seen Again?

If the busiest part of stablecoin payments in past years has been U cards, the next phase worth paying attention to might be the PayFi infrastructure.

For a long time, PayFi was easily simplified to "card issuance" or "consumer cashback," making it seem more like a user product track rather than a financial infrastructure track.

However, in the past two years, obvious changes have been taking place.

The financial infrastructure related to stablecoin issuance, payments, and settlements has become one of the few assets in the crypto industry capable of consistently generating cash flow, and the PayFi track associated with it has gathered nearly all types of players, from crypto-native projects, traditional payment giants, stablecoin issuers, exchanges, to dedicated stablecoin public chains, all positioning themselves in their own ways.

What best illustrates this is the series of actions by traditional payment giants:

In October 2024, Stripe acquired the stablecoin infrastructure company Bridge for about $1.1 billion, viewed as one of the largest mergers in the crypto space at the time;

A year and a half later, in March 2026, Mastercard announced its intention to acquire stablecoin infrastructure provider BVNK for up to $1.8 billion, about $700 million more than Stripe, breaking the record;

Almost at the same time, Visa expanded its cooperation with Bridge, already acquired by Stripe, planning to promote stablecoin-associated cards from 18 countries to over 100 countries;

Earlier, PayPal had already launched its own stablecoin, PYUSD;

When viewing these actions from payment giants, card organizations, and large fintech companies on the same map, it’s no longer a singular company's isolated bet on crypto payments, but a collective early positioning of the entire payment industry around the stablecoin entry.

This is because the impact of stablecoins extends beyond just payment experiences; it encompasses deeper profit and power structures within traditional financial systems—specifically relating to who can control accounts, cross-border channels, and settlements in the new era. From this perspective, the giants' proactive connection of on-chain accounts, stablecoin assets, and merchant collection points can be viewed not just as embracing innovation, but also as a reluctance to be sidelined in the next round of payment and settlement restructuring.

However, as giants begin to vie for the underlying aspects themselves, the window for independent infrastructure players becomes clearer—it’s either they become an irreplaceable part of a giant's network or grow their own network. After all, regulatory matters, licensing, KYC/AML, partnerships with card organizations, and localized compliance are precisely the elements that C-end U card products, which have previously relied on traffic and subsidies, find the hardest to sustain long-term.

This also explains why companies like WasabiCard focus this round of funding primarily on building global compliance systems, connecting multi-bank business networks, and upgrading core settlement systems—these directions may not be glamorous, yet they are crucial foundational capabilities that need to be established as stablecoin payments transition from user products to financial infrastructure.

Looking further into the future, the imagination around PayFi could extend to AI Agent payments. If in the future, AI Agents begin to perform automated transactions on behalf of users, then payment infrastructure cannot be designed solely around "humans." Machines will likewise require callable accounts, verifiable authorizations, controllable limits, auditable transaction records, and the capability to automatically execute small, high-frequency payments within compliance boundaries.

This would complicate the ultimate scenario for stablecoin payment infrastructure, though this remains a more distant imagination.

But it at least indicates that the value boundaries of stablecoin payments are far larger than a U card.

Final Words

Crypto payment cards are undoubtedly a good business.

They connect stablecoins with real-world consumption, allowing users to intuitively feel that "U can be spent." This is why U cards have quickly gained traction in the Chinese market, becoming the most easily understood entry point of PayFi for ordinary users.

However, the biggest dividends may not lie within the cards themselves.

In the past, markets were more likely to remember a card, an app, a cashback promotion, or a low-rate entry point, but as stablecoins permeate larger-scale real-world business scenarios, what truly determines the long-term landscape of the industry could be the deeper underlying capabilities.

Players like WasabiCard, who may not be the most familiar names in the Chinese market, nonetheless represent the notion that stablecoin payments are a slow business that Still demands substantial operations. If they can continue to scale in compliance, card issuance, settlement, acquiring, cross-border payments, and corporate APIs, they have the opportunity to become key companies in the age of PayFi.

Returning to the two recent developments, they actually point to the same thing: the competition in stablecoin payments is shifting from the visible "card face" to the unseen "underlying."

Because of this, as more capital begins to reassess stablecoin payment infrastructure, the industry may be entering a new phase.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。