How to calculate the mNAV value of $MSTR and what is mNAV!

Today I saw many friends discussing the value of MSTR's mNAV, believing that mNAV has fallen below 1 and that they should sell Bitcoin to repurchase stocks instead of selling stocks to buy Bitcoin: native, but in fact, the mNAV value has not yet entered negative territory.

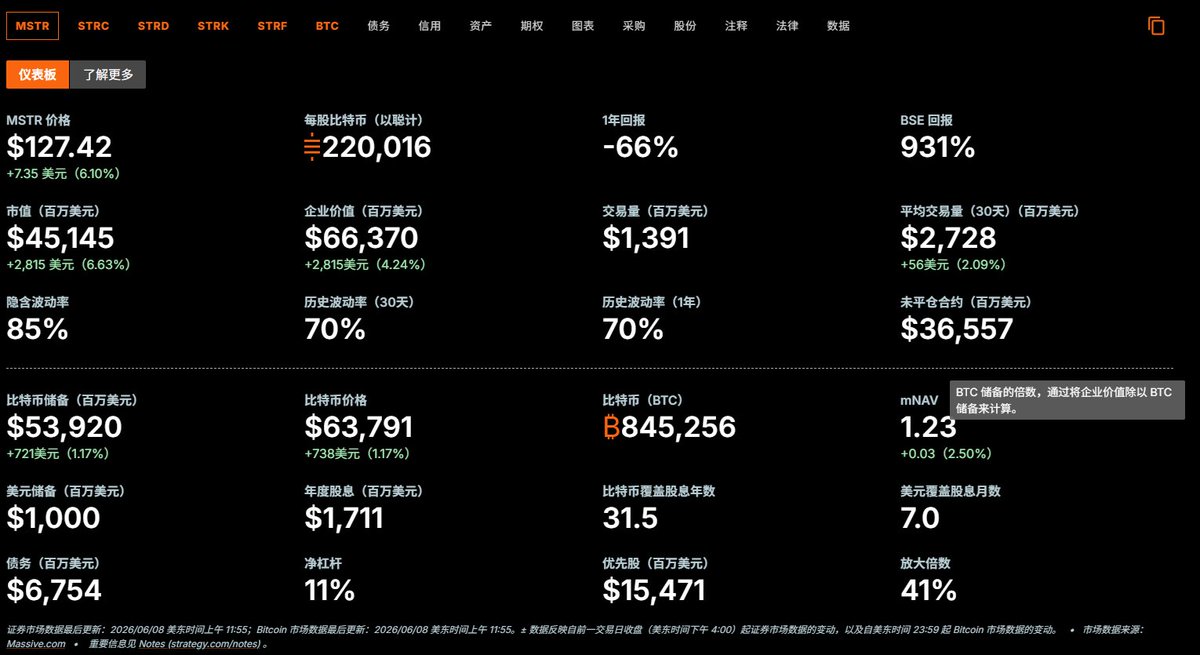

Saying that MSTR's mNAV is less than 1 is actually calculated using MSTR’s common stock market value ÷ BTC reserves value. If calculated this way, MSTR's common stock market value is about 45.233 billion dollars, and BTC reserves value is about 53.934 billion dollars, directly dividing gives about 0.84.

However, this 0.84 is not the mNAV defined by Strategy officially. It is also not what we normally refer to as mNAV; mNAV can be simply understood as how many times the market is willing to pay to buy the Bitcoin asset package behind MSTR.

The official calculation method for Strategy's mNAV is: mNAV = enterprise value ÷ BTC reserves value

And enterprise value is: total market value of common stock + debt + nominal value of perpetual preferred stock - latest disclosed cash balance

So in fact, according to the officially released data, it should be:

53.934 + 10 - 67.54 - 154.71 = 32.709 billion dollars

Then use the common stock market value divided by this remaining asset:

45.233 ÷ 32.709 = 1.38

This indicates that if debt, preferred stock, and cash are accounted for, the remaining assets after properly ranking common stock actually stand at around 1.38 times.

And MSTR’s mNAV actually represents:

First, it represents the market's premium for MSTR's Bitcoin.

If mNAV is above 1, it indicates that the market is not just treating MSTR as BTC but also providing an extra premium. This premium may come from Saylor's financing ability, MSTR’s stock liquidity, the options market, NASDAQ index components, leveraged exposure, and expectations of continued accumulation of BTC.

This is also why MSTR is considered a leveraged Bitcoin.

Second, it represents whether MSTR's financing flywheel can still turn.

When mNAV is high, MSTR selling stock to buy BTC is often interpreted as enhancing each share of BTC. Because financing with high premium stock buys real BTC. MSTR has also publicly provided a mNAV threshold for common stock ATM issuance, for example, that they do not issue common stock to buy BTC in principle when it is below 2.5 times, with exceptions mainly for paying debt interest and preferred stock dividends.

Third, it represents the market’s confidence in MSTR.

The higher the mNAV, the more the market believes that MSTR is not just an ordinary BTC holding company, but a financial machine that can continuously finance in the capital market, expand BTC reserves, and increase each share of BTC. The lower the mNAV, the less the market is willing to pay a premium for this structure, and it even begins to view it as a high volatility BTC position with debt and preferred stock pressure.

Fourth, when mNAV is close to 1, it indicates that MSTR's premium is compressed.

At this point, the significance of continuing to sell common stock to buy BTC will diminish, because the market is no longer willing to grant MSTR a high financing premium. If it really falls below 1, it means the market value of the entire capital structure is less than the book market value of BTC it holds, and the market begins to discount it.

This is similar to the situation with Grayscale's GBTC before it joined the spot ETF.

In simple terms, when MSTR's mNAV is less than 1, buying MSTR's stock is theoretically lucrative.

#Bitget is here to be VIP! Crypto, US stock, CFD, global opportunities in one stop.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。