Original | Odaily Planet Daily (@OdailyChina)

Author|Azuma (@azuma_eth)

In the context of a sluggish crypto market and increasingly contracting liquidity, entrepreneurs in the industry are facing unprecedented pressure to break through.

However, Odaily recently learned that several entrepreneurial teams have begun to view the Hyperliquid ecosystem as a breakthrough direction, hoping to help direct traffic to themselves and realize their own value capture through building trading frontends, strategy platforms, AI Agents, and HIP-3 custom markets (customizable oracles, leverage limits, settlement rules), among other methods.

In the past, giving a frontend to a DEX sounded unimaginative, because the market always had this inertia — the real value is captured by liquidity, matching engines, and the underlying protocol itself, not by those frontend windows that are reliant on it.

But as the market elevates Hyperliquid's positioning to the level of "on-chain Nasdaq," the value and imagination of this business are also changing.

Odaily Note: Refer to "After 220 Days of Trade.xyz Launch, Hyperliquid is Becoming the 'New Nasdaq'"

Analogous to traditional stock markets, retail investors do not directly trade on Nasdaq or the New York Stock Exchange; the platforms that truly build relationships with users are often broker platforms like Robinhood, Interactive Brokers, and Charles Schwab — the exchanges provide the underlying market, liquidity, and matching capabilities; brokers are responsible for user entry, product design, and experience optimization.

If the hypothesis that Hyperliquid becomes the new generation of Nasdaq holds, then those applications built on Hyperliquid that are responsible for directly interfacing with users and optimizing the trading experience will have roles that are no longer merely simple frontends, but more akin to "brokers" in traditional financial systems.

Starting from HIP-3, how do these "brokers" make a profit?

Before understanding these specific "broker" platforms, we need to briefly answer two questions. One is what is HIP-3? The other is how can these HIP-3 based projects generate profits?

Firstly, it should be clarified that not only HIP-3 projects can "start a business" around Hyperliquid. Theoretically, any team can build its own products based on Hyperliquid's underlying liquidity and trading capabilities; some choose to create trading frontends, some opt for mobile applications, and some develop strategy platforms, AI Agents, or asset management tools, all sharing the responsibility of driving traffic to Hyperliquid and expanding its user boundaries.

Among all these directions, HIP-3 has the highest imagination and has already achieved certain success. In simple terms, HIP-3 allows third-party teams (Builders) to deploy perpetual contracts based on Hyperliquid's underlying liquidity and matching system and operate their own trading markets.

This means that entrepreneurial teams no longer need to redundantly create a new chain or rebuild a matching system, nor do they need to bear the development and security costs of high-performance trading infrastructure, but can directly utilize Hyperliquid's mature infrastructure to create the most user-facing layer of products.

In some sense, this is highly similar to the broker system in traditional finance. Nasdaq itself does not help users with investment advice, UI design, community operations, or providing strategy products; these tasks are ultimately completed by brokers like Robinhood. Thus, the significance of HIP-3 can be understood as further opening up the "broker" market space built on Hyperliquid.

As for the profit model of these "brokers," while some projects do aim to generate revenue through derivative services (such as asset management and strategy performance income), currently, the most direct source of income for such "broker" projects remains the sharing of transaction fees and the appreciation expectations of HYPE.

According to Hyperliquid's current mechanism requirements, third-party deployed markets will adopt higher fee standards than the native markets, a significant portion of which will be returned to the deployer or frontend operator. This means that once a frontend successfully masters user entry, it will unlock real, continuous cash flow directly linked to trading volume. If a frontend can achieve tens of billions in daily trading volume, relying solely on fee commissions could generate an impressively large revenue scale.

Additionally, Hyperliquid officially requires third parties to stake at least 500,000 HYPE when deploying custom trading applications (it has stated that this will gradually decrease in the future). Given the recent strong market performance of HYPE and its fundamental conditions, the appreciation potential of HYPE itself is also one of the core revenue sources for such projects.

As for the future, the token issuance behavior of upper-level "broker" projects will also become a potential source of revenue, which does not need to be elaborated further.

Typical Project Overview

Trade.xyz: Bringing US Stocks, Commodities, and Indices to Hyperliquid

If one were to find the project that best showcases the imagination of the Hyperliquid ecosystem, Trade.xyz would undoubtedly be the first choice.

In one sentence, what Trade.xyz is doing is "bringing traditional financial market assets onto Hyperliquid." Currently, Trade.xyz has successively launched perpetual contract products including Nasdaq Index, S&P 500 Index, gold, crude oil, and some US stocks. For crypto users, this means they can participate in the price fluctuations of traditional financial markets directly through Hyperliquid's liquidity system without leaving the chain environment.

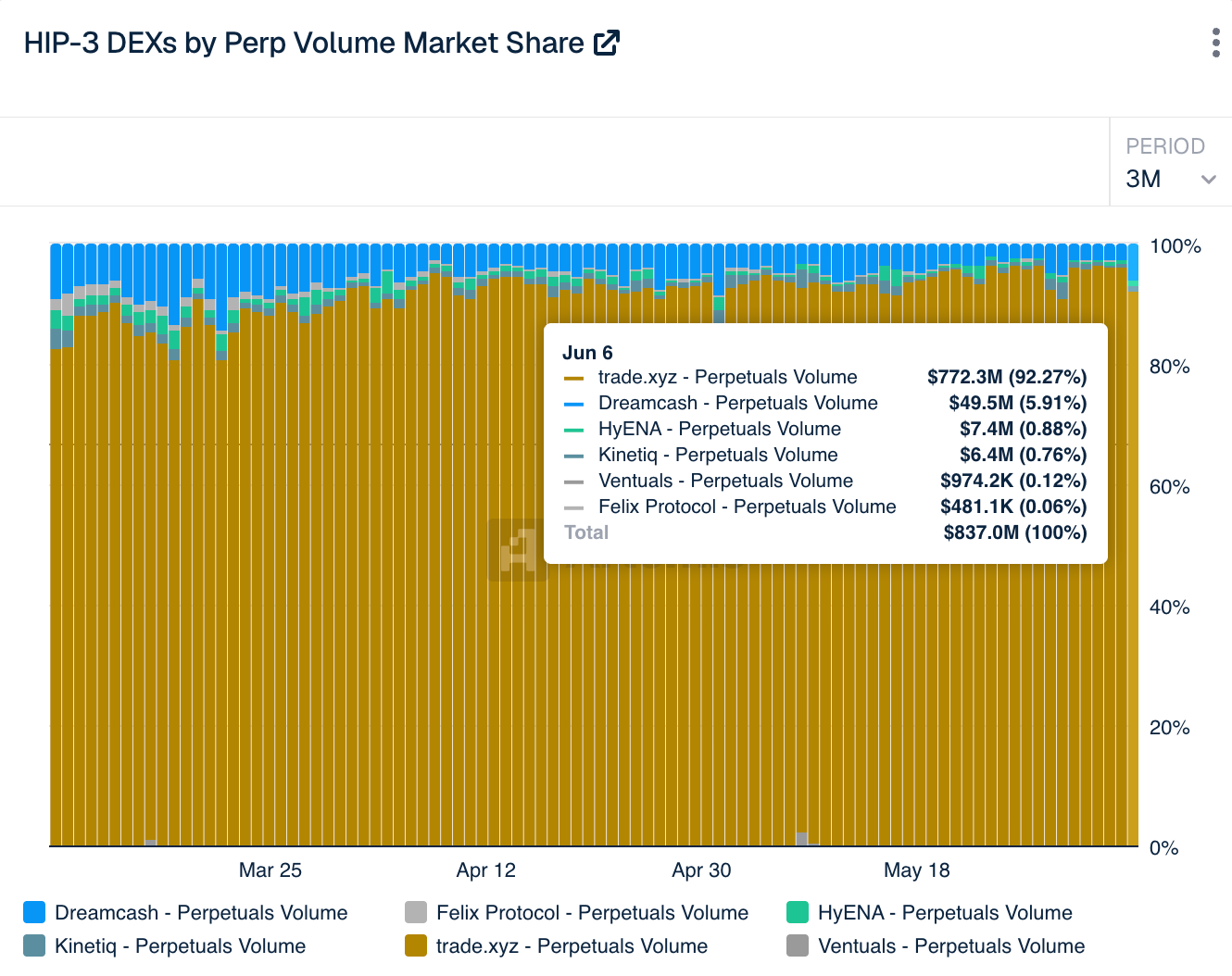

As of now, Trade.xyz dominates both open interest (OI) and daily trading volume with an absolute leading share. Real-time data from Artemis and The Block shows that it has monopolized about 90% of the current HIP-3 market share.

For Hyperliquid, the significance of Trade.xyz lies in extending the asset boundary of the ecosystem. Many people believe that whether Hyperliquid can ultimately grow into an "on-chain Nasdaq" is not primarily about how much trading volume it can create, but whether it can become a unified trading network covering diverse asset classes, thus accommodating new user groups and market demands.

For Trade.xyz itself, its value lies in being the first to occupy the promising track of trading traditional financial assets on-chain. To this day, the explosive trading volume and revenue data from Trade.xyz have proven the strategic success of the platform.

Dreamcash: The Capturer of Mobile Traffic

If Trade.xyz's goal is to expand the asset boundary of Hyperliquid, then Dreamcash focuses on the user boundary.

For a long time, cryptocurrency trading products have faced a common problem — they are often designed for professional trading users. Complex on-chain operations, obscure jargon, and high-threshold capital management methods have kept many potential users out. Even with platforms like Hyperliquid that already offer excellent trading experiences, the main user group remains primarily composed of native cryptocurrency traders.

Dreamcash aims to solve this problem. Unlike many products that emphasize trading functionality, Dreamcash resembles a trading app for the mobile internet era. The project team has invested significant effort into mobile experience, reward systems, and user growth mechanisms, hoping to lower the barrier for ordinary users to engage in on-chain trading through a more lightweight, gamified product design. Users can simply log in with their email or social account and leverage cryptocurrencies or global macro assets with one click, just like buying and selling stocks, in a matter of seconds.

As of the publication date, Dreamcash has surpassed 100,000 cumulative downloads on both iOS and Android platforms.

Ventuals: Pre-IPO Market Pioneer

Ventuals has not chosen to focus on existing mainstream assets in the market but has extended its reach to the area with the highest barriers in traditional finance — private equity in the primary market.

In the traditional financial market, equity subscriptions for imaginative tech unicorns like OpenAI, SpaceX, and Anthropic are often monopolized by top investment banks and multi-billion dollar funds; retail investors not only lack access but also face extremely long lock-up periods and poor liquidity. Ventuals' core logic is to utilize the HIP-3 characteristic that allows customizable clearing and settlement rules to package the pre-IPO equity of these unlisted companies into on-chain perpetual contracts, allowing global retail investors to directly engage in the long and short speculation of their valuations before these unicorns officially go public.

One critical reason Nasdaq has become one of the world's most important capital markets is that it continuously meets the financing and pricing needs of new economy firms, and what Ventuals is trying is, to some extent, a similar approach — enabling the on-chain market not just to trade existing assets but also to provide a price discovery mechanism for future assets.

Of course, this direction still has a long way to mature, but it is already one of the most noteworthy evolutionary directions for on-chain capital markets.

Based: The Next Stop, "Super App"

The goal of Based is to create a crypto "super app" encompassing trading, prediction markets, payment, and consumption scenarios.

Currently, Based offers trading terminal products on web, desktop, and mobile (iOS, Android) platforms. Through Based, users can trade spot and perpetual futures on Hyperliquid, access prediction markets via Polymarket, and make cryptocurrency purchases in the real world using Based Visa.

After the implementation of HIP-3, Based has taken a further step from simply being a Hyperliquid frontend by collaborating with Ethena to launch a custom trading protocol called HyENA based on Hyperliquid. Unlike other HIP-3 projects that primarily innovate around trading targets, HyENA focuses on the margin itself. This protocol introduces a margin system centered on yield-generating stablecoins (USDe), aiming to enable users to continuously generate yield from idle margins while trading.

In some sense, this resembles taking the logic of money market funds from traditional financial markets into on-chain trading scenarios. In traditional broker systems, idle funds in client accounts are often automatically allocated to money market funds to enhance capital utilization efficiency. HyENA tries to reconstruct this experience in the on-chain environment.

Minara AI: When Agents Begin to Become Users

If Trade.xyz, Dreamcash, Based, and other projects are still competing for human user entry, Minara AI represents a more futuristic direction — the Agent entry.

The core product of Minara is a financial execution layer for AI, allowing users to issue trading instructions directly to AI tools like Claude and Cursor using natural language, with Minara invoking Hyperliquid's underlying trading capabilities to perform operations like opening and closing positions and managing leverage. In other words, in Minara's vision, the future may not have humans directly using trading interfaces, but AI Agents configured by users.

In some sense, this trend is not limited to the Hyperliquid ecosystem but is one of the most noteworthy trends across the entire internet world.

The Open Combination Relationship Brings Hyperliquid's Strongest Moat

As more and more teams begin to choose to build upper-layer applications based on Hyperliquid, a more industry-specific question has started to be contemplated by an increasing number of people — What does the combination relationship between Hyperliquid and these on-chain "brokers" mean for the competitive landscape of exchanges?

In the past, most people's understanding of exchanges was still at the "product competition" stage. Everyone was competing on who had better UI, more listed tokens, lower transaction fees, and who could attract more users.

However, Hyperliquid is driving a radically different direction of competition. More and more market participants are realizing that what Hyperliquid aims to create is not the familiar user-facing trading platform, but a set of financial infrastructure that can be directly called upon by APIs, programs, or even AI systems, with upper-layer "brokers" built on top of it to interface with users.

In some sense, this resembles the evolutionary path of software under the AI wave. In the traditional internet era, products competed on UI, entry points, and user duration; but in the AI era, an increasing number of products are starting to degrade into "capability layers" — the API itself is becoming the new traffic entry.

This is the new evolutionary direction that Hyperliquid is leading. It is precisely because of this that more and more practitioners have begun to perceive Hyperliquid as a "Financial Operating System" (Financial OS), which only needs to be responsible for unifying capabilities at the bottom layer, while upper-layer "brokers" will be responsible for creating specific scenarios.

Once this structure is formed, a strong binding symbiotic relationship will emerge between Hyperliquid and these upper-layer "brokers." For Hyperliquid, each additional upper-layer application equals a new traffic entry, new user channel, and new trading scenario; the protocol itself does not need to personally operate these products but can continuously share transaction fees and expand the liquidity depth of the entire network. For these upper-layer applications, they heavily rely on the liquidity, matching efficiency, and on-chain trading experience that Hyperliquid has established; they do not need to recreate chains, rebuild order books, or restart liquidity from scratch, as long as they do two things well — bring users in and keep users engaged.

This means that the future competition logic may no longer be between one exchange and another, but may gradually evolve into competition among different financial networks. As more applications, Agents, and trading entry points choose to build on the same liquidity network, the network itself will form an increasingly strong attraction effect. The platforms that successfully aggregate the most developers, most applications, and most user entry points will also have the deepest liquidity and the broadest market coverage capability.

Perhaps this is the strongest moat of Hyperliquid and the most imaginative aspect of the new Nasdaq.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。