TL;DR

Compliance Process: US regulators are beginning to establish compliant pathways, HYPE ETF is promoting the entry of Perp DEX into traditional portfolios

Asset Boundary Expansion: RWA assets becoming perpetual, Pre-IPO perpetualization, and the perpetualization of event markets break the boundaries of crypto assets

Market Landscape Changes: CEX remains the absolute main entrance, Perp DEX is rising rapidly, and ETFs and prediction markets are entering the competition

Value Reconstruction: 24/7 price discovery capability, global liquidity aggregation, capital efficiency increase, and promotion of asset innovation ability

Risk Spillover: Absence of price anchors, insufficient liquidity, oracle time discrepancies, regulatory uncertainties, and expectation pricing with emotional amplification

Outlook and Conclusion: Perpetual contracts are entering their second phase, transforming from crypto-native leverage tools to global asset pricing infrastructure

Perpetual contracts are one of the most typical native products in the crypto market. They have no expiry date and use a funding fee mechanism to keep contract prices fluctuating around the underlying price, allowing users to hold long and short exposures in a margin form. For traders, they are leverage tools; for exchanges, they are a core source of fees and liquidity; for the market, they are a high-frequency expression of crypto asset price discovery and risk preferences. However, recent developments indicate that perpetual contracts are undergoing deeper changes. They are no longer just trading tools for BTC, ETH, SOL, or altcoins; they are beginning to enter prediction markets, Pre-IPO valuations, commodity prices, stock indices, and RWA assets. The boundaries of perpetual contracts are expanding from "crypto leverage tools" to "global risk asset pricing tools."

I. Role Reshaping: From Crypto Native Tools to Compliant Financial Products

The initial advantage of perpetual contracts arose from the structure of the crypto market itself. The 24/7 trading, cross-border flow, high volatility, and fragmented spot market of crypto assets make them inherently suitable for perpetual contracts, which have no expiry, adjust funding rates, and facilitate margin trading.

1.1 Changes in the Landscape of Crypto Market Perpetual Contracts

In recent years, CEX perpetual contracts have long been the core revenue for exchanges like Binance, OKX, Bybit, and Bitget; DEX perpetual contracts have gone through multiple iterations from dYdX, GMX, Drift, and Jupiter perpetual contracts to Hyperliquid.

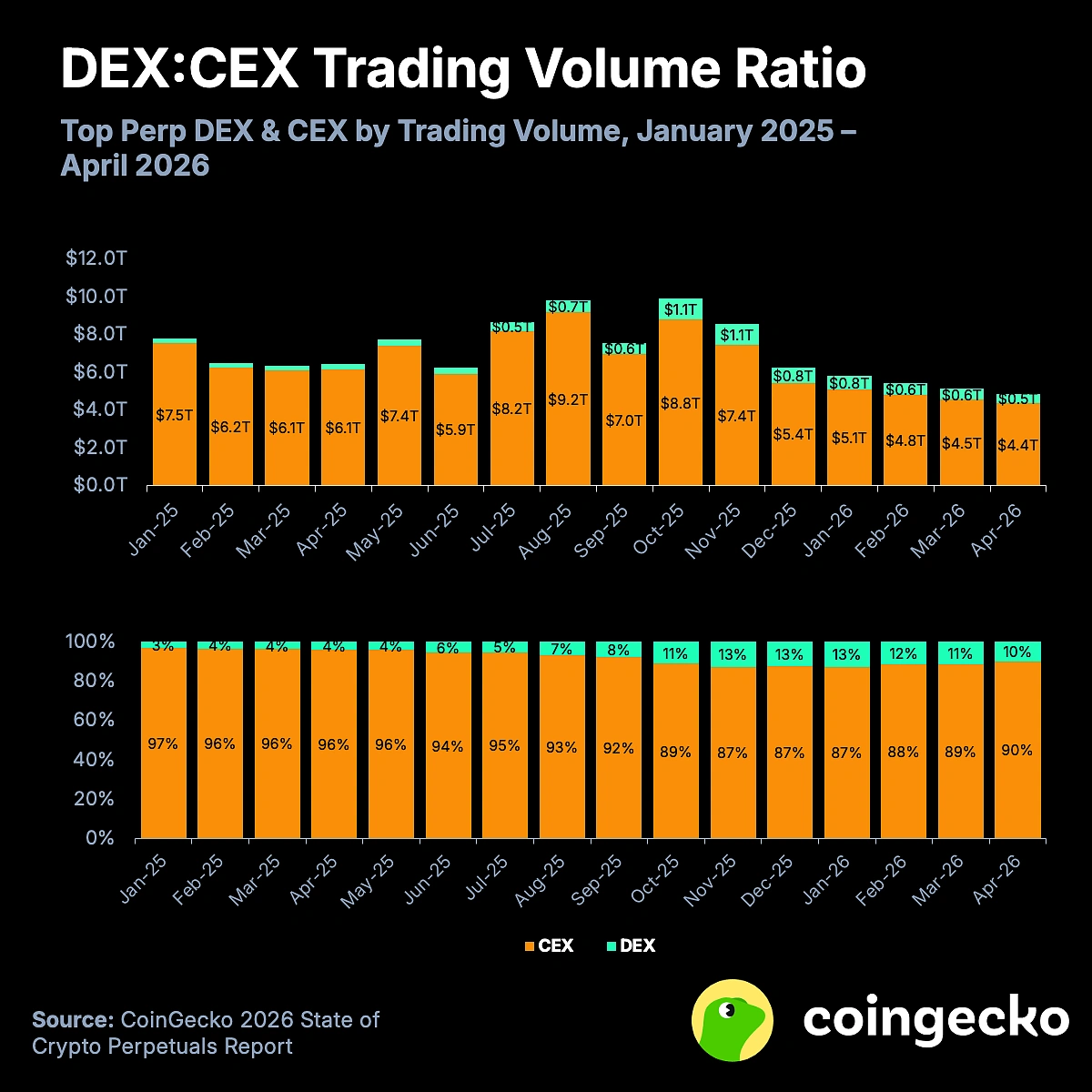

The 2026 Crypto Perpetuals Report published by CoinGecko shows that CEX remains the absolute main entrance in the perpetual contract market. However, since 2025, the market share of DEX perpetual contracts has been steadily increasing, currently stabilizing between 10%-13%. While CEX still occupies an absolute dominant position, on-chain infrastructures like Hyperliquid are continuously eating into the market share of centralized exchanges.

Source: https://www.coingecko.com/research/publications/state-of-crypto-perpetuals-report-2026

1.2 US Regulation Begins to Establish Compliance Pathways for Perpetual Contracts

On May 29, the CFTC approved the listing of BTCPERP contracts on KalshiEX and included them in the futures contract regulatory framework. This marks the first time in the US that a clear regulated listing case for crypto perpetual contracts has been provided, indicating that a compliant perpetual futures market is starting to emerge within the country. On the same day, CFTC staff issued an explanatory letter and no-action letter to Coinbase Financial Markets, confirming that some crypto asset perpetual contracts may be treated as offshore futures, and allowing eligible FCMs to transfer customer crypto assets to offshore brokers as margin. This provides another compliant pathway for US customers to access the global crypto derivatives market through regulated intermediaries.

This changes the market positioning of perpetual contracts. In the past, perpetual contracts were mainly seen as high-leverage trading tools for the offshore crypto market; now, as the US regulatory framework becomes clearer, perpetual contracts are accelerating their integration into the mainstream financial system.

1.3 Institutions Begin Pricing On-Chain Derivatives Platforms

Institutional capital is entering the on-chain perpetual contract space in the form of ETFs. After 21Shares launched THYP and TXXH, Bitwise launched BHYP, and Grayscale introduced HYPG with management fees as low as 0.29%. Unlike traditional crypto ETFs, the underlying assets of these products are not Bitcoin or Ethereum, but Hyperliquid — currently one of the largest on-chain perpetual contract trading platforms.

This means that the market is beginning to view on-chain derivatives exchanges themselves as investable assets. Investors are no longer just allocating HYPE tokens but are also investing in the trading volume, fee income, liquidity network, and ecological growth represented by Hyperliquid. If Bitcoin ETFs have allowed Bitcoin to become an asset that can be allocated in traditional finance, then HYPE ETFs signify that on-chain perpetual contract platforms are entering institutional portfolios.

II. Asset Boundary Expansion: From Crypto Native Assets to RWA, Pre-IPO, and Event Markets

If regulation and the emergence of ETFs mean that perpetual contracts are beginning to gain mainstream financial recognition, it is even more noteworthy that the scope of assets they carry is also changing. From commodities and stocks to valuations of unlisted companies and event markets, more and more risk assets that traditionally belonged to the financial system are starting to enter the perpetual contract framework.

2.1 RWA Perpetual Contracts

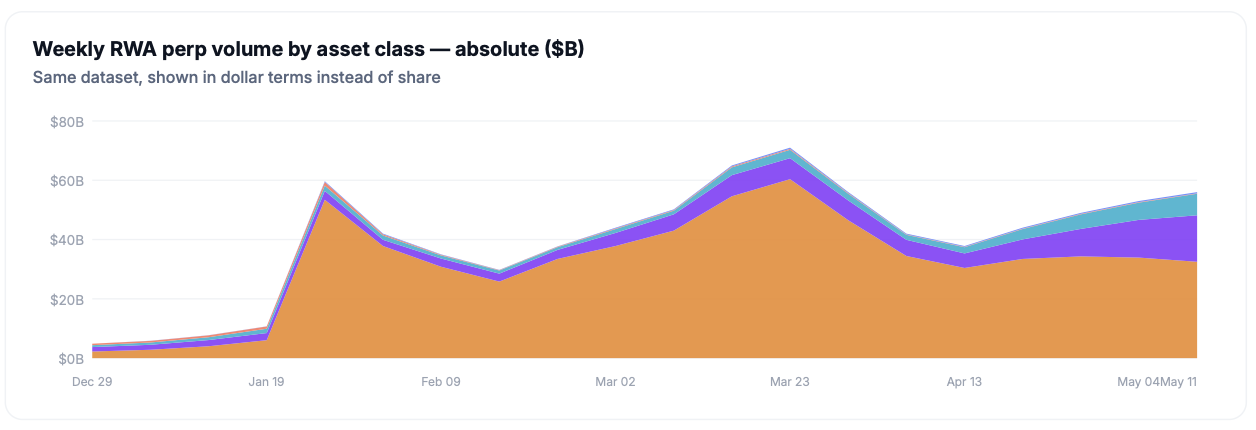

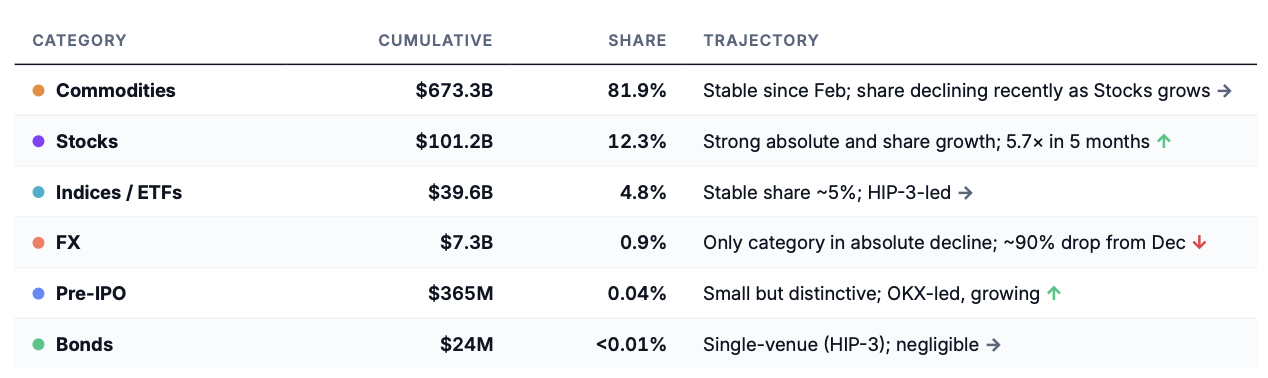

According to the "RWA PERPETUALS State of the Market" report released by CoinMarketCap Research in May 2026, cumulative trading volume of non-crypto asset perpetual contracts (RWA Perpetuals) has reached $821.8 billion among the 17 centralized and decentralized trading venues surveyed, indicating that this market has gradually moved from the proof-of-concept phase to scaled trading.

Source: https://coinmarketcap.com/academy/article/rwa-perpetuals-state-of-the-market-%E2%80%94-may-2026

From an asset structure perspective, commodities are the absolute core of the current RWA perpetual contract market. Gold, silver, WTI crude oil, and Brent crude oil commodities account for about 81.9% of the cumulative trading volume. These assets have established spot markets, a unified global pricing system, and a long-standing demand for risk hedging, making them the easiest to be carried by perpetual contracts.

Stock assets contribute about 12.3% of the trading volume, ranking second. Trading is primarily focused on high-profile tech and growth stocks such as Tesla, NVIDIA, Circle, and Intel. Compared to the commodity market, stock perpetual contracts rely more on individual stock narratives and event-driven factors, but as on-chain traders' demand for US stock risk exposure increases, their growth rate is noticeably faster than other asset classes.

Index and ETF assets account for about 4.8%, mainly including the S&P 500, NASDAQ 100, and related ETF products. These assets are closer to Beta exposure trading tools in traditional financial markets, with transparent pricing sources and relatively easier oracle implementation, making them an important direction for future institutional funds' entry into the on-chain derivatives market.

Forex perpetual contracts currently account for only about 0.9%, with underlying pairs including USDJPY, USDTRY, etc. Due to the traditional forex market itself having extremely high liquidity and a mature leverage system, on-chain forex perpetual contracts have not yet shown significant advantages, and their overall scale remains relatively limited. Pre-IPO and bond perpetual contracts account for less than 0.1% of trading volume and have yet to form an effective market.

Overall, the current RWA perpetual contract market exhibits a distinct structure characterized by "commodity-driven, stock growth, and index exploration". What concerns the market most is not necessarily the highest trading volume, but rather traditional risk assets with established pricing systems and global liquidity that truly support the development of RWA Perpetuals.

2.2 Pre-IPO Perpetual Contracts

In May 2026, Pre-IPO perpetual contracts began to be launched intensively. On May 7, OKX launched pre-market perpetual contracts such as SPACEX/USDT, OPENAI/USDT, and ANTHROPIC/USDT; on May 17, Hyperliquid's ecological project Trade.xyz introduced the SpaceX Pre-IPO perpetual contract; on May 21, Binance launched pre-IPO perpetual contracts and successively introduced related products based on expectations of public market valuations for SpaceX and OpenAI. Additionally, Hotcoin has also launched pre-market perpetual contracts for SPACEX, OPENAI, ANTHROPIC, and ANDURIL, reflecting that the trading targets of perpetual contracts are expanding from crypto assets to unlisted company valuation expectations.

The essence of these products is not trading stocks but trading expectations of unlisted company valuations. SpaceX, OpenAI, and Anthropic do not have publicly traded stock prices, nor can equity freely circulate. Therefore, Pre-IPO perps are more akin to "synthetic price markets established around IPO expectations". Their value lies in allowing users to express judgments on unicorn valuations early; the risk is that the price anchor is highly fragile.

On May 28, the SPACEX-USDH perpetual contract on Hyperliquid dropped from $2,277 to $1,254 within about 30 minutes, a decrease of approximately 45%, triggering approximately $1.51 million in nominal value liquidation. This incident indicates that while Pre-IPO perpetual contracts provide a new channel for valuation discovery of unlisted companies, in the absence of publicly available price anchors, their prices are more susceptible to liquidity, expectation changes, and market sentiment shocks, leading to more fragile price discovery mechanisms.

2.3 Perpetualization of Event Markets

Traditional prediction markets trade on discrete event outcomes, such as election results, economic data, policy approvals, and sports results. Users buy and sell the probabilities of these events occurring, with the market ultimately settling on "yes" or "no". In contrast, perpetual contracts trade on continuous prices, with their core mechanism being to maintain a balance between market prices and reference prices through funding rates. In the past, these two types of markets had completely different product forms and user bases. However, in 2026, these boundaries began to blur.

In April, Polymarket announced it would launch perpetual contract products; in May, Hyperliquid launched Offchain Event Contracts, beginning to explore the price trading of macro events and specific events; in the same month, Kalshi announced plans for regulated perpetual contract products and intends to launch multiple crypto asset perpetual contracts. Prediction market platforms have begun to introduce perpetual contract mechanisms, while perpetual contract platforms are also starting to explore event trading, with the previously independent development tracks gradually converging.

The essence of the underlying changes in this trend is that what the market focuses on is shifting from "event results" to "event expectations": how the market's expectations of the event change and whether these expectation changes create trading opportunities. This indicates that the core capability of perpetual contracts is no longer "leverage," but rather "turning any quoted expectation into a continuous market." As long as a certain target has sufficient market attention, can form price references, and can maintain trading through funding rates or contract mechanisms, it has the potential to be included in the perpetual contract framework.

III. Platform Route Differentiation: The Battle for Entry Among CEX, Perp DEX, Prediction Markets, and ETF Issuers

In the past, users could only access the perpetual contract market through exchanges. In the future, exchanges, Perp DEX, ETFs, and prediction markets may jointly constitute a multi-layered entry system.

3.1 CEX: Still the Absolute Main Entrance, But Expanding Towards RWA and Pre-IPO

CEX remains the liquidity core of the perpetual contract market. Data from CoinGecko shows that in the first four months of 2026, the Top 11 Perp CEX had an average monthly trading volume of $4.69 trillion, accounting for about 90% of the total trading volume in the perpetual contract market; among them, Binance and OKX hold shares of 33% and 15%, respectively, in the Perp CEX market. Despite rapid growth in on-chain perpetual contracts in recent years, the current market landscape still exhibits significant centralization characteristics, with the vast majority of trading activity, liquidity, and price discovery processes concentrated in leading exchanges.

The advantages of CEX are threefold. First, deep liquidity. Mainstream exchanges can quickly aggregate market makers and user orders. Second, high product listing efficiency. Third, a mature risk management system. CEX already has margin, forced liquidation, funding rates, risk control limits, and user stratification mechanisms.

However, CEX also has obvious weaknesses: lower transparency, platform pricing methods dependent on centralized rules, and users needing to trust the exchange's settlement and risk parameters. When CEX lists Pre-IPO perpetual contracts that do not have a public spot anchor, how the platform sets index prices, funding rates, and post-IPO settlement rules becomes a core issue.

3.2 Perp DEX: Hyperliquid Stands Out, But Competition Has Just Begun

The core platform on the DEX side is Hyperliquid. According to CoinGecko data, Hyperliquid currently accounts for about 3.9% of the total trading volume among all perpetual contract exchanges, ranking ninth among all CEX and DEX perpetual contract platforms; simultaneously, it holds over 50% of the open interest in DEX perpetual contracts, making it the most dominant platform in the current on-chain perpetual contract market.

Hyperliquid's uniqueness lies in that it is not a simple AMM, but an on-chain order book based on its own L1. Its advantages are that the trading experience is close to that of CEX while retaining on-chain settlement, transparency, and ecological expansion capabilities. HIP-3 further allows third parties to deploy more RWA, indices, commodities, and Pre-IPO markets, indicating that Hyperliquid's positioning is expanding from a single crypto perpetual contract DEX to a multi-asset perpetual contract infrastructure.

However, DEX competition is not over. Emerging Perp DEXs such as Pacifica, Extended, and Variational continue to fight for market share and have surpassed established on-chain derivatives markets such as Jupiter and dYdX. Lighter, edgeX, Aster, Ostium, and Avantis are also making moves in various sub-tracks.

The advantages of DEX include transparency, global accessibility, rapid asset innovation speed, and the ability to absorb stablecoin capital from crypto-native users. However, weaknesses include: oracles, liquidation, MEV, depth of market making, system risk control, and on-chain execution costs remain long-term challenges. The flash crash of the Hyperliquid SpaceX perp indicates that even leading Perp DEXs with strong order book capabilities may expose liquidity and liquidation risks when the underlying asset lacks a spot anchor.

3.3 Competition for New Entrances: ETFs and Prediction Markets are Competing for Users

The competition in the perpetual contract market is evolving from competition among trading products to competition for user entrances. In the past, if users wanted to gain leverage exposure to crypto assets, they usually had to trade through centralized exchanges like Binance, Hotcoin, or on-chain perpetual contract platforms like Hyperliquid. However, with the development of ETFs and prediction markets, an increasing amount of capital is entering the perpetual contract ecosystem through new channels.

ETFs are among the most typical representatives of this trend. Institutions such as 21Shares, Bitwise, and Grayscale have successively launched or applied for HYPE ETFs, indicating that traditional investors no longer need to directly use Hyperliquid, manage wallets, or participate in on-chain trading to gain risk exposure to on-chain derivative infrastructure via securities accounts. For institutional funds, ETFs provide a more familiar and compliant participation path; for on-chain protocols, it signifies that exchanges are being viewed as investable assets themselves.

At the same time, prediction markets are also beginning to expand into the perpetual contract field. Polymarket announced the launch of perpetual contract products, and Kalshi introduced products like BTCPERP after obtaining regulatory approval. Prediction market platforms are attempting to extend from "event outcome trading" to "continuous price trading," while perpetual contract platforms are also exploring pricing expressions of macro events, policy expectations, and real-world events.

From a longer-term perspective, future competition may no longer be between CEX and DEX but rather a struggle among different entrances for user, liquidity, and price discovery rights. Exchanges, on-chain protocols, ETF issuers, and prediction market platforms are all trying to become important entrances to the next-generation global risk asset trading network.

IV. The Dual Attributes of Perpetual Contracts: 24/7 Price Discovery and Risk Amplification

As regulatory boundaries, asset boundaries, and market entrances continue to expand, perpetual contracts are evolving from single crypto derivatives to global risk asset trading infrastructure. Their value is no longer limited to providing leverage but lies in their ability to continuously provide trading, price discovery, and liquidity aggregation capabilities for various assets and expectations. However, the expanding asset coverage and increasingly complex market structure also mean that new risks are being introduced into this system.

4.1 Value Reconstruction: From Trading Tool to Global Price Discovery Layer

The expansion of perpetual contract boundaries reflects a change in role positioning. In the past, perpetual contracts primarily served leveraged trading of crypto assets; today, as commodities, stocks, indices, Pre-IPO assets, and event markets gradually enter the perpetual contract framework, their functions are evolving toward a broader price discovery layer.

24/7 Price Discovery Capability: Traditional financial markets have fixed trading hours, and when significant events occur at night, on weekends, or in cross-timezone markets, prices often cannot reflect immediately. In contrast, the perpetual contract market can operate continuously, providing global investors with a real-time risk pricing mechanism. Research from TD Securities shows that the oil-related market on Hyperliquid has already reflected about 80% of oil price changes before the traditional market opens, showcasing the potential of on-chain markets as a supplementary price discovery layer.

Global Liquidity Aggregation: Stablecoin settlement lowers the barriers for cross-border trading, allowing users from different countries and regions to trade the same risk asset in the same market. For crypto-native users, they do not have to leave the on-chain ecosystem to gain exposure to traditional financial assets like gold, crude oil, stock indices, and Pre-IPO valuations.

Capital Efficiency Increase: Perpetual contracts do not require holding underlying assets or involve physical delivery, allowing for risk exposure and asset allocation at a lower cost. Compared to the complex account opening, custody, and settlement systems in traditional markets, perpetual contracts provide a more efficient trading method for global investors.

Asset Innovation Capability: The gradual entry of commodities, stocks, indices, Pre-IPO assets, and even event markets into the perpetual contract framework indicates that perpetual contracts have evolved from a single crypto product into a generic trading container. More assets and expectations that were previously difficult to directly put on-chain or lacked liquidity are gaining price discovery and trading capabilities through perpetual contracts.

However, the greater the value of perpetual contracts as price discovery tools, the wider the risk impact range. As more assets and markets lacking a unified pricing system are incorporated into the perpetual contract framework, the boundaries between price discovery and price distortion are becoming increasingly blurred.

4.2 Risk Spillover: From Leveraged Volatility to Expectation Distortion

The expansion of perpetual contracts does not mean that risks disappear; on the contrary, the sources of their risks are becoming more complex.

Absence of Price Anchors: BTC and ETH have established spot markets, and gold and oil have globally unified pricing systems, but underlying assets like SpaceX, OpenAI, and Anthropic do not have a continuously publicly traded spot market. Their prices rely more on financing valuations, over-the-counter quotes, media information, and market sentiment. In the absence of reliable price anchors, so-called price discovery can easily devolve into expectation games.

Long-Tail Asset Liquidity Insufficiency: In May 2026, the SpaceX perpetual contract on Hyperliquid dropped by about 45% within about 30 minutes, triggering large-scale liquidations. This event illustrates that even on leading on-chain trading platforms, Pre-IPO and long-tail RWA assets may experience severe volatility due to liquidity shortages, concentrated holdings, or liquidation mechanisms.

Oracle and Market Time Discrepancies: Stocks, commodities, and indices generally have fixed trading hours, while on-chain perpetual contracts typically support 24/7 trading. When the underlying reference market is closed, price updates will rely more on oracles and market expectations, potentially leading to early price reflections, opening gaps, and funding rate distortions. For key windows like earnings reports, macro data releases, and unexpected events, oracle delays themselves may become sources of risk.

Regulatory Boundary Uncertainties: While the gradual entry of crypto perpetual contracts into regulatory frameworks is a positive signal, the regulatory issues involving RWA perpetual contracts, single-stock perpetual contracts, Pre-IPO perpetual contracts, and event perpetual contracts are much more complex. Single-stock products may touch upon securities regulations, Pre-IPO products may involve restrictions on private equity transfers, while prediction markets may simultaneously face constraints from commodity regulation, gambling regulation, and state-specific regulations.

Expectation Pricing and Emotion Amplification: As event markets, Pre-IPO markets, and real-world assets continue to enter the perpetual contract framework, the targets of market trading are expanding from "asset prices" to "future expectations." As prices increasingly depend on expectations rather than spot anchoring, perpetual contracts can become efficient price discovery tools but can also amplify sentiment and narrative fluctuations.

Therefore, the future of perpetual contracts is not solely about expanding more asset categories but finding a new balance among asset innovation, liquidity depth, price anchoring, and regulatory frameworks. They could become the 24/7 pricing layer for global risk assets, or they might become a new leverage system for amplifying market sentiment and expectation fluctuations.

V. Outlook and Conclusion: The Second Phase of Perpetual Contracts, Global Risk Asset Pricing Infrastructure

Current perpetual contracts are entering their second phase.

The first phase involved crypto-native leverage tools. It mainly served BTC, ETH, and crypto token trading, with core competition surrounding liquidity, leverage multiples, transaction fees, and listing speed. In this phase, perpetual contracts were one of the most important revenue sources for crypto exchanges and served as a core tool for the market to express long and short views.

From the series of changes since 2025, it is evident that perpetual contracts are transitioning to their second phase — global risk asset pricing infrastructure. Commodities, stocks, indices, Pre-IPO, event markets, and RWA assets are gradually entering the perpetual contract framework; US regulators are beginning to explore compliant pathways; on-chain perpetual contract platforms are gaining institutional attention; ETF issuers are starting to include Perp DEXs as investment targets. The focus of competition for perpetual contracts is shifting from “who offers higher leverage” to “who can carry more assets, more liquidity, and more price discovery.”

Three signals are worth continuing to monitor in the future:

Whether the market structure continues to migrate on-chain: Currently, CEX still occupies about 90% of perpetual contract trading volume, but DEXs have shown stronger expansion capabilities in the RWA and innovative asset fields. If the open interest on-chain continues to increase, it indicates that perpetual contracts are evolving from a trading market to a risk-bearing market.

Whether non-crypto assets can become new growth engines: Currently, RWA perpetual contracts are still dominated by commodities like gold, silver, and crude oil, while stocks, indices, and Pre-IPO markets are still in the early stages. If these asset classes can form sustained liquidity, perpetual contracts will further enter the traditional financial asset pricing system.

Whether the compliance framework can continue to improve: The Kalshi BTCPERP, Coinbase obtaining CFTC no-action status, and the emergence of HYPE ETFs all indicate that regulation and institutional capital are starting to enter this field. However, what ultimately determines the market ceiling remains the price discovery mechanism, liquidity depth, and regulatory sustainability.

Conclusion

Perpetual contracts initially solved a technical problem—how to achieve continuous trading without an expiry date. But today, as perpetual contracts begin to take on more pricing functions of traditional financial markets, their boundaries are no longer determined by asset categories but by price discovery capability. Any asset or expectation that can form market consensus, gain liquidity support, and continue to attract attention has the potential to be included in this framework.

Therefore, what truly deserves attention in the future may not be who has launched more trading pairs or who has offered higher leverage, but rather who can establish the most credible prices, aggregate the broadest liquidity, and gain dual recognition from regulators and the market. The ultimate outcome of the competition in perpetual contracts may not just be a contest of trading tools, but a struggle for global asset pricing power.

About Us

Hotcoin Research, as the core investment research institution of Hotcoin Exchange, is dedicated to turning professional analysis into your practical tools. We analyze market trends through "Weekly Insights" and "In-Depth Reports"; leveraging our exclusive column "Hotcoin Selected" (AI + expert dual screening), we help you identify potential assets and reduce trial-and-error costs. Every week, our researchers also engage with you through live streams, interpreting hot topics and predicting trends. We believe that warm companionship and professional guidance can help more investors navigate cycles and seize the value opportunities of Web3.

Risk Warning

The cryptocurrency market is highly volatile, and investment itself carries risks. We strongly recommend that investors invest with a full understanding of these risks and within a strict risk management framework to ensure fund safety.

Website: https://www.hotcoin.com/zh_CN/learn/index/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。