Written by: Yajin

On April 29, 2025, Mastercard held a press conference at its headquarters in Purchase, New York, officially announcing the "Agent Pay" product [3]. There was no sensational reaction on that day, with the industry mostly treating it as another routine announcement from the card organization. Over the next 12 months, things became unusual. In May, Coinbase released x402, using the HTTP status code 402, which had been reserved since 1998 but never used, for the first time for real, allowing USDC transfers to be embedded directly in HTTP responses [1]. Two months later, Cloudflare launched Pay per Crawl using the same status code, introducing per-call pricing for AI crawlers [9], indicating that the idea of "paying with HTTP 402" spread from the crypto circle to content providers. Two months later, the protocol layer joined the fray: in September, Google collaborated with over 60 companies to launch AP2, while OpenAI and Stripe simultaneously introduced ACP, enabling ChatGPT for the first time to directly complete checkout for users on Etsy during conversations [2][4]. In October, card organizations themselves entered the game, with Visa and Cloudflare jointly releasing TAP, which for the first time issued a verifiable card organization identity to agents [5].

Entering 2026, the entire track shifted from "scattered emergence" to "standardization." In February, Lightning Labs adapted the 402 idea to Bitcoin and created L402 [8]. In March, Stripe and Paradigm jointly launched MPP, while Tempo's mainnet went live, and 12 days later, the entire scheme was submitted to the IETF for standardization [6]. In April, the Linux Foundation took over the x402 Foundation, with over 20 founding members including card organizations (Visa, Mastercard, American Express), cloud vendors (AWS, Google, Microsoft), and crypto infrastructure (Coinbase, Circle, Stripe), three camps that were originally competing with each other [1]. This was the first time a payment protocol had endorsements from all three camps on the same stage.

Within a year, six new payment protocols + three revival plans for HTTP 402 + IETF standardization emerged, driven by one common incentive: AI agents began to have their own payment needs. This new demand gave rise to the entire track, which the industry began to uniformly refer to as Agentic Payment: allowing agents to act as independent payment entities that are recognized, authorized, settled, and accountable. The fundamental assumption of "the final decision maker is a person," which has been in place for 60 years, has changed for the first time.

This series of five articles will break down this matter. This article will first clarify the background: where the traditional payment stack stands and which areas each of the three forces are targeting. The next three articles will each focus on one of the engineering paths, with the final article doing a horizontal comparison.

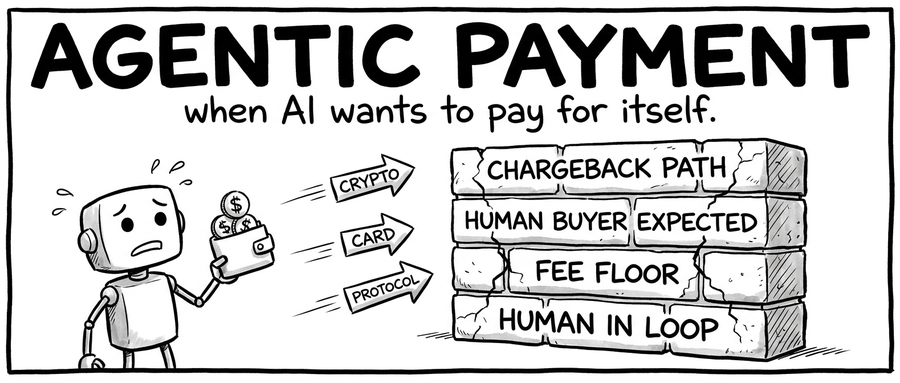

Why the Traditional Payment Stack is Not Suitable for Agent Payments

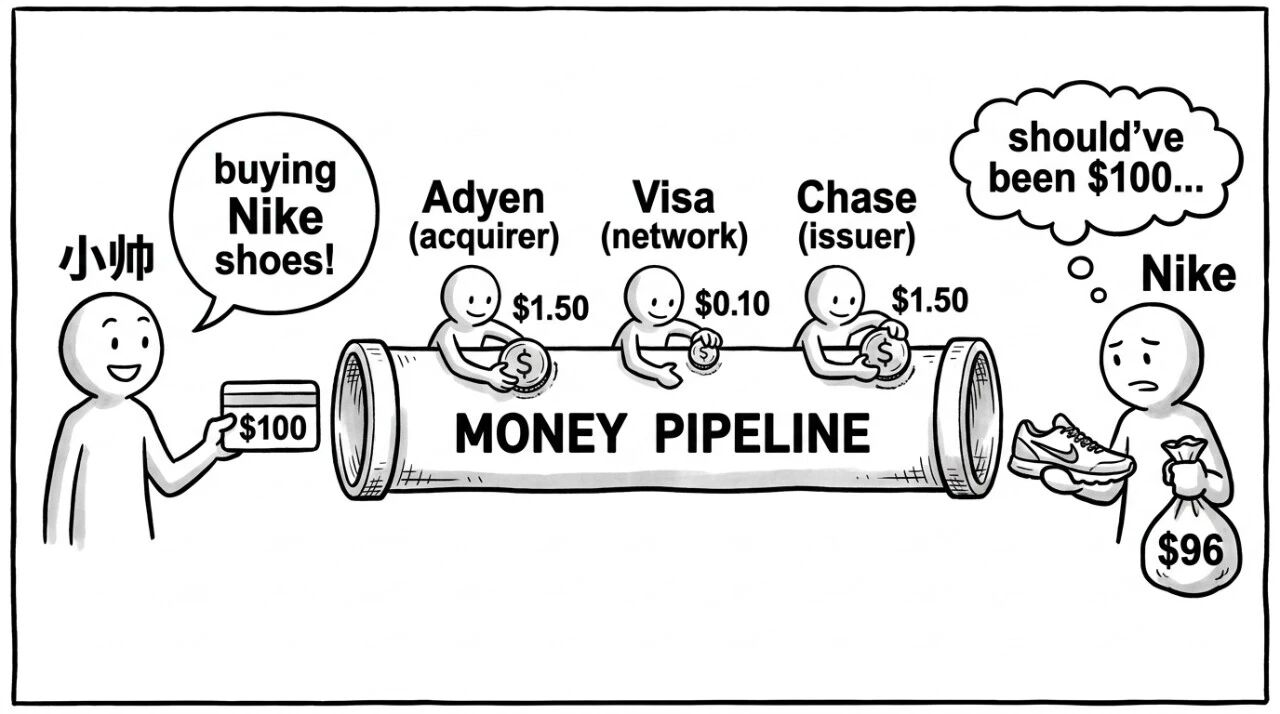

To understand why protocols have emerged, let's first look at how money flows in a traditional consumer payment. For example, Xiao Shuai is a running enthusiast who buys running shoes on the Nike website using a Visa credit card. The issuing bank (issuer, possibly Chase) is behind the card number. The merchant Nike cannot process card payments directly; it must pass the transaction to the acquiring bank (acquirer, such as Adyen). Adyen sends the transaction through the Visa network to Chase. Chase deducts $100 from Xiao Shuai's account, and part of that $100 will remain as a fee: for a $100 transaction, the issuer takes about 1.5% (called interchange), Visa collects about 0.1% (called network fee), and Adyen takes about 1.5% (called processing fee). Finally, approximately $96 goes to Nike's account.

This 3-4% is not paid by Xiao Shuai, but by Nike (Xiao Shuai's card is still deducted $100, and Nike actually receives $96). Why is Nike willing to pay this cost? Because card organizations have accumulated a nearly irreplaceable asset over the past sixty years: chargeback. This mechanism provides a safety net for consumers like Xiao Shuai, enabling them to place orders online and from unfamiliar merchants with confidence. If Xiao Shuai discovers that the running shoes are the wrong model, that Nike has not shipped the order, or that there is an unauthorized charge on his card, he can call Chase to initiate a dispute. The card issuer, Visa, Adyen, and Nike together follow a long-established arbitration process, and if the dispute is successful, he can get his money back. Nike pays 3-4% for this consumer trust.

The premise of this entire mechanism is based on several assumptions that payment stack engineers have accepted since the 1960s: first, humans are in the loop. The fundamental assumption of each card payment is that "the final decision maker is a person," so the chargeback safety net is meaningful, and KYC (Know Your Customer) can be assigned to a natural person. Second, a single transaction amount is economically viable enough to support fees. Visa/Mastercard card rails run a transaction end-to-end, and the standard quotation for acquirers to merchants is approximately 2.9% + $0.30. This is reasonable for a $100 retail purchase. In a $0.005 priced API call/data endpoint/crawler request, it is economically unfeasible: the fee exceeds the transaction cost by 60 times.

Third, merchants expect buyers to be human. Merchants' anti-fraud models, inventory strategies, and customer service processes assume that buyers are human beings with IP histories, device fingerprints, and genuine consumption habits. Fourth, the chargeback chain must be connectable. The dispute procedures of card rails assume that buyers can describe "I didn't buy this" or "it doesn't match the description." The three questions, "who is the buyer, what was purchased, and where is the error," have been clear in retail consumption over the past 60 years.

LLM agents break all four of these assumptions simultaneously. Imagine an AI research agent completing a task: it needs to pull content from dozens of webpages, query several paid data endpoints, and purchase one or two small reports, with each action priced between $0.001 and $0.10. No human presses the "confirm" button for these actions, and the cost per transaction is far below the $0.30 threshold of card rails; merchants are not dealing with humans, and in case of issues, they cannot even describe "who authorized what." All four assumptions fail.

AI reasoning services like Anthropic, OpenAI, and Replicate can currently operate based on a "prepayment + internal measurement" model: they bundle thousands of API calls into one large card payment to bypass the lowest fee rate constraint of card rails. However, once an agent begins to buy reports, subscribe to tools, and sign API contracts on its own, this architecture breaks down.

More direct signals come from content providers. Cloudflare revealed in its AI Crawl Control report in August 2025 that their clients' websites returned more than 1 billion HTTP 402 status codes on average per day [9]; publishers used this simplest form to inform AI bots: "You must pay to see the content." The issue is that the HTTP 402 status code has been reserved since the 1998 HTTP/1.1 standard and has never led to a widely adopted payment protocol. When AI bots receive it, they treat it merely as a general access denial error and cannot convert it into real payments. The new protocols x402, Pay per Crawl, and L402 aim to solve this problem: to add a genuinely functioning protocol layer atop HTTP 402 that enables AI bots to automatically check out.

Another set of critical data within the same ecosystem: traditional search engines direct readers to the original website, while AI crawlers do not. According to Cloudflare's statistics from June 2025, Google sends back one visit for every 14 crawls, while OpenAI's bot has a ratio of 1700:1, and Anthropic's bot reaches as high as 73000:1 [9]. After AI crawlers retrieve content, they directly provide answers within platforms like ChatGPT and Claude, meaning users will not visit the original site. The past path where publishers relied on "being searched → users clicked → ad monetization" has completely broken.

Putting these signals together: the traditional payment stack cannot handle the high-frequency micropayments of agents, AI reasoning services can only bypass with prepayment, and content providers receive neither crawlers’ payments nor users’ traffic. On one side, agents must have payment capabilities; on the other side, merchants/publishers must have methods to receive agents' money, with traditional payment protocol stack's four assumptions standing in between. The gap is large enough that the three types of players almost simultaneously noticed it and jumped in, each providing three different approaches with their respective judgments and assets.

Three Forces, Three Approaches

The three approaches correspond to three commercial logics, each targeting different aspects of the traditional payment stack that have been disrupted. This section will clarify their stances, while the engineering details of the three paths will be broken down in the following three articles.

Crypto Native Path: Bypassing Card Rails, Using Stablecoins Directly

Since card rails cannot economically support transactions under 1 cent, the solution is to bypass them and use stablecoins for on-chain settlements. The first to scale this approach is Coinbase with its release of x402 in May 2025. It embeds USDC transfers directly into HTTP 402 responses: when an agent requests resources, the server returns 402 + price, the agent authorizes it using a wallet to sign EIP-3009, and Coinbase's facilitator pays the gas on-chain. On the Base chain, gas costs less than $0.0001 per transaction, with settlements taking around 2 seconds. As of April 2026, when the Linux Foundation took over, x402 had processed a cumulative total of 165 million transactions, with about $50 million in total flow and 69k active agents, with Solana accounting for about 65% of transaction volume [1]. This number is relatively small in the traditional payment industry. In fiscal year 2025, Visa processed $14.5 trillion, approximately 260 billion transactions; Mastercard managed roughly $9.2 trillion for the year. The cumulative flow of x402 in its first year is roughly equivalent to what Visa processes in 2 minutes and Mastercard in 3 minutes. It appears small. However, it is essential to note that x402 is targeting a micropayment market that traditional card rails cannot cater to due to the minimum fee rate threshold, thus not competing on the same battlefield as Visa/Mastercard's traditional retail transactions.

The same concept is blossoming in other ecosystems. Lightning Labs applied it to Bitcoin, creating L402 [8]; Skyfire added a layer of KYC identity for agents to facilitate USDC stream micropayments; AI reasoning services like Anthropic use it for per-call billing [7]; Cloudflare's Pay per Crawl employs the same protocol layer for content providers to collect payments from crawlers, with publishers like Conde Nast/TIME/AP already on board [9]; Circle directly entered the field in May 2026 to promote Agent Stack for vertical integration.

In May 2026, AWS released Bedrock AgentCore Payments, which supports x402; it marks the first time a public cloud giant has natively supported agent payments. Specifically for API service providers, BlockSec has developed an x402 paid endpoint for on-chain address tagging and Phalcon compliance risk screening, with a starting price of $0.10 per call, settled in USDC on Base [1].

Transforming Credit Card Rails: Keeping the Rail, Only Changing the Credential

Card organizations are not planning to let agent traffic exit their rails, so they choose to change themselves. The representative solution is Mastercard's Agent Pay, released in April 2025 [3]. It doesn’t create anything new but integrates agent identities into their MDES tokenization infrastructure that has been in operation for ten years: MDES, originally used for virtual card tokens for Apple Pay and Google Pay, now has two added fields (agent identification + a session-scope object that specifies limits, merchant ranges, and expiration times). When ChatGPT or Microsoft Copilot uses Agent Pay to help users check out, the settlement route continues through card rails, preserving the interchange and chargeback dispute procedures entirely. The money continues to be divided under the old framework: card organizations collect interchange + network fees, issuers take the bulk of interchange, and acquirers/PSPs take processing fees. The moat lies in the chargeback safety net, a dispute resolution mechanism supported by decades of case law, for which there is still no equivalent alternative in the crypto path as of 2026.

Visa has taken a different approach: in October 2025, they collaborated with Cloudflare to launch the Trusted Agent Protocol, issuing verifiable identities to agents based on HTTP Message Signature/Web Bot Auth, with 12 partners including Adyen, Checkout.com, and Worldpay integrating for pilots [5]. Stripe selected a third path, transforming its existing Issuing product into "programmatically issuing one-time virtual cards for agents" [10], directly allowing agents to call the Stripe Issuing API to generate virtual cards to complete transactions, which forcibly aligns the minimum fee threshold of card rails with the high-frequency demands of agents.

Agent Protocol Layer: No Money Movement, Only Producing Intent Credentials

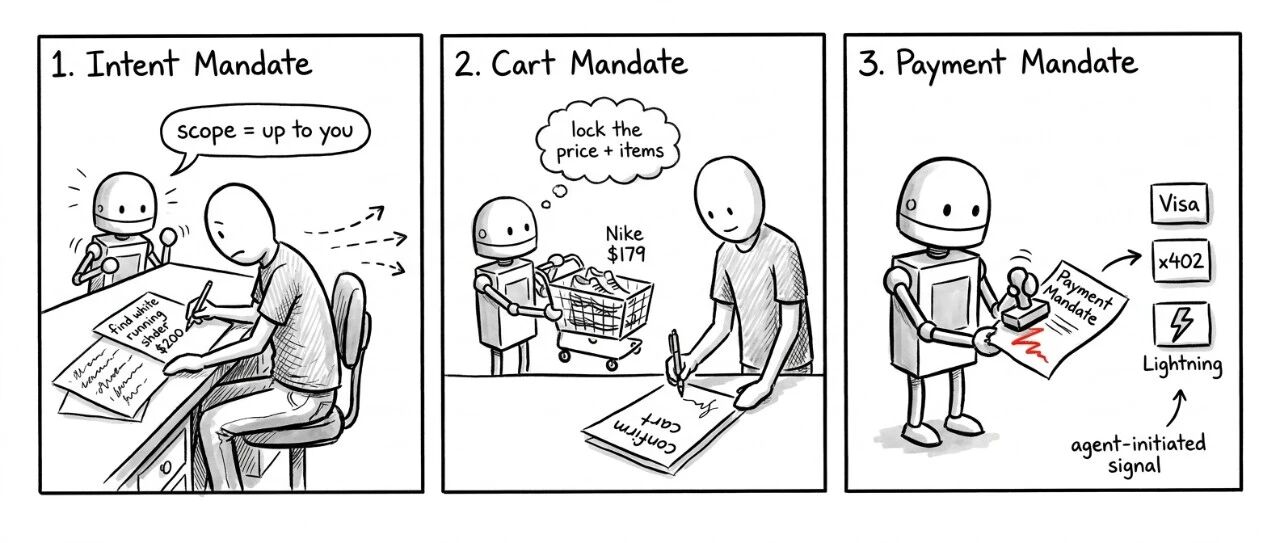

Neither undermining nor issuing new receipts, it standardizes the format of "intent credentials" exchanged between agents and merchants. The representative solution is AP2, launched by Google in September 2025 in collaboration with over 60 companies [2]. AP2 utilizes W3C Verifiable Credentials to divide the shopping process into three signed steps, with each step signing a cryptographic credential (collectively referred to as Mandate):

- 1. The user first signs Intent Mandate: instructing the agent "what to do" (for example, "find a pair of white running shoes under $200"). After signing, the user can leave, and the agent takes this authorization to search for products.

- 2. Once the agent finds specific products, it shows the shopping cart to the user, who signs the Cart Mandate in real-time when confirming: locking in what to buy and for how much.

- 3. At the moment the agent initiates the payment, it signs the Payment Mandate: instructing downstream parties (card organizations / chain / Lightning) "this payment is initiated by the agent on behalf of the user, process it according to this scope."

The three-layer signatures form a complete chain, with downstream rails, whether Visa card, x402 USDC or Lightning, all obtaining the same cryptographic evidence. AP2 itself does not settle; money does not flow through it; Google earns the right to set standards on this path: once AP2 becomes a de facto standard, all rails will attach on top of it. Coinbase and Lowe's have already demonstrated the complete shopping process with AP2 + stablecoins [2].

Simultaneously, OpenAI and Stripe launched ACP, taking a different path: directly converting ChatGPT into a shopping window. The Information later reported that OpenAI was charging Shopify merchants a platform fee of about 4% [4], marking the first time LLM vendors made money directly at the checkout layer. In March 2026, Stripe and Paradigm jointly released MPP, supporting their own Tempo chain and IETF standardization proposals [6]; OpenAI and Anthropic entered the list of design partners for MPP, a first in the history of any payment protocol design.

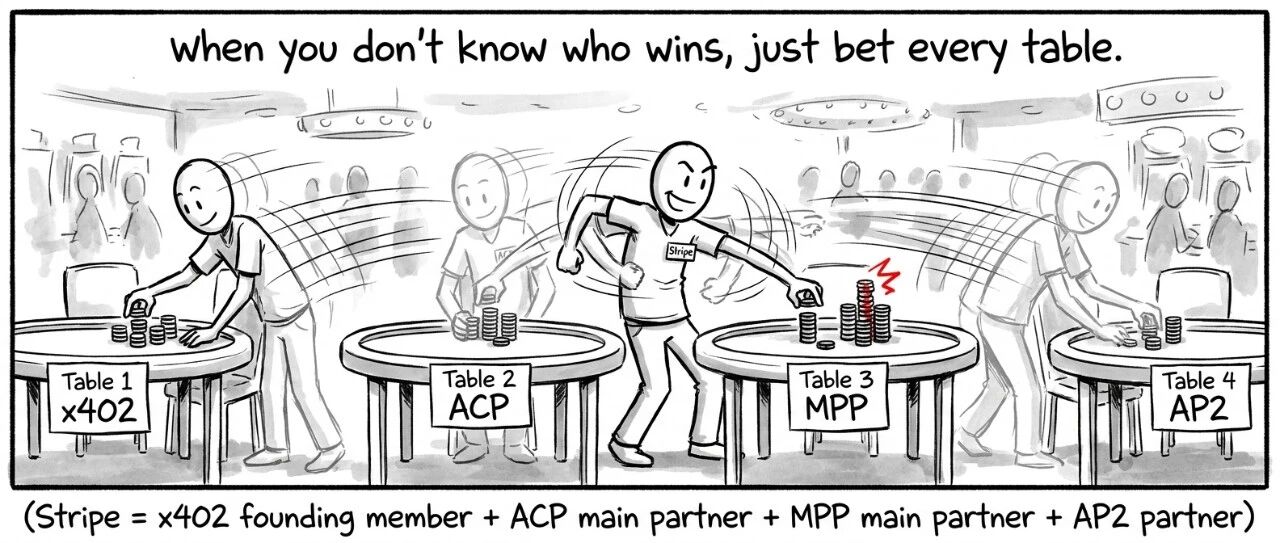

These three paths are not mutually exclusive. Stripe is simultaneously a founding member of the x402 Foundation, a key advocate for ACP, a main champion of MPP, and a partner of AP2, betting on all four standards. This itself is clear evidence of the uncertainty in the landscape for the first half of 2026 [6].

What to Discuss Next

The current landscape remains unclear, meaning all three paths are still testing their answers. Behind each path is a complete engineering structure, business model, customer demographic, and regulatory position, each linked to its own set of security risks, and they must be examined separately to enable comparison. The following articles will focus on this aspect. The second article will discuss the crypto native path. How did x402 activate HTTP 402, a "zombie status code" that had remained unused for 27 years? How can Skyfire turn KYC into the identity infrastructure of the agent era and pull in Anthropic for use? How did Cloudflare's Pay per Crawl create a paid market for publishers using the same status code? The common commercial judgment behind these three lines is that the traditional card rails can never come into the market for any transactions priced below 1 cent.

The third article will look at how card organizations are responding. Mastercard's Agent Pay inserts agent identities into its ten-year-old MDES tokenization framework, effectively adding a layer on its strongest asset; Visa's TAP issues verifiable identities to agents, echoing the traditional intuition of "I need to know who you are before allowing you to swipe a card"; and Stripe's issuing for agents programmatically issues one-time virtual cards, essentially forcing high-frequency micropayments onto card rails. The core issue behind these three stances is: during the agent era, does the legal definition of "cardholder" still hold?

The fourth article will shift to the protocol layer, where things have been surprising: protocols like AP2, ACP, and MPP do not move money but compete for the format standards of "intent credentials" in the agent era. AP2 chains together cryptographic signatures through three types of Mandates, ACP directly turns ChatGPT into a checkout interface, and MPP sends HTTP 402 into IETF standardization processes. Those who win at this level will become the OS on top of all rails.

The final article will make a horizontal comparison. It will place the three paths on the same table, comparing identity, funds, and dispute resolution; the uniquely impactful attack scenarios in the agent era; how the industry compensates for responsibility gaps while regulators remain silent; and what kind of industrial judgments are reflected behind Stripe's simultaneous betting on four standards despite seeming contradictions. If readers are still not familiar with certain payment terms by this point, they can glance at the quick reference table at the end before continuing; the remaining four articles in this series will assume that the reader already understands terms like chargeback, acquirer, issuer, interchange, merchant of record, token, and Mandate.

Terminology Quick Reference Table

References

[1] Coinbase. "Introducing x402." May 2025. https://www.coinbase.com/developer-platform/discover/launches/x402 ; Linux Foundation. "Launching the x402 Foundation." April 2, 2026. https://www.linuxfoundation.org/press/linux-foundation-is-launching-the-x402-foundation-and-welcoming-the-contribution-of-the-x402-protocol ; BlockSec x402 paid API (address tagging + Phalcon compliance screening endpoint, starting at $0.10 per call, settled in USDC on Base). https://x402.blocksec.ai/ ; Visa Annual Report FY2025 (SEC 10-K). https://investor.visa.com/ ; Mastercard FY2025 results. https://investor.mastercard.com/[2] Google Cloud. "Announcing Agent Payments Protocol (AP2)." September 16, 2025. https://cloud.google.com/blog/products/ai-machine-learning/announcing-agents-to-payments-ap2-protocol ; AP2 official documentation. https://ap2-protocol.org/

[3] Mastercard. "Unveils Agent Pay." April 29, 2025. https://www.mastercard.com/global/en/news-and-trends/press/2025/april/mastercard-unveils-agent-pay-pioneering-agentic-payments-technology-to-power-commerce-in-the-age-of-ai.html

[4] OpenAI. "Buy it in ChatGPT." September 29, 2025. https://openai.com/index/buy-it-in-chatgpt/ ; Agentic Commerce Protocol GitHub. https://github.com/agentic-commerce-protocol/agentic-commerce-protocol

[5] Visa. "Trusted Agent Protocol press release." October 14, 2025. https://investor.visa.com/news/news-details/2025/Visa-Introduces-Trusted-Agent-Protocol-An-Ecosystem-Led-Framework-for-AI-Commerce/default.aspx

[6] Stripe. "Developing an open standard for agentic commerce." 2026. https://stripe.com/blog/developing-an-open-standard-for-agentic-commerce ; Stripe. "Introducing the Machine Payments Protocol." 2026. https://stripe.com/blog/machine-payments-protocol ; IETF Internet-Draft "The Payment HTTP Authentication Scheme." https://datatracker.ietf.org/doc/html/draft-ryan-httpauth-payment-01 ; The Defiant. "Tempo launches mainnet, unveils Machine Payments Protocol with Stripe." March 2026. https://thedefiant.io/news/blockchains/tempo-launches-mainnet-unveils-machine-payments-protocol-with-stripe

[7] Skyfire. https://skyfire.xyz/ ; "Skyfire Launches Open KYAPay Protocol With Agent Checkout." June 26, 2025. https://www.businesswire.com/news/home/20250626772489/en/

[8] Lightning Labs. "The Agents Are Here." February 11, 2026. https://lightning.engineering/posts/2026-02-11-ln-agent-tools/

[9] Cloudflare. "Introducing pay per crawl." July 1, 2025. https://blog.cloudflare.com/introducing-pay-per-crawl/ ; Cloudflare. "Introducing AI Crawl Control." August 28, 2025. https://blog.cloudflare.com/introducing-ai-crawl-control/ ; Cloudflare. "The crawl before the fall... of referrals." June 2025. https://blog.cloudflare.com/ai-search-crawl-refer-ratio-on-radar/

[10] Stripe. "Giving agents the ability to pay." 2025. https://stripe.com/blog/giving-agents-the-ability-to-pay ; Stripe Issuing for agents docs. https://docs.stripe.com/issuing/agents

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。