In the past few days, the largest on-chain perpetual contract platform in the world by trading volume is undergoing a rare value discovery.

This platform is called Hyperliquid, and its token valuation has already surpassed Solana, closely following BNB. At least in terms of token prices, it is no longer at a disadvantage compared to centralized exchanges such as Binance.

However, there is a sword hanging over Hyperliquid.

At the end of May, the CFTC approved the first truly compliant perpetual contracts in the United States. Many see this as another victory for Hyperliquid, unaware that the clarity of the rules means that a group of more powerful enemies is on the way, and a protracted war has already begun.

CFTC Grants Amnesty for Contracts

On May 29, the CFTC approved Kalshi's listing for the first real Bitcoin perpetual contract BTCPERP. On the same day, it issued a no-action letter to CFM, a subsidiary of Coinbase, allowing the latter to connect U.S. customers to global options and perpetual contracts, with the pathway being through Coinbase's Bermuda entity, treated as "foreign futures," and allowing customers to use Bitcoin, Ethereum, and stablecoins as collateral. Accompanying measures included a committee policy statement regarding the listing of perpetual contracts, related explanatory guidance, and a staff guide covering 7×24 trading, clearing, and settlement.

CFTC Chairman Selig stated in a column that whether perpetual contracts exist has never been a question; the real question is whether they exist under U.S. regulation, standards, and the rule of law, or are driven offshore to grow unchecked. Trump claimed credit on Truth Social, stating that the former "anti-crypto army" nearly destroyed the U.S. crypto industry, and he saved it.

The Hyperliquid Policy Center, Hyperliquid's lobbying organization, welcomed this while expressing hope that this framework serves not only centralized intermediaries but also covers on-chain protocols that truly carry a large volume of perpetual contract trading.

Hyperliquid's biggest critic, former Multicoin partner Kyle, then poured cold water on the Hyperliquid community: "What you're getting now is a guarantee of liquidity distribution from a company that will never be regulated in the U.S."

So what does the CFTC's approval really mean for Hyperliquid?

Offending CME is Scarier Than Offending Binance

Perpetual contracts are futures with no expiration date. Traditional futures must be settled or extended when they expire, while perpetual contracts are maintained in balance via "funding rates," where both sides periodically pay each other a fee to keep the contract price close to the spot price. This allows traders to hold a directional position long-term with less capital in a 7×24 market, which is why it is far more popular in the crypto market than traditional futures.

Friends who frequently work on trading platforms know that to legally operate a perpetual contract trading platform in the U.S., three types of business licenses are required: DCM, corresponding to the trading platform itself; DCO, corresponding to the clearing house, the centralized clearing counterparty; and FCM, corresponding to the intermediaries. None of these can be missing.

However, the entire regulatory framework for operating a trading platform, by design, excludes locations like Hyperliquid that do not qualify for DCO from the broker's access list, because these types of Perpetual DEX do not essentially need to rely on a "clearing house."

Before this policy adjustment, Coinbase acquired a trading platform with a DCM to compliantly launch perpetual contracts, then used the clearing house Nodal Clear to force the product into a five-year, cash-settled futures contract, relying on the clearing house's cash adjustments to simulate funding rates.

The CFTC's new policy did not touch upon the current framework that relies on "centralized clearing houses."

The new "no clearing house" model that Hyperliquid wants to pursue has encountered obstruction from two giants in the traditional financial industry.

According to Bloomberg, the CME, a Chicago commodities trading platform, along with ICE, the parent company of the New York Stock Exchange, has been lobbying on Capitol Hill, demanding that Hyperliquid be forced into the DCM registration framework, mandated to conduct KYC and AML, and increase trading surveillance and position limits.

CME and ICE are not players in the crypto world. CME's foundation rests on commodities and stock index futures, with contracts for crude oil, gold, agricultural products, interest rates, and stock indices being its cash cows for decades; ICE controls a range of trading platforms, including the New York Stock Exchange. Hyperliquid initially only dealt with perpetual contracts for crypto assets, and their paths did not cross.

What truly pushed Hyperliquid into this territory is the TradeXYZ market built on the native protocol "HIP-3." With HIP-3, anyone can list new perpetual contracts on top of Hyperliquid's underlying liquidity. The underlying assets can be stocks or real assets like crude oil and gold. During the Iran War, trading volume for crude oil and gold perpetual contracts on TradeXYZ surged dramatically. Hyperliquid essentially moved CME's most profitable business onto the chain, and it operates 7×24 trading, no permissions required, with on-chain settlement.

The number of open contracts on TradeXYZ continues to grow.

Offending CME is much scarier than offending Binance.

Another lingering concern is the age-old question: "Who takes the blame?"

The instinct of regulation is to find an entity that can be held accountable: if something goes wrong, who should I summon, who should I punish? In the traditional framework, those being regulated are intermediaries like FCM, DCO, and DCM, which are tangible; however, under the declaration of "decentralization," "who takes the blame" remains legally a blank.

Hyperliquid is caught in the middle; it is closed source, with only a few validation nodes deployed at the same location in the early days, far from being "unaccountable," but it also does not have a clear legal person on the front like a traditional trading platform.

Not long ago, a SPACEX-USDH pre-IPO contract on Hyperliquid crashed by 45% in thirty minutes as a single excessively large position consumed the thin liquidity, causing significant losses for many users. The contract design's often-criticized "ADL" mechanism inherently harms some retail investors' interests. A "non-accountable" trading platform is evidently not acceptable to the CFTC.

Finally, the CFTC did not present a formal rule this time, but rather a combination of policy statements, "no-action letters," and guidance. It lacks legal backing, meaning the next CFTC chair could overturn everything with one statement. Before it becomes a formal rule or congressional legislation, today's progress is merely temporary.

Good News

The product form that Hyperliquid relies on is perpetual contracts with stablecoins as collateral. The CFTC's approval effectively stamps this entire model. Whether Congress will outright ban perpetual contracts is no longer a mystery; the biggest concern that has plagued this sector for years has been removed.

The pie itself is still growing. Today, the vast majority of Americans, whether retail or institutional, have no idea what a perpetual contract is. Once compliant pathways are opened up, the scale of this market's expansion will be exponential.

The deeper benefits come from the CFTC's regulatory philosophy. The CFTC has never implemented circular regulations but focused on principles and outcomes: no market manipulation, no stealing customer funds, and maintaining market integrity. As long as these principles are adhered to, whether you are a traditional trading platform or an on-chain protocol, theoretically, you could fall under its regulation. More importantly, once the CFTC obtains jurisdiction, it is exclusive, with state laws and other regulations automatically yielding. For an industry that fears repeated regulatory shifts, this kind of certainty is indispensable.

In addition, the expected Clarity Act includes an "8-prong decentralization test." If a protocol passes this test, it can provide perpetual contract trading services without holding clearing and trading licenses. This leaves a narrow door open for Hyperliquid.

Famous trader Ansem's optimistic narrative has been endorsed by many members of the HL community; he stated: "If Hyperliquid becomes the underlying liquidity engine for various financial trading platforms, called upon by countless front-ends like AWS for cloud computing, and its settlement stablecoin is USDC, then every increment Hyperliquid makes generates demand for the dollar out of thin air." A pro-crypto government that understands this relationship has no reason not to protect it.

Crossroads

Hyperliquid faces three paths.

The first path is to maintain offshore operations, keeping Americans "out the door." Maintaining the status quo isn't bad for Hyperliquid; liquidity is still improving, 7x24 trading and pre-IPO contracts will only increase its attention. However, as Kyle pointed out, choosing this path means you have a product that can attract users but can never be legally integrated into the U.S. financial system.

The second path is to fully establish operations onshore. Hyperliquid has enough funds to acquire the necessary licenses and replicate Polymarket's approach to create a clean Hyperliquid US. This means sacrificing "decentralization" and compromising to a framework centered around "clearing houses," thus losing offshore liquidity.

The third path is to continue pursuing decentralization until it passes the "8-prong decentralization test" outlined in the Clarity Act. This path is the most attractive but faces greater obstacles.

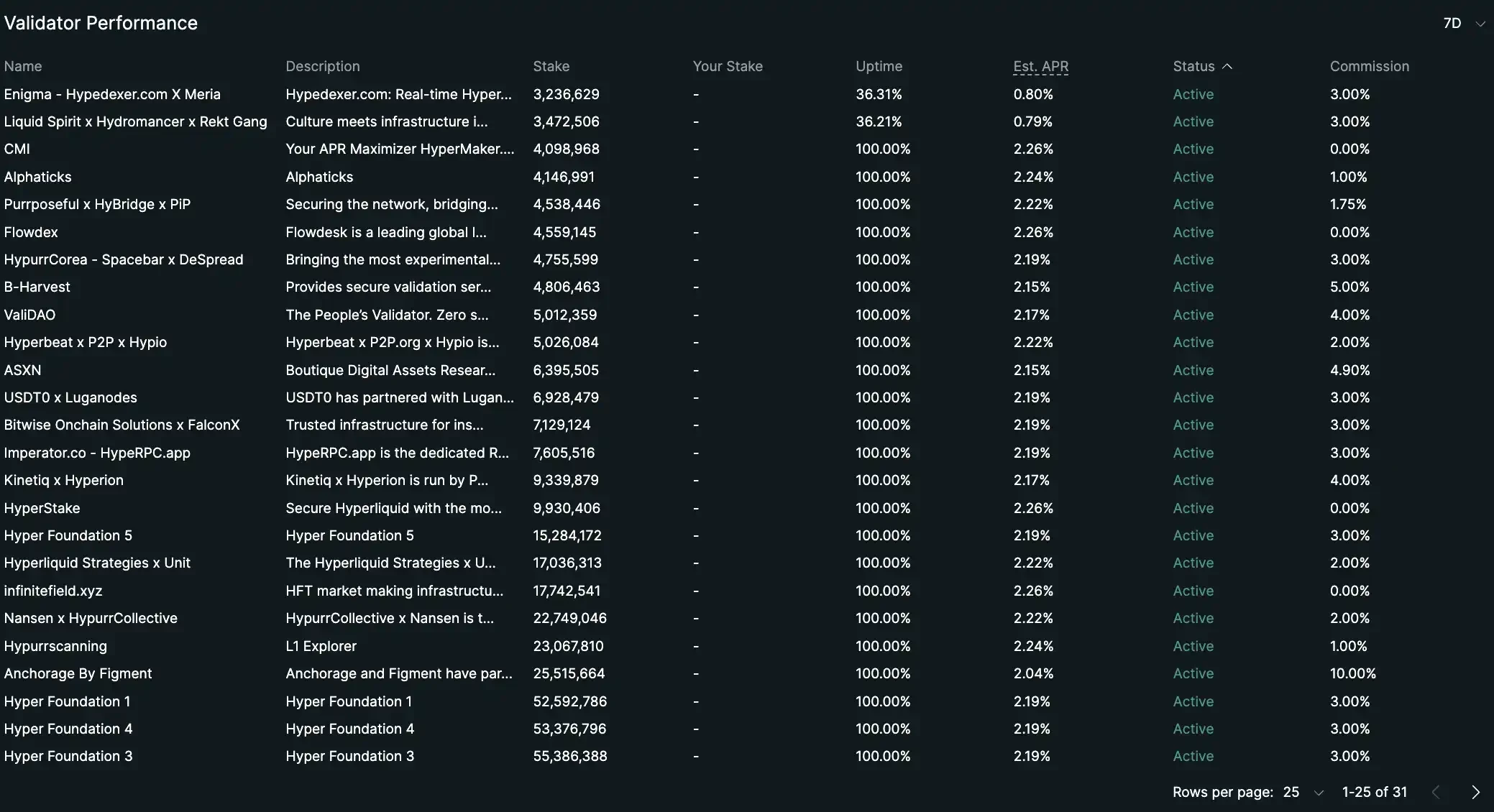

Since its TGE, the number of validation nodes in the Hyperliquid network has expanded from single digits to 26, with the vast majority belonging to external teams. If Hyperliquid can accelerate its decentralization process and walk through this "narrow door," it will become the first perpetual contract market not dependent on clearing houses, accepted by the U.S. compliance system in pure protocol form.

Hyperliquid's validator nodes

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。