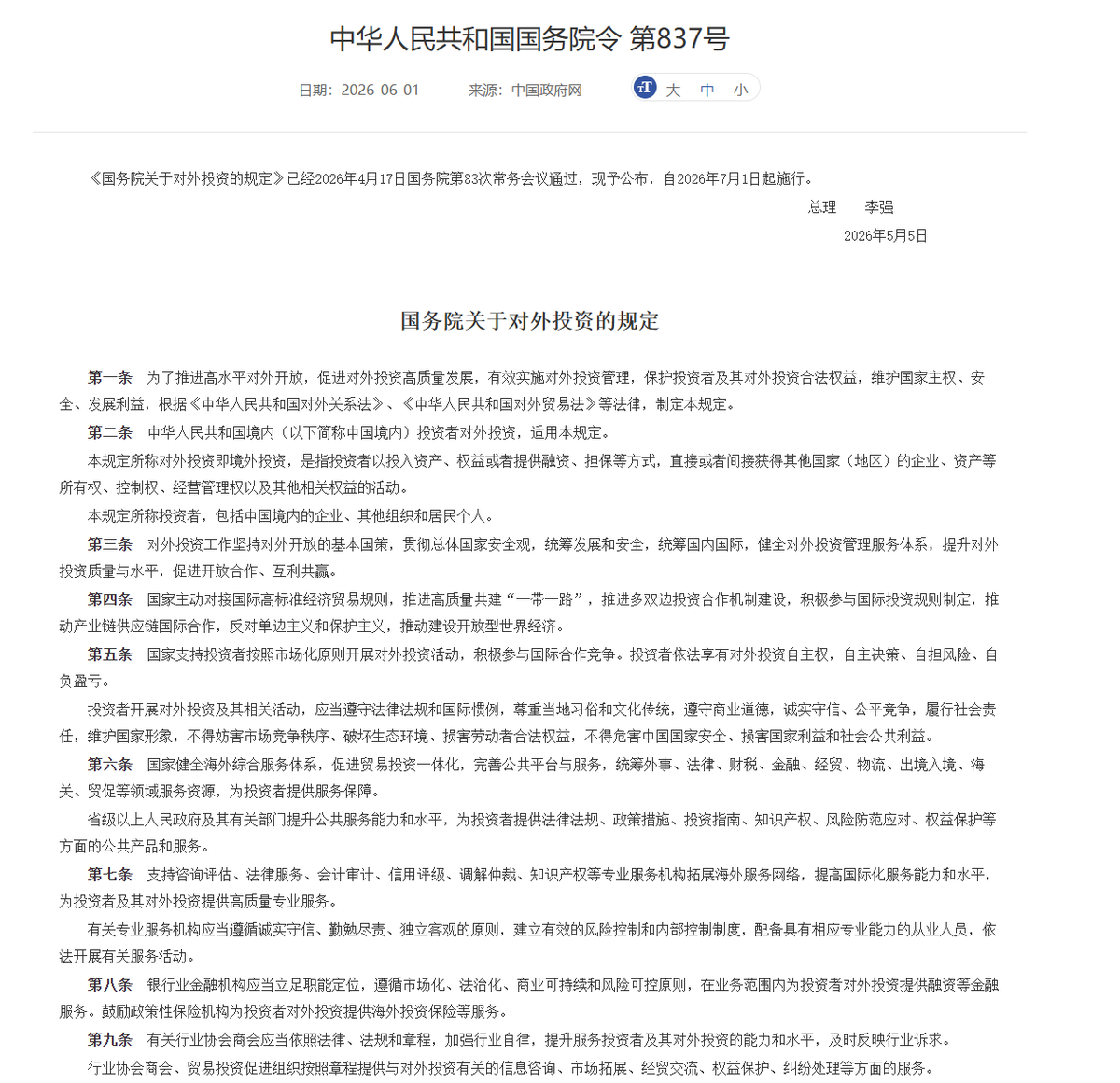

Detailed Interpretation of the Regulations on Foreign Investment by the State Council — — Don't scare yourself unnecessarily

This morning, I saw friends discussing Order No. 837 of the State Council of the People's Republic of China, which is the "Regulations on Foreign Investment by the State Council." Many friends have some misunderstandings, especially those who like to scare themselves or others.

First, let’s say the conclusion: Currently, there is no impact on individuals. There is no new unified foreign investment reporting system for individuals, nor has there been any announcement on the implementation of reporting for personal investments in U.S. stocks or cryptocurrencies after July 1. This does not mean it will not be implemented; it’s just that the details of such reporting have not yet been released, and it's still unclear if they will be issued on July 1—that's the big premise.

The State Council document only states:

The specific management measures for foreign investment by personal residents within China shall be formulated by the investment and commerce authorities of the State Council.

Of course, this does not mean there is no impact at all. For the first time, China has officially included personal overseas investment by residents in the foreign investment framework at the State Council level and has made it clear that subsequent personal management measures will be formulated. This upgrades the previously decentralized "overseas investment regulation logic" spread across the Development and Reform Commission, Ministry of Commerce, State Administration of Foreign Exchange, China Securities Regulatory Commission, Cyberspace Administration, and anti-money laundering system into a unified basic framework at the State Council level.

This means that if it is officially implemented in the future, regardless of whether it is U.S. stocks, ETFs, Hong Kong assets, RWA, on-chain securities, or some cryptocurrency assets, as long as they correspond to overseas assets and rights to income, they may be included under the same foreign investment regulatory logic. In other words:

Residential individuals' foreign investment may be included in the management in the future.

The foundation of this logic should be based on CRS, CARF (China does not participate, but Hong Kong does), anti-money laundering, foreign exchange, and KYC data from banks and brokers forming a cross-validation. Because without "verification" information, relying solely on self-reporting is indeed quite difficult.

Additionally, there is another very important point that I have been reminding my friends about for a long time: the State Council's regulations on foreign investment primarily apply to investors within China and funds within China. In plain language, the restrictions are mainly on Chinese people still living in China.

However, if a person has been living overseas for a long time, has local tax residency status, local legal income, local bank accounts, and invests using overseas legal income, that is not the same as domestic funds routing overseas. The new regulations are not specifically aimed at normal overseas investments by Chinese people abroad, but rather focus on managing situations where domestic funds, domestic accounts, domestic services, and domestic rights to income are routed out through various means.

After coming into effect, the focus for ordinary people is first to distinguish whether the investor is a resident of China or a domestic enterprise (we will not talk about enterprises, as they already have reporting channels, mainly ODI).

1. If domestic individuals are buying U.S. stocks, the most compliant way is still through channels authorized by the state, such as QDII, mutual fund connectivity, and offshore asset products issued by qualified domestic institutions.

Using overseas broker apps to open accounts and trading U.S. stocks remotely from within China is already being cleaned up; the China Securities Regulatory Commission’s May document explicitly prohibits overseas institutions from providing account opening, trading instructions, and fund transfers as cross-border securities services in China, and also prohibits individuals or institutions from assisting domestic investors in opening accounts improperly.

2. If one already has overseas identity, overseas income, and overseas bank accounts, like living in Singapore, being a local tax resident, and using overseas legal income to invest in U.S. stocks, the focus should be on proof of the source of funds, tax residency status, broker KYC, CRS reporting, etc.

The new regulations themselves do not specifically target overseas Chinese in this situation; the focus is to prevent domestic funds from routing out to purchase overseas assets.

3. If domestic individuals are buying cryptocurrencies, it will be more complicated. China already has strict restrictions on virtual currency transactions and services provided by overseas exchanges to residents in China. Regulatory actions to further prevent and address virtual currency risks will occur in 2026.

After the new regulations come into effect, if one uses stablecoins, exchanges, or on-chain wallets to buy overseas equity, RWA, tokenized securities, or overseas funds, it may essentially be treated as domestic funds investing abroad.

Therefore, the biggest impact of this document on individuals is not an immediate restriction, but that personal overseas asset allocation is officially included in the national foreign investment regulatory framework. The rules have not been fully implemented yet, but in the future, whether it is U.S. stocks, ETFs, RWA, on-chain securities, or some cryptocurrency assets, as long as they correspond to overseas assets and rights to income, they will be more easily managed uniformly according to the foreign investment logic.

In simpler terms, the previous lack of systematic management by departments or methods is now more clearly defined. For purely domestic funds and purely domestic identity, the rules have become stricter.

Overall, from the current perspective, it is not that individuals will have to report immediately after July 1 for buying U.S. stocks or cryptocurrencies, but rather that the State Council has first included residents' foreign investment into the management framework, making it "lawful." The next thing to watch is whether the Development and Reform Commission, Ministry of Commerce, State Administration of Foreign Exchange, and other departments will continue to issue details and reporting plans for personal foreign investment.

#Bitget is here and it's VIP! Crypto, U.S. stocks, CFD, global opportunities laid out in one stop

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。