Original | Odaily Planet Daily (@OdailyChina)

Author | Asher (@Asher_0210)

The prediction market is advancing into perpetual contracts, finally moving from official announcements to execution.

Last week, Polymarket and Kalshi both made significant progress. The Beta version of Polymarket's perpetual contracts has been opened for testing to some users and will gradually expand access over the next four weeks; Kalshi has obtained CFTC approval to launch the Bitcoin perpetual contract BTCPERP.

In fact, Odaily Planet Daily had previously discussed this trend in the article "Polymarket and Kalshi are getting into perpetual contracts, while exchanges are simultaneously sneaking into the prediction market's home": the expansion of prediction market platforms into perpetual contracts, while exchanges are also entering event trading, leading to blurred boundaries between the two. In the article "What does the U.S. government's first lifting of the ban on crypto perpetual contracts mean for the market?", we also analyzed the significance of Kalshi's approval of BTCPERP for the compliant crypto derivatives market in the U.S.

Now, both directions have become more concretely defined. One is conducting small-scale product testing, while the other has obtained regulatory approval. The paths are different, but the signals are consistent: prediction market platforms are no longer satisfied with just event trading; instead, they are starting to enter a higher frequency and more standardized derivatives market.

Polymarket opens Beta version of perpetual contracts, gradually increasing volume over the next four weeks

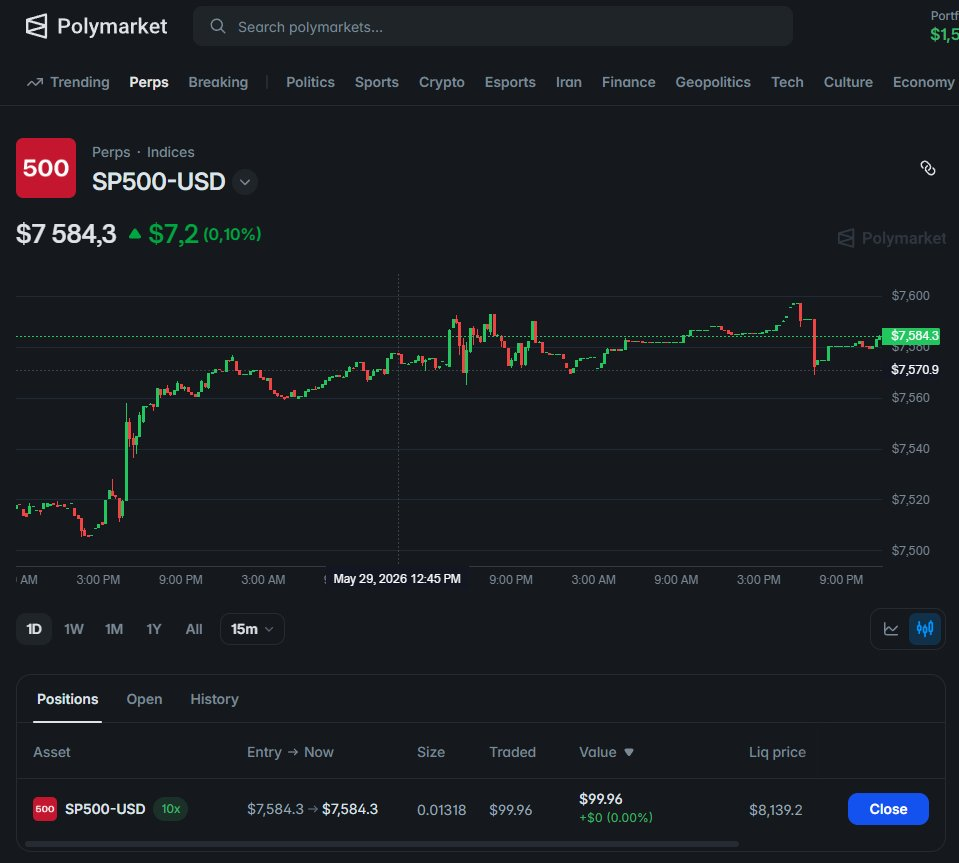

Polymarket officially launched the Beta test

Last week, Polymarket's DeFi Engineering Vice President, Josh Stevens, announced on the X platform that Polymarket Perps Beta has been opened for some users at polymarket.com, and will gradually expand access over the next four weeks. He also mentioned that some applicants were added to the testing list through private messages, and although a few slots might still be released, no new testers will be added at this stage.

Currently, Polymarket has not disclosed the complete set of trading pairs, leverage, margin rules, and funding rate mechanism supported by Perps. This means that this Beta is more like a small-scale product test rather than a large-scale launch for all users. What Polymarket needs to confirm first is not how much trading volume can be generated in the short term, but whether this new trading functionality can operate stably.

This is also evident from Josh Stevens's statements. When recruiting test users, he mentioned that he hoped participants would provide feedback on “aspects they dislike” and possible improvements for the UI. In other words, Polymarket is currently more focused on whether the order process, position display, mobile compatibility, and overall interaction are smooth. For features like perpetual contracts that are more similar to exchanges, the product experience itself is the first threshold.

Feedback from some test users on the X platform indicates that the Polymarket Perps Beta version already supports basic opening operations; some users mentioned they have opened a BTC leveraged long position in the test interface, and screenshots show that cryptographic assets and indices have appeared as underlying assets. However, these still belong to early testing feedback, and the final trading pairs and specific features will need to wait for further disclosure from the official side.

Early feedback focused on qualifications, liquidity, and trading experience

In early feedback, users first mentioned issues regarding testing eligibility and KYC. The Beta phase is only open to a select group of users, with early applicants needing to apply for eligibility through private messages on the X platform, and some testers needing to complete KYC identity verification. Although there are claims in the community that these restrictions may be adjusted after the official version is released, at the current stage, questions such as "verification needed," "did not receive early eligibility," and "will this affect future airdrops or points," have already caused some dissatisfaction among users.

More core concerns come from liquidity. A perpetual contract is not merely completed by being able to open a position; what truly determines the experience is the depth of the order book, slippage control, and transaction stability under high volatility. Some community users frankly express that perpetual liquidity is the real test.

Another issue is user habits. Polymarket's core users are more accustomed to binary event contracts to buy Yes or No and then wait for the event settlement. However, Perps introduces leverage, liquidation, funding rates, and continuous position management. This mechanism is familiar to professional contract users; however, for a large number of new users entering from prediction markets, the learning cost and risk of losses will be significantly higher.

Additionally, Polymarket has previously faced user complaints about delays, order lags, ghost fills, etc.; this raises concerns among some users that similar issues, if they occur in the Perps scenario, could have a more significant impact than in regular prediction markets. In prediction markets, a few seconds of delay might just mean missing a better price; however, in high-leverage trading, delays, abnormal transactions, or unstable position displays can directly affect profit and loss.

Therefore, Polymarket Perps is currently in a stage of adaptation. On one hand, early testing feedback has not been harsh; many users also appreciate the clean interface and direct usability; on the other hand, access barriers, liquidity, leverage risks, and trading stability are all issues that must be addressed before a full rollout.

Kalshi opens the entry for perpetual contracts with a compliance license

In contrast to Polymarket, which is still in small-scale testing, Kalshi's progress occurred more directly at the regulatory level.

On May 29, the U.S. CFTC approved Kalshi to launch a Bitcoin perpetual contract, which references the Bitcoin spot price and will be traded as a futures product. According to the announcement, the CFTC reviewed based on Section 5c(c)(4) of the Commodity Exchange Act and Regulation 40.3, concluding that BTCPERP meets relevant regulations and the core principles applicable to designated contract markets (DCM).

The significance of this step is not only that Kalshi has added a BTC contract, but that it has brought a product that has long existed primarily in offshore exchanges and crypto-native platforms into the framework of regulated exchanges in the U.S. Perpetual contracts are among the highest trading volume and most familiar derivatives in the crypto market, but related products have long been absent in the compliant U.S. market. Kalshi's approval essentially opens the door for the "U.S. compliant version of crypto perpetuals."

This also continues Kalshi's consistent approach. It does not rush to capture users with aggressive products first and then seek regulation; rather, it seeks regulatory approval first and then expands its trading categories with its compliance status. Previously, Kalshi packaged political, economic, weather, sports, and other event contracts into regulated financial products using its DCM status; now it is beginning to replicate this path for crypto perpetual contracts. In other words, Kalshi aims to become not just a prediction market but a broader compliant derivatives exchange.

However, the regulatory passport also means clearer boundaries. While approving BTCPERP, the CFTC noted that perpetual contracts are not suitable for all asset classes; for assets not yet covered, market participants must still submit for review under Regulation 40.3. This means Kalshi can leverage regulatory certainty to establish advantages, but it is challenging to roll out a large number of trading pairs as quickly as offshore exchanges or crypto-native platforms. Its expansion will be slower and more influenced by regulatory pace.

This is exactly the difference between Kalshi and Polymarket. Polymarket is more about validating market demand first and gradually addressing compliance boundaries; Kalshi seeks regulatory space first and then uses regulatory certainty to expand product offerings. The former's advantage lies in crypto-native traffic and product speed, while the latter's advantage lies in U.S. compliance identity and institutional narrative.

Therefore, the approval of BTCPERP is not just Kalshi introducing a new trading category, but a signal of its identity transformation. Kalshi is moving closer from being a "prediction market platform" to a "regulated derivatives exchange."

With the opening of the contract entry, the real test has just begun

Polymarket and Kalshi are both pushing forward the perpetual contracts, which is fundamentally not about adding a new feature to prediction markets, but continuing to push their business boundaries toward the direction of exchanges.

Prediction markets themselves do not lack trading scenarios. Elections, sports, macro data, crypto prices, corporate events, and breaking news can all be packaged into tradable markets, and Polymarket and Kalshi have already proven that event trading is a sufficiently profitable business. However, perpetual contracts open up another layer of increment: they are more standardized and more easily accommodate the funds and trading habits of mature traders. For the platforms, doing Perps is not because prediction markets are not profitable, but to engage in a more mature contract business beyond event trading.

However, this path is not easy. After entering perpetual contracts, Polymarket and Kalshi's competitors are no longer just other prediction markets but also mature crypto trading platforms like Hyperliquid, Binance, OKX, and Bybit. Users will directly compare liquidity, slippage, execution stability, leverage experience, and risk control capabilities. The brand and traffic of prediction markets will not automatically convert into competitiveness in contract trading.

Thus, the real test of perpetual contracts is not whether the platforms can launch more new trading pairs, but whether they can convert event traffic into trading traffic. Only when users are willing to trade volatility and manage positions here long-term, instead of just opening the platform for a major event, can prediction market platforms truly touch the door of exchange business.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。