Week 4 of May 2026

Statistical Period: May 20, 2026 – May 26, 2026

Data Cutoff: May 26, 2026

Core Narrative

Over the past week, the battle between macroeconomic factors and regulations has deepened. The minutes from the Fed's May FOMC meeting released on May 21 confirmed the market's biggest concern - the minutes showed that some members have begun discussing "if inflation remains high, raising interest rates should be back on the table." The yield on 30-year U.S. Treasuries briefly surpassed 5.10%, while the CME's implied probability of a rate hike in December climbed to 35% mid-week, a new high since 2026.

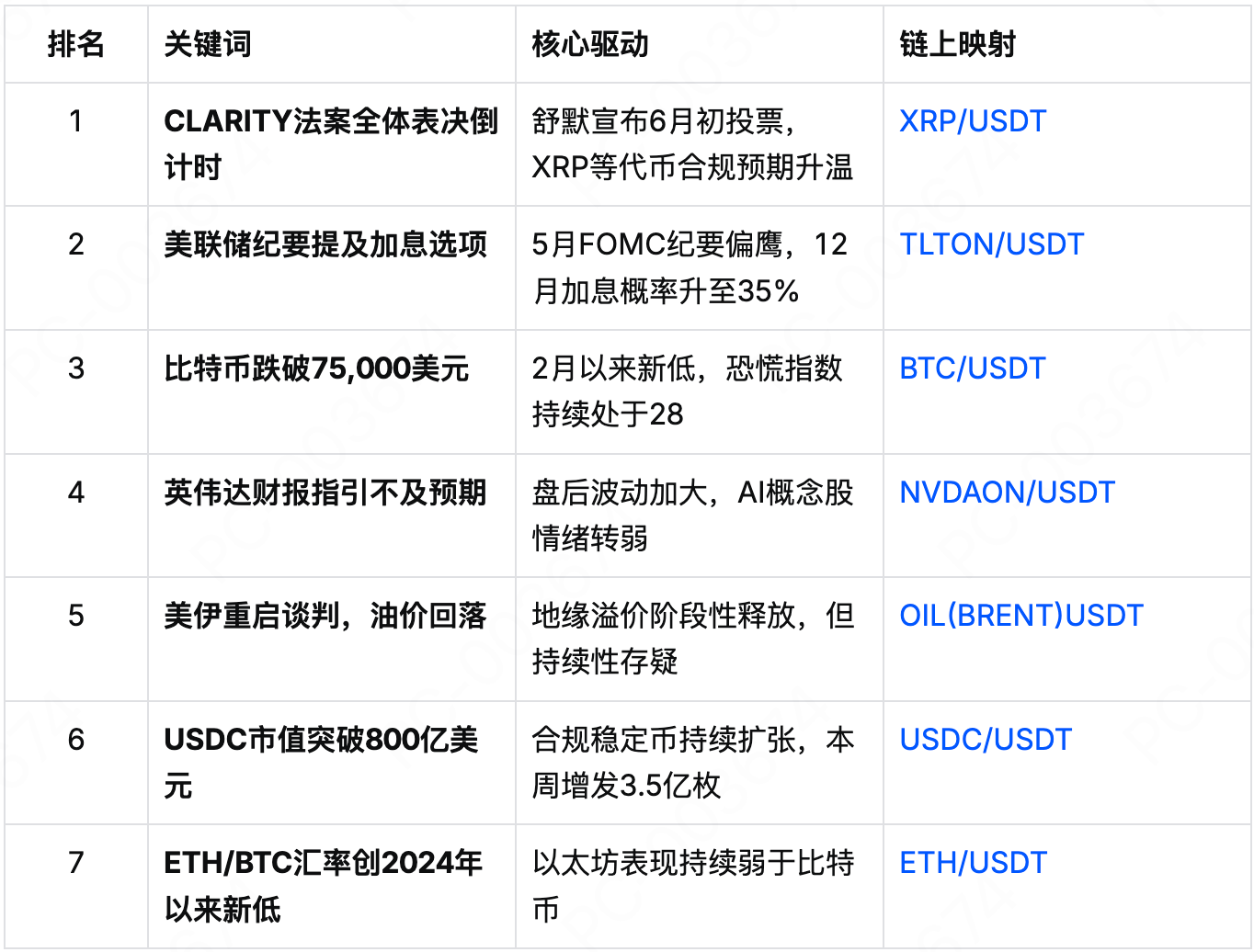

Meanwhile, key progress was made in cryptocurrency legislation. On May 22, Senate Majority Leader Schumer announced that the CLARITY Act would be included in the agenda for a full vote, with a final vote expected in early June. Market expectations for the bill's passage shifted from "possible" to "certain," although this institutional advantage remains suppressed by the macro shadow of tightening liquidity.

Bitcoin continued to search for a bottom this week. After a brief rebound to $78,500 on May 20, prices fell again with the hawkish wording from the FOMC minutes, dropping below the $75,000 level on May 23 to a low of $74,200, a new low since February. Ethereum also fell below the $2,000 psychological level, closing at $1,980. As of May 26, Bitcoin was at $74,800, with the cryptocurrency market's fear and greed index holding steady at 28 (in the fear range).

Geopolitical signals showed signs of easing. On May 20, the U.S. and Iran restarted indirect negotiations in Oman, leading oil prices to retreat from their highs, with Brent crude oil dropping below $105 per barrel, and WTI crude reported at $101 per barrel. However, market skepticism about the sustainability of the negotiation results persisted, keeping oil prices well above levels seen at the beginning of the year.

In the U.S. stock market, Nvidia's financial report on May 22 was mixed - revenue slightly exceeded expectations but the guidance for the next quarter fell short of the most optimistic forecasts, resulting in volatile after-hours trading. The tokenized NVDAON also faced downward pressure. Overall, the market is still digesting the new norm of "higher for longer" interest rates.

1. Core Dynamics in the Cryptocurrency Market

1. Institutional Funds: ETF Outflows Slow but Still Net Outflows, BlackRock Sees Rare Zero Inflows in a Single Day

Sales pressure on Bitcoin spot ETFs continued at the start of the week but eased in the latter half. According to data from Farside Investors and Coinglass, there was a total net outflow of approximately $420 million from May 20 to May 23 over four trading days, including a net outflow of $180 million on May 20 and $150 million on May 21. Outflows on May 22 and 23 shrank to $60 million and $30 million, respectively. On May 24, the market saw a small net inflow of about $20 million, marking the first single-day positive inflow since May 13.

BlackRock's IBIT recorded a rare single-day zero net inflow on May 22 since its launch, indicating that even the most committed institutional buyers chose to wait in the face of macro uncertainty. Grayscale's GBTC continued to experience outflows, but the rate of outflow has decreased from an average of $200 million per day during peak periods to about $50 million.

As of May 26, total cumulative net inflows for Bitcoin ETFs remained at approximately $58.5 billion, slightly down from the previous week. Ethereum ETFs continued their net outflow trend, with a total outflow of approximately $12 million this week.

In the derivatives market, approximately $650 million was liquidated across the entire network this week, with long positions accounting for about 75%. On May 23, when Bitcoin dropped below $75,000, liquidations amounted to $280 million, and market leverage saw a decrease.

2. Price Performance: Bitcoin Drops to New Low Since February, $75,000 Becomes a Pivotal Point

This week's price movement for Bitcoin can be divided into two phases:

- Phase One (May 20-22): Weak Rebound, Second Bottoming. After a sharp drop the previous week, Bitcoin attempted to rebound to $78,500 on May 20, but trading volume was significantly insufficient. Following the hawkish remarks from the FOMC minutes on May 21, prices quickly retraced gains. On May 22, prices further dipped to around $76,000, with $75,000 at risk.

- Phase Two (May 23-26): Break Below $75,000 Testing $74,000 Support. During the Asian session on May 23, Bitcoin officially dropped below $75,000, reaching a low of $74,200. The subsequent two trading days oscillated in the $74,500-$75,500 range. $75,000 shifted from a psychological support to a short-term resistance.

Ethereum underperformed compared to Bitcoin, with the ETH/BTC exchange rate dropping to around 0.026, the lowest since 2024. Solana fell below $85, and XRP retreated below $1.30.

Data Source: CoinGecko, MEXC

Technically, Bitcoin's daily RSI is near 35, not yet entering the oversold zone (below 30), indicating room for further decline. If $75,000 confirms a valid breakdown, the next support area is in the $72,000-$73,000 range (the low point tested multiple times since January). The probability of Bitcoin falling below $70,000 by the end of May on Polymarket has risen to 22%, while the probability of dropping below $75,000 is at 89%.

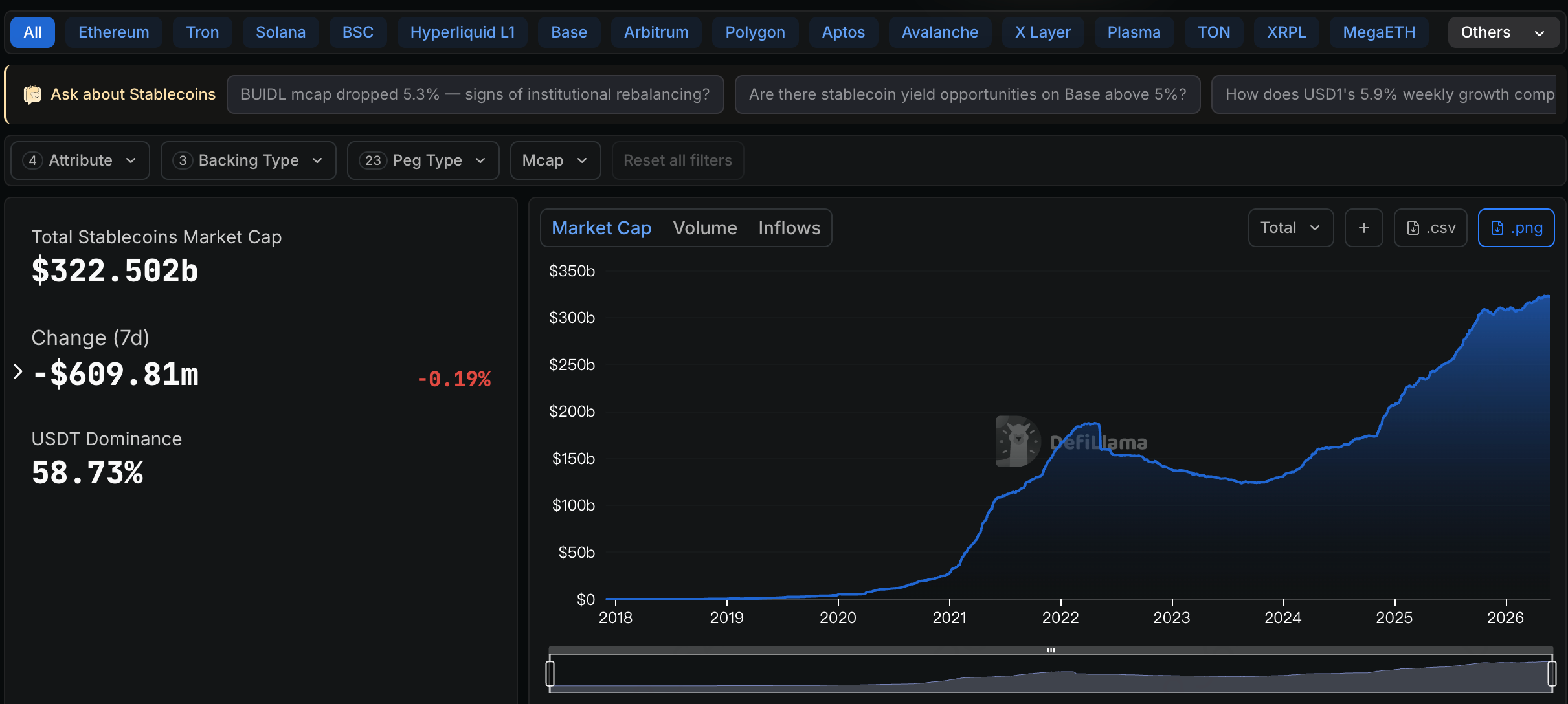

3. Stablecoins: Total Market Capitalization Exceeds $322.5 Billion, USDC Continues to Expand

The total market capitalization of stablecoins exceeded $322.5 billion this week. USDT’s market cap is around $190.5 billion, with a slight market share decline to 58.73%; USDC’s market cap surpassed $80 billion, reaching approximately $80.5 billion, with its market share increasing to 24.8%. The continuous issuance of USDC reflects a heightened preference among institutions for compliant stablecoins, especially in the context of the upcoming vote on the CLARITY Act.

On May 23, Circle minted another 200 million USDC on the Ethereum mainnet, bringing the total issuance for the week to 350 million. Yield-generating stablecoin sUSDS had a total locked amount exceeding $12 billion, becoming one of the fastest-growing assets in the DeFi space.

2. Global Asset Performance

1. Equity Market: FOMC Minutes Weigh on Risk Appetite, Nasdaq Weekly Drops

The minutes from the Fed's May FOMC meeting were released on May 21. The minutes stated: "Some participants noted that if inflation does not decline as expected, the committee may need to consider further tightening." This marks the first mention of "interest rate hikes" as a potential option in official minutes since 2026.

After the minutes were released, all three major U.S. stock indices fell. As of the close on May 23, the S&P 500 index recorded a weekly decline of 1.5%, and the Nasdaq index fell 2.2%, ending a two-week streak of gains. The semiconductor sector was hit hard, with the Philadelphia Semiconductor Index down 3.5% for the week.

Nvidia's earnings report released after hours on May 22 showed mixed results: revenue was $38.2 billion, a year-on-year increase of 68%, slightly above the expected $38 billion; however, the guidance for the next quarter was $39-40 billion, below the most optimistic forecast of $42 billion. The stock price dropped 3% in after-hours trading, while the tokenized NVDAON also weakened. Home Depot's (HD) report released on May 20 showed same-store sales fell short of expectations, reflecting weak consumption related to real estate in the U.S. under a high-interest-rate environment.

2. Commodity Market: Oil Prices Retreat from Highs, Gold Falls Before Rising

Crude Oil: The news of the U.S. and Iran restarting indirect negotiations on May 20 alleviated concerns about supply disruptions. WTI crude oil fell from $107 per barrel at the beginning of the week to $101 per barrel on May 23, and Brent crude dropped from $112 per barrel to $105 per barrel. However, on May 25, reports surfaced that the negotiations did not make significant progress, causing oil prices to rebound slightly to WTI $103 per barrel. Overall, prices decreased by about 4% for the week.

Gold: The rising expectations of rate hikes initially pressured gold prices, with COMEX gold futures dropping to $4,520 per ounce on May 21. However, as the dollar index declined from its highs (from 105.8 to 105.2), gold prices rebounded after May 23. As of May 26, COMEX gold was reported at approximately $4,600 per ounce, showing a slight weekly increase of 0.5%. Silver performed strongly, with COMEX silver reported at $79.5 per ounce, rising 1.8% for the week.

3. Bond Market: 30-Year U.S. Treasury Yield Stabilizes Above 5%, Rate Hike Pricing Moves Upward

The yield on 30-year U.S. Treasuries reached 5.12% this week, closing at 5.08%, solidly above the 5% mark. The yield on 2-year U.S. Treasuries rose to 4.45%, while the yield on 10-year U.S. Treasuries rose to 4.62%. The degree of the yield curve inversion deepened, with market concerns about the economic outlook coexisting with stubborn inflation expectations.

CME FedWatch tool indicated that as of May 26, the probability of a 25 basis point rate hike in December 2026 is 35%, while the probability of a 50 basis point rate hike is at 8%. A month ago, these figures were 2% and 0%, respectively. The market has fully priced in that there will be no interest rate cuts before September.

The tokenized treasury product TLTON (iShares 20+ Year U.S. Treasury Bond ETF) launched on MEXC saw a significant increase in weekly trading volume, reflecting increased user demand for hedging rate expectations. International ETF token trading pairs like EEMON/USDT, EFAON/USDT, and INDAON/USDT have also been launched on the platform.

3. In-Depth Analysis of Key Themes

Theme One: The CLARITY Act Enters Countdown to Full Vote - Can Institutional Dividend Counteract Macro Headwinds?

On May 22, Senate Majority Leader Schumer announced that the CLARITY Act would be included in the agenda for a full vote, with a final vote expected in the week of June 2. The bill was previously passed by the Senate Banking Committee with a 15-9 vote, and by the House with a 294-134 vote. With considerable bipartisan support, the market generally expects the bill to pass procedural hurdles in the Senate with over 60 votes, ultimately being sent for presidential signature.

Institutional impacts on the market:

- Regulatory Certainty Premium: The bill will clarify the jurisdictional boundaries of the SEC and CFTC over digital assets, especially defining "which tokens fall under commodities," potentially granting legal "innocence" status to assets like XRP and SOL that were questioned by the SEC. This week, XRP showed relative resilience, outperforming Bitcoin.

- Lower Entry Barriers for Traditional Financial Institutions: After the legal framework for custody, clearing, and trading execution is clarified, banks and registered brokers can legally conduct crypto business. It is expected that a new wave of institutional funding will flow in within 6–12 months following the bill's passage.

- Mismatch Between Short-term and Long-term: In the current macro tightening environment, institutional advantages may serve more as a "buffer in a downturn" than as an "engine of upward movement." Historical experience indicates that the price boost from regulatory clarity usually becomes evident within 3-6 months post-legislation.

Theme Two: Fed Minutes Confirm "Interest Rate Hike Option" - Rate Expectations Reset Close to Completion

The wording of the May FOMC meeting minutes was more hawkish than the market anticipated. In addition to discussing the "interest rate hike option," the minutes also mentioned "the labor market remains tight, and service inflation is unwinding slowly." The core PCE data for April will be released on May 29 (Thursday), and the market expects a year-on-year figure still above 3.0%.

Implications for Crypto Assets:

- Valuation Model Reconstruction: As a zero-yield risk asset, crypto assets are highly sensitive to real interest rates. The real yield on 30-year U.S. Treasuries (TIPS) has risen from 1.8% in April to 2.1%, challenging the "digital gold" narrative for Bitcoin.

- Increased Pressure on Miners: With Bitcoin prices dropping to the $74,000-$75,000 range, they are approaching the shutdown cost line for some older mining rigs (assuming electricity costs of $0.07 per kWh, Antminer S19 series shutdown price is about $72,000). If prices continue to decline, it could trigger miner sell-offs, creating a negative feedback loop.

- Rising Stablecoin Lending Rates: As rate hike expectations increase, deposit rates for USDC/USDT in on-chain lending protocols have risen from 4% to 5.5%, increasing the opportunity cost of holding cash.

Theme Three: U.S.-Iran Negotiation Window Opens, Geopolitical Risk Premium Temporarily Eases

On May 20, under the mediation of the Sultan of Oman, the U.S. and Iran restarted indirect negotiations aimed at achieving a 60-day "pause in hostilities" and opening certain shipping routes through the Strait of Hormuz. Following the announcement, oil prices fell by over 5% in a single day. However, on May 25, Iran stated that "the U.S. proposal did not meet Iran's core concerns," leading to a stalemate in the negotiations and a subsequent rebound in oil prices.

Market Outlook: The energy market is still torn between "optimism from negotiations" and "realities of supply disruptions." The closure of the Strait of Hormuz has persisted for over 40 days, rapidly depleting global oil stocks. Even if some progress is made in the negotiations, restoring a daily throughput of 17 million barrels will take several weeks. Oil prices are expected to remain high at $100-$115 per barrel over the next month, continuing to support inflation.

4. Market Hot Words Cloud

5. Core Focus for the Upcoming Week

Economic Calendar (May 20 – May 26, SGT)

Note: The above tokenized assets are now live on the MEXC spot market, and each batch of newly launched varieties enjoys azero fee privilege for the first 30 days.

6. Platform Updates

1. New Listings Continue to Accelerate: SpaceX Pre-IPO, Nexus, and Samsung with SK Hynix Perpetual Contracts All Launched

This week, MEXC has accelerated its pace of new listings, covering three major tracks: primary markets, emerging public chains, and traditional equity:

- SpaceX Pre-IPO Launchpad: On May 20, MEXC launched the SpaceX Pre-IPO Launchpad event, issuing 7,700 SPACEX(PRE) tokens, each priced at 650 USDT or USD1, with subscriptions open until May 21. This token aims to give users early economic exposure linked to SpaceX’s valuation, with no lock-up period, allowing free trading in the spot market after token distribution. The entire subscription and trading process incurs zero fees.

- Nexus (NEX) Launch: On May 20, MEXC officially listed the Layer 1 public chain Nexus (NEX), opening NEX/USDT and NEX/USDC spot trading pairs, and also launched NEXUSDT perpetual contracts (up to 20x leverage). This project combines zero-knowledge proofs with native order books, with a total supply of 100 trillion tokens, showing significant volatility in the early days; users in the assessment zone should be aware of the risks.

- Samsung and SK Hynix Perpetual Contracts: On May 20, MEXC officially launched perpetual contracts for Samsung Electronics (SAMSUNGUSDT) and SK Hynix (SKHYNIXUSDT). That evening, both major Korean semiconductor stocks surged significantly - Samsung Electronics closed up 8.51%, and SK Hynix up 11.17%. The tokenized contracts allow investors to participate in the market dynamics of leading Korean semiconductor companies without needing offshore accounts.

2. Welfare Continued Upgrades: Two Major Activities for Pizza Day and Multiple Gifts Ongoing

Coinciding with the Bitcoin Pizza Day, MEXC launched a "Pizza Day Special Event", running from the event start date until June 5. Users can enjoy a 0 fee rate when purchasing digital currencies using Apple Pay or Google Pay, and new users who make their first purchase of 100 USDT can receive an airdrop of 10 USDT, with the top 300 users by net purchase amount eligible for a share of a prize pool of 15,000 USDT. The "Pizza Day Urban Run" parkour game is also underway, allowing users to collect "pizza vouchers" by completing daily tasks like check-ins, deposits, and transactions, with a 100% chance of winning in different difficulty lanes, with the prize pool including up to 1 BTC, gold tokens XAUT, contract bonuses, and exclusive merchandise.

Disclaimer: This report is for research reference only and does not constitute any investment advice. Prices of crypto assets are highly volatile, and geopolitical events and macroeconomic changes may significantly impact the market. Investors should independently assess based on their risk tolerance. Any platform products or trading pairs mentioned in this report are presented as objective data and do not constitute a buy or sell recommendation.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。