This report is written by Tiger Research. Circle released its financial report for Q1 2026. The interest income from USDC reserves still accounts for more than 90% of total revenue. To break this highly concentrated structure, Circle is advancing several initiatives, including the Ark network. Where will the next stage lead?

Summary

- With Q1 2026 performance as a turning point, Circle is accelerating its paradigm transformation—from a mere stablecoin issuer to a comprehensive infrastructure operator in the digital asset industry. Its forward-looking business strategy revolves around three core pillars.

- Maximizing USDC profit margins and circulation: Reserve interest accumulates on both external and proprietary platforms. This quarter, the usage of USDC in Circle's proprietary channels (CPN) increased, driving the RLDC profit margin to a historic high of 41.4%. To expand the issuance scale, Circle has partnered with the DEX platform Hyperliquid.

- Launching its own L1 network "Arc" to diversify Gas and transaction fee income: Currently, 94% of Circle’s revenue comes from USDC reserve interest. Once Arc expands Circle's platform business and generates platform fee income, the structural issue of over-reliance on reserve interest will fundamentally be resolved.

- Seizing the AI payment entry through Agent Stack: Circle is vying for standard discourse in autonomous micropayments between AI agents. Based on the progress of infrastructure construction and the effective date of the "GENIUS Act," the full commercialization goal is set to be achieved by 2028.

Overall, Circle will aggressively expand USDC issuance through anchor platforms like Hyperliquid as a short-term focus, while conducting vertical integration of its financial stack around its own L1 (Arc), payment network (CPN), and AI micropayments (Agent Stack). The key is that the growth of USDC circulation and the diversification of infrastructure have formed a mutually reinforcing positive cycle.

Circle is evolving from a purely interest income business to a platform business driven by volume and transaction fees.

Q1 2026 Review: Profit Margins are Recovering

1. Revenue Growth and Margin Improvement – Improved Profit Quality from Proprietary Platform Proportion

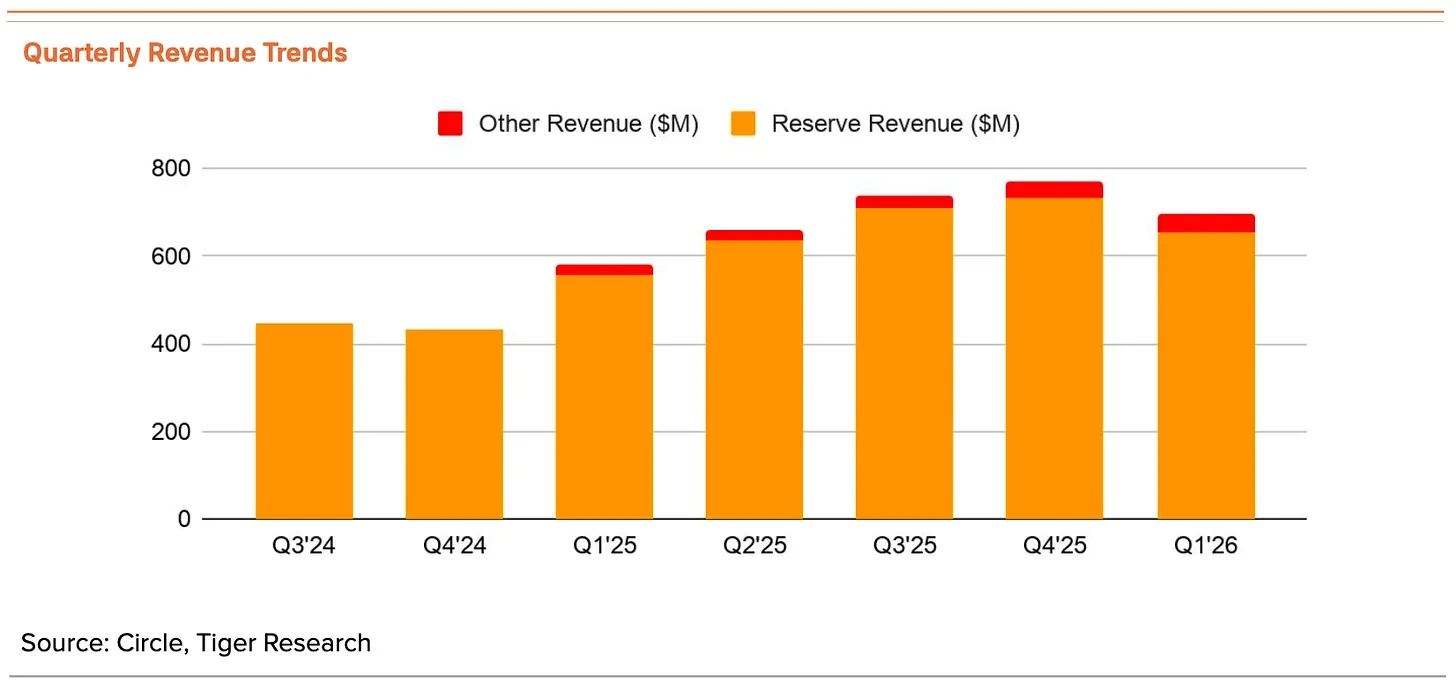

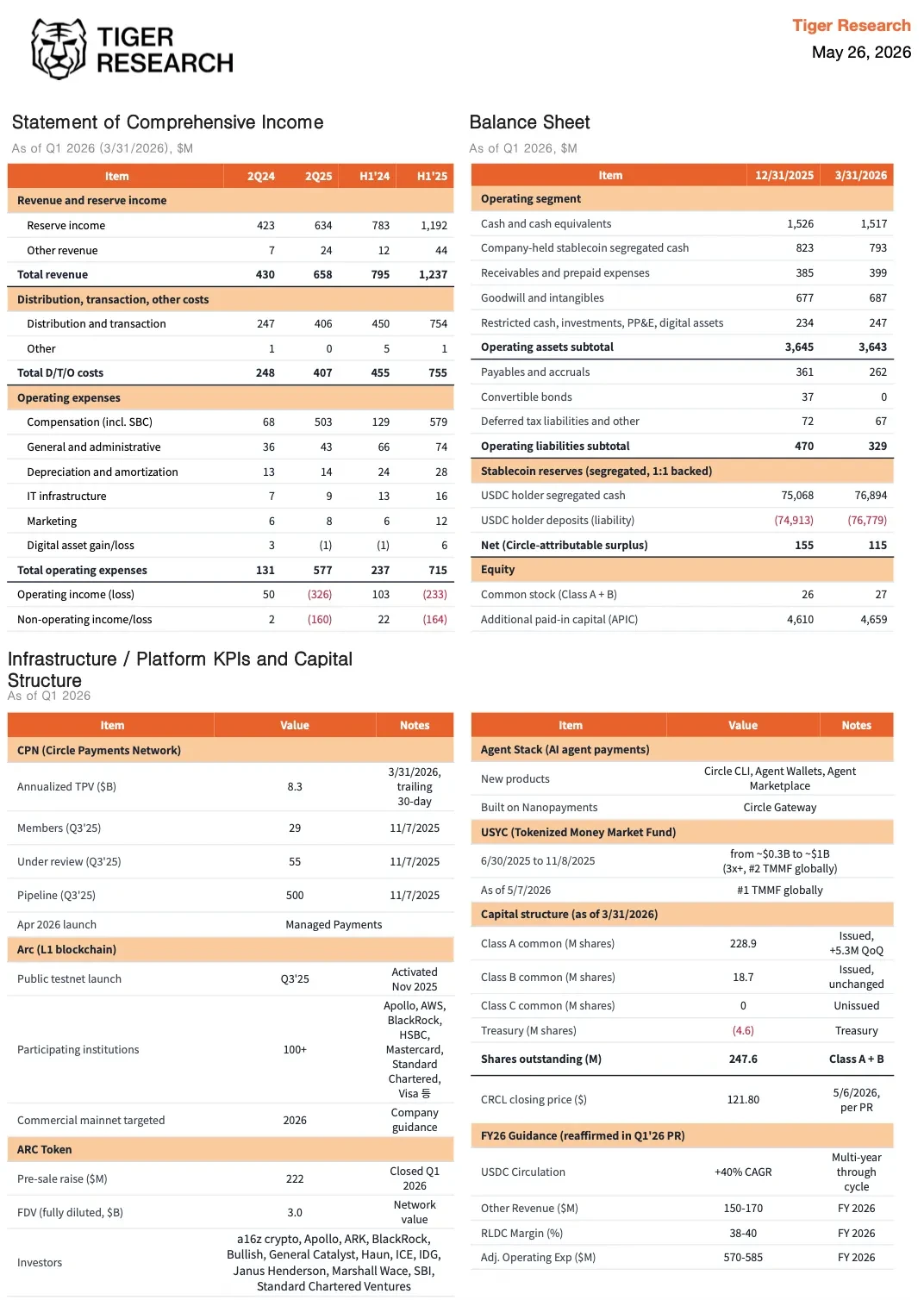

In Q1 2026, revenue reached $694 million (up 20% year-on-year), with adjusted EBITDA at $151 million (up 24% year-on-year), resulting in an adjusted EBITDA margin of 53%, indicating improved profitability. Currently, 94% of Circle's total revenue relies on reserve interest income.

The reserve yield declined by 31 basis points quarter-on-quarter (from 3.81% to 3.50%), putting direct pressure on revenue. Nevertheless, the RLDC profit margin has risen for the third consecutive quarter, reaching a historic high of 41.4%. Despite the pressure on interest-based income, Circle has still successfully improved its core profit quality.

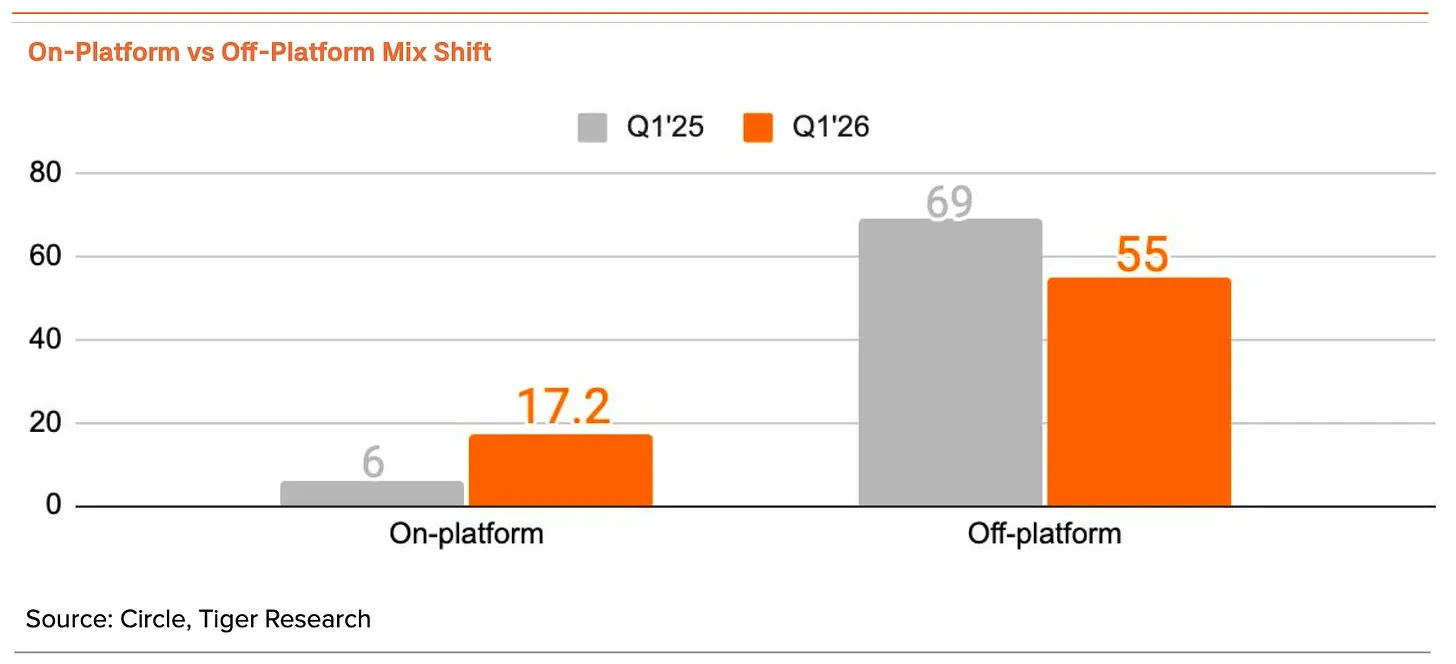

The key driver behind the margin improvement is the continuous rise in the usage proportion of USDC on Circle's proprietary platforms. This quarter, the proportion within the platform increased from 6% to 17.2% (up 1,149 basis points year-on-year), while the proportion outside the platform narrowed to 55%.

This change reflects the success of Circle's own payment network CPN (Circle Payments Network) with institutional clients. The number of member financial institutions increased to 136 in a single quarter (up 36% quarter-on-quarter), with annual total payment volume (TPV) expanding to approximately $8.3 billion (up 17% quarter-on-quarter).

The phased launch of CPN’s payment product line has supported this trend.

- Fiat Payments (launched Q2 2025): Cross-border payments covering over 50 countries, supporting local currency receipts and payments

- Stablecoin Payments (launched Q3 2025): Direct payments and settlements using compliant stablecoins (USDC, EURC) in over 180 countries

- Custodial Payments (Q2 2026, launched in April): Circle provides licensing, custody, compliance, and USDC liquidity through a single integrated API; partners only need to handle fiat currency without bearing the pressures of digital asset custody, operation, and compliance

This is crucial for long-term profit quality, as different ways of attributing income to deposit locations are vastly different. Balances held on external platforms like Coinbase must share reserve interest income with the platform, while balances held on Circle Mint, CPN, and other proprietary platforms fully belong to Circle.

In other words, the higher the proportion within the platform, the lower the partner revenue-sharing costs, thus increasing the RLDC profit margin. With the same revenue scale, Circle's actual profitability correspondingly enhances.

Of course, the fee income from CPN itself has yet to scale significantly. As CFO Jeremy Fox-Geen pointed out in the previous quarter's earnings call, the current priority is to expand the network size rather than accelerate monetization. CPN currently serves more as a channel to bring funds into Circle's proprietary platforms rather than a direct fee channel. As a transition strategy to defend against external distribution costs, Q1 performance confirms the effectiveness of this path.

2. Decline in Net Profit Signals Hidden Behind Growth

However, a noticeable divergence exists between revenue growth and margin improvement, contrasting with the trend of net profit. The net profit for Q1 was approximately $55 million, down 15% year-on-year.

The main reasons are the amortization of stock option expenses after the IPO and a substantial increase in infrastructure and research and development spending before the launch of Arc. After excluding one-time and non-cash items, the adjusted figures remain robust. Nevertheless, the trend of net profit still warrants continuous attention.

Circle Moves Towards Full Vertical Integration

1. USDC: Strengthening Core and Expanding Issuance

In Q1 2026, reserve interest income reached $653 million, accounting for 94% of total revenue. Circle's core business is highly concentrated on reserve interest, and revenue growth depends on the continuous expansion of USDC issuance.

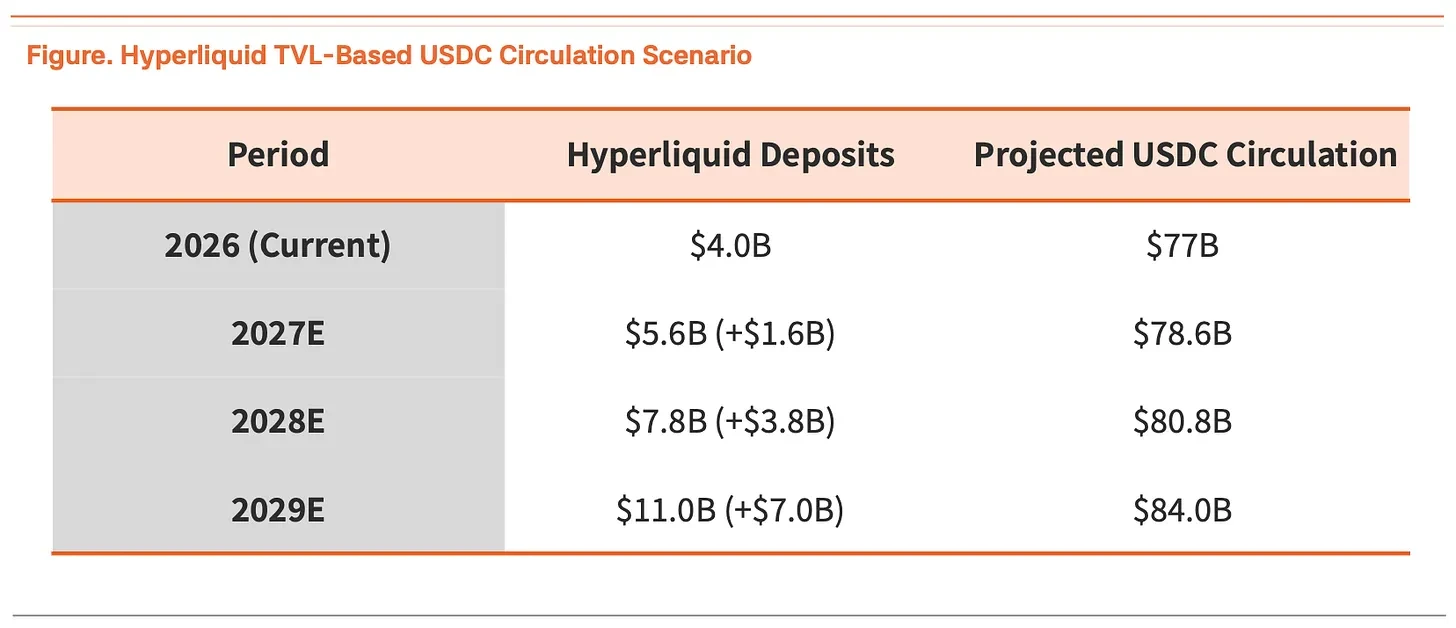

The current circulation of USDC is about $77 billion. The central issue of Circle's structural growth is how far this circulation limit can be pushed. The previous rapid expansion of USDT relied on its early positioning in Binance trading pairs.

Circle plans to replicate this "grab" approach on the DEX platform Hyperliquid. The recent acquisition of the native stablecoin USDH by Coinbase is a typical example—Hyperliquid did not deploy USDH as a native trading pair but sold it instead, registering USDC as the official base trading pair.

The deposit growth on Hyperliquid directly drives USDC issuance. Hyperliquid's TVL grew from $2 billion in Q1 2025 to $4 billion in Q1 2026, peaking at $6 billion. As Hyperliquid uses USDC as the base deposit asset, platform growth directly translates into new USDC issuance. The projected circulation outlook based on this is as follows.

In this scenario, the incremental contribution from just the Hyperliquid platform is expected to raise the total USDC circulation from $77 billion to $84 billion within three years. A single platform will contribute over 10% of the total circulation, becoming a significant issuance channel.

Transferring 90% of reserve interest income to the platform does compress recent margins. However, the returns obtained are unparalleled in scale—approximately 15 trillion Korean won (around $11 billion) in daily transaction volume and a 17% share of the DEX derivatives market. This deal is nearly acceptable.

If the Hyperliquid derivatives product line further materializes, the positive cycle structure will become even more stable. For Circle, which prioritizes circulation expansion over margins, even if profit-sharing is required, Hyperliquid represents a strategic stronghold worth seizing.

2. Arc: How Circle Breaks Free from Interest Rate Dependency

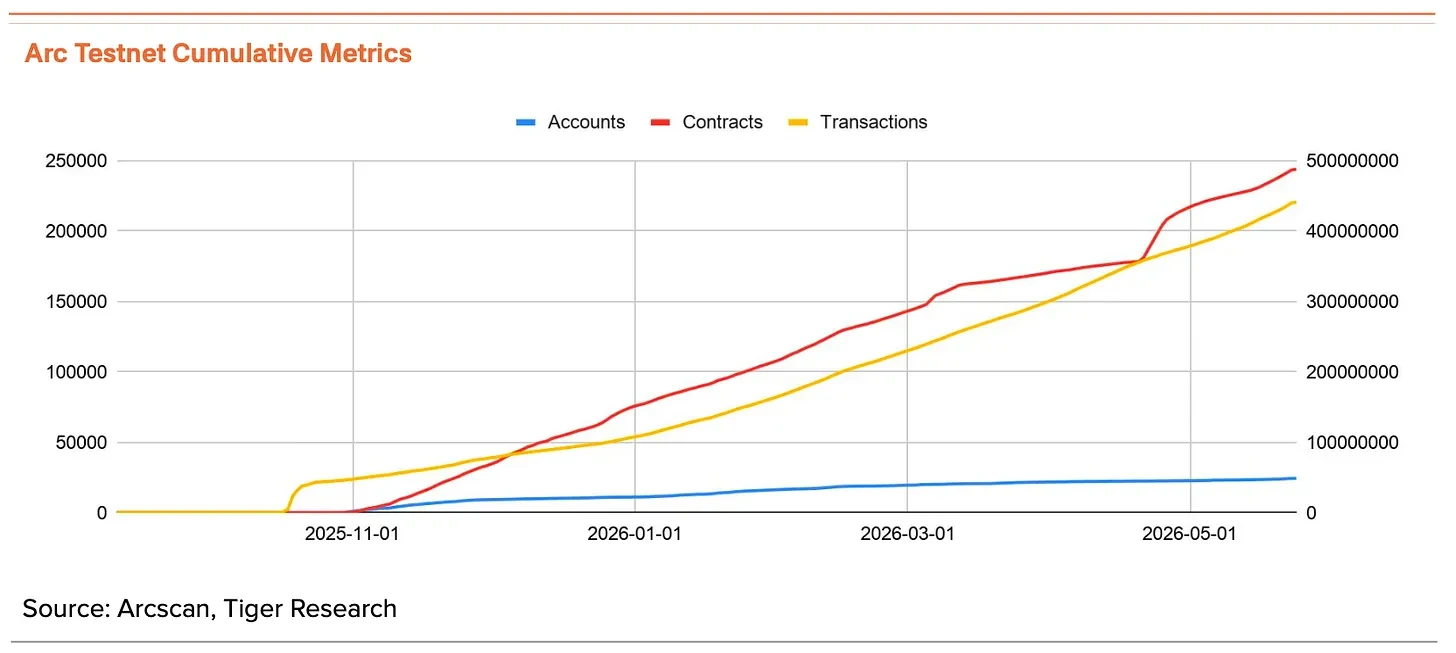

As mentioned earlier, Circle's revenue is highly concentrated on reserve interest, making its business structure structurally vulnerable during a rate-cutting cycle. Arc is still in the testnet phase and has not yet generated visible revenue. With recent institutional financing of approximately $222 million, Arc has emerged as core infrastructure fundamentally cutting off interest rate dependence.

The primary target market for Arc is global cross-border payments. According to the World Bank report (RPW No. 54), the global average remittance cost is 6.36%, with bank remittance costs as high as 14.99%. The high-cost structure is caused by multi-tiered intermediaries in SWIFT, opaque forex spreads, and delays in weekend settlements.

In response to these inefficiencies in traditional finance, Circle aims to build platform business revenue on Arc. Reducing reliance on interest through infrastructure fee income is based on two major pillars.

Circle Payments Network (CPN): Connecting global institutions and enterprises to Arc for cross-border payments and settlements while charging processing fees from the traffic. The institutional onboarding in Q1 is laying the foundation for transaction revenue post Arc mainnet launch.

On-chain Forex Engine (StableFX): Supporting on-chain stablecoin exchanges, replacing the high intermediary spreads of traditional forex. During execution, smart contracts collect preset fees from each transaction currency.

StableFX adopts an RFQ quoting model instead of SWIFT's fixed cost structure. Market makers compete in real-time, providing optimal wholesale spreads. Large transfers can settle 24/7 without SWIFT’s fixed fees and without slippage.

The more traffic on CPN and the transaction volume of StableFX, the more direct infrastructure and fee income. This forms a closed loop of non-interest income structure.

This transformation has been validated through the testnet and participating enterprises. According to Arcscan data, the public testnet has recorded around 430 million transactions since its opening, with approximately 3.26 million within the last 24 hours. Over 100 global institutions have participated, including BlackRock, HSBC, Visa, and AWS.

In addition to traditional financial institutions, the blockchain prediction market Polymarket has also joined the ecosystem.

This is not just a pilot for products and platforms. Arc is attracting real enterprises and driving real transaction flows. If Arc operates as expected, Circle's revenue structure will expand from USDC reserve interest to infrastructure operation income. Arc is the first step in breaking free from interest rate ties.

According to the roadmap, Arc's mainnet is scheduled to launch this summer. Meaningful Arc revenue is expected to gradually materialize after the mainnet launch.

3. Agent Stack: Blueprint for Autonomous AI Payments

The "agent economy," where AI entities replace humans in decision-making and autonomously complete transactions, is approaching. Global tech giants like Google and OpenAI have begun actively deploying such autonomous systems.

The bottleneck lies in payment infrastructure. The fees generated by AI entities calling APIs are priced in micropayments (sub-cent levels), which traditional payment systems cannot handle. Routing such micropayments to credit card networks will result in fees exceeding the principal—every transaction would incur a loss. Structurally, agent payments cannot fit into existing card tracks.

Circle aims to fill this gap by launching the "Circle Agent Stack" with USDC as the settlement asset and providing a toolkit to build supporting environments.

- Agent Wallets: AI autonomously holds and sends USDC within the rules set by humans (e.g., spending limits)

- Agent Marketplace: A shop where AI procures API services and settles by usage

- Agent Nanopayments: Instant USDC settlements starting from about $0.000001, with zero Gas fees

- Circle CLI: A command-line tool for creating wallets and connecting agents

- Circle Skills: Enabling AI agents to directly call modules of Circle's financial products

Currently, this portion of revenue has also yet to reach a visible stage. The market adoption and revenue recognition path is expected to advance along the following phased roadmap.

2026 (Infrastructure Phase): Building the technical foundation for processing large-scale micropayments. The Arc mainnet will be activated this summer, anchoring the integration of partners with Circle CLI and financial modules.

2027 (Regulatory Anchoring Phase): The "GENIUS Act" will formally take effect, providing institutional assurance for enterprises. Exemptions for stablecoin securities and 100% backing by safe assets will be established at the legal level, allowing even conservative enterprise legal teams to trial the USDC payment system internally without risks.

2028 (Commercialization and Monetization Phase): Technical foundations and regulatory legitimacy will be fully aligned. The agent economy will be fully commercialized. Enterprises will grant real spending authority to AI entities, leading to large-scale transactions, and the contributions of Agent Stack will officially reflect in financial report revenue.

Therefore, before traffic-driven revenue is fully realized in 2028, Agent Stack will be more reflected in the stock price as an "expected premium"—this is the capital market's pricing of future market positioning value, rather than a realization of current revenue.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。