Detailed Interpretation of the China Securities Regulatory Commission's Investigation of Tiger, Futu, and Changqiao Cases — What are the key red lines this time? What is the impact on individuals?

Presumably, everyone knows that today the China Securities Regulatory Commission penalized Tiger, Futu, and Changqiao, three brokerage companies, but what are the main reasons for the penalties? Let’s discuss it in detail.

This time, the regulatory commission released three articles regarding the punishment, which I have all taken screenshots of, namely:

1. The CSRC seriously investigates the illegal cross-border business operations of Tiger and other institutions.

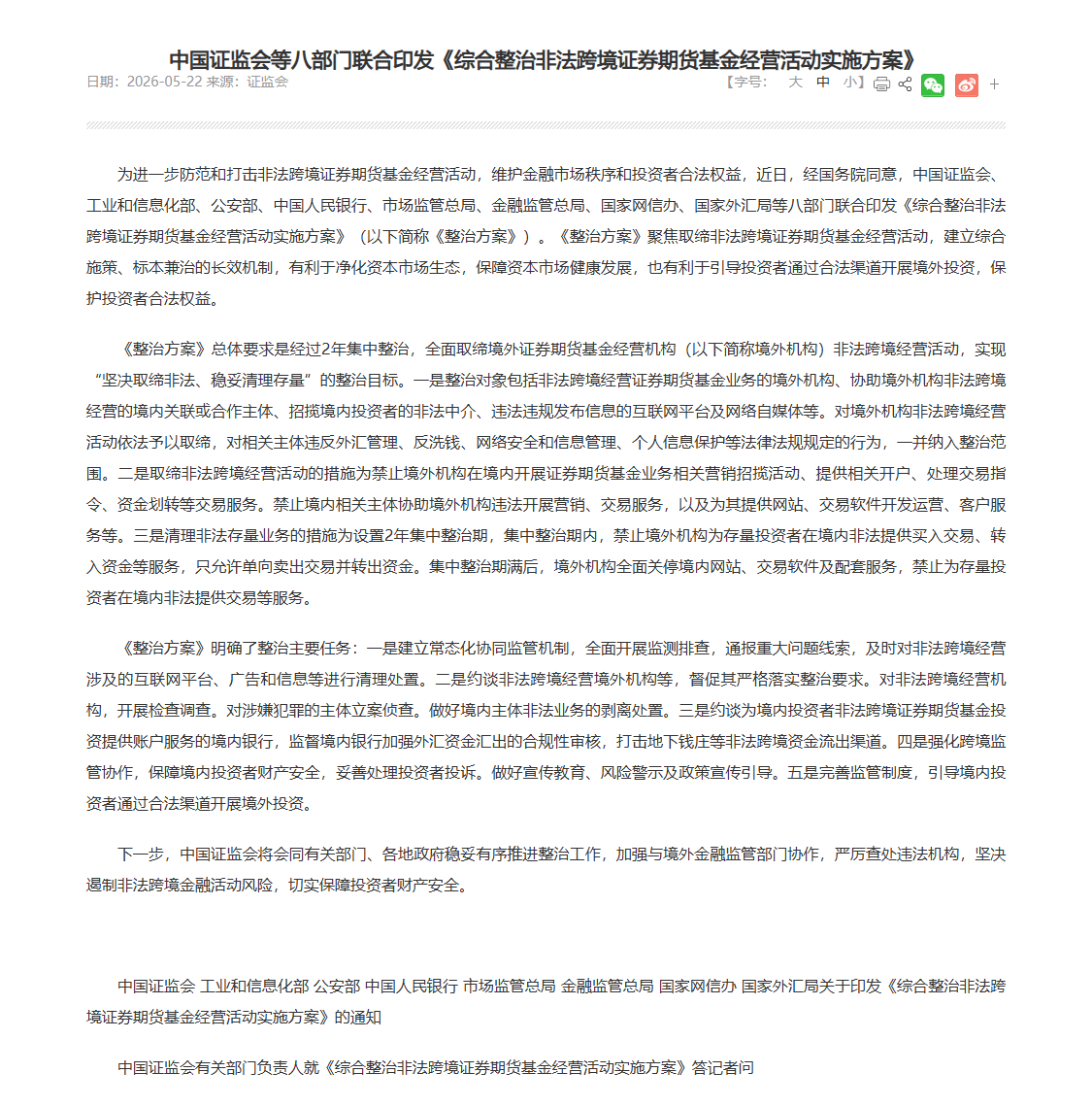

2. The China Securities Regulatory Commission and eight other departments jointly issued the "Implementation Plan for Comprehensive Rectification of Illegal Cross-Border Securities, Futures, and Fund Business Activities."

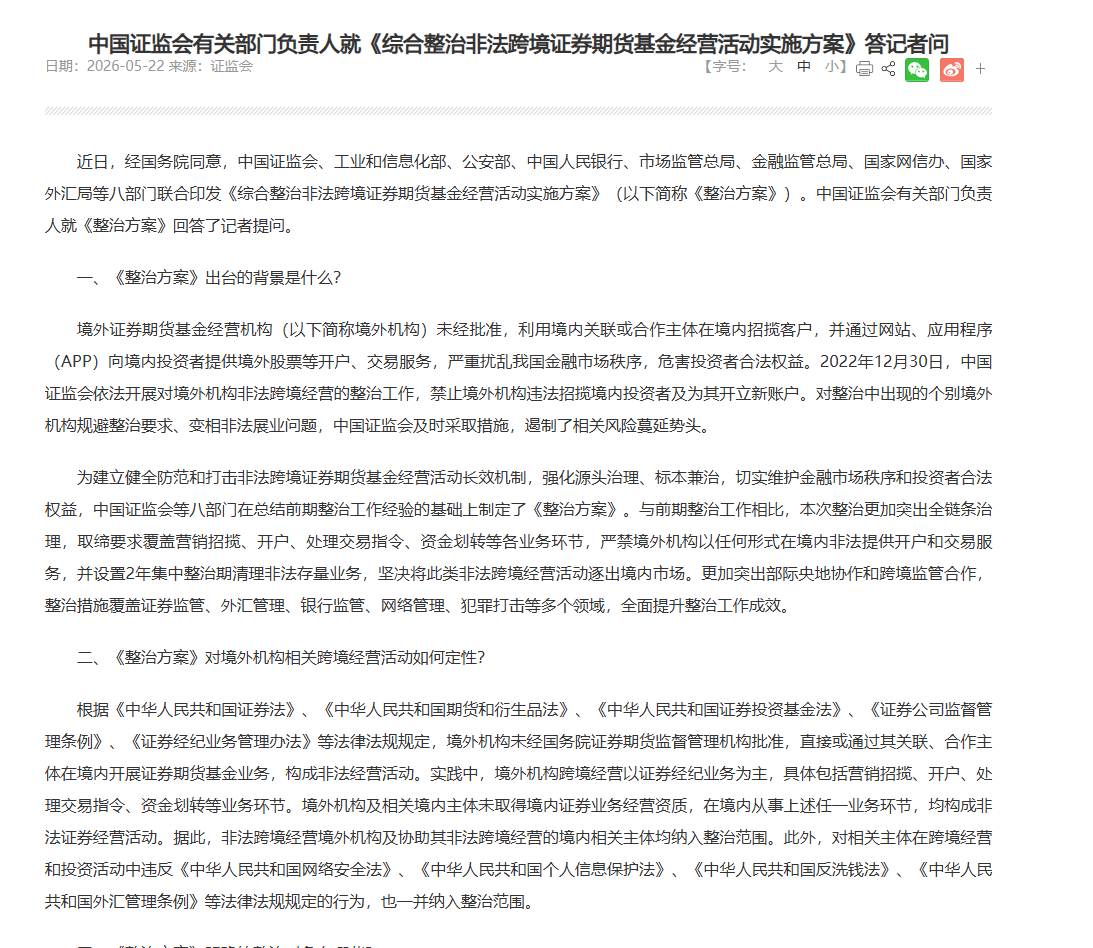

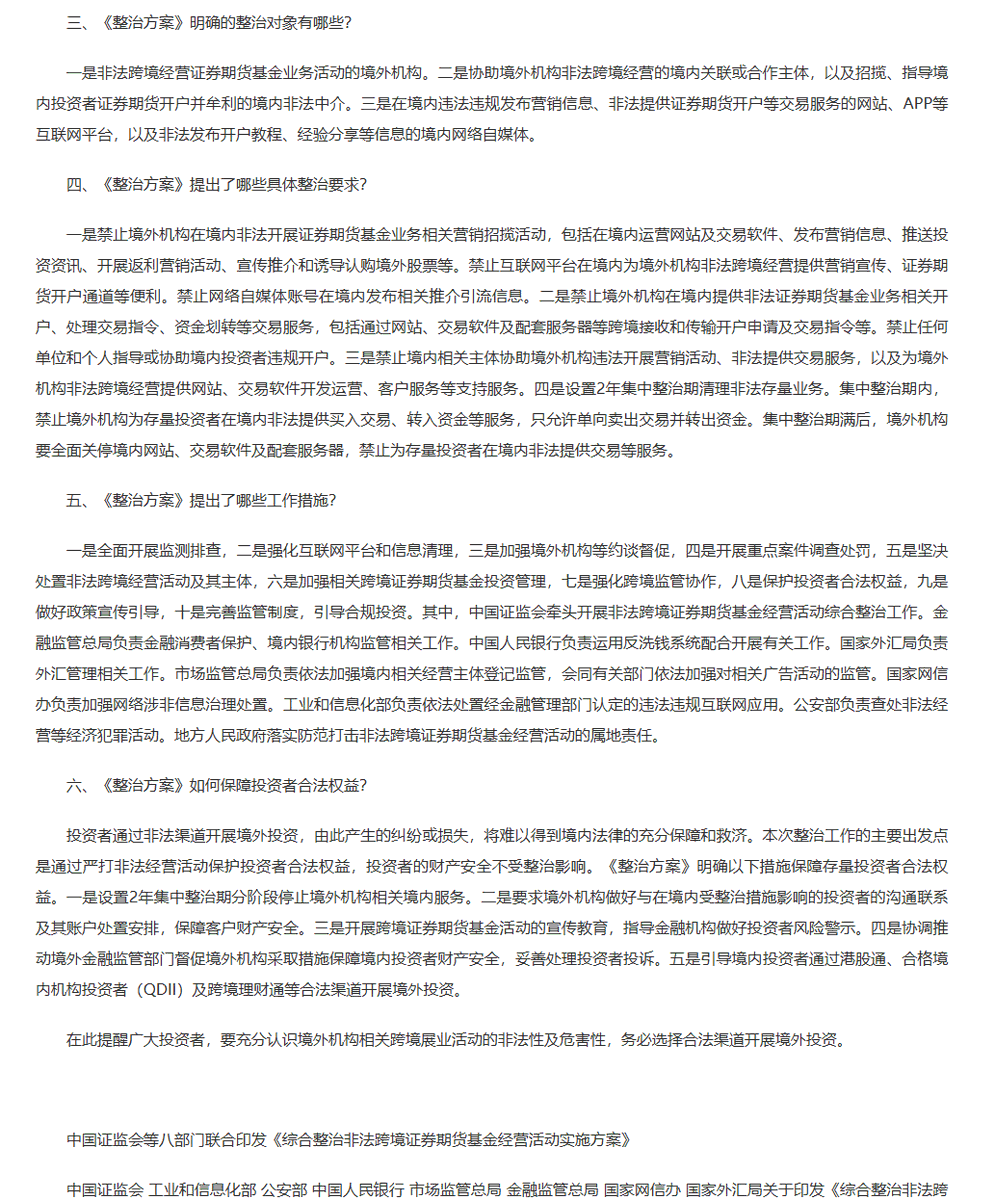

3. A responsible person from the CSRC answered reporters' questions about the "Implementation Plan for Comprehensive Rectification of Illegal Cross-Border Securities, Futures, and Fund Business Activities."

The initial qualification is:

“The relevant entities of Tiger, Futu, and Changqiao, both domestically and abroad, conducted securities brokerage business and securities financing business without approval and without obtaining the necessary licenses, while conducting related securities business services such as marketing and promotional activities for securities trading, handling trading instructions, and obtaining relevant profits, constituting illegal operation of securities business.

In addition, the three institutions’ domestic and foreign relevant entities also engaged in illegal public fund sales and illegal futures brokerage activities.”

It appears that these three companies conducted business in China without a license; while they all have licenses overseas, they do not hold one within China, which is the fundamental original sin.

From the perspective of Chinese regulation, although the transactions occur in foreign markets, such as Hong Kong stocks and US stocks, the clients are in China, marketing is in China, account opening guidance is in China, trading instructions are initiated from within the country, and the capital also involves the cross-border flow of domestic residents, it is not just a simple foreign brokerage service for foreign clients, but rather unlicensed securities operations inside China.

If it were only a matter of licenses, it would be too simplistic; the root cause still lies in "cross-border capital flow."

The political plan released by the regulatory commission this time has three clear points:

1. The targets for rectification include foreign institutions illegally operating securities, futures, and fund businesses, domestic affiliated or cooperating entities assisting foreign institutions in illegal cross-border operations, illegal intermediaries soliciting domestic investors, and internet platforms and self-media that publish information in violation of laws and regulations.

2. The measures for eradicating illegal cross-border operations include prohibiting foreign institutions from conducting marketing and solicitation activities related to securities, futures, and funds within China, as well as providing related account opening, handling trading instructions, transferring funds, and other transaction services.

3. The measures for clearing illegal existing businesses involve setting a two-year focused rectification period during which foreign institutions are prohibited from illegally providing transactional services such as buying trades and transferring funds to existing investors in China, allowing only one-way selling transactions and fund transfers out.

These three points again clarify the theme of "unapproved channels for resident funds to invest abroad."

At this point, there is a very clear context: the current rectification superficially targets illegal cross-border operations, but essentially aims to cut off unapproved channels for domestic residents to invest overseas, particularly cutting off the inflow of new capital to foreign brokerage accounts.

In simple terms, it is about cracking down on domestic capital going overseas through foreign investments.

This means China is systematically closing down the "foreign licenses + domestic client acquisition + app trading + cross-border capital flow" financial channels.

This further illustrates that even if you have an international license, as long as you solicit Chinese users as customers, you will need a Chinese license; without it, you are operating illegally.

More critically, this represents a convergence of capital account controls, financial license regulations, data supervision, anti-money laundering regulations, and internet platform supervision. If it were just violations of securities business, the CSRC alone would suffice, but this time it involves the CSRC, the central bank, the foreign exchange bureau, public security, internet information, market regulation, and the financial supervision administration—eight departments working together—indicating that the regulatory target is no longer merely "unlicensed securities brokerage," but rather a cross-border capital entrance that circumvents the domestic financial regulatory system.

Thus, even if you have a license, if it is determined that you are assisting domestic funds to go overseas, you will still be penalized; licenses are a strict requirement, but not the only one.

Of course, domestic investors buying US stocks and Hong Kong stocks are not completely denied, but must be routed through officially recognized channels, such as QDII, mutual recognition of funds, mutual connectivity, qualified domestic and foreign institutional arrangements, or other regulatory recognized cross-border investment channels in the future.

So surely someone will ask, is it illegal to buy or sell US stocks or Hong Kong stocks through brokers like Charles Schwab, Interactive Brokers, or BIT now?

From the currently published documents, the entities targeted in this crackdown are the brokerage firms, while individuals are not the main objects of punishment in this rectification; in other words, if individuals merely buy and sell stocks through brokerage firms, it does not involve any rectification or punishment.

Therefore, as individual investors, they are currently safe and will not face any punitive measures. However, "domestic illegal intermediaries soliciting and guiding domestic investors to open accounts for profit" fall within the scope of punishment this time.

Although I guess everyone might not care, the fact is, if you are still promoting foreign brokers within China, guiding domestic investors to open accounts and buy and sell US stocks, it is indeed illegal.

Currently, the three illegal activities defined by the CSRC that can lead to personal accountability are:

1. Individuals continuing to provide referrals, account opening links, tutorials, community guidance, collecting commissions, or rebates may be recognized as illegal intermediaries.

2. Individuals assisting others in fund deposits, currency exchange, splitting currency purchases, custody, or transfers not only involve securities issues but may also concern foreign exchange and anti-money laundering.

3. Individuals utilizing false purposes for currency purchase, circumventing quotas, unclear sources of funds, or tax evasion will not be penalized based on this securities rectification but on foreign exchange, tax, and anti-money laundering rules.

These three points directly implicate individuals; of course, from an enforcement perspective, it doesn't mean that if you have posted a promotional message, you will be arrested. It should be if it involves certain cases or individuals, it could easily become joint liability, and if someone reports it, there is a high probability of risk.

To summarize:

China is including residents’ cross-border investments into national financial management. Previously, users could bypass the constraints of domestic financial market product supply simply by downloading apps, completing KYC, binding bank cards, and converting currency to fund their investments. Now, regulations need to be redefined to state that as long as services are effectively rendered to domestic residents, foreign licenses cannot be used to circumvent Chinese licensing, foreign exchange, data, anti-money laundering, and investor protection regulations.

This is also of reference significance for cryptocurrency, RWA, tokenized stocks, pre-IPO, and structured products abroad. Future issues will not only focus on whether there are licenses overseas and if they are compliant enough, but it will shift to whether marketing, account opening, providing trading entry, handling fund paths, offering Chinese customer service, and referral through KOLs are directed at domestic users.

As long as these paths exist within China, they could potentially be dealt with as illegal cross-border financial activities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。