During this 13F disclosure season for the US stock market, one of the most closely watched funds is not Bridgewater or Berkshire, but a fund with a very unique name—Situational Awareness LP.

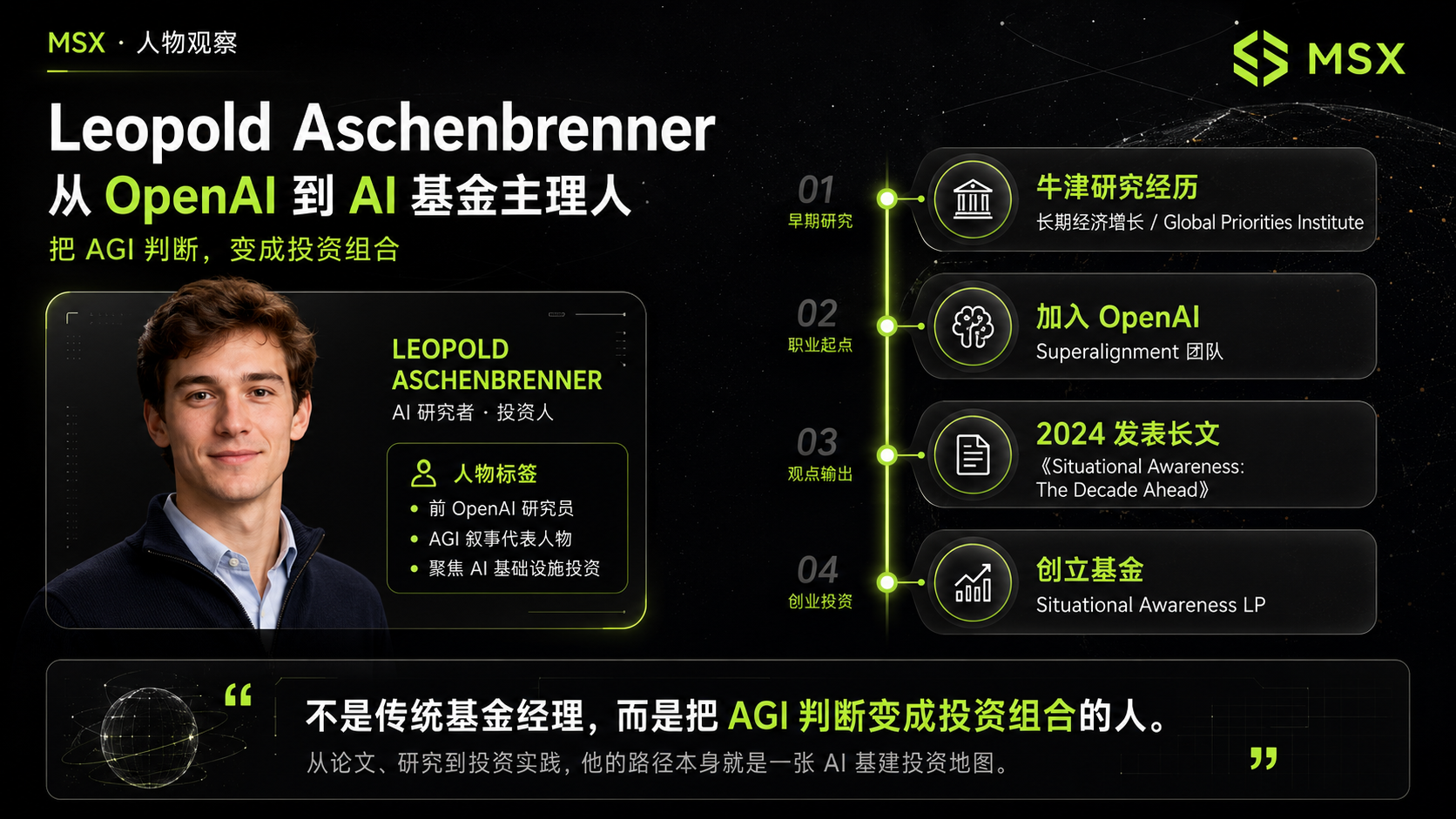

Its principal Leopold Aschenbrenner is not a traditional Wall Street veteran but a former member of the OpenAI Superalignment team. In 2024, he published a lengthy article titled “Situational Awareness: The Decade Ahead”, which presents a very radical view that AGI may arrive more quickly than most people imagine, and what will truly be scarce in the future is not just model capability itself but also compute power, electricity, data centers, chips, storage, and the national-level resource competition surrounding the AI arms race.

Two years later, it has been proven that he was right.

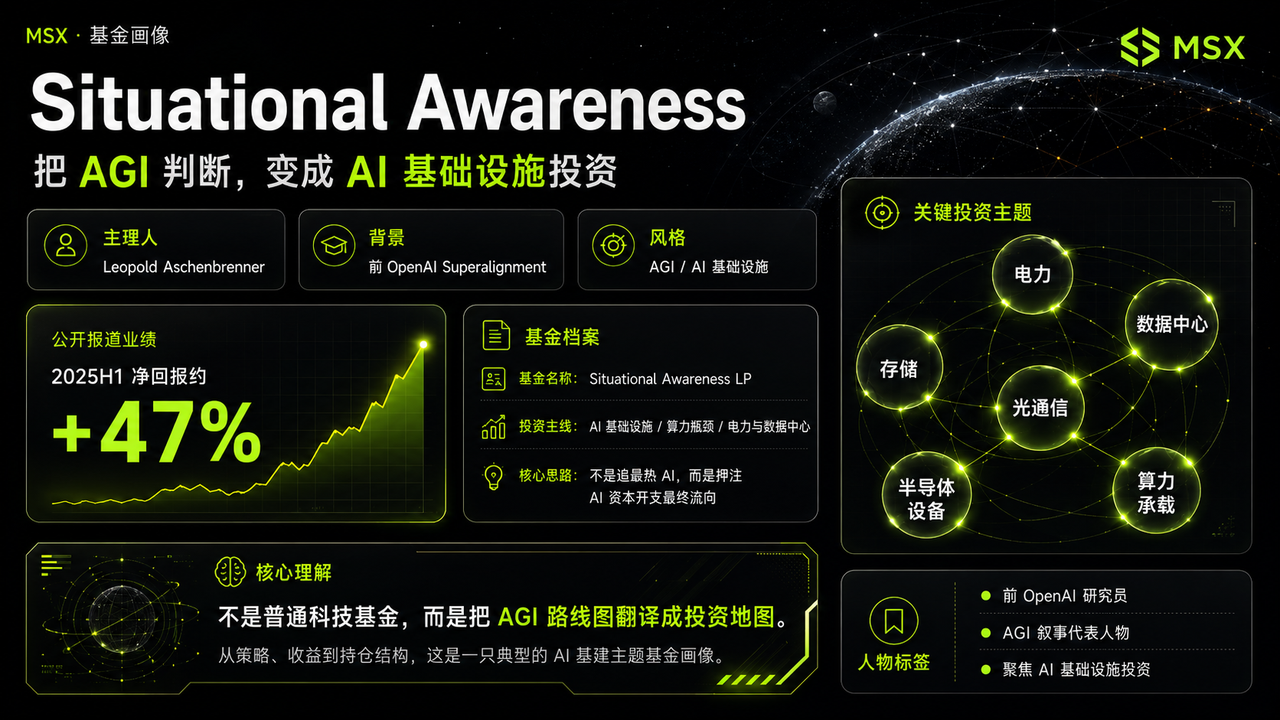

Leopold has internalized a set of judgments about the future of AGI over the next decade and mapped these judgments onto capital markets. That is why Situational Awareness, from its inception, has not behaved like an ordinary tech fund but has more closely resembled a direct translation of the AGI roadmap into an AI infrastructure investment map.

This is why every move in the AI investment field garners much attention from the market, and the latest disclosed 13F documents indicate that this most knowledgeable AI bull seems to be quietly building a massive position in put options.

1. SALP: A product that turns AGI belief into a fund

Public information shows that Leopold founded a company focused on AGI, supported by prominent Silicon Valley figures such as Patrick Collison, John Collison, Nat Friedman, and Daniel Gross.

According to market reports, Situational Awareness achieved a net return of approximately +47% after fees in the first half of 2025, significantly outperforming the S&P 500 and technology hedge fund indices during the same period. Its uniqueness lies in the fact that it does not merely take a bullish view on tech stocks but focuses heavily on AI infrastructure, betting on where AI capital expenditure will ultimately flow.

As mentioned at the beginning, its underlying logic is that if AGI truly accelerates, the first companies to be revalued may not be those at the application layer but those that control compute power, electricity, data centers, storage, optical communications, semiconductor equipment, and energy resources. Therefore, its high returns do not rely on simply buying an index but rather on a selection of highly elastic AI infrastructure targets, such as Bloom Energy, Sandisk, Lumentum, CoreWeave, and Core Scientific.

Here it is necessary to explain what a 13F is.

A 13F is a quarterly disclosure document submitted by institutional investment managers to the SEC in the United States, typically used to observe the quarterly holdings changes of large funds in US stocks, ETFs, and related options. However, it is essentially only a snapshot at the end of the quarter, revealing "what was disclosed at a certain point in time," and cannot fully reconstruct the entire trading strategy of a fund, especially regarding options, as the 13F does not show exercise prices, expiration dates, nor whether it corresponds to other positions, nor derive the fund's true net exposure directly.

This is also where misinterpretation occurs most easily when interpreting this document.

The report date for this Q1 13F is March 31. Last10K shows the document was submitted on the evening of May 15 in the Eastern US, but the SEC acceptance date was May 18. This means it was not simply “not submitted,” but rather there was a time delay between the submission and when the market actually saw the disclosure results, which is why there has been much discussion about "waiting for Leopold's 13F" on social media platforms.

More importantly, the results of this 13F disclosure do not entirely align with initial market expectations. Many expected that Leopold would continue to significantly increase positions in core AI assets like Nvidia, Broadcom, AMD, TSMC, and ASML. However, the reality is that SALP has established a large number of PUT options positions, covering SMH Semiconductor ETF, Nvidia, Oracle, Broadcom, AMD, Micron, TSMC, ASML, Intel, and other core AI and semiconductor targets.

This has prompted the market to rethink a question: Why is the person who believes most in the acceleration of AGI starting to buy insurance for AI leaders?

If it’s merely summarized as “bearish on AI,” it’s too simplistic; the real analysis should consider the macro context in which he made this move and what changes in the AI trading structure this reflects.

2. Understanding SALP's latest 13F: From betting on AI to managing AI volatility

The most shocking action revealed in this 13F is that SALP has established a large number of put options positions:

- The largest is a PUT on the SMH Semiconductor ETF, disclosed at a value of approximately $2.043 billion;

- Followed by a PUT on NVDA, approximately $1.568 billion;

- Then an ORCL PUT, approximately $1.073 billion;

- AVGO PUT, approximately $1.006 billion;

- And AMD PUT, approximately $969 million;

- Additionally, it has established new positions in MU PUT, TSM PUT, ASML PUT, INTC PUT, etc.;

On the surface, this seems like a bearish stance on AI leaders, but the issue is that PUTs do not necessarily represent unilateral shorting—after all, the option amounts in a 13F are more about disclosing the nominal value according to the scale of the underlying securities and do not equal the real premium costs actually invested by the fund. More importantly, the 13F does not reveal exercise prices, expiration dates, whether it corresponds with other positions, nor does it show the real net exposure in the portfolio.

Therefore, to simply state that Leopold is “completely bearish on Nvidia and semiconductors” is not precise; a more reasonable interpretation is that he is buying “insurance” for his long positions in AI infrastructure, as many of the assets originally held by SALP are themselves high elastic, high volatility, and interest rate-sensitive companies, such as Bloom Energy, CoreWeave, Core Scientific, IREN, Applied Digital, and Sandisk mentioned previously, whose long-term logic is related to AI infrastructure but whose short-term prices are often very dependent on risk appetite and valuation environment.

Once the market begins to reduce risk due to rising oil prices, recurring inflation, high interest rates, or geopolitical conflicts, these high-elasticity assets are often the first to be sold. This also relates to the macro context at the end of March: on one hand, the situation in the Middle East and the risks of US-Iran conflict have raised expectations for oil prices; on the other hand, rising oil prices will exacerbate inflation stickiness, decreasing market confidence in rate cuts.

For high-valuation growth stocks, this means “double pressure”: rising oil prices push up inflation, inflation suppresses rate cuts, and if interest rates do not go down, the valuations of long-duration tech assets will be compressed.

Given this context, Leopold's action of establishing a large number of PUTs becomes easier to understand; he is not denying AI, but rather acknowledging that even if the long-term logic of AI is strong, it cannot completely ignore macro headwinds.

Especially for a fund like SALP, where many assets are high beta. If they only hold offensive positions, once the market experiences a systemic pullback, the portfolio's net value will fluctuate significantly. By buying PUT options on liquidity-rich and representative core AI assets like SMH, NVDA, AVGO, AMD, and ORCL, it can use relatively standardized tools to hedge against the systemic pullback risk of the entire AI trade.

The true implication behind this is that Leopold has not turned from an AI bull into an AI bear, but shifted from a "one-sided aggressive long position on AI" to "continuing to bet on AI infrastructure while starting to manage path volatility."

This represents a more mature approach to portfolio management.

3. So where is Leopold's offensive direction?

If the newly established PUTs address the “defensive issue,” then the added, reduced, and cleared positions truly inform us about Leopold's offensive direction.

From the disclosures, SALP has retained and increased positions in several AI infrastructure-related targets, for instance, a slight increase in Sandisk's underlying stock, and CoreWeave's underlying stock, IREN, Applied Digital, Riot Platforms, CleanSpark, Bitfarms, Bitdeer, etc., are also on the increase list. Key long positions still retained include Bloom Energy, Sandisk, CoreWeave, IREN, Core Scientific, and Applied Digital.

This indicates that it has not abandoned AI; on the contrary, it remains committed to the same long-term logic: AI capital expenditure will continue to be transmitted downwards, and the real beneficiaries will be those companies that control electricity, data centers, storage, compute capacity, and infrastructure bottlenecks.

This is very close to the main judgment of MSX for Q2. In our article AI infrastructure surged throughout Q1; by Q2, who can still sustain “high valuation”?, we emphasized that the focus of AI trading has shifted from purely GPUs to networks, storage, and electricity, and now the market is more concerned with the continued expansion of capital expenditures by large firms, ultimately flowing towards which orders, revenue, and profit. The advantages of equipment, networks, storage, and electricity are not because they are more appealing, but because they align better with the current market's aesthetic for realizable capabilities.

From this perspective, SALP's long positions are very representative: Bloom Energy corresponds to electricity and independent energy supply; CoreWeave, Applied Digital, Core Scientific, and IREN correspond to data centers, compute hosting, and infrastructure support; Sandisk, Micron, and TSM positions correspond to storage, semiconductor manufacturing, and hardware supply chains.

In other words, Leopold is not avoiding AI; he is more concerned with where AI money is ultimately spent and who can convert that money into revenue on the financial statements.

When looking at reductions and closures, there is also a wealth of information. SALP has closed positions in INTC CALL, Lumentum, Cipher Mining, and reduced positions in CoreWeave CALL, Bloom Energy, Core Scientific, among others. The most notable point here is that it is not simply withdrawing from a particular direction but reducing a portion of positions that have already risen significantly, exhibit high volatility, or possess stronger leverage attributes.

For instance, in the case of CoreWeave, it has reduced its CALL while still holding onto the underlying stock, indicating it has not completely abandoned CoreWeave but is shifting from a more aggressive options expression back to a more controllable underlying stock expression. Likewise, for Bloom Energy and Core Scientific, the reductions do not imply failure of logic, but more likely risk management and return realization at the portfolio level.

The complete liquidation of Lumentum is even more intriguing. In the MSX Q1 recap, AI hardware and optical communications were the two strongest main lines, with AXTI, AAOI, LITE, LWLG achieving doubling-level growth. The strength of optical communications essentially stems from the explosion in demand from AI data centers for optical interconnects, optical modules, and network links, but the issue is that the stronger a main line performs in Q1, the more likely it is to face crowded trades and declining risk-reward ratios in Q2.

Therefore, Leopold clearing LITE and reducing some high-elasticity AI infrastructure positions does not necessarily indicate that he no longer views this direction positively, but could more realistically acknowledge that the most successful trade from Q1 may not necessarily be the trade with the best cost-performance ratio in Q2.

This is the most important aspect of this repositioning, as it is not denying AI but actively making a structural switch, moving from indiscriminately buying all AI chains to retaining those assets that can better sustain long-term capital expenditures, hold more infrastructure attributes, and endure macro fluctuations.

What he has given up is not AI, but rather the linear fantasy that “all AI will rise together.”

This 13F is essentially just a snapshot as of March 31 and does not represent that Leopold still holds exactly the same positions as of May, but it still provides strong insights into the current market conditions.

First, the long-term main line for AI has not ended, but the trading structure has changed; the future will not simply see every AI increasing but will focus on who can deliver results, who can earn premiums, who is too crowded, and thus needs hedges.

Second, in a high oil price, high-interest rate, high-volatility environment, the truly effective strategy is not simply full offense nor comprehensive defense, but rather defense in offense—core positions betting on certainty, marginal positions betting on elasticity, while using hedging tools to control the portfolio's drawdown. Essentially, Leopold's actions this time demonstrate this logic through real positions.

Third, this also confirms a significant change in the US stock market by 2026: index beta is weakening while structural alpha is strengthening. In the past, just buying the seven sisters or Nvidia might have guaranteed success; but now the market is more selective, it will ask every company: can your AI story ultimately turn into orders? Can it turn into revenue? Can it turn into profit? If not, even high valuations will be compressed.

This is also why AI infrastructure 2.0 will become important. In the future, funds will not only look at GPUs but will seek true realizable segments along the compute power → interconnection → storage → electricity → data center infrastructure chain.

Final Thoughts

If viewed superficially, the most eye-catching aspect of this 13F is that string of huge PUT options.

But if one truly reviews the entire portfolio, one will realize that Leopold is not “turning from an AI bull to a bear” but rather undertaking a more mature upgrade: still betting on AI infrastructure in the long term, while short-term recognizing the volatility risks of high-valuation, high-elasticity assets.

This is the most significant takeaway from this 13F; it indicates that while the direction of AI may still be correct, the path to that direction will definitely not be linear.

For real fund managers, what matters has never been just betting correctly on the endpoint, but also to survive and navigate through volatility along the way.

For ordinary investors, the greatest insight from this 13F is clear: AI trading in 2026 has transitioned from “buying stories” to “buying realizations”; from “buying leaders” to “finding bottlenecks”; from “one-sided offense” to “offense with defense.”

This is the most interesting and certainly should not be overlooked signal.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。