The regular army is here! SEC approves NYSE new regulations, RWA and US stocks on-chain are about to enter the era of "transfer of rights"!!

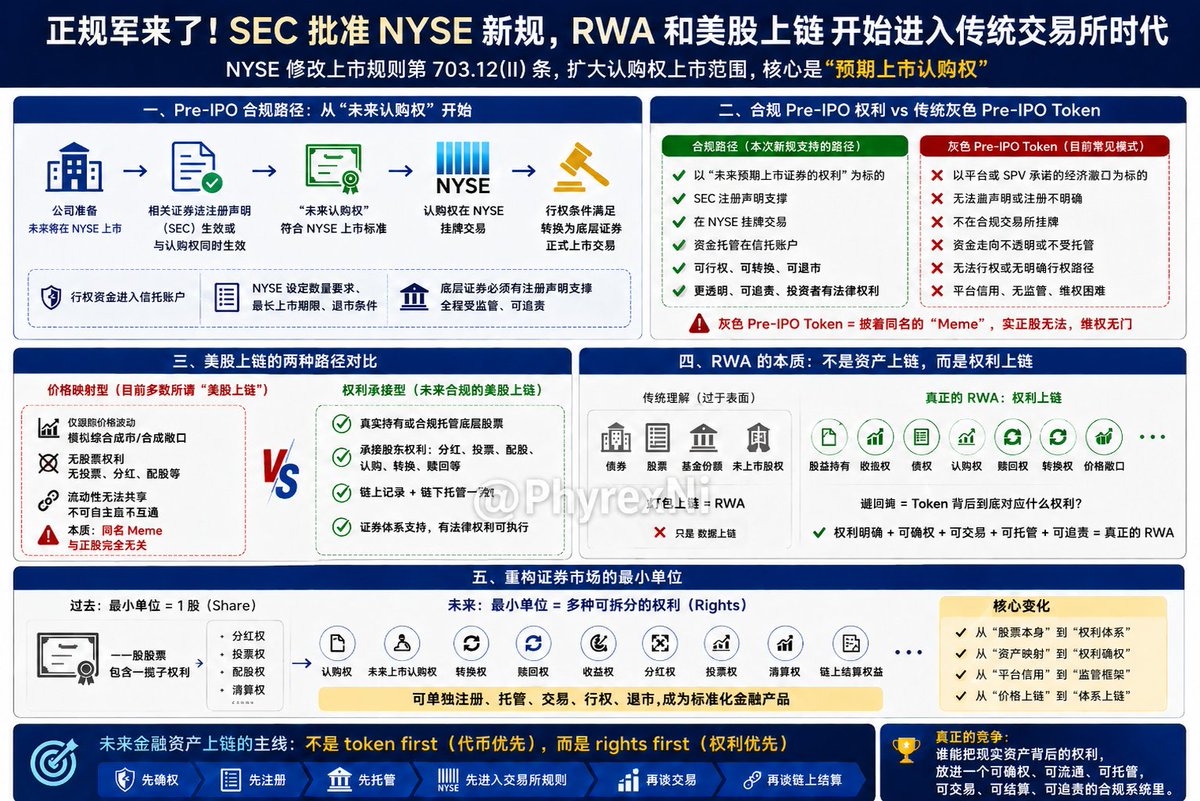

Today, the New York Stock Exchange received SEC approval to amend Section 703.12(II) of the NYSE Listed Company Manual, expanding the scope of subscription rights listed on the New York Stock Exchange.

The core of this amendment is the "anticipated listing subscription rights." In other words, the underlying securities themselves have not officially entered the trading stage. As long as these securities will be listed on the New York Stock Exchange in the future, and the related securities law registration statement has been announced effective by the U.S. Securities and Exchange Commission, or it becomes effective simultaneously with the listing of subscription rights, then this future subscription right can already be traded on the New York Stock Exchange.

What is this? This is a prototype of Pre-IPO moving towards a compliant exchange framework. It is also the core issue that Pre-IPO, RWA, and US stocks on-chain truly face in both traditional finance and cryptocurrency sectors recently.

In the past, many so-called Pre-IPOs were essentially not investors actually buying shares of OpenAI, SpaceX, Anthropic, or Stripe, but rather purchasing an economic exposure promised by a platform, an SPV, or an issuer. Investors think they are buying equity, but in reality, they may not hold shareholder status, voting rights, dividend rights, information rights, or direct control of real shares.

This is the biggest problem with many Pre-IPO Tokens now. What users purchase actually has nothing to do with the underlying stocks; it is merely a "Meme" cloaked in the same name. There is simply no entity to defend their rights!

This new regulation from the NYSE starts from the framework of traditional securities law, first confirming rights, confirming registration statements, and confirming the future underlying securities will enter the NYSE listing system, before allowing these future subscription rights to be listed on the exchange.

This is the key point.

Future truly compliant Pre-IPO will turn the "right to obtain listed securities in the future" into a product that can be registered, custody, traded, exercised, delisted, and be subjected to regulatory accountability. The difference from many current Pre-IPO Tokens is that the latter is more about platform credit, while the former pertains to securities rights under exchange rules.

Besides Pre-IPO, this amendment also holds very important significance for US stocks on-chain.

If US stocks on-chain only mean mapping stocks like Nvidia, Tesla, and Apple onto the chain, then it’s merely price on-chain, or even closer to Contracts for Difference or synthetic exposure. This is what I have been saying — the ceiling is very low, and many so-called US stocks on-chain are merely a same-name Meme.

Liquidity cannot be shared; the same US stock mapped on different platforms is a different thing. At most, it is merely an exposure tracking price fluctuations, not to mention holding shareholder rights, nor does it mean users can participate in dividends, voting, stock allotments, subscriptions, conversions, redemptions, and a series of corporate rights events.

True US stocks on-chain must not only include the names of the stocks, but also require shareholder rights. Stocks can be tokenized, but all rights behind the stocks must also be addressed. Otherwise, so-called US stocks on-chain are merely transferring stock prices onto the chain, not the securities system.

Moreover, this time it is not simply allowing securities to go on-chain, but rather reconstructing the smallest unit of the securities market.

This has a direct impact on RWA as well.

In the past, many people understood RWA as assets going on-chain, as if simply mapping bonds, stocks, fund shares, or unlisted company equity into a Token means RWA. This understanding is too superficial.

Real RWA is not about assets going on-chain, but about rights going on-chain.

The Token itself is meaningless; what matters is what rights it corresponds to behind the Token. Is it ownership, income rights, debt rights, redemption rights, subscription rights, conversion rights, or price exposure? Currently, many so-called RWA are merely re-packaging itself on-chain, and fundamentally still opaque structured products.

So for me, the future main line of financial assets going on-chain is not token first (tokens are limited), but rights first (rights are prioritized).

#Bitget has arrived—it’s VIP! Crypto, US stocks, CFD, the global opportunity is laid out in one stop

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。