Original Author: Sleepy

Yesterday I saw an article titled: "A New AI King is Born! Anthropic's Valuation Explodes to $1.2 Trillion, Surpassing OpenAI for the First Time."

This title understands the era too well; there's AI, there’s a comeback, a new king ascending, and a figure so large it exceeds people's imagination. It’s like a gong. Once it sounds, it’s hard not to look up.

How did this $1.2 trillion valuation come about? It actually stems from the on-chain Pre-IPO market.

The so-called on-chain Pre-IPO market doesn’t trade ordinary stocks that you can see in your brokerage account. It's more like a designed "risk exposure before a company's IPO." Some tokenize, create SPVs, or use synthetic structures to slice the expected future IPO of a private company into small pieces and facilitate trades on-chain. It opens a window for ordinary investors that was previously hard to access and provides the market with a real-time price. Anthropic was priced at $1.2 trillion in this market.

For the past two years, the feeling AI leaves for ordinary people often isn't "I’m part of a new era," but rather "the new era has passed me by." Nvidia has risen, cloud providers have risen, large model companies have gone through rounds of financing, but most of the core equity is locked up in private markets. We can see the ship but can't touch the ticket. Hence, any ticket that could possibly lead to companies like OpenAI or Anthropic would inherently have a filter.

But the more moments like this, the more we need to extract the numbers from the title, place them on the table, and see how they actually came about. Anthropic might be one of the AI companies worth serious research right now. But the issue is that a good company, a great era, and an aggressive price cannot automatically merge into one entity.

On the crypto trading platform Jupiter, Anthropic's Pre-IPO token had a daily trading volume of only $1.39 million, with only 329 traders in the past 24 hours. And it is this $1.39 million and 329 traders that reflect the illusion of a trillion-dollar valuation.

However, I don’t wish to discuss whether Anthropic is worth anything, nor the issue of whether trading Pre-IPO assets on-chain has problems. I want to clarify a more fundamental question first: What conditions must a price meet to be qualified as a "valuation"?

Proof of Birth for Prices

In February 2026, Anthropic completed its Series G financing. It raised $30 billion, with a valuation of $380 billion, led by Singapore’s sovereign fund GIC and hedge fund Coatue Management. A month later, OpenAI also announced it had completed its latest round of financing, raising $122 billion and achieving a valuation of $852 billion, with major investors including SoftBank, Microsoft, and other institutional investors.

How were these two sets of numbers generated?

Taking Anthropic's Series G financing as an example, GIC manages over $700 billion in sovereign wealth, while Coatue manages over $60 billion in global tech hedge funds. Each has a due diligence team with dozens of members that spent months analyzing Anthropic's technical architecture, revenue curves, customer retention rates, and competitive landscape. The final $30 billion investment came with a complete set of legally enforceable rights structures, including anti-dilution protection, priority in liquidation, information rights, and board observer seats. If Anthropic performs worse than expected or trends downward, these clauses ensure that GIC and Coatue can reclaim their principal first.

They are purchasing more than just a number; they are acquiring a complete set of legally enforceable rights.

What about the $1.2 trillion on Jupiter? Over 300 traders, more than a million dollars in daily trading volume, and no commitments or obligations from Anthropic behind the tokens. What you buy is not a small piece of ownership in the company, but merely a receipt for a bet on-chain.

The way these two prices are presented in the report titles is completely identical, both labeled as "valuation of XX billion."

In 1985, economist Albert Kyle published the classic paper "Continuous Auctions and Insider Trading," introducing the concept of "market depth," using λ to measure the degree of price impact by unit fund inflows. In a deep market, buying $100 million may only cause a 0.1% price fluctuation; while in a shallow market, $50,000 could cause a 20% price fluctuation. The larger λ is, the greater impact a single transaction has on price, and the thinner the consensus information carried by the price itself.

The situation for Anthropic on Jupiter is that a liquidity pool of $1 million supports an implied valuation of $1.2 trillion. The ratio of liquidity to valuation is approximately 1:1,200,000. If someone wanted to sell a position worth $10 million at a $1.2 trillion valuation in this market, the entire liquidity pool would be directly drained ten times. This price is non-executable; it only exists on paper and cannot be cashed out in the real world.

If it is only treated as a reference indicator, that is understandable. The problem is, it hasn’t been treated that way. It has become the evidence for "officially surpassing OpenAI," the title for "the birth of a new king globally," and the cognitive input for many readers.

This act of packaging the marginal price of a thin market into widespread consensus hasn’t just begun today. It has been happening for nearly four hundred years.

The Tavern in Haarlem

On February 3, 1637, Haarlem, Netherlands.

In a small tavern, about thirty people sit around a long table. According to the customs of Amsterdam and Haarlem at the time, these informal tulip auction gatherings were held several times a week, usually conducted in the tavern’s back hall. Participants were familiar local merchants and floral brokers.

The item being auctioned that day was a Semper Augustus bulb. Its red and white petals were considered a masterpiece of creation, with only a few known to exist in all of Holland. The bidding lasted all night, with a final sale price of 10,000 Dutch guilders.

In Amsterdam in 1637, a canal-side row house sold for about 5,000 guilders, and a skilled worker earned about 300 guilders annually. One bulb equated to two luxury homes, or 33 years of a craftsman’s salary.

And this price's birth came solely from thirty people, a closed space, and alcohol as a catalyst, without any external constraints, market maker obligations, or information disclosure requirements. Bidders raised each other's emotions and did not need to bear any obligations except for payments when bidding.

The next day, the transaction price was recorded in a booklet printed in Haarlem. The booklet was sent via postal routes to cities like Leiden, Rotterdam, and Utrecht. Farmers and small merchants who read it had no idea how this figure was generated; to them, the price in the printed material equated to the market price. Some began hoarding ordinary variety bulbs, believing the whole market would be buoyed up.

On February 6, at a tulip auction in Alkmaar, suddenly no one raised their bid. Next came Haarlem and Amsterdam, and within a day, buying activity across the Netherlands disappeared. Those who had hoarded bulbs at market prices found no one to buy them, causing prices to crash, dropping over 90% within a week.

Looking back, that "10,000 guilders" for the Semper Augustus was not a market judgment but a judgment from a room. Yet through the amplification of print, the room's judgment transformed into national cognition.

Eight-three years later, in 1720, London.

Shares in the South Sea Company rose from £128 at the beginning of the year to £1,050 in June. Founded in 1711, this trading company held a monopoly on British trade with South America, yet actual trading profits were very slim. The true driver behind the soaring stock price was a complex debt-for-equity scheme where the company proposed to take on national debt and convert it into company shares, then sustain the whole scheme by continuously pushing up the stock price.

Newton sold his shares in the South Sea Company at £300, profiting £7,000. But then the price continued to skyrocket. In July, Newton bought back in, this time at a high price. After the crash in the fall of that year, his total losses amounted to £20,000, equivalent to ten years’ salary as master of the Royal Mint.

Newton may not have considered how the figure he'd referenced, "£1,050," was generated.

In 1720, there were no electronic trading systems, no central counterparties for clearing. Buying and selling South Sea Company shares required physically going to the company office in London to process the transfer or doing so through brokers in several coffee houses on Exchange Alley. Daily actual transactions may have numbered only in the dozens to hundreds, with just around a hundred direct trading parties involved.

These prices were recorded by price lists at Jonathan's Coffee House. When newspapers reprinted these price lists, they did not annotate "Today, 12 transactions took place, with a total volume of approximately £8,000." Readers across England saw only "South Sea Company: £1,050" as one number.

When the panic selling began at the end of July, the price, generated by a limited game among several hundred people, was instantly breached. There were no market makers obliged to buy back, no circuit breakers, and no central bank intervention. By December, the stock price fell back to £124, nearly returning to the beginning of the year.

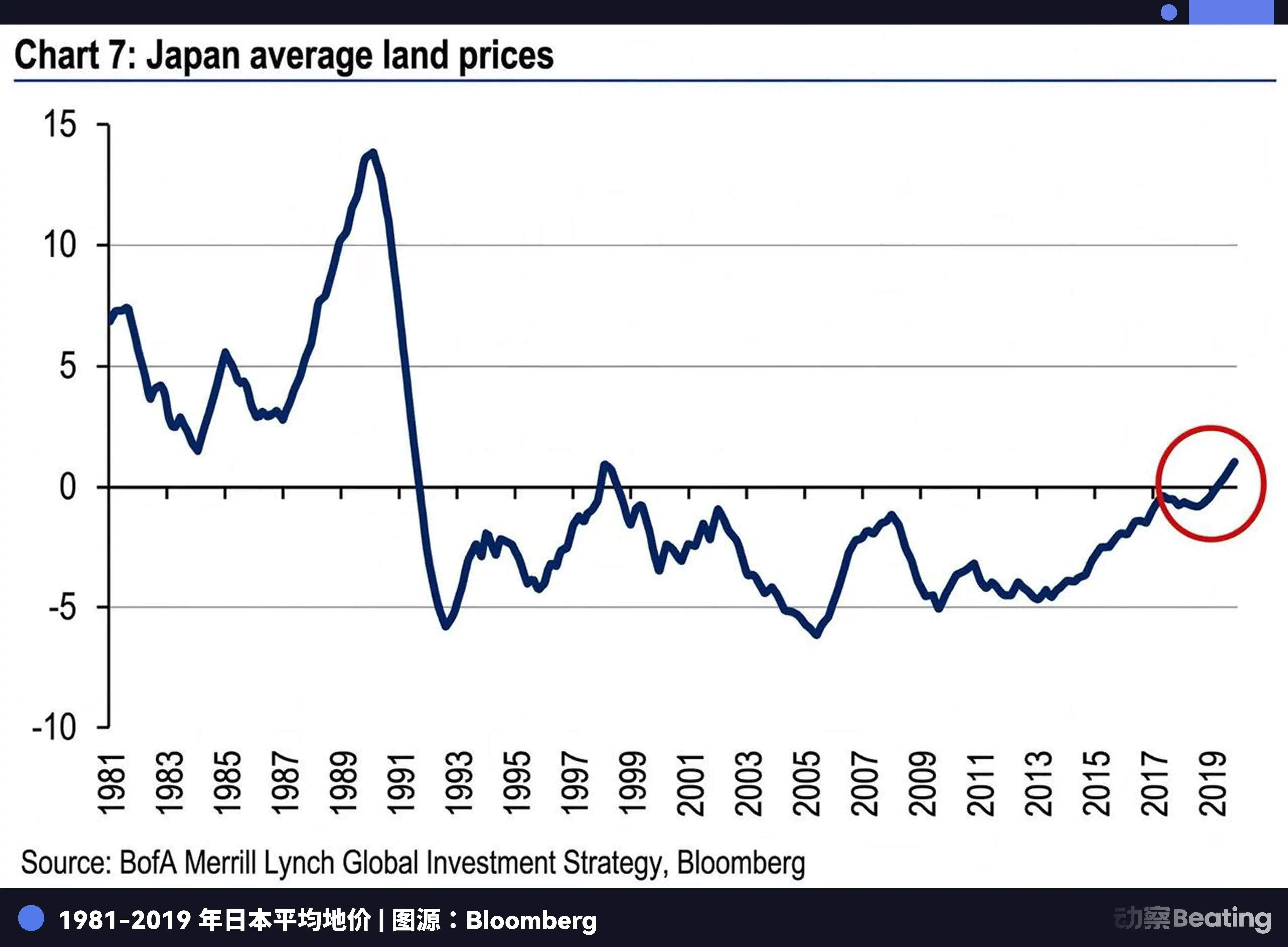

Jump forward another 260 years. In the late 1980s, Tokyo.

"The land beneath the Imperial Palace in Japan is worth more than the entire state of California." This statement was widely quoted by global media in 1989. At that time, the estimated total value of the 2.3 square kilometers of land where the palace is located, based on surrounding land prices, was approximately $850 billion, while the total assessed value of all land in California was about $500 billion. However, this estimate only referenced the prices of a few actual transactions in the Ginza and Marunouchi areas.

Japan's land market has a unique structural feature: extremely low liquidity. Japanese landowners regard real estate as family assets to be passed down through generations rather than traded for arbitrage. At the peak of the bubble in 1989, the annual number of land transactions in Tokyo's core commercial area was extremely limited. Occasionally, plots that entered the market were usually due to owner bankruptcy or family inheritance disputes, with a large number of well-funded buyers eager to establish positions competing for the scarce supply.

The prices produced under this extreme supply-demand imbalance were extrapolated by real estate evaluation agencies as the "fair value" of all the land in that area; their logic was that if this small piece of land was worth 20 million yen per square meter, every adjacent piece should also be worth that price.

In 1990, Japan's central bank began raising interest rates continuously, and banks tightened loan standards. When companies were forced to sell real estate to repay loans, the true test of liquidity began. Sell orders surged while buy orders dwindled. Actual settlement prices were 50% to 80% lower than the so-called market valuations.

The national land price index in Japan subsequently fell for a full 26 years, only beginning to gently rise again in 2016.

The tavern in Haarlem, the coffee house in London, the real estate evaluation firm in Tokyo, the Jupiter DEX on Solana. Four scenes spanning nearly four hundred years share the same narrative structure:

A few participants create an extreme price in an extremely thin market → The media spreads it as a widespread consensus → A larger public makes decisions based on it → When liquidity is truly tested, the price returns.

The media is evolving: booklets, newspapers, telegraphs, television, WeChat official accounts, but that core loophole has never been repaired; when prices are disseminated, their birth conditions are systematically omitted.

Why?

Complex Stories Always Compressed into a Well Disseminated Number

Business reporting has a natural dilemma: the real world is too complex, and the window for dissemination is too short.

What actually happens with a company often involves financing structure, product progress, revenue quality, competitive landscape, equity rights, exit paths, and market sentiment. But the headline is only a line, and the reader's attention lasts just a few seconds. Thus, expressions like "valuation surpasses ten billion," "market capitalization evaporates by a hundred billion," "unicorn born," "super platform rises" become an easily chosen compressed mode. It’s a narrow door that complex business information must go through when entering public discourse.

Writers are of course inside this door. We all know that explaining the conditions of a valuation's birth is far more challenging than writing an impactful headline. The former requires patience, length, and the reader's willingness to linger; the latter only requires a sufficiently bright number to instantly signal "there’s something going on here." If a headline were to read "Anthropic's On-chain Pre-IPO synthetic assets at marginal prices in a low trading volume market, extrapolated to an implied valuation of $1.2 trillion," it may be more accurate but could lose its ability to disseminate before reaching the reader.

If it reads "A New AI King is Born," it’s a different story. It has drama, competition, thrones, and a human love for the power transition. Dissemination is not just the transporting of facts; it’s more like a juicer. Facts are thrown in, and what comes out is emotion.

The second reason is the market structure. The Chinese business information environment lacks a key role: short sellers.

In the US capital markets, a high price divorced from the fundamentals won’t last long. Research firms like Muddy Waters and Citron identify targets where prices far exceed levels supportable by liquidity or fundamentals, then publicly release reports while shorting to profit.

They have a strong economic incentive to demonstrate the birth conditions of a number to the public. Muddy Waters' report shorting Luckin Coffee lasted 89 pages, using 92 full-time and 1,418 part-time investigators, recording over 11,000 hours of store footage across 981 locations, cross-referencing 25,843 receipts. All of this was to prove one thing: that the number of daily sales per store reported by Luckin was false, with the actual figure being roughly half of the claimed number.

This level of confrontational research requires two prerequisites. First, mechanisms to profit from "price return" must exist; second, legal protections should allow short reports to be shielded from suppression. Both conditions are present in the US stock market but virtually nonexistent in the Chinese A-share market and primary market.

The result is that no one can earn money by questioning valuations, and thus there’s no motivation to pursue the conditions under which that price was generated.

Short sellers are not destroyers. They are correction mechanisms in the pricing system. The removal of such correction mechanisms results in price deviations that can continue to expand without any resistance until one day they collapse under their own weight. And every day before that collapse, the market appears normal.

The consequence of these two forces overlapping is that there are plenty of examples in Chinese business history.

In June 2015, LeEco's stock price on the Shenzhen Stock Exchange hit a peak, with a market capitalization of about 170 billion yuan. Jia Yueting depicted the LeEco ecosystem, spanning mobile phones, televisions, cars, sports, and films, with a concept of seven sub-ecosystems' chemical reactions leading investors to believe these businesses' synergistic effects should be priced not by division but by the exponential growth of the entire ecosystem.

No one questioned what amount of capital was at play to reach this 170 billion market capitalization. LeEco's average daily trading volume in 2015 was indeed not low, but over 70% of its shares were locked, and the actual circulating stock was much smaller than the scale implied by the total market capitalization. Those retail investors and small institutions capable of trading inflated the price based on limited circulation, and that price was automatically multiplied by total shares to yield the "170 billion."

A large number was produced → Entered the leaderboard → Provided a sense of certainty → No one had the motivation or capability to question → An even larger number was produced.

In this light, Anthropic's "$1.2 trillion" is not surprising; it’s merely a byproduct of the system operating normally.

Anxiety, Anxiety

Let’s read that $1.2 trillion from another angle.

What kind of people would, in a market with a liquidity pool of only over a hundred million dollars, purchase a synthetic token without legal protections at an implied valuation three times higher than the latest institutional round?

The answer is those whose FOMO is so strong they are willing to pay an anxiety premium for it.

When Anthropic's Series G financing closed in February 2026, the valuation was $380 billion. Two months later, the implied valuation of tokens on Jupiter was already more than triple that number.

Is this 3x premium due to an information advantage? Do traders on Jupiter understand Anthropic's business better than GIC's due diligence team? Obviously not. This premium isn’t about a cognition gap but rather serves as a form of psychological insurance against the fear of "missing out."

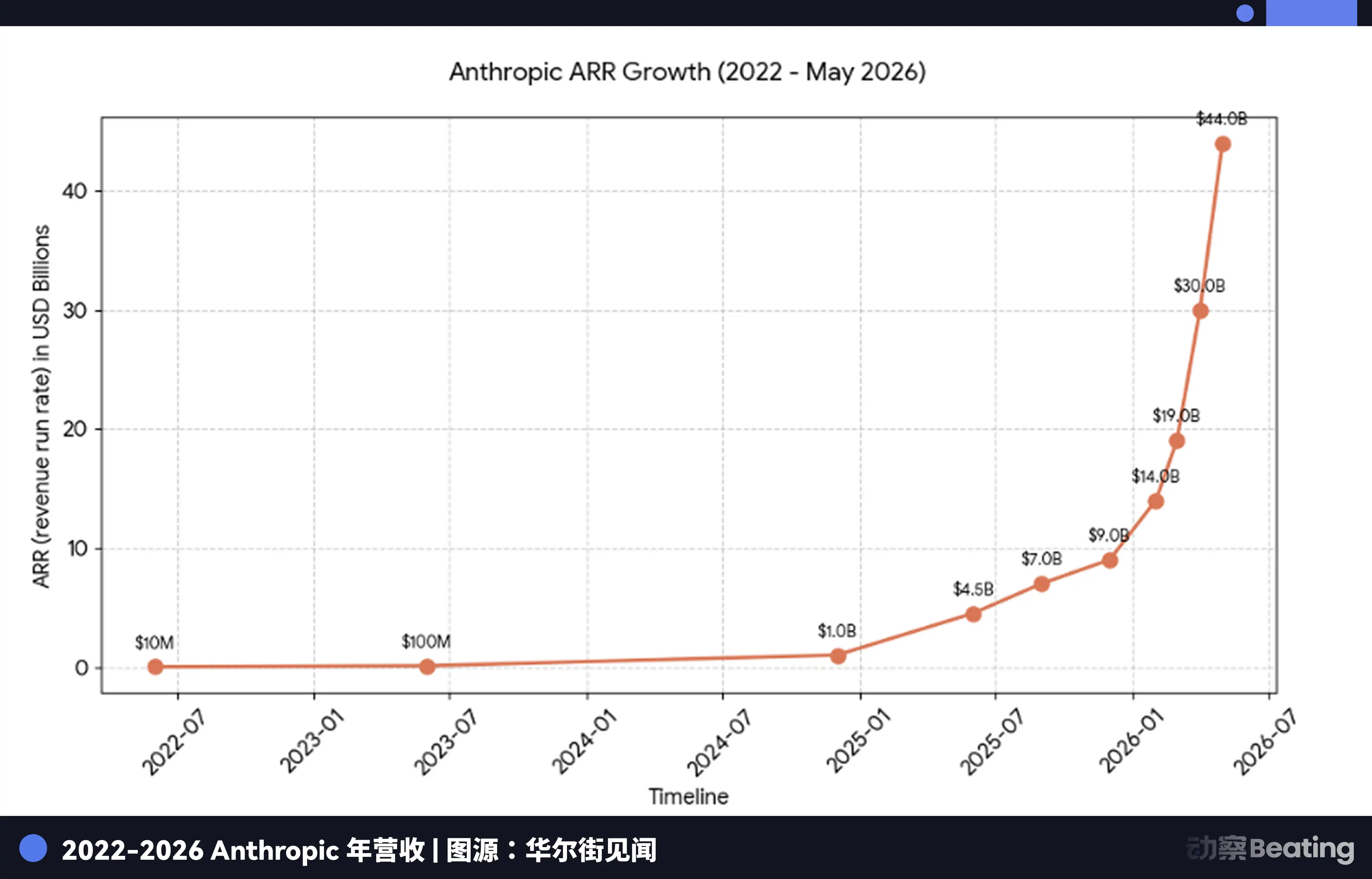

If you are someone active in the cryptocurrency space from 2025 to 2026, what do you witness? Anthropic's annual revenue skyrockets from $9 billion at the end of 2025 to $30 billion by May 2026, tripling in three months—a growth rate and amount that eclipses the vast majority of Crypto projects. Claude Code's penetration into the developer community has broken all expectations. Yet, the daily active users of most blockchain applications linger in the thousands to tens of thousands.

Fear of missing out spreads in the crypto community. Are we standing on a sinking ship, with AI being the truly new land of the decade?

The Pre-IPO tokens on Jupiter provide an entry point; no VC identity is needed, no relationship networks required, and no million-dollar thresholds. With just a few thousand dollars, one can have on-chain exposure to Anthropic.

Buyers from different channels experience different anxieties.

On-chain token buyers are mostly crypto natives. Their anxiety stems from the fear that AI may be replacing Crypto as the genuinely disruptive force of this era, leaving them trapped in an old narrative.

OTC buyers are often traditional primary market participants and family offices. Their anxiety arises from their trading flows not being cutting edge and being excluded from the hottest targets. According to a Reuters report on April 14, Anthropic has already received interest from multiple VCs willing to invest at an $800 billion valuation, while TechCrunch stated on April 29 that the next round could finance $50 billion at a $900 billion valuation. The panic intensifies when you can't even secure a share allocation.

Buyers on second-hand equity platforms are often high-net-worth retail investors in the US. Their concern is that during every tech giant IPO, retail is always the last to board the train, as the price increase by the time of listing is entirely consumed by VCs and employees.

Yet, these people share a commonality; they know very well the premium is extremely high and the exit is difficult, yet they still buy in, because the psychological cost of "missing out" outweighs the economic cost of "getting stuck."

Behavioral economics suggests that the pain felt from losses is about 2.5 times the pleasure felt from equivalent gains. Yet, FOMO runs deeper than loss aversion. Loss is a one-time pain while FOMO is a continuous agony. Humans tend to end the former to alleviate the latter.

So, that $1.2 trillion figure is most accurately interpreted as: there exists a group, about 3,546 addresses and 298 daily active traders, whose anxiety level is strong enough to pay a premium based on an implied valuation three times that of a top sovereign fund in a market with a liquidity pool merely over a hundred million dollars to establish risk exposure.

This is valuable information in itself. It cannot tell you how much Anthropic is worth, but it precisely measures the temperature of a certain group.

Beyond Price

In thin markets, prices create narratives, narratives attract followers, and purchases from followers temporarily validate prices. The cycle continues until the number of followers and available funds become insufficient to maintain that price.

Participants each have their own decision-making logic. But there may be many ordinary readers who merely read an article and, unknowingly, internalize the outcome of a simple game of over three hundred participants as their perception of the world.

A $30 billion game produces a $380 billion valuation that rests behind GIC and Coatue’s collective pricing, wagering the reputation of sovereign funds and top hedge funds. A $1.2 trillion valuation supported by a daily trading volume of just $1 million is backed by the marginal behavior of over three hundred addresses in an unregulated market.

From the tavern in Haarlem in 1637 to the DEX on Solana in 2026, humanity has invented countless forms of markets, media channels, and financial instruments. Yet one problem persists, unresolved for nearly four hundred years: how can the conditions for a price's birth, meaning how many people, with how much money, under what constraints it was generated, become an indispensable part of its dissemination?

Perhaps this problem cannot be solved. But at the very least, it should be known.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。