Original author: Ada, Deep Tide TechFlow

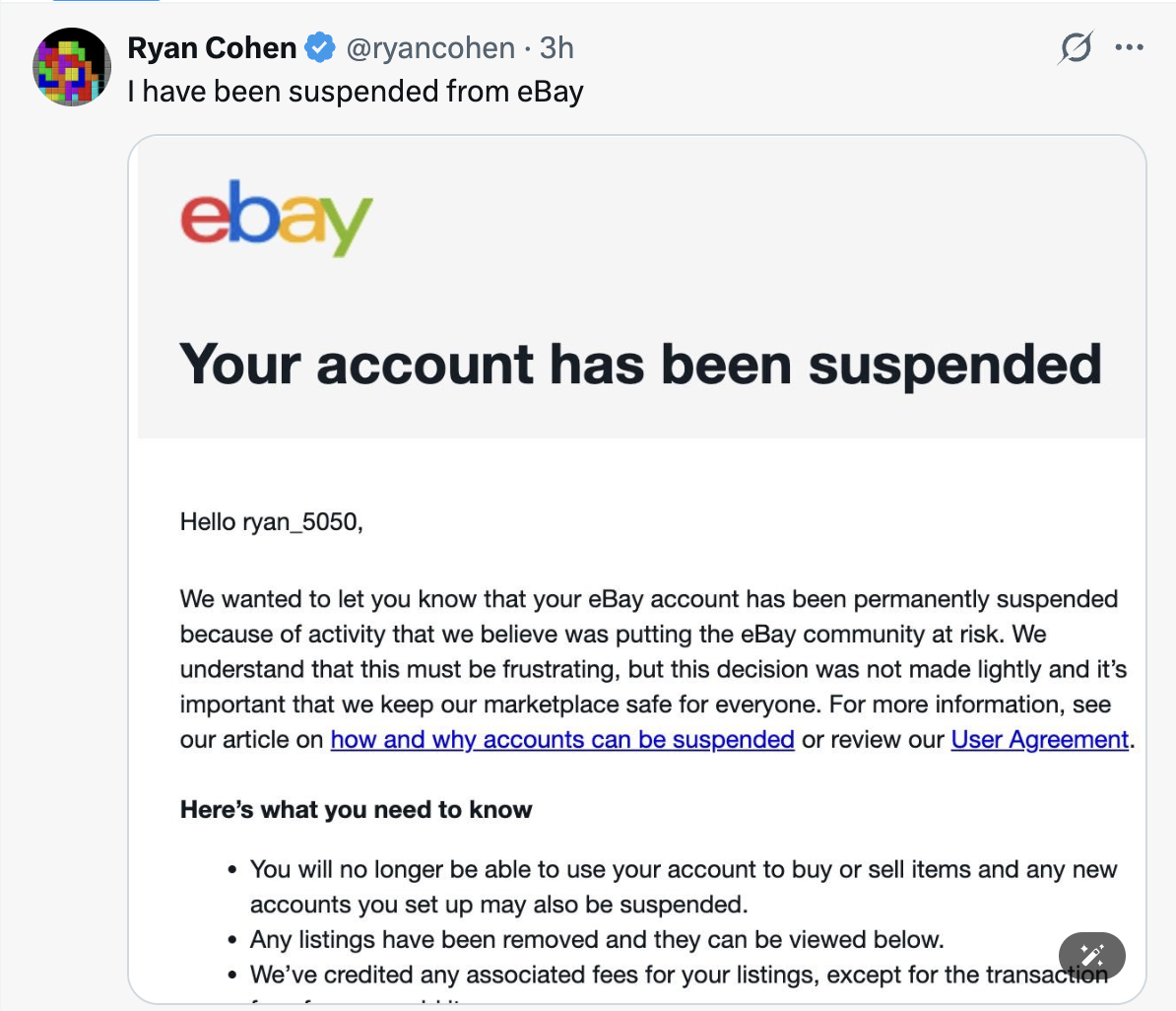

In the early morning of May 7, GameStop CEO Ryan Cohen posted a screenshot on X.

eBay notified him that his account has been permanently suspended, stating, “We believe this activity poses a risk to the eBay community.”

Just 24 hours earlier, he had listed a pair of socks on his personal eBay account with the caption: Selling things on eBay to raise money to buy eBay.

It sounds like a joke, but he is serious. Just three days prior, he had thrown a $56 billion acquisition offer to the eBay board.

A Flimsy Offer

On May 4, GameStop announced a non-binding acquisition proposal for eBay at $125 per share.

GameStop stated in its announcement that the acquisition offer would be paid half in cash and half in GameStop common stock, representing a 20% premium over eBay's closing price of $104.07 on Friday, and a 46% premium over the closing price on February 4 (when this gaming retail giant began acquiring shares in the company).

On Monday, eBay's stock price rose about 5% to around $109, significantly below GameStop's $125 acquisition offer. Meanwhile, GameStop's stock price fell about 10%, indicating skepticism among investors regarding the completion of this deal.

GameStop currently has a market capitalization of about $11.2 billion, only a small fraction of the $56 billion transaction size. Although the company has received a $20 billion financing intention letter from TD Bank, the funding gap remains significant.

What next? Cohen answered on CNBC's camera: “We offer a plan of half cash and half stock, and we have the ability to issue more stock to complete this transaction.”

In other words, it's about printing stock. Using shares from a company with a market value of $11.2 billion to acquire equity in a company valued at $55.5 billion. For eBay shareholders to accept GameStop stock as consideration, it seems that GameStop's stock price would need to rise five times first.

So how does the market view this?

Kalshi traders believe that the probability of GameStop completing the acquisition by 2026 is only 26%, although the total trading volume of the new contract is very low, just slightly above $2,000.

On the Polymarket platform, traders are even more pessimistic. Traders on that platform believe that the chance of GameStop completing the acquisition is only 15%.

Semafor cited informed sources reporting that eBay's board met this week to review the proposal, but this deal “seems to be stillborn,” as Cohen failed to persuade any major shareholder to publicly support him.

A Carefully Designed Performance

On May 6, 48 hours after the offer was submitted, Cohen began listing items on his personal eBay account, including socks, miscellaneous items, and personal belongings, with total auction bids reaching tens of thousands of dollars.

He also aggressively attacked the eBay board on Twitter, accusing them of mismanagement. On that day, he first received a notification from eBay that he had reached the monthly listing limit. Then his account was suspended.

The suspension notice stating “poses a risk to the eBay community,” paired with a person trying to acquire eBay, is incredibly absurd.

But this is just Cohen's performance. Since the bid could not scare the board, he decided to use noise to activate GME retail investors. Let the stock price rise first, and then there will be stock as consideration.

Why did Cohen initiate the acquisition?

There is a background here. In early 2026, GameStop's board adjusted Cohen's compensation plan, allowing him to receive up to $35 billion in stock incentives if the company's market value reaches $100 billion. However, with GameStop's current market value at only about $11.2 billion, achieving $100 billion through selling game discs is nearly impossible, so the company must grow its market value through acquisitions.

Cohen's “selling socks to acquire eBay” script was never meant for the board, but for the retail investors in the WSB section on Reddit.

From Bitcoin to eBay

Zooming out, you will find that from Bitcoin to eBay, Cohen's narrative has always been the same.

In February 2025, he flew to meet Saylor. Three months later, he announced his entry. According to Reuters, GameStop spent $513 million to buy 4,710 Bitcoin at an average cost of about $108,917.

While Saylor leveraged the entire balance sheet of Strategy and issued bonds weekly to buy, Cohen stopped after buying $500 million, which only accounted for 10.4% of GameStop's cash reserves at that time. Strategy increased its holdings almost weekly, but GameStop’s Bitcoin holdings did not increase at all.

Until around January 23, 2026, GameStop transferred all 4,710 Bitcoins to Coinbase Prime, preparing to liquidate.

After the Bitcoin transfer, Cohen gave interviews to several foreign media, where he discussed acquisition plans and vowed to make GameStop an investment holding platform “similar to Berkshire Hathaway.” When reporters pressed him about the Bitcoin strategy, he threw out that oft-quoted line: “This strategy is more attractive than Bitcoin.”

What is this “more attractive strategy”? It seems to be the $56 billion acquisition of eBay.

The logical chain closes here: first, use Bitcoin narrative to drive up stock price and attention, when book losses appear, turn around, then shift to the next grand narrative of acquiring a holding platform and creating a Berkshire-like $100 billion empire. Each story is bigger than the last, but none of them truly land.

Saylor represents belief, but Cohen is the true performer. He doesn’t need a trading closure, just a narrative closure is enough. Once the Bitcoin narrative is finished, he'll move on to eBay. Once eBay is finished, what will the next be? No one knows, but there will definitely be a next.

Why eBay?

eBay has stable cash flow, stable GMV, and stable shareholder returns. It is targeted for annual revenue of $31 billion, and as long as the merged company maintains eBay's valuation multiples, its market value could potentially break the threshold.

So what does Cohen want?

One explanation is: he needs a story bigger than Bitcoin.

GameStop's core problem has never been a lack of cash; the $9.4 billion cash reserve on its books is real ammo. However, as a gaming retailer that started with physical stores, physical games, and second-hand transactions, GameStop's traditional business has long been eroded by digital downloads, self-operated stores by platform operators, and subscription services, which can no longer support an $11.2 billion market value.

Retail investors buy into Cohen, into memes, into the possibility of “the next Berkshire.”

But possibility requires constant nourishment.

The Bitcoin treasury can hold out for a while. Once the flywheel turns in reverse, it needs something more stimulating. Acquiring a publicly traded company worth five times itself is a story stimulating enough.

As for whether the transaction can succeed? It doesn't matter.

What matters is that after this offer is submitted, CNBC will invite him on the show, The Wall Street Journal will write an exclusive interview, and Reddit will boil again, with GME's stock price experiencing several days of dramatic fluctuations. In the volatility, option bulls can make money, retail investors can have the illusion of “we won again,” and Cohen himself can cash out some stock incentives.

Listing socks and getting suspended can bring a wave of free traffic.

When Performance Art Meets Capital Markets

It is important to note that Cohen is a serial entrepreneur with a real track record; he sold Chewy for $3.35 billion to PetSmart. He knows that eBay's board would never sell the company to a competitor with a market value only one-fifth of its own; the $56 billion acquisition is very unlikely to succeed. He knows that TD Bank's $20 billion is insufficient, and stock dilution through issuing shares would be directly rejected by eBay's shareholders.

But he doesn’t care; he just needs to perform.

And the true audience for this performance is liquidity, the attention economy itself. In this era where all assets are priced based on narratives, whoever can generate the loudest noise can gain the most liquidity in the short term.

Listing socks and getting suspended is a hundred times more effective than issuing a proper press release. Overnight, all financial media are writing about Cohen, and all social platforms are sharing that suspension screenshot. The free global exposure is worth far more than the transaction volume of the items listed.

In today’s capital markets, the line between performance art and investment actions has become blurry. In the past, proposals were made for genuine acquisitions; now proposals are made to induce stock price volatility. Volatility brings profits, and profits are the exit strategy. Cohen and his team play this game best.

Cohen will never truly bet, always preparing for the next performance. But one point can be clearly seen now. When a CEO of a publicly traded company has to rely on listing socks on eBay to prove his seriousness about acquiring eBay, and then is permanently banned by eBay on the grounds of “posing a risk to the community,” this itself is the most precise footnote on the capital market of this era.

When the tide goes out, the fastest to run are always those fleeting trend-followers, while the true believers may also disdain the performance.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。