Author: Vaidik Mandloi

Introduction:

At this moment, in a corner of Crypto Twitter, a trader is intently watching the candlestick chart on the screen. The weekly increase of the token before him has reached 1400%. The classic pump-and-dump script is unfolding again, but the project itself has almost no real user base. Most circulating chips are concentrated in a few dormant wallet addresses that have never moved. He recognized this familiar pattern at a glance and foresaw the impending outcome.

Thus, he made the move that any rational trader would choose. He opened a short position. He bet that the price was about to crash and then went to sleep peacefully. When he woke up the next day, his position had been forcibly liquidated.

The key is: his judgment was not wrong. That pump was indeed a false prosperity. What he did not know was what kind of force he was betting against.

This is not a fictional plot but a real case that occurred in September 2025 with the $MYX token. In just one week, the price of this token skyrocketed from $1.30 to $18.42. During this time, the project team released no major announcements, and there were no substantial updates to the product. There were no new users entering the market, nor was there any increase in on-chain activity. The traders attempting to unravel the false surge and choose to short ultimately lost a total of $89.51 million.

Such tokens are what the industry refers to as "criminal tokens." The project team locks up a majority of the circulating chips for a long time and colludes with specific trading institutions to manipulate price movements. They carefully set up liquidity traps to hunt down any investors attempting to participate in the long-short game. This article will deeply analyze the structural logic of such manipulations, further revealing the pattern of chip control ownership and dissecting the deep-rooted reasons behind the industry's long-standing regulatory absence.

Manipulation Structure

Every criminal token scam begins with a secret agreement signed by both parties.

One party is the project team that dominates the issuance of the token. The other party is the so-called "market maker." These institutions are essentially trading companies that provide bidirectional quotes to exchanges, and their function is to maintain the token's liquidity. This market-making mechanism is a common industry practice. The real trick lies in the wording of the contract clauses.

The profit-sharing framework usually adopts a 70/30 ratio. This means that for every $1 in trading profit that the token generates, 70 cents go to the market maker, and 30 cents go to the project team. The current situation is that this contract's role is not limited to capital distribution patterns. The written terms also clearly stipulate that the market maker is responsible for "price management" after the token goes live.

This practice is referred to as price guidance in the industry. Its essence is that after receiving fees, the market maker pushes the price in any direction according to both parties' wishes during that week. Reports indicate that in MYX and thousands of token projects using the same operational template, the payment scale of such arrangements exceeds $30 million per cycle.

More importantly, the current state of token acquisition is such that market makers do not obtain tokens through purchase but always borrow them in a lending form.

This arrangement, known as the lending-option model, is the standard paradigm under which market makers collaborate with the project team on paper. At issuance, the project team typically lends the market maker a large number of tokens worth tens of millions of dollars. Theoretically, the market maker has a 12-month period to either return the tokens or buy them back at a preset high price. This is stipulated in the document. However, the actual situation is often quite different. Market makers sell the borrowed tokens as soon as they are loaned out, flooding the market with supply and causing prices to plummet. After the price drops, they buy back tokens at a low price to return to the project team, profiting from the price difference.

Fraudulent token projects also use the lending-option model, with the only variant being the addition of a second source of income to this framework. In addition to selling borrowed tokens, the operators have figured out how to extract profits from retail traders who notice the manipulation and attempt to short the crash.

From a technical standpoint, the effective functioning of this model requires the team and market makers to have nearly complete control over token supply. In most of the fraudulent token issuance patterns, they indeed possess this control. Typically, more than 90% of the tokens are concentrated in wallets that can be traced back to the same operators. On block explorers, these wallets appear as a long list of unrelated addresses, creating the illusion of a broad holder base. However, on-chain analysis nearly always reveals that these addresses are actually controlled by the same group of people, deliberately dispersed to disguise themselves as natural holdings.

In the MYX case, the concentration of holdings was extremely high. At the price peak, only about 20% of the supply was controlled outside the team and its allies. The remaining 80% is stored in two types of addresses. Part of it is locked in custody contracts, meaning that these tokens have yet to meet circulation conditions. The rest is stored in the wallets of core contributors and early investors, who may have the conditions to sell but choose to hold. In any case, these tokens do not enter market circulation.

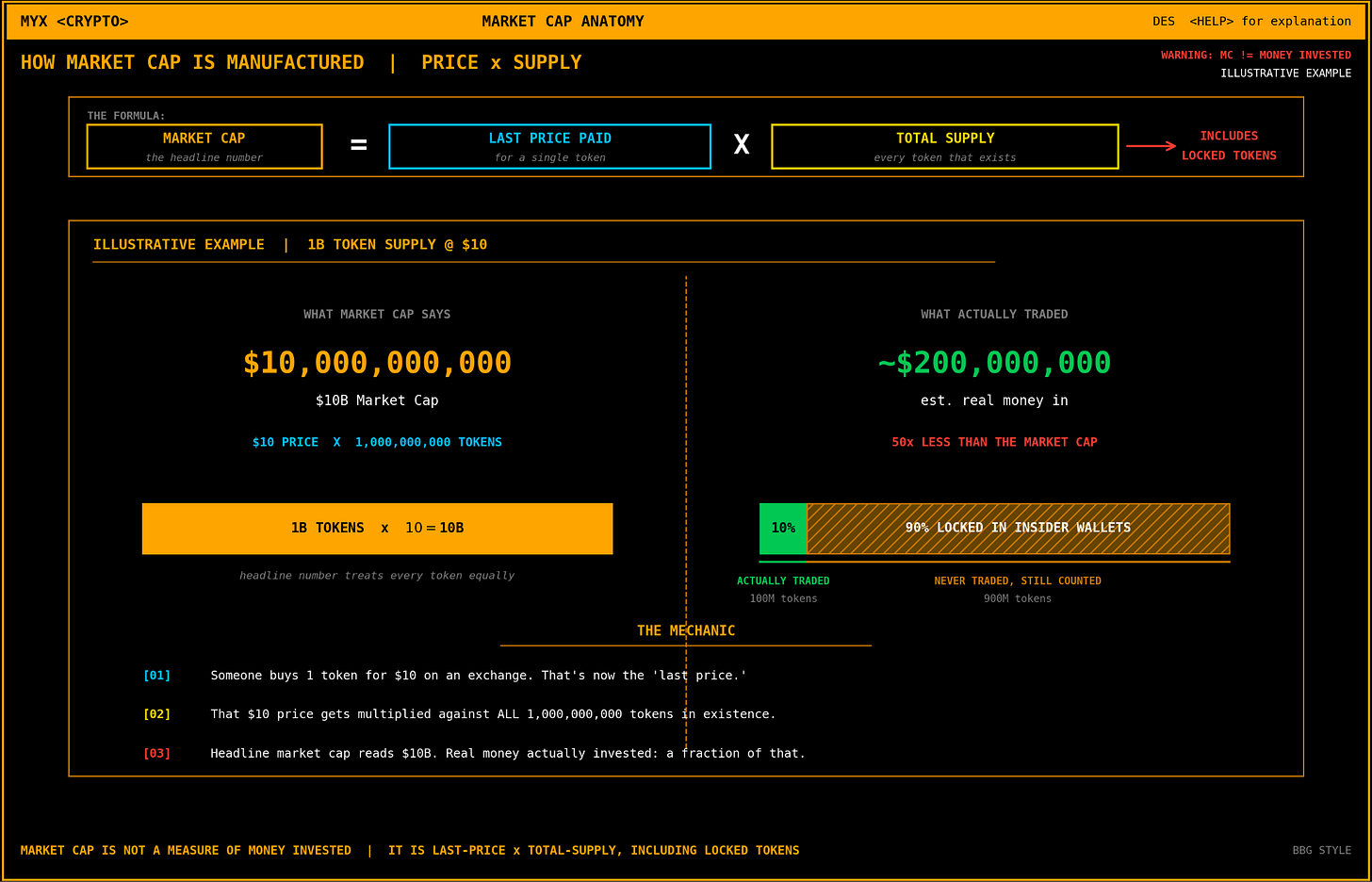

Usually, this is the essential difference between fully diluted valuation (FDV) and market capitalization (MC) of a token. Fully diluted valuation calculates the total number of all tokens that may exist in the future. Market capitalization only counts the tokens currently in circulation. However, in fraudulent token projects, even this distinction loses meaning, as the supply regarded as circulating is, in fact, also not freely tradable.

This is precisely why MYX's market capitalization was able to surge from $200 million to $3.35 billion within a week, without any new user registrations and without any new funds entering the protocol. In fact, the small number of MYX tokens circulating on exchanges was pricing those who had not participated in trading.

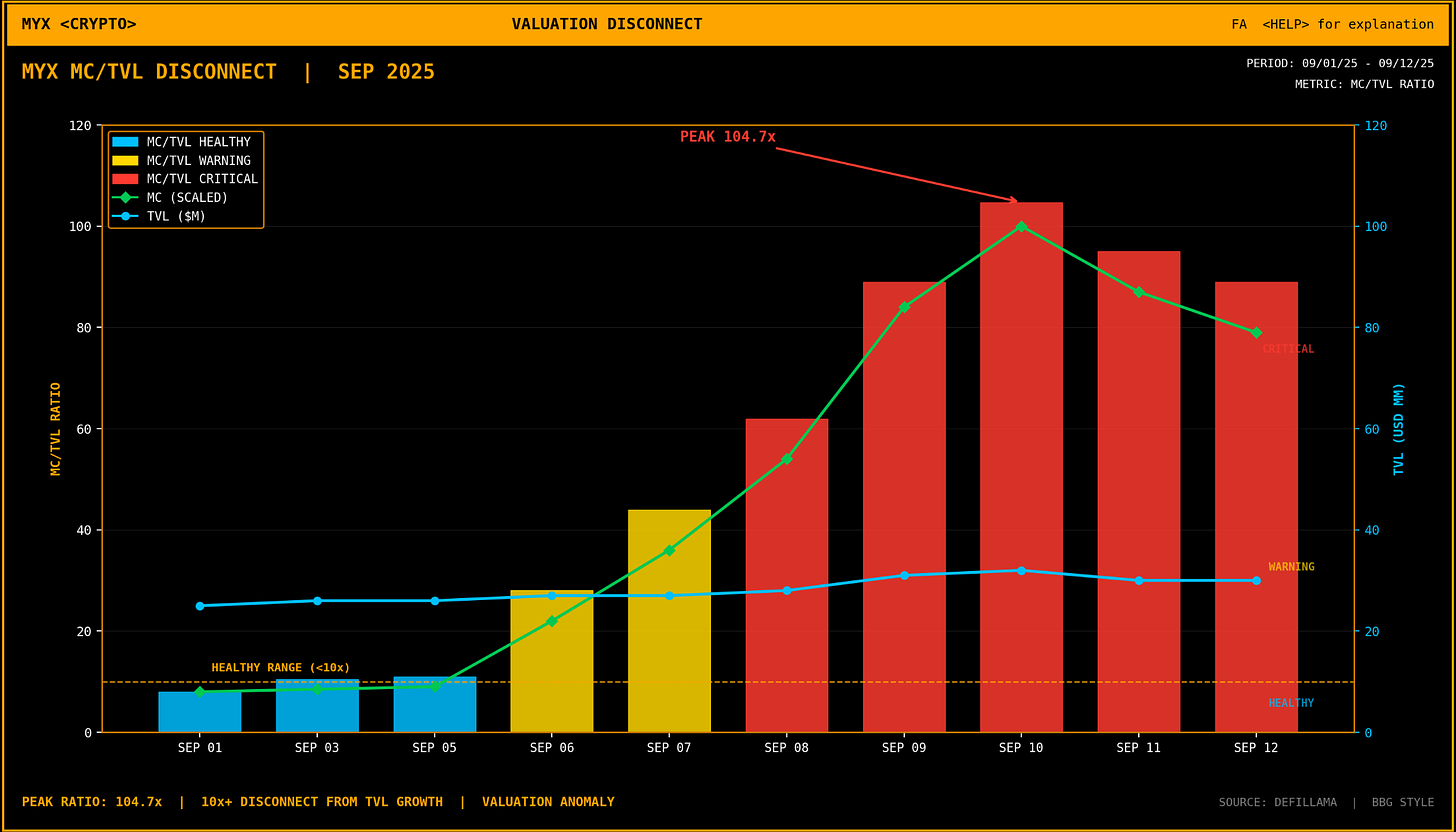

Anyone reviewing the data can clearly perceive the vast gap between MYX's price and its actual business fundamentals. There is a standard DeFi metric in the industry called TVL (total value locked). This refers to the total amount of funds users have deposited into the protocol to use the product. During the week when the market cap surged to $3.35 billion, MYX's TVL remained consistently within the range of $25 million to $32 million. The market cap to TVL ratio was approximately 100. Even for leading DeFi protocols like Uniswap and Aave, this ratio is only between 1 and 4. Deeper examinations reveal that MYX's annual revenue as a business entity is only about $5 million, yet the market gives it a valuation of $17.7 billion. This results in a sales multiple of approximately 3,500 times.

As early as before MYX entered the public eye and became a market hotspot, these layouts had quietly begun. Months before the price surge, the manipulation team had already established wash trading on several exchanges, including PancakeSwap, Bitget, and Binance.

The so-called wash trading means the same trading party acts as both buyer and seller, essentially buying and selling to fabricate high trading volume. Since leading exchanges highly rely on trading volume indicators when selecting and promoting tokens, once a token creates a volume bubble on a single platform, it can often smoothly land on the next exchange. Investigators tracing MYX's trading history found that dozens of small buy orders spread across different exchanges ultimately converged to the same centralized wallet. The operators elevated market demand through a large number of small wash trades with themselves to create an illusion of market activity.

The Four Phases of the Harvesting Scheme

The entire manipulation typically progresses in four phases, with each step targeting the typical trading psychology of retail investors.

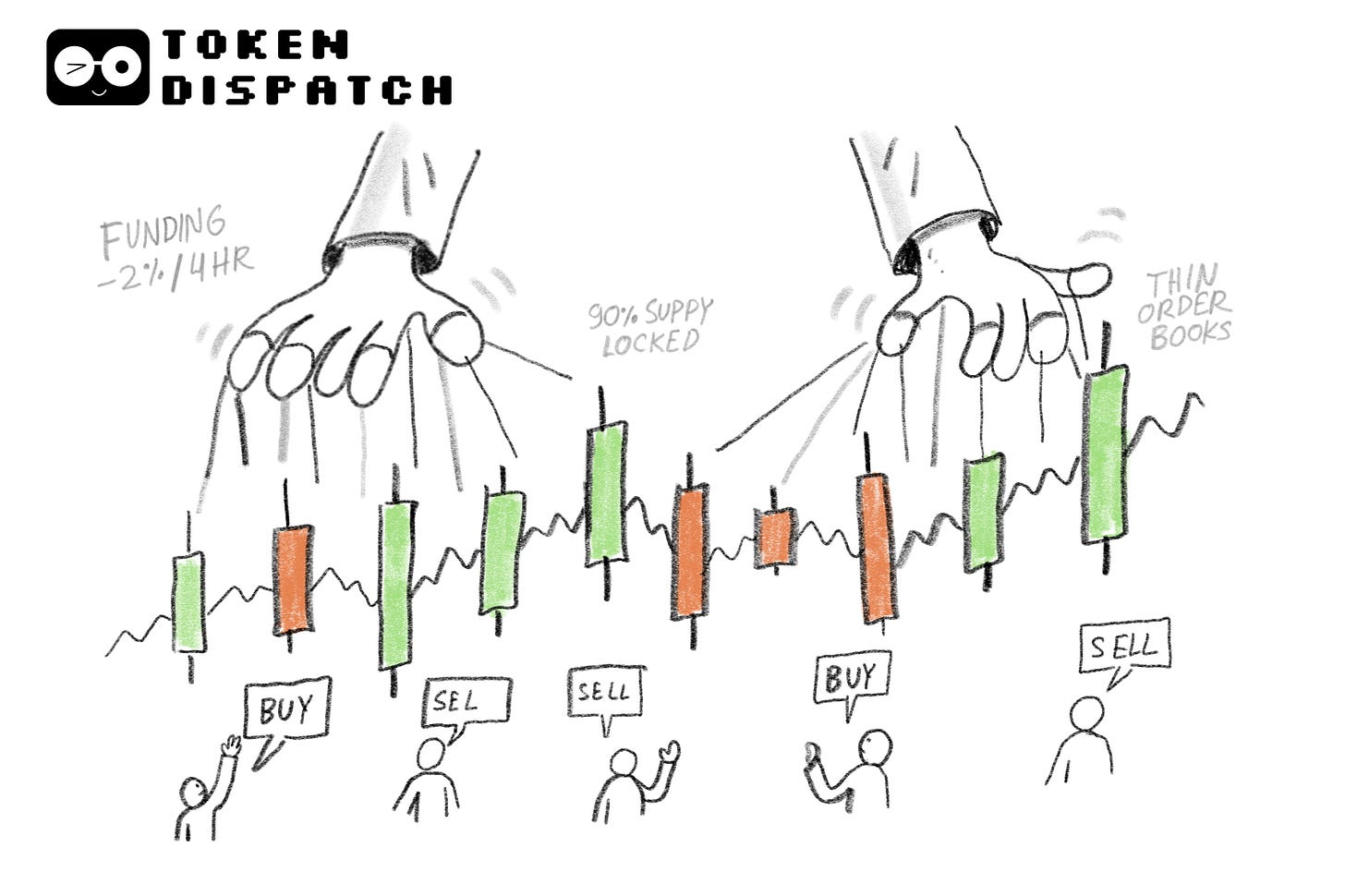

Phase 1: Trapping Shorts. Market makers start to raise the token price, while the actual trading volume remains extremely limited. This operation is very easy to achieve because most circulating chips are locked, and the order book depth of secondary exchanges like Bitget and Gate is inherently insufficient. In a state of liquidity scarcity, a small amount of capital can easily trigger a 5% to 10% price fluctuation. For example, in the case of RAVE, another type of criminal token, even though the price has been significantly raised and daily trading volume reaches billions, only $172,000 of unilateral funds is needed on Gate to push the price up by 1%. The cost to raise the price by 10% is less than $2 million.

The initial price increase is not intended to earn long profits, but the operators are actually coveting the capital from short positions. The core goal of phase one is to create the illusion that the price surge cannot be sustained, thus enticing skeptical traders to enter and short.

This seems counterintuitive; however, the more obvious the traces of manipulation are, the more beneficial it is for the operators to position themselves. Legitimate market makers seek a naturally smooth price trend. In contrast, criminal token operators deliberately expose signs of artificial manipulation, which is key to attracting shorts.

Phase 2: Setting the Trap. Once a significant amount of short capital flows in, the operators begin to close part of the long positions used to pump the price while simultaneously unwinding some hedging positions and deliberately creating a significant correction, coupled with a sharp shrinkage of open contracts. The price drop, accompanied by a reduction in open interest, technically resembles a local top formation. This makes traders who are still on the sidelines believe that the price surge has ended, prompting them to short during the pullback.

Phase 3: Squeeze Rally. At this point, short traders begin to face substantial losses. Most trading in criminal tokens is not spot trading but is completed via perpetual contracts. To maintain long-short balance, the exchange charges a funding fee. Every few hours, traders holding positions need to pay fees to their counterparts. The paying direction depends on the premium or discount of the perpetual contract price relative to the spot price. If the perpetual contract is at a premium, longs pay shorts; if at a discount, shorts pay longs. In a normal market environment, this rate is about a fraction of a percent per day.

However, in the ongoing squeeze in the criminal token market, the short funding rate can soar to -2% every 4 hours. Converted, this means deducting 12% from the margin per day just to maintain the short position. Holding a position for a week, before the token price establishes a clear direction, 84% of the principal has been depleted due to funding fees.

Besides the funding rate, leverage is also a key variable. In the criminal token market, short positions are generally opened with high leverage of 20x, 50x, or even 125x. With 50x leverage, a 2% adverse price movement can trigger liquidation, forcing the position to zero out.

When short positions face mass forced liquidation, the domino effect immediately manifests. Each round of liquidations is accompanied by mandatory buy-ins, pushing prices higher. Price increases further harm higher short positions, resulting in a chain reaction of liquidations. Traders who accurately identify fake breakout signals ultimately become the largest source of buying pressure, propelling the market higher.

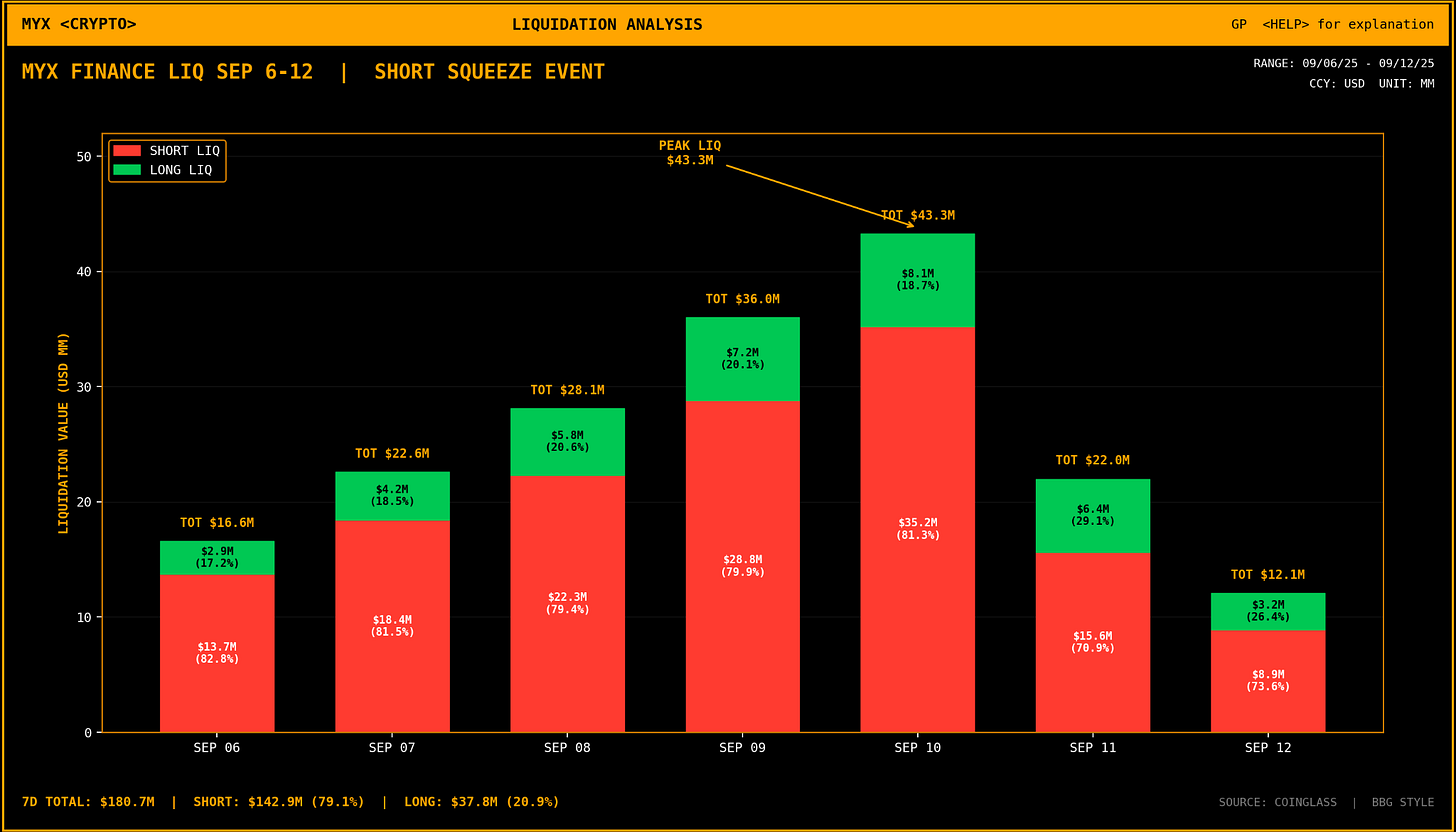

The situation of MYX exemplified this extreme development perfectly. On September 8, 2025, the amount of liquidation for that token reached $16.53 million in a single day, of which $13.68 million was attributed to shorts. As a reference, the total open interest for MYX that day was about $262 million. This means that over 6% of the leveraged positions for that token were liquidated within 24 hours, and almost all liquidations came from shorts. During the entire price surge, the total amount of short liquidations reached $89.51 million, while long liquidations were only $23.45 million. The long to short liquidation ratio was approximately 4:1.

In phase 4, the distribution pattern enters. Once the short positions have been cleared and the price peaks, the operators will reverse their positions. They not only establish short positions and close out previous long positions but also begin transferring locked tokens to centralized exchanges. This is where seasoned on-chain traders are most susceptible to traps. When tokens flow from known operator wallets to exchanges, the market generally interprets this as impending selling pressure, making shorting appear to be a rational choice. However, such deposits are often deceptive. During the operation cycle of criminal tokens, this is often used as an empty trap, with the real distribution not yet initiated.

The foundation upon which this manipulation structure stands is the extreme scarcity of counterparties. A healthy market should gather diverse participants with different beliefs, time horizons, and information advantages. However, the criminal token market is not like this. Whether going long or short, the counterparty in every transaction is essentially the same operator who is performing according to a predetermined script.

The controller of circulating chips is the dominator of the market.

The operational logic of criminal tokens can all be traced back to the same source. The project team and its affiliates almost monopolize all circulating chips. It is this high level of control that allows the operators to manipulate both spot and contract markets simultaneously on the same token. It is this high degree of control that allows them to navigate the pace of price increases accurately. It is also this level of control that enables them to initiate squeeze rallies at opportune moments. No other force in the market holds enough chips to counter them.

The current state of MYX illustrates this: open interest surpasses market capitalization, two-thirds of trading volume is concentrated on Bitget, and the short funding rate has remained at punitive high levels for several days. Traders attempting to go against the trend in shorting this rally, while accurately identifying technical signals of false buy pressures, have failed to realize that this is, in fact, a meticulously designed manipulation scheme.

The above signs are not hidden or hard to detect. The wallet clusters are clearly recorded on-chain, the trading volume distribution is easily visible on Coinglass, and the identity of the market maker is even explicitly stated in project financing documents. The reason the industry remains indifferent is that all parties are making gains from it. Market makers extract trading shares, the project team calculates treasury valuations based on their controlled chips, and exchanges receive fees regardless of the transaction's authenticity. Only retail investors become the ultimate payers.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。