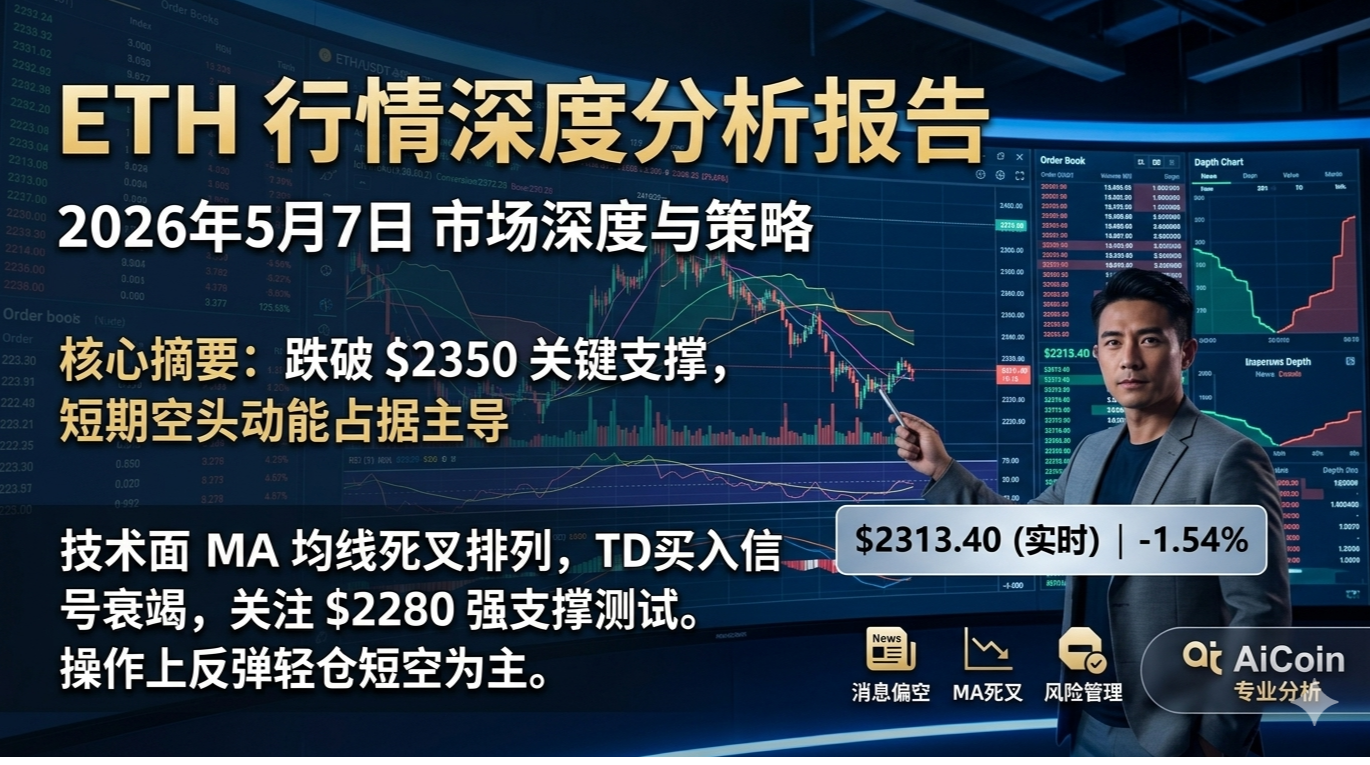

In Miami in May 2026, Consensus 2026 became the site where Bitcoin was simultaneously revalued by “two systems”: at the venue, Eric Trump mentioned—about 18 months ago, JPMorgan had called Bitcoin a “joke asset,” but now it was revealed that the bank allowed high net worth clients to use Bitcoin holdings as collateral for housing loans. Merrill Lynch and Charles Schwab were also “embracing Bitcoin,” which meant that these tightly regulated financial institutions were incorporating Bitcoin into the KYC, anti-money laundering, and capital regulation framework. On the same stage, Grant Cardone promoted his “real estate + Bitcoin” combination, cramming $100 million of Bitcoin exposure into a $235 million real estate project, pushing Cardone Capital's Bitcoin position to about $200 million. This design of embedding Bitcoin within the structure of real estate funds would directly alter the product's classification in securities regulation and taxation, also raising the reporting and compliance costs for investors. As attendees were still basking in the excitement of the “bank door opening,” at the other end of Europe, Germany's Finance Minister Lars Klingbeil confirmed plans to abolish the “one-year tax exemption” and instead tax Bitcoin gains similarly to stock gains. This meant that the long-term tax-free benefits that retail and institutional investors in Europe had relied on were being cut off, and German family asset allocation and asset management product design would have to rewrite their tax assumptions. Ironically, behind Eric Trump on stage was the American Bitcoin mining company supported by the Trump family, which reported a net loss of $82 million in Q1 2026: revenue was only about $62 million and had decreased by about 20% quarter-on-quarter, marking two consecutive quarters of losses. Mining companies were being squeezed by both the volatility of cryptocurrency prices and compliance costs. The opening of bank ports, tightening tax benefits, and shrinking profits for mining companies—a series of actions occurring in and around May 2026—pulled Bitcoin from being a “marginal asset” into the same net of mainstream finance and sovereign taxation. At this moment, Bitcoin was written into mainstream financial terms, as well as into stricter tax forms and audit reports; a new regulatory cycle had begun.

JPMorgan's Attitude Reversal: Is Bitcoin Collateral Cracking Open Regulatory Doors?

While mining companies were still bearing the compliance costs, the winds at the bank ports had already been named in Miami. Eric Trump recalled on the Consensus 2026 stage that about 18 months ago, JPMorgan had referred to Bitcoin as a “joke asset,” but he now revealed that the bank allowed customers to use Bitcoin holdings as collateral to apply for housing loans. This idea of “Bitcoin mortgage loans” was currently reported only by him, with no official announcement from JPMorgan and lacking product details, strictly speaking, it was still unverified information, but even if it was just an internal pilot discussion, it indicated that inside this tightly regulated American bank, the compliance label and risk weights for Bitcoin had already been rewritten from “joke” to a potential asset that could be included in the list of collateral.

Once Bitcoin was accepted as collateral under the existing regulatory framework, banks would have to incorporate such assets into a complete KYC, anti-money laundering, asset valuation, and capital adequacy management chain: from customer identity verification to on-chain source of funds review, from daily market volatility discounts to collateral liquidity stress tests, and finally reporting capital usage and risk concentration at federal and state levels. Eric Trump also mentioned that Merrill Lynch and Charles Schwab were “embracing Bitcoin”; for retail and high-net-worth clients, Bitcoin exposure was transforming from a gray area into a standard product that could appear on compliant account statements. For regulators, if this type of exposure and the credit secured by it continued to grow, it would force them to discuss new standards for collateral quality, liquidity discount rules, and concentration limits, and the boundaries of traditional brokerage, banking, and brokerage platforms were being redrawn around Bitcoin.

Real Estate + Bitcoin Combination: Compliant Product or Regulatory Gray Area?

The stage shifted from bank branches to the Miami venue, where Grant Cardone presented another script for “embracing Bitcoin”: at Consensus 2026, he loudly promoted a so-called “real estate + Bitcoin” mixed strategy, publicly disclosing that in a real estate transaction of approximately $235 million, an additional exposure of about $100 million in Bitcoin was layered in, claiming that Cardone Capital's Bitcoin holdings amounted to about $200 million, hoping to “outperform traditional REITs” through this structure. On the surface, this was a real estate product backed by physical assets; in essence, it was embedding a high-volatility position within a real estate vehicle constrained by securities and fund regulations, bundling risk assets that should be managed separately in brokerage accounts with the perception of stable rental cash flows.

Under the current U.S. securities and fund regulation framework, whether such mixed products could be considered compliant public offerings or only available to qualified investors depended on several key points: first, how to fully disclose the risks arising from severe fluctuations in Bitcoin prices in the fundraising documents; second, how to adopt transparent, repeatable valuation methods in net asset calculations to ensure that crypto positions are not “invisible” on the balance sheet; and third, how the management would fulfill their fiduciary duties in such a structure and explain why an additional layer of Bitcoin risk would be added to leveraged real estate projects. Cardone currently emphasizes potential yield and liquidity advantages, but these claims lack long-term performance data confirmed by independent third-party audits. Regulatory bodies and limited partners are truly focused on how this asset combination is classified in terms of securities regulation and taxation—once this real estate vehicle is identified as a general partnership or fund for tax purposes, the gains from Bitcoin positions will directly alter how investors (individual or institutional) report capital gains tax, while exposing whether there is potential for regulatory arbitrage through structural packaging, which is the key dividing line determining whether it is viewed as an innovative product or a regulatory gray area.

Germany Ends One-Year Tax Exemption: Full Tax Burden Increase for Retail and Family Offices

As the Bitcoin positions in real estate funds were still wrestling with tax classifications, Germany's Ministry of Finance directly turned the table at the regulatory level. Under the current system, individuals could avoid paying capital gains tax as long as they held Bitcoin for more than a year; this clause had long been regarded as one of the world's most lenient tax arrangements. In May 2026, Finance Minister Lars Klingbeil publicly confirmed that the government planned to abolish this “one-year tax exemption” rule, replacing it with taxation akin to stock earnings. The shift in regulatory discourse was also clear: transitioning from exceptional treatment for “private wealth assets” to being taxed alongside financial assets like stocks, tax authorities would no longer reserve special exemptions for long-term holders but would require them to face taxable gains and reporting obligations just as they would for securities investments.

The direct stakeholders being pushed into the limelight were local retail investors, family offices, and institutional accounts primarily focused on long-term holdings. The one-year tax exemption window had once been seen as a制度红利 of “buy and hold to avoid the tax office,” but now this assumption had been shattered, and the cost-benefit calculation for long-term holdings and domestic reporting must be rewritten. Family offices and high-net-worth clients need to renegotiate their strategies, whether to continue reporting taxes in Germany, structure investments offshore, or simply reduce their Bitcoin allocations, while retail investors must face the reality that each reallocation might trigger a tax liability. Critics have already pointed out that this adjustment deviates from the previous policy direction encouraging long-term holding, potentially squeezing the space for “long-term investors.” However, whether actual migration scale and holding behavior will experience a cliff-like change remains a matter of judgment. More broadly, as a core economy in the EU, Germany was once seen as a “friendly template” for crypto tax systems; now tightening the rules provides political legitimacy for other member countries to raise tax burdens or promote regional coordination, and it plants new uncertain variables in reclassifying domestic and offshore investment maps for European investors.

Trump-affiliated Mining Companies Continuous Losses: Dual Pressures from Compliance Costs and Price Fluctuations

If Germany is redrawing the earnings line at the tax front, American mining is being “doubled down” on the costs by both regulation and the market. American Bitcoin, co-founded by Eric Trump and supported by the Trump family, has delivered a dismal performance in such an environment: the company disclosed consecutive quarterly losses, with a net loss of about $82 million in Q1 2026, up from about $59 million in the previous quarter, while revenue was only about $62 million, a decline of around 20% quarter-on-quarter. In the context of tightening output cycles and stricter local electricity regulation, such a profit and loss structure means that each price decline, intensified competition for computing power, or adjustment in electricity prices would be quickly amplified in financial reports, and the disclosure rules of the U.S. public market do not allow such fluctuations to be “hidden in the ledger.”

For investors, this is not just an issue of an ugly quarterly report. As a mining company listed in the U.S. securities market, American Bitcoin must continuously disclose risk factors and internal control statuses. The expansion of losses not only weakens its narrative space for telling a growth story but may also compress its future financing capabilities and affect its risk rating in the eyes of regulators. More challenging is that the Bitcoin reserves, mining costs, and gross margins that the outside world can see come largely from single-source estimates, and the real safety margins remain to be validated by subsequent financial reports and third-party statistics. Under the dual pressures of tightening regulation, rising compliance costs, and a profit heavily dependent on price fluctuations, electricity policies, and computing power landscapes, capital, projects, and regulatory resources are being slowly shifted toward mining companies that can prove they are “using less electricity and have more controllable compliance costs,” which will reshape the mining landscape in the coming years.

Bitcoin's Coming of Age Ceremony: Accepting Regulation Comes with a Higher Price

When JPMorgan, Merrill Lynch, and Charles Schwab were publicly named as “embracing Bitcoin,” allowing high-net-worth and retail customers to obtain relevant exposure through compliant accounts, and even rumors emerged that they accepted housing loan applications secured by Bitcoin holdings, this type of asset, which belonged to the edge circles, was, for the first time, viewed as a subject that could be incorporated into bank risk control models and collateral lists; at the same time, Germany's finance minister confirmed plans in May 2026 to abolish the “one-year tax exemption” rule, bringing Bitcoin gains into the capital gains tax system similarly to stocks, combined with the reality of American Bitcoin's Q1 2026 reports disclosing consecutive losses and declining revenues, delivered a serious wake-up call to all participants in the chain: once entering the view of mainstream finance and taxation, the previous narrative of “unregulated safe haven” will be replaced by a new order of “highly regulated, high-cost but sustainable participation.” For platforms and users, this coming-of-age ceremony has two sides: on one hand, the opening of bank ports and the increase of compliant exposures, but with stricter KYC, anti-money laundering, and risk limits, real estate funds and limited partnership structures embedding Bitcoin positions must face more disclosure and reporting obligations; on the other hand, actions like Germany tightening the tax system weaken the tax benefits of long-term holding but provide a clearer reporting path and a more predictable compliance framework. The true variables lie ahead: whether Germany's approach will be replicated by other European countries or even more jurisdictions, whether U.S. regulatory bodies will introduce more detailed classifications and capital rules for loans secured by Bitcoin and mixed products, will determine whether the “coming of age costs” for Bitcoin are merely a short-term pain or become a long-term high-load new normal written into the global financial order.

Join our community, let’s discuss together and become stronger!

Official Telegram community: https://t.me/aicoincn

AiCoin Chinese Twitter: https://x.com/AiCoinzh

OKX Benefits Group: https://aicoin.com/link/chat?cid=l61eM4owQ

Binance Benefits Group: https://aicoin.com/link/chat?cid=ynr7d1P6Z

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。