Original Author: Sleepy.md

On April 29, 2026, Microsoft, Google, Meta, and Amazon submitted their Q1 results on the same day. If we look at the capital expenditure guidance given by these four companies separately, the number approaches $650 billion. This scale is already equivalent to an entire year's GDP of Sweden.

In other words, the four richest technology companies in the world are preparing to use the economic volume of a moderately developed country for the ticket that leads to the era of AGI.

Now everyone’s eyes are firmly fixed on the ticket to AGI. At this moment whimsically dubbed the global AI asset "battle night," if we slightly shift our gaze from those grand narratives to look at those unremarkable, hidden corners, you will discover a covert struggle about physical shackles, capital anxiety, and industrial restructuring, which has actually reached a critical point of revelation.

How did a company without a financial report bring down the U.S. stock market?

What truly controls market sentiment may not necessarily be the companies with the most profit on the books, but rather the enterprise regarded by everyone as a "totem of faith."

April 29 was supposed to be the most significant day of earnings season for U.S. stocks. However, before the listed companies submitted their reports, the market first experienced a sudden and unanticipated stampede. According to Goldman Sachs data, this was the second worst trading day for AI assets since the beginning of this year.

The trigger was not poor performance from any listed company, but rather a report from the Wall Street Journal the day before, which stated that OpenAI had failed to meet its revenue targets for 2025, and the goal of having over 1 billion active users was still far off. More painfully, the report mentioned that OpenAI CFO Sarah Friar had internally warned that if revenue growth continued to fall short of expectations, the company might find it difficult to uphold its $600 billion commitment to computing power procurement.

A company that is not publicly listed and does not need to release financial reports was able to cause Oracle's stock to drop 4%, CoreWeave to fall 5.8%, and even SoftBank, located across the Pacific, to crash 12% in the over-the-counter market, all due to a rumor.

When the $600 billion promise of computing power collided with unfulfilled revenue growth, the market suddenly realized that the most dangerous aspect of the AI narrative was not the lack of belief in the future but rather that the future was simply too expensive.

Over the past two years, OpenAI has been like a religion in Silicon Valley.

Graphic card procurement, data center construction, cloud vendor expansion, startup valuations—many seemingly disparate decisions are all based on the same judgment: that model capability will continue to leap forward, user scale will continue to expand, and AGI will ultimately turn all today's expensive investments into future tickets.

The strongest aspect of this logic is its self-reinforcement. The more believers there are, the higher the valuation; the higher the valuation, the less willing people are to doubt.

However, around April 29, the market began to seriously question the cash flow issues of this faith; even OpenAI had to face customer acquisition costs, user retention, revenue growth rates, and computing bills.

The Money Printer and the Cooling System

The most fascinating aspect of the internet era is that growth appears almost limitless.

A piece of code is written, copied to ten million users, and the marginal cost is minimized. Over the past twenty years, Silicon Valley has dared to disrupt traditional industries using "cash burning for growth" based on this belief: as long as the network effect is strong enough, scale will swallow costs.

But in the AI era, the digital world's money printer is being choked by the physical world's cooling system.

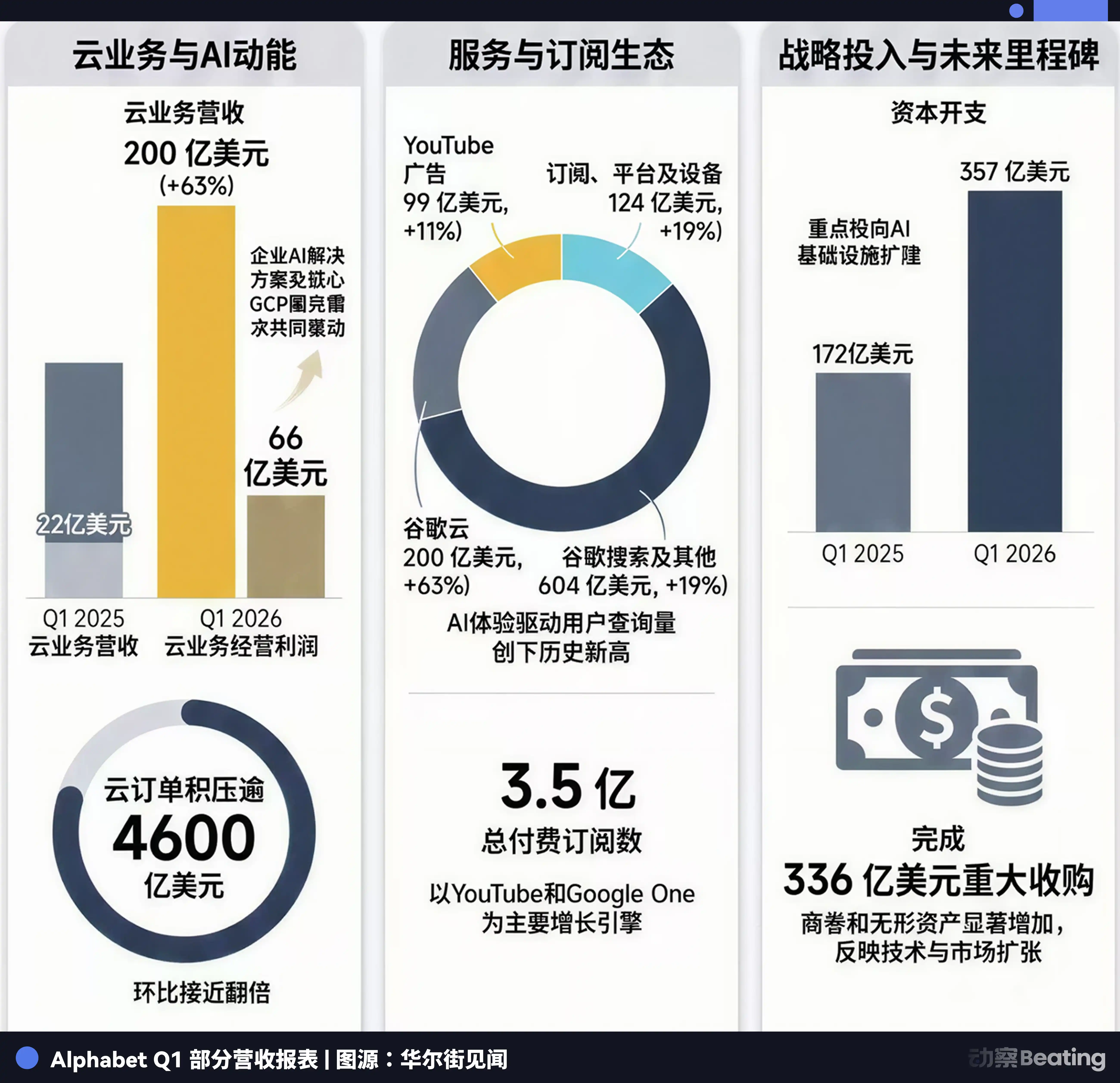

During the earnings call on April 29, despite the cloud business's astonishing growth rate of 63% (with quarterly revenue surpassing $20 billion for the first time), Google CEO Pichai expressed helplessness: "If we could meet the demand, cloud revenue could have been even higher."

Behind this statement lies the peculiar business dilemma of the AI era: demand far exceeds supply, yet growth is ruthlessly constrained by the physical world.

Google has $462 billion in cloud order backlog, nearly doubling from the previous period. AI solutions product growth has seen a year-on-year increase of nearly 800%, Gemini Enterprise’s paid users have grown by 40% from the previous quarter, and API token usage skyrocketed from 10 billion to 16 billion per minute.

These numbers, in any internet company, would signify growth worth celebrating. But in Pichai's statement, we can hear a new type of dilemma emerging in the AI era: customers are already queuing, money is on the way, but servers have yet to be built, power has yet to be connected, and advanced chips have not yet been manufactured in the foundries.

It’s not a lack of demand; it's too much demand, pulling growth back into the physical world.

Microsoft is facing the same dilemma. Azure's growth rate reached 40%, and AI annual revenue surpassed $37 billion; this number was only $13 billion in January 2025, nearly tripling in 15 months.

However, Microsoft’s capital expenditure decreased to $31.9 billion from $37.5 billion in the previous quarter. Microsoft explained in its earnings report that this was due to "the timing of infrastructure construction." The implication is that while money can be allocated today, data centers won’t spring up overnight; GPUs can be ordered, but power, land, cooling systems, and construction timelines cannot be hastened by capital markets.

When everyone thinks we are rushing toward a virtual world, what ultimately determines the outcome remains the oldest heavy assets and physical laws.

Computing power is becoming a new type of "land resource": limited in the short term, slow to build, important in location, and first comers first secure the supply. In this land grab, it is not because the four giants have all figured out the returns that they dare to push capital expenditure to the level of $650 billion; it is because they fear that if they do not hoard these "lands," they may not even be at the table tomorrow.

The Money Burning Approach

After the market closed on April 29, despite similarly exceeding expectations with earnings and raising capital expenditure, Google’s stock rose 7%, but Meta plummeted 7%.

To be fair, Meta delivered quite a stellar report with revenue of $56.31 billion, a year-on-year growth of 33%, the fastest growth rate since 2021; EPS reached $10.44, significantly exceeding Wall Street's expectations.

But Zuckerberg made a taboo move by raising Meta's 2026 capital expenditure guidance to $125 billion to $145 billion. The better the performance, the more anxious the market became. Because what investors are truly worried about is not whether Meta is making money now, but whether it intends to use cash earned from today's advertising business to support a risky AI gamble with an unclear repayment pathway.

The market's punishment was ruthless, and the difference lies in the granularity of business monetization.

Google, Amazon, and Microsoft's AI expenditure can at least be accounted for in a relatively clear ledger.

Google has a cloud order backlog of $462 billion, Amazon has AI annual revenue for AWS, and Microsoft has paid users for Copilot along with high RPO. Every dollar they burn, while it may not immediately recoup its cost, at least Wall Street knows roughly where that money will come back from: enterprise customers, cloud contracts, software subscriptions, and computing power rentals.

This is why the capital market is willing to continue listening to their stories. The stories can be distant, but the payment path cannot be entirely invisible.

The trouble for Meta is that it does not have a cloud business to sell externally.

It has poured in thousands of billions of dollars, which ultimately have to be realized through a more complex path. Meta's AI assistant needs to increase user stickiness, recommendation algorithms need to improve ad conversion, AI-generated content needs to extend user engagement, and smart glasses and future hardware need to become new entry points.

This logic is not invalid; it's just that the chain is too long. Cloud vendors burning money are putting GPUs into already signed contracts; Meta burning money is putting GPUs into an ad efficiency model that has not been fully proven. The former can be discounted, while the latter can only be initially trusted. Although logically sound, the monetization chain is too long, and Wall Street lacks the patience.

In capital markets, patience is a luxury. Especially when capital expenditures are pushed to the hundreds of billions level, investors are willing to pay for the future but will not pay indefinitely for ambiguity.

What’s more anxiety-inducing is the time lag.

Amazon CEO Andy Jassy candidly stated during the call that the majority of the funding invested in 2026 will not yield returns until 2027 or even 2028.

This means that the giants are pushing today's cash flow onto the realization of capacity two years down the line. There is a gap involving data center construction, chip supply, power access, customer demand, and model iteration. Any deviation in one link can lead to a re-evaluation by capital markets.

The greatest danger of the AI arms race lies here: money is spent today, stories are told today, but answers will not be revealed until two years later.

Blurring Industrial Boundaries

AI has not quickly pushed search off the table as many expected two years ago.

When ChatGPT first emerged, the market once believed that search ads would be swallowed up by direct answers, and companies like Perplexity were given high hopes. However, in Google’s earnings report on April 29, the data showed that search query volume hit an all-time high, and ad revenue reached $77.25 billion, growing 15% year on year.

This resembles the "Jevons Paradox" in the AI era. In 1865, British economist William Stanley Jevons discovered that improvements in steam engine efficiency did not reduce coal consumption; rather, they led to a significant increase in coal usage because the efficiency improvements made steam engines affordable for more people, thereby igniting overall demand. Similarly, AI has made search more complex, leading users to ask more questions.

This is also why Google finds it easier to persuade the market compared to Meta. It has cash flow from old gateways, and new books from cloud businesses; it can make money from ads as well as from corporate demand for computing power. AI has not torn down its walls; at least so far, it has helped thicken them.

Similar boundary reconstructions are occurring in the chip industry. On the same day, the mobile chip king Qualcomm released a revenue report of $10.6 billion. During the call, CEO Cristiano Amon announced a major decision: Qualcomm is officially entering the data center market, collaborating with a top hyper-scale cloud vendor on custom chips expected to be shipped later this year.

Qualcomm's main battlefield has always been mobile devices. But as AI's computational load begins to redistribute between the cloud and the edge, it must redefine its position.

If future AI is entirely handled by large cloud models, the value of mobile chips will diminish; if edge AI becomes standard, Qualcomm must demonstrate that it does not only belong to mobile but can also enter inferencing, terminals, and low-power data centers.

Its entry into data centers is less offensive and more defensive.

As AI shifts from being a "luxury of the cloud" to a "standard of the edge," all industrial boundaries start to blur. Mobile chip companies try to enter data centers, cloud vendors begin developing chips in-house, and chip companies are exploring models. Qualcomm's "defection" is merely the tip of the iceberg in this major reconstruction.

The Same Gold Rush, Two Sets of Valuation Languages

The same AI gold rush in U.S. stocks has already entered a stringent "monetization disproof period." Even the leading semiconductor process control and inspection equipment manufacturers face market revaluation if they exhibit even a hint of geopolitical and tariff risk. On April 29, after hours, KLA Corporation reported an unexpected revenue of $3.415 billion, with a Non-GAAP EPS of $9.40, higher than the expected $9.16.

However, the stock price briefly dropped 8% after hours.

The reason was not poor performance but market concerns over tariffs and exposure to China. KLA’s client list includes numerous Chinese foundries. Against the backdrop of U.S.-China tech decoupling, this "exposure to China" hangs like the sword of Damocles over them. No matter how impressive the performance, it cannot offset the market's instinctive fear of geopolitical risks.

In the A-share market, a different language is being used.

Here, performance is certainly important, but often, performance is just fuel; what truly ignites is the narrative, whether you hold a ticket called "domestic substitution."

On the evening of April 29, Cambrian delivered an impressive Q1 report: revenue of 2.885 billion yuan, a year-on-year surge of 159.56%, marking the first time it surpassed the 2 billion mark in a single quarter; net profit reached 1.013 billion yuan, a year-on-year growth of 185.04%. The following day, Cambrian's stock surged, and its total market value surpassed 670 billion yuan, achieving a historical high with an increase of over 62% since the beginning of the year.

On the same day, Muxi Technology also released its financial report, with revenue of 562 million yuan, a year-on-year increase of 75%, and a significant reduction in losses from 233 million yuan in the same period last year to 98.84 million yuan. This is the first Q1 report from this GPU company, which only got listed in December 2025.

Both are part of the AI infrastructure chain, yet the U.S. stock and A-share markets provided completely different pricing reactions.

KLA faces a complex ledger of a global supply chain, where performance, orders, tariffs, exposure to China, and export controls may all factor into the valuation model.

Cambrian and Muxi Technology, on the other hand, are up against a different narrative environment; the stronger the external restrictions are, the easier it is to amplify the strategic value of domestic computing power. U.S. stocks are applying a risk discount, while A-shares are offering a scarcity premium.

The Exit of Smart Money

But just as the market was cheering for Cambrian, one detail seemed somewhat glaring.

By the end of 2025, super investor Zhang Jianping still held 6.8149 million shares of Cambrian, valued at about 9.2 billion yuan, making him the second-largest individual shareholder of the company. By the time of this Q1 report, he had quietly exited the top ten shareholders list.

If we roughly estimate the funds corresponding to this reduction based on the Q1 stock price range, it was at least in the tens of billions. The specific price is unknown to the outside, but it can be confirmed that before the performance explosion and stock price hit a new high, the first to benefit from this narrative dividend chose to cash in.

There are always two types of people in the market: those who buy into the narrative and those who price it.

Zhang Jianping clearly belongs to the latter. He entered the market before Cambrian became a common consensus and turned away after it was written into the grand narrative of "domestic computing power leader."

On this $650 billion earnings night, Silicon Valley giants are anxious amid computing power shortages, Wall Street analysts are tormented by the time lag in monetization, while A-shares are busy revaluing domestic computing power.

In this same AI gold rush, every market is using its own language. The U.S. stock market talks about return cycles, while the A-share market discusses domestic substitution; cloud vendors talk about order backlogs, while Meta discusses ad efficiency; OpenAI has not released a financial report but still pulls the strings of the entire computing power chain.

Everyone is convinced they have bought a ticket to the AGI era. But no one knows when this performance will conclude and where the exit lies. The ticket to the AI era is certainly expensive. But more expensive than the ticket is knowing when to exit.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。