Original Title: "Powell's Departure, Oil Prices Rising, Hawkish Tone Heating Up -- Wall Street Comments on the Federal Reserve's Decision"

Original Author: Zhao Ying

Original Source: Wall Street Journal

The Federal Reserve kept its stance unchanged, yet Wall Street heard a louder hawkish tone. Three dissenting votes against maintaining an accommodative bias, soaring oil prices creating inflationary pressures, and the nearing end of Chairman Powell's term collectively pushed the market from pricing in rate cuts to a more complex assessment of rate hike risks.

According to the Wind Trading desk, at the FOMC meeting on April 29, the Federal Reserve maintained the target range for the federal funds rate at 3.50%-3.75%. Post-meeting interpretations from Goldman Sachs, Bank of America, JPMorgan Chase, and HSBC all pointed to the same conclusion: what truly matters is not the interest rate decision itself, but the expanding divergence in the wording of the statement, indicating a loosening consensus within the committee on policy direction.

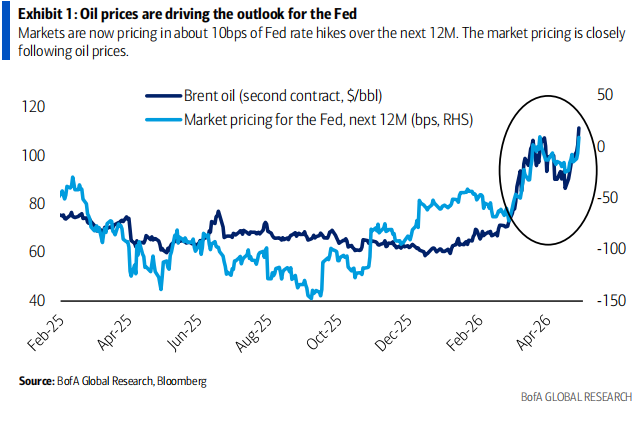

The deteriorating situation in Iran made oil prices another key theme of the meeting. Bank of America noted that the 2-year Treasury yield rose 10 basis points that day, with only about 3 basis points occurring after the Fed's decision was announced, while the remaining 7 basis points were primarily due to Brent crude oil surging 8% to $120 per barrel. JPMorgan Chase also believed that the situation in Iran and the risks in the Strait of Hormuz were pushing energy prices higher, directly restricting the Federal Reserve's room for accommodation.

The transfer of power heightened policy uncertainty. Powell confirmed that this would be his last FOMC meeting as chairman of the Federal Reserve and stated that after his term ends, he would continue to serve on the FOMC as a regular governor, with the duration of his continued service yet to be determined. Meanwhile, the Senate Banking Committee has advanced Kevin Warsh's nomination to be the next Federal Reserve chairman. An era of monetary policy is officially coming to an end, and the successor's policy style and communication framework are becoming the new focus of the market.

Three Dissenting Votes, Accommodative Bias No Longer Stable

The most notable signal from this meeting was the internal division within the FOMC regarding the statement's wording.

Goldman Sachs economist David Mericle pointed out that three committee members, Hammack, Kashkari, and Logan, opposed the wording of the statement that implied an accommodative bias, which was unexpected by Goldman Sachs. Meanwhile, Miran supported a rate cut, aligning with Goldman Sachs' previous judgment.

The controversy centered on the statement's wording regarding "the timing of additional adjustments." This phrasing is seen in market contexts as a signal that maintains the possibility of further rate cuts. The opposition from the three members to retaining this wording suggests that some decision-makers are unwilling to continue providing a one-way accommodative hint to the market.

Powell acknowledged at the press conference that the committee had "intense discussions" around policy guidance. He stated that the number of committee members supporting a shift to more neutral guidance had increased since March, indicating that the FOMC's central position is moving towards a "more neutral" rate outlook, although most members believe that the current timing is not yet mature. He even mentioned that wording adjustments "might come at the next meeting at the earliest" — that is, at the meeting on June 16-17.

HSBC also emphasized that the essence of the disagreement is that the policy direction is no longer one-sided. Although the three committee members supported keeping the interest rate unchanged, they clearly opposed continuing to maintain an accommodative bias, effectively signaling to the market that the next action could be either a rate cut or a rate hike.

"Rate Hike" Returns to Pricing, Rate Cut Threshold Raised

Wall Street's common judgment is that the Federal Reserve has not officially shifted to rate hikes, but the term "rate hike," which has been dormant for a long time, has officially returned to the market's view.

Bank of America stated that after the slightly hawkish FOMC meeting concluded, coupled with new highs in oil prices, the market has now priced in nearly 10 basis points of rate hike within the next 12 months. The bank also noted that this is different from the rate hike cycle in 2022, as the current energy shock will also exert downward pressure on growth, a point Powell had hinted at during the press conference.

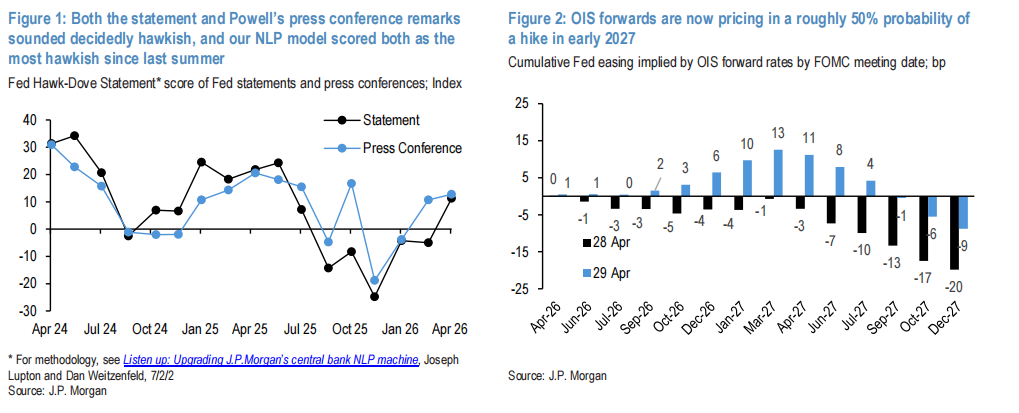

JPMorgan Chase provided an even more hawkish interpretation. Their natural language processing model indicated that the hawkish rating of this statement and Powell's press conference achieved the highest level since June 2025. The bank stated that the pricing in the money market has quickly shifted from previously "close to a full rate cut by the end of 2027," to "close to a 50% probability of a rate hike by early 2027."

Goldman Sachs, however, maintained a more cautious stance. The bank still predicts that the Federal Reserve may cut rates in September and December, but believes that the threshold for rate cuts has clearly risen without significant weakness in the labor market. Goldman Sachs stated that the risks of prolonged pauses in interest rates are rising, but they remain highly skeptical about the possibility of rate hikes.

HSBC's forecast is the most stringent. The bank anticipates that the Federal Reserve will not cut rates in 2026 and 2027. HSBC believes that if core PCE inflation does not fall below 3%, or even 2.5%, discussing rate cuts is virtually impossible, and its own forecast indicates that core PCE inflation will remain above 3% before the end of 2026 and above 2.5% before the end of 2027.

Oil Prices Take Center Stage, Iranian Situation Dominates Pricing Logic

Unlike previous instances where the Federal Reserve's statements dictated market responses, this time, energy prices became the core variable in the interest rate market on the day of the meeting.

Bank of America stated that of the 10 basis points rise in the 2-year Treasury yield, only about 3 basis points can be attributed to the Fed's decision itself, while most of the increase came from Brent crude oil rising to $120 per barrel. The bank believes that the main driving force behind the current Federal Reserve outlook is the situation in Iran and oil prices, rather than a simple policy reaction function.

JPMorgan Chase also attributed the rise in front-end yields and the flattening of the yield curve to the deteriorating situation in the Middle East and risks in the Strait of Hormuz. The rise in oil prices not only lifts inflation expectations but also makes it more challenging for the Federal Reserve to release easing signals.

Powell clearly mentioned at the press conference that under the current context of high uncertainty around war and energy prices, most committee members believe there is no need to adjust policy guidance at this time. JPMorgan Chase noted that Powell also set the preconditions for potential rate cuts, stating that stability in energy prices and progress on tariff issues are necessary.

Goldman Sachs believes that even if geopolitical conflicts end in the future, some FOMC members may still hold reservations about rate cuts while inflation remains closer to 3% rather than 2%. Even if inflation pressures mainly stem from tariffs and energy price transmissions, policy easing may not arrive quickly.

Powell Bows Out, Warsh’s Succession Introduces New Variables

This meeting also marked the nearing end of Chairman Powell's term.

Bank of America stated that this is Powell's last FOMC meeting as chairman of the Federal Reserve. Goldman Sachs' report also mentioned that Powell indicated he would continue to serve on the FOMC as a regular governor after his term ends on May 15, with the duration of his continued service yet to be determined.

Regarding the reasons for his continued tenure, Goldman Sachs stated that Powell mentioned he is waiting for related investigations to conclude in a transparent, definitive manner before deciding when to leave. JPMorgan Chase and HSBC also noted that Powell intends to keep a low profile and will not obstruct the operations of the FOMC under Warsh's leadership.

The progress of Warsh's nomination has become a focal point for the market. JPMorgan Chase stated that the Senate Banking Committee has voted along party lines to approve his nomination. HSBC pointed out that the full Senate vote has not yet been completed, but if things progress smoothly, Warsh is expected to officially take office before the June meeting.

HSBC believes Warsh may bring systematic changes to the policy communication framework. The bank’s interest rate strategist noted that Warsh has previously expressed skepticism about the Federal Reserve's "dot plot" interest rate forecasting mechanism. If forward guidance is weakened in the future, volatility in the bond market could increase, and long-term interest rate term premiums may also face upward pressure.

Rate Volatility and Policy Uncertainty Coexist

For fixed income investors, the messages conveyed by this meeting are not singular. Short-end yields are suppressed by oil prices and hawkish pricing, delaying expectations for rate cuts, but rate hikes have not yet become a consensus scenario among investment banks.

Bank of America believes that the current rise in yields has, to some extent, hedged against the impact of interest rate volatility for the investment-grade bond market. Since implied volatility of interest rates remains below the peak in March this year, the technical outlook for investment-grade bonds still has phase support.

JPMorgan Chase indicated that short-end yields are under pressure, mid-term Treasury valuations appear high, and the policy uncertainty brought about by the leadership transition means that the interest rate market is entering a more complex game stage.

HSBC maintains a "maximum bullish" stance across multiple assets and focuses on U.S. stocks. The bank stated that although interest rate expectations have undergone a hawkish reassessment, risk assets performed strongly in April, with optimistic sentiment regarding profitability in the artificial intelligence industry chain remaining an important narrative in the multi-asset market.

Overall, Wall Street concludes from this FOMC that: the Federal Reserve did not change interest rates, but changed the probability distribution of the next actions in the market. Powell's departure, rising oil prices, and Warsh's succession mean that investors are no longer facing a simple timeline for rate cuts, but a new interest rate environment driven by inflation, energy, employment, and policy communication.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。