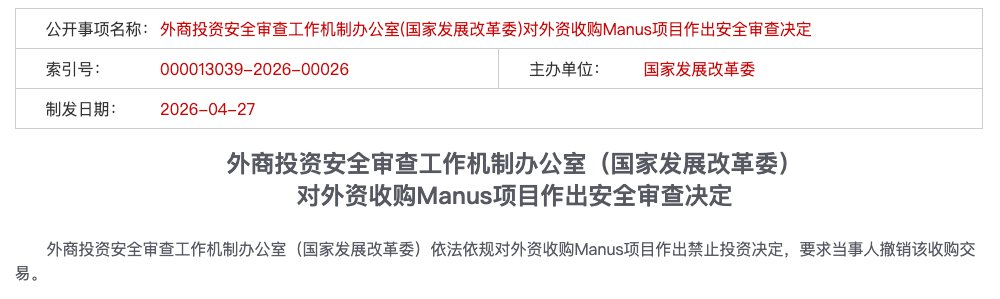

On April 27, 2026, the Office of the Foreign Investment Security Review Mechanism (National Development and Reform Commission) made a decision to prohibit foreign investment in the acquisition of the Manus project, requiring the parties involved to withdraw from the acquisition transaction.

In just a few dozen words, the button to terminate this transaction valued at over $2 billion was pressed directly. The efforts put into refining Manus’s products, slicing the legal framework, financing, and exit arrangements over the years all came crashing down, rendered pointless.

This is the first publicly halted foreign capital acquisition case in the AI field since the implementation of the Foreign Investment Security Review Measures in January 2021.

What is unique about this transaction is that both parties involved have been legally restructured abroad: Meta is a U.S. company, and Manus has completed its registration in Singapore, establishing a holding structure in the Cayman Islands. However, Chinese regulatory authorities still ultimately made a decision to prohibit investment.

The spillover effects of this case are also being felt by AI companies like Moonlight Dark Side, ByteDance, and Leapstar, which are facing clearer compliance guidance.

Behind this lies a deeper issue: the traditional offshore structure is becoming completely ineffective. Entrepreneurs must clarify their compliance paths from Day 0.

This article does not tell a story, but gets straight to the point - what laws and regulations are being followed by regulators; where are the red lines drawn for the "bath-style going abroad"; and from today onward, how companies should choose.

1. What laws and regulations are being followed?

Looking back at the Manus case, the industry's initial discussions mostly focused on "what happened" - migration, slicing, prohibition. But as the details of the case gradually surface, the focus of the legal community returns to a more fundamental question: By what authority can the regulators stop this transaction? What laws are they relying on? What regulations are they citing?

The answer is not found in a single law, but in a three-tiered regulatory logic. The synergy among the three layers ultimately constitutes an inescapable review logic.

First Layer: Identifying "Chinese Entity" - The Underlying Basis for Penetrating Review

This is the legal starting point of the entire case: What exactly is Manus’s company?

From a legal perspective, the answer seems clear - Manus has completed its registration in Singapore, the holding structure is located in Cayman, and the parent company Butterfly Effect Pte is a genuine Singaporean entity. This is the core legal argument presented by the Manus team throughout the transaction:

“Our entity structure has been converted to an overseas structure.”

But the regulators’ response is:

Formalities do not count; substance is what matters.

The law firm Jincheng Tongda & Neal systematically analyzed from a legal perspective why the "legal shell's offshore restructuring" failed in the Manus case. The root cause is that the core assets of AI have substantial ties to the Chinese legal domain across four dimensions:

- Team Dimension: The engineer team that masters the underlying core logic has long accumulated R&D experience within China, and their technical capabilities have been developed and trained in China;

- Computational Power Dimension: Domestic R&D has formed path dependencies for technical interfaces and computational resource scheduling, with the architectural genes of the core system marked by Chinese labels;

- Algorithm Dimension: The development and training of the core model weights have completed within China, representing the most legally significant "technical source";

- Data Dimension: The training data accumulated through human feedback reinforcement learning (RLHF) based on massive user interactions is highly concentrated within China.

These four dimensions point to the same conclusion: Manus's legal form is Singaporean, but the "technical substance" of Manus as a company, its origin, core, and foundation are all in China. Based on the principle of "substance over form," this substantial connection is sufficient to constitute the basis for penetrating review from a regulatory perspective - this is the first cornerstone of all subsequent legal actions.

Thus, although in 2022, Xiao Hong established Butterfly Effect Technology in Beijing, in 2023, built a "Cayman-Hong Kong-Beijing" red-chip structure, and in 2025, migrated to Singapore completing team slicing and business isolation. However, legal recognition does not consider "when it was migrated out," but rather "where it came from." Any technological asset originating in China does not change nationality merely by a change in registration.

Second Layer: Export Restrictions and Regulatory Avoidance - Legal Qualities of Bath-Style Going Abroad

Once the first layer is established: Manus is identified as a "domestic enterprise," the legal logic of the second layer follows: transferring core assets abroad constitutes an export action. Export actions must adhere to export control regulations.

Manus's three-step actions form a complete puzzle of "avoiding export control" in the eyes of regulators:

First step, subject transfer. The company was transferred from China to Singapore, establishing the overseas entity Butterfly Effect Pte, completing the first step of "de-Chinization" legally.

Second step, team and asset relocation. Almost two-thirds of the staff (80 out of 120) in China were laid off, retaining over 40 core technical staff who relocated to Singapore.

Third step, data and business disjunction. Clearing domestic social media accounts, blocking access from Chinese IPs, terminating cooperation with domestic firms like Alibaba Tongyi Qianwen.

Legally, the technical knowledge, R&D capabilities, and algorithmic experience carried out of the country by core technical personnel constitute "technical exports" potentially covered by the "Prohibited or Restricted Export Technology Catalog." Meanwhile, according to the Data Security Law and the Data Export Security Assessment Measures, the large amounts of user interaction data training completed before disjunction were highly concentrated within China - the data gene has already been written into the model, and the disjunction action cannot be retrospectively deleted.

Thus, the penetrating logic of regulation can be summarized in a cold phrase:

Codes are written on Chinese soil, and data grow from Chinese users - this is "Chinese assets"; transferring is exporting, and exports are subject to control.

Moreover, the essence of "bath-style going abroad" is to cover substantive violations with formal compliance, which constitutes systematic avoidance of export control regulations.

Third Layer: Proactive Declaration Mechanism - One Cannot Say "I Didn't Know"

If the first two layers represent "substantive violations," the third layer represents "procedural violations" - and it’s the most easily convicted line.

Article 4 of the Foreign Investment Security Review Measures clearly states that for foreign investment involving important information technology and key technologies, the parties "shall proactively declare to the Office of the Work Mechanism before implementing the investment." This is a mandatory pre-declaration obligation, not a "suggestion," nor "to be supplemented after an incident occurs."

Throughout the transaction process, Manus and Meta never made any form of proactive declaration to Chinese regulatory authorities until the completion of the transaction. During the lengthy months of the closing period, Manus and its investors seemed to reach a dangerous tacit understanding: as long as the regulators did not knock on the door, they wouldn't proactively open the window.

In legal practice, "failure to declare" in itself constitutes a serious independent violation. It conveys the signal: either knowingly breaking the law or deliberately avoiding it. Either way, regulators are unlikely to let it go lightly.

A compliance lawyer summarized post-incident:

"The biggest compliance flaw exposed by the Manus case is not the controversy of the applicability of certain regulations, but that the enterprise fundamentally abandoned its declaration obligations to Chinese regulators. Within the legal system, evading procedures is even less tolerable than substantive violations."

Looking back, the ending of Manus was already determined at the first layer: once penetrating review determines that you are a "substantively Chinese entity," the export control logic of the second layer and the declaration obligations of the third layer will automatically unlock. The three tiers of legal reasoning proceed step by step and interlock, forming a logical closed loop. In this closed loop, no link is left for "luck."

2. Why is it the National Development and Reform Commission?

The Ministry of Commerce was the first to take action. On January 8, 2026, a spokesperson for the Ministry of Commerce publicly stated that it would assess consistency with export controls, technology import and export, foreign investment, and other related laws and regulations concerning the acquisition. However, on April 27, the hammer fell from the National Development and Reform Commission.

This switch in departments has its implications. Some experts believe that the Ministry of Commerce is relying on the “Prohibited or Restricted Export Technology Catalog,” which describes the controlled technologies very specifically: technology for AI interactive interfaces specifically used for the Chinese language and minority languages. After "bathing," all services of Manus have been switched to English, and Chinese users are barred from access. This means that if the line of export control is simply followed, there may be some controversy.

This creates a space for the controversy of regulatory applicability. However, we tend to lean towards a deeper meaning; after all, the applicability of the law is ranked lower than political considerations.

The National Development and Reform Commission manages "security review," while the Ministry of Commerce manages "technology import and export." The involvement of the National Development and Reform Commission indicates that this matter has transformed from "business" to "sovereignty."

In other words, the National Development and Reform Commission, as a macro department with more comprehensive economic management authority than the Ministry of Commerce, sends a clear signal with its intervention - this is not an incident of law enforcement against a single company but rather a systematic deterrent of "strike once to prevent a hundred strikes."

Killing one serves as a warning to many.

All practitioners still observing from the sidelines have now seen where the red lines are drawn - they are not in vague areas of specific clauses but in maintaining national security, an undeniable final measure.

3. Four High-Risk Trigger Points

Based on the Manus case and the "penetrating review" principles established by the Foreign Investment Security Review Measures, the following four red lines are now clear. Stepping on any one of these, the "bath-style going abroad" path should be abandoned.

Red Line 1: Founder Holds a Chinese Passport, Has Not Renounced Chinese Citizenship

The founding member of Manus, Xiao Hong, is a Chinese national. The jurisdiction of Chinese export control laws covers natural persons. This means that the founder themselves could also become a focus of regulatory attention, and related arrangements cannot only be understood at the company level.

A harsher reality is across the Pacific: in the geopolitical risk assessments of North American VCs, the funding environment for Chinese founders has also been tightening. Leading Silicon Valley venture capital firms like a16z, under geopolitical pressure, have dramatically reduced their investment willingness towards founders holding Chinese passports.

The B round of financing for Manus was led by Benchmark, but afterward, Benchmark faced strong backlash from U.S. political circles regarding this investment, with several Republican senators claiming that the transaction was "assisting the Chinese government."

Investors at Silicon Valley's Founders Fund expressed candidly:

The founder is Chinese, the company is in Beijing, and the core technology is a general AI agent - that is the "original sin."

Both sides are closing doors. If you hold a Chinese passport, American capital is uneasy; if you have Chinese technology, Chinese regulators won’t let go. This gap is narrower than most people think.

Red Line 2: Received State Assets

It is not only "sovereign wealth fund direct investments" that count as state assets. Government guide funds at all levels, state-owned components in RMB fund LPs, loans from policy banks - these all fall within the recognition of "state asset blood transfusions." Also, those office, computational power, and talent subsidies that are often complained about during application are kept in mind for later accounting during audits.

Red Line 3: The First Line of Code Was Written in China

The initial writing location of core code, the completion location of algorithm model training, the storage location of technical documents - these seemingly "purely technical" facts legally constitute proof of the "technical source." The early development of Manus was completed within China, and when the team relocated to Singapore, the code they carried itself constituted technical exports. Moreover, Manus never made any technical export declaration concerning this transfer.

Red Line 4: Used Chinese Data

This is an illusion many AI entrepreneurs easily fall into: believing that as long as domestic users are cleared, and Chinese IPs are blocked, the company becomes clean.

But in the eyes of regulators, the "technical substance" looks not only at code but also at data genes.

The Data Security Law and the Data Export Security Assessment Measures have explicit review requirements for cross-border transmissions involving "important data." Although Manus has shut down Chinese services and blocked Chinese IPs, the early accumulated user interaction data had completed core model training - the data genes are etched into the model weights and cannot be retrospectively cleaned away. Data grown from Chinese users means the model carries a Chinese label.

4. Entrepreneurs in Specific Industries: Align Starting Now

The Safety Review Measures set a security review mechanism for foreign investments that may impact national security, focusing on defense security areas, and also important fields where foreign investment gains actual control, such as important information technology, key technologies, significant infrastructure, and important resources.

In the current regulatory environment following the Manus case, the following points deserve special attention:

First, the judgment of "actual control" in practice does not only look at equity ratios; if foreign investors can have a significant influence on a business's operational decisions, personnel, finances, technologies, etc. (e.g., having a veto right or key technology knowledge), they all fall within this scope. This definition is quite broad. For example, if you only hold 5% of the equity corresponding to a U.S. dollar fund, but that 5% comes with a veto right, it could be recognized as “having a significant influence on the business’s operations,” thereby classified as "actual control" and trigger a review.

Second, the National Development and Reform Commission, as the leading department of the work mechanism, has the right to make compliance window guidance based on national security assessments. For example, on April 24, 2026, the National Development and Reform Commission required certain AI companies to reject U.S. funding guidance; although this was not explicitly listed in the articles, it falls within the scope of "daily security review work and preventive management" as authorized in Articles 3 and 7 of the Safety Review Measures.

Third, it is not advisable to evade reviews through VIE, proxy holding, trust, etc. In practice, once an arrangement for avoiding review is identified, the enterprise might face risks of rectification, suspension, withdrawal, or other compliance measures.

Conclusion: The past "fence-sitting" gray pathways have been fully sealed off in all directions. From now on, enterprises must clarify their compliance position from Day 0.

Especially in the AI track, only one of the following two paths can be chosen.

Path A: Go the U.S. Funding Route - Completely Clean Exit

If you decide to take U.S. dollar funds, follow the Silicon Valley path, with the ultimate goal of being acquired or listed in the U.S. stock market, then what you need to do is not "bathe" but "exchange blood."

A hard standard: you cannot step on even one of the aforementioned four red lines.

Specifically, this means four things:

First, the founder must resolve their nationality. Holding a Chinese passport is itself a compliance risk label in the eyes of U.S. VCs. If you're determined to go down this path, renouncing Chinese citizenship is not an option; it is a prerequisite.

Second, do not take state assets. Any funding involving government guide funds, state-owned LPs, or policy bank loans should undergo thorough compliance penetration during the early financing stages, and may require withdrawal or repurchase if necessary.

Third, the code source must be abroad. This is the harshest and most critical point. The first line of core algorithm code must be completed outside China. The domestic team can only work on non-core modules or peripheral businesses. You need to establish a genuine abroad-based R&D center with solid capabilities from the start - not a shell, but an entity.

Fourth, data and users must be isolated from Day One. From the outset, do not touch Chinese user data. It is not a matter of "post-cleaning," but "never having owned it."

The precondition for taking this path is that you can bear the cost of being completely severed from the domestic market. You give up revenues, users, and brand synergies from the Chinese market. You are betting that the returns from globalization will sufficiently cover this cost. Moreover, even if you accomplish all of the above, you will still face an increasingly unfriendly America - the founder's Chinese identity remains seen as "original sin" by certain factions in Silicon Valley.

Path B: Go the Domestic Funding Route - Bind to the National Team

If you do not want to, or cannot go the U.S. funding route, then make compliance your moat.

The core logic is: Only on Chinese soil can Chinese capital thrive

First, actively embrace state and private capital. Prioritize accepting RMB funds, government guide funds, and central enterprise investment platforms during financing. This is not a forced choice; it is a strategic binding: having a state capital background is the hardest regulatory pass.

Second, make compliance a first-mover advantage. While others in the industry still try to find ways around it, you proactively declare security reviews, actively complete data classification and grading, and actively file technical exports. In the eyes of regulators, you are "one of them"; and in the eyes of the market, your compliance investment is a barrier that latecomers cannot catch up to in the short term.

Third, turn qualification certifications into licensing barriers. Certifications for x86 compatibility, data security capability maturity, and recognition of "specialized and innovative" in related technology fields - these are not costs; they are licenses. In a tightening regulatory environment, having a license versus not having one makes all the difference between life and death.

Fourth, proactively declare security reviews. According to Article 4 of the Foreign Investment Security Review Measures, foreign investment involving important information technology and key technologies must proactively declare before implementing the investment. For enterprises following the domestic funding route, this is not a burden; rather, it represents the best posture for signaling your position to regulators.

Taking this route, you accept the valuation logic and exit rhythm of RMB funds - rapid acquisitions of $2 billion may not be relevant to you, but you gain stable policy expectations and continued operating rights in the domestic market.

No Third Path to Growing Bigger

The wall-sitting model of "Cayman holding + Singapore operation + domestic R&D + U.S. dollar financing" has been sentenced to death. Continuing to hesitate on this path is not flexibility but danger. Regulators will not grant exemptions simply because you have yet to clarify your thoughts.

If you choose U.S. funding, follow cleanly. If you choose domestic funding, bind thoroughly.

This is the only operational manual left for AI cross-border entrepreneurs from the Manus case.

In Conclusion: The Butterfly Effect, a Prophecy Fulfilled

Manus named its parent company Butterfly Effect - reflecting the concept of the butterfly effect. Looking back at this name now, one can only exclaim that it has turned into a prophecy.

This butterfly flapped its wings twice, stirring up two storms. One was an acquisition invitation from Silicon Valley, and the other was a prohibition decree from Beijing. Now, the dual-strike momentum of regulation has taken shape, transforming the acquisition invitation into a compliance illusion, which will be recorded in the financing memorandums of every subsequent cross-border technology enterprise.

Reflecting on that "9-month exit with a $2 billion acquisition" perfect path, it was actually laced with triple compounding landmines from the very beginning:

- Technology Landmine: The moment the core AI code was generated within China, exposure triggered regulatory scrutiny;

- Data Landmine: Using data from China cannot be reversed;

- Identity Landmine: In this era, technology has nationality, and those who create technology also have nationality.

Follow the law and regulations, what was once a principle is now an ironclad rule.

Today's focus is not on convicting anyone, but on seeing a trend: the gray area of previously relying on registration locations, structures, and entity switches to maneuver is being consistently compressed. For founders, going abroad is no longer a game of “evading regulations beforehand, then patching compliance,” but rather, they must contemplate the entity, funding, technology, data, and declaration pathways clearly from Day 0.

May every founding team searching for a way out within the cracks of this era, whether you choose to fully commit to the U.S. funding track or delve into the domestic system, be able to recognize the rules, stand firm, and go further.

*This article is a subjective analysis by the editorial team based on publicly available information and industry observations, aimed at providing multidimensional perspectives for discussion. Any content in the article does not constitute legal opinions or investment advice. For any specific legal issues or business decisions, be sure to consult with licensed professional lawyers.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。