Key Points

This report is written by Tiger Research. The macro environment remains supportive, although the pace has slowed: global M2 hit a historical high of $13.44 trillion, and Bitcoin ETF flows turned to net inflow for the first time in 14 months. However, the oil shock triggered by the Iran conflict pushed March CPI up to 3.3%, narrowing the Fed's interest rate cut path.

Bitcoin on-chain indicators are shifting from undervaluation to early equilibrium: key on-chain indicators have moved out of the panic zone of the first quarter. The current price is $70,500, approximately 13% lower than the average entry cost for long-term holders of $78,000. Breaking this level would be a major signal for a short-term trend reversal.

The target price of $143,000 and the potential for a 2x increase remain valid: based on a neutral benchmark of $132,500, adjusted for fundamentals -10% and macro +20%. This is a downward adjustment from the $185,500 target in the first quarter, but the significant pullback in spot prices means the actual upside potential from the current price has instead increased.

Macro Tailwinds Still Present, but Momentum Has Slowed

Since the release of the first quarter report, Bitcoin has fallen about 27%, with April's average price hovering around $70,500. The Iran conflict introduced a new variable, but the overall macro environment remains favorable. It is not the direction that has changed, but rather the speed.

Liquidity at record highs, but not effectively transmitted to Bitcoin

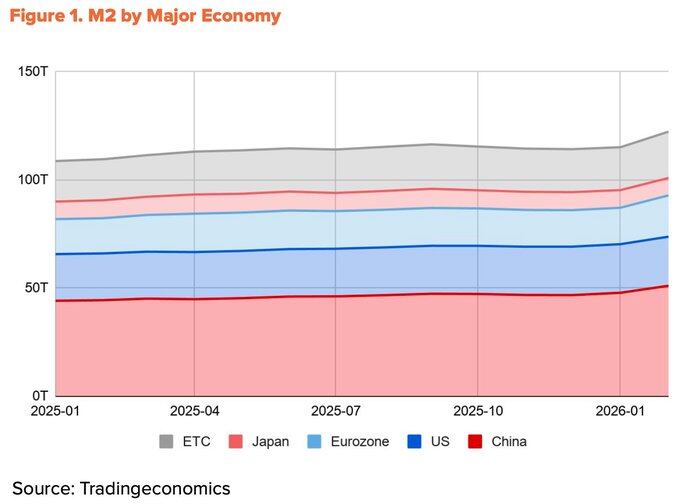

As of February 2026, global M2 continues to expand towards a historical high of nearly $13.44 trillion. However, Bitcoin has dropped 27% since the first quarter. Liquidity and price are exhibiting inverse movements.

The source of liquidity explains this divergence. Over the past year, more than 60% of M2 growth among the four major economies (China, the United States, the Eurozone, Japan) came from China, thanks to the People's Bank of China's reserve requirement cuts and the formal shift to an easing stance in the first quarter.

The contribution from the U.S. is only 10%. The issue is that the channels through which the liquidity from China enters the Bitcoin market are limited. Domestic crypto trading restrictions still exist, while indirect channels through Hong Kong and Singapore mainly serve institutional funds. Global liquidity is at a historical peak, but the share that can actually reach the Bitcoin market is shrinking.

Iran Conflict Slows Fed Rate Cut Pace

Due to hindrances in the transmission of liquidity from China, dollar liquidity remains a major driver of Bitcoin. However, even this has been delayed due to the Iran conflict.

Following the U.S. strikes against Iran on February 28, the Strait of Hormuz was blocked. Brent crude oil soared to $118/barrel in mid-March, and Dubai crude set a historical high of $166/barrel. This shock directly drove up inflation. The U.S. March CPI rose from 2.4% in February to 3.3%, marking a two-year high. Consequently, the Fed's room for rate cuts has narrowed. The March dot plot reduced the expectation for rate cuts in 2026 to only once.

Nevertheless, the direction of easing has not changed. In mid-April, part of the Strait of Hormuz reopened, and oil prices significantly fell back to around $90. Core CPI stabilized at 2.6%, indicating that the shock has not yet fully spread to the overall economy. President Trump officially nominated Kevin Warsh as the next Fed Chairman at the end of January, and the Senate confirmation hearing is ongoing. Powell's term will end on May 15, and the tendency for easing is likely to continue. The number of rate cuts may be reduced, but the direction remains unchanged.

Institutional Fund Flows Begin to Reverse

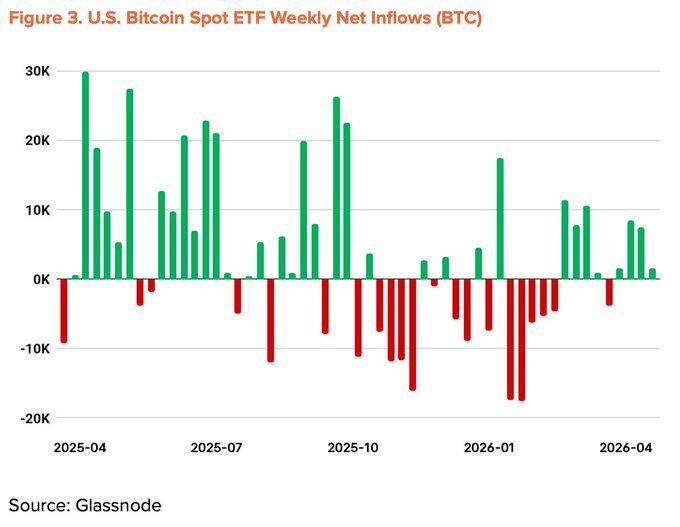

Institutional outflows that drove the first quarter decline have begun to reverse. Bitcoin spot ETFs recorded their worst monthly outflow since their launch in November 2025 and had been in net outflow for five consecutive months. However, since March, monthly net inflows have turned positive. As of mid-April, the cumulative capital flow for the year has turned positive, and total assets under management have rebounded to $96.5 billion.

Corporate coin-holding actions have also accelerated. Strategy invested $2.54 billion to acquire 34,164 Bitcoins in a single week (April 13-19), increasing total holdings to 815,061 BTC. However, the number of companies participating in this trend has not significantly increased.

Macro Indicator Adjusted to +20%

Structural tailwinds remain intact: liquidity expansion, a tendency for policy easing, institutional fund flows returning to positive, and the progress of the U.S. CLARITY Act. Recent headwinds—the oil shock triggered by Iran and the slowdown in Fed rate cuts—partially offset these positives. The macro indicators for the second quarter were adjusted down 5 percentage points from the first quarter to +20%.

From Undervaluation to Early Equilibrium

The on-chain indicators have moved out of the extreme panic zone and are transitioning towards the boundary of undervaluation and equilibrium. Key indicators such as MVRV-Z, NUPL, and aSOPR have left the panic area of the first quarter and entered the early recovery phase. While a significant surge similar to the rebound from the panic zone is unlikely, historical data shows that the average annual return starting from this area consistently remains in double digits. The current risk-reward ratio remains favorable.

Notably, the average cost basis of short-term holders (STH) is gradually declining. This indicates that speculative funds are exiting while new buyers accumulate at lower price points. The timing aligns with the resurgence of ETF net inflows and substantial purchases by Strategy, supporting the view that institutional investors are continuously accumulating in the discounted range, thus lowering the average entry cost.

The key risk level is $54,000, which is the overall network average cost basis. If this level is breached, the entire network will enter an unrealized loss state, becoming the bottom in extreme scenarios. The strongest resistance level is at $78,000, coinciding with the average entry cost for long-term holders.

The current price of $70,500 is approximately 13% below this resistance level, and a significant amount of recently entered short-term funds are in an unrealized loss state. A decisive breakthrough above $78,000 in the short term is worth closely monitoring.

Surface Growth, Underlying Stagnation

In the first half of April, Bitcoin's daily average trading volume reached 564,000 transactions, a year-on-year increase of 37.9%. While the surface data is impressive, the details tell a different story.

During the same period, the number of active addresses dropped to 428,000, a year-on-year decrease of 13.2% and a month-on-month decrease of 4.2%. The average transaction size dropped to 1.19 BTC, a 34.1% decline from the previous quarter's 1.80 BTC. While the number of transactions has risen, both participants and the value of each transaction are declining. This pattern reflects repeated small transfers by a few users rather than widespread economic utilization of the network. A significant portion of the growth in trading volume may stem from mechanistic flows such as exchange deposits, unrelated to real growth.

The first quarter report maintained the fundamental indicators at 0%, based on expectations for the expansion of the BTCFi ecosystem. Entering the second quarter, this argument has clearly weakened. According to The Block's "2026 Digital Asset Outlook," Bitcoin L2 TVL has dropped 74% this year, and total BTCFi TVL has decreased by 10%, now accounting for only 0.46% of Bitcoin's total supply (91,332 BTC). While some protocols like Babylon and Lombard have seen growth, the overall ecosystem has contracted.

Fundamental Indicators Adjusted to -10%

Surface growth has failed to translate into real network expansion, and the underlying data supporting the BTCFi argument has weakened. The balance of conflicting signals that previously offset each other has been broken. The fundamental indicators for the second quarter were adjusted down from 0% to the bottom line of -10%.

Target Price of $143,000, Still 2x Upside Potential

Using the TVM method, the neutral benchmark calculated at early April 2026 average price is $132,500. After adjusting for fundamentals -10% and macro +20%, the 12-month target price is set at $143,000.

This figure is about 23% lower than the first quarter target of $185,500. However, the actual upside potential has instead widened. Based on the average price, the upside has increased from +93% in the first quarter to +103% in the second quarter.

The downward adjustment in the target price does not imply pessimism. The macro direction and on-chain structure still support a medium to long-term bullish logic.

Three short-term observation points:

- A decisive breakthrough above the mid-term equilibrium level of $78,000;

- Continuous net inflow into ETFs;

- A shift in Fed policy following the easing of geopolitical risks.

If these three conditions are met simultaneously, the target of $143,000 remains achievable.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。