Last night, Nvidia's stock price briefly reached $70 during trading and surged 20% after hours, due to its latest earnings report exceeding everyone's expectations.

Intel disclosed its Q1 fiscal results for 2026 on Thursday, with revenue of $13.6 billion, a 7% year-over-year increase, exceeding Wall Street's consensus estimate by 11%. The non-GAAP earnings per share were $0.29, compared to analysts' expectations of $0.01, exceeding expectations by 29 times, which is an extremely rare discrepancy among large-cap stocks. Following the announcement, Intel's stock price rose 20% after hours.

The Q2 guidance also provided a more aggressive direction, with revenue expected to be between $13.8 billion and $14.8 billion, above the consensus estimate median. New CEO Lip-Bu Tan summarized the performance during the conference call with a statement indicating that CPUs are re-embedding themselves back into an essential foundational position of the AI era.

This is one of the most discussed topics in the market for Intel over the past two years, as the company was once believed to have completely missed the first wave of AI.

On one hand, it failed to produce GPUs that could rival Nvidia, and on the other hand, it struggled to keep pace with TSMC's advanced manufacturing nodes. However, in the past 12 months, as more AI deployments shifted from model training to inference and autonomous "agent" orchestration, the CPU, once regarded as a basic "computer brain," has found renewed demand. Intel's rebound this quarter marks the first financial realization of this technological narrative.

Data Center Business Makes a U-Turn

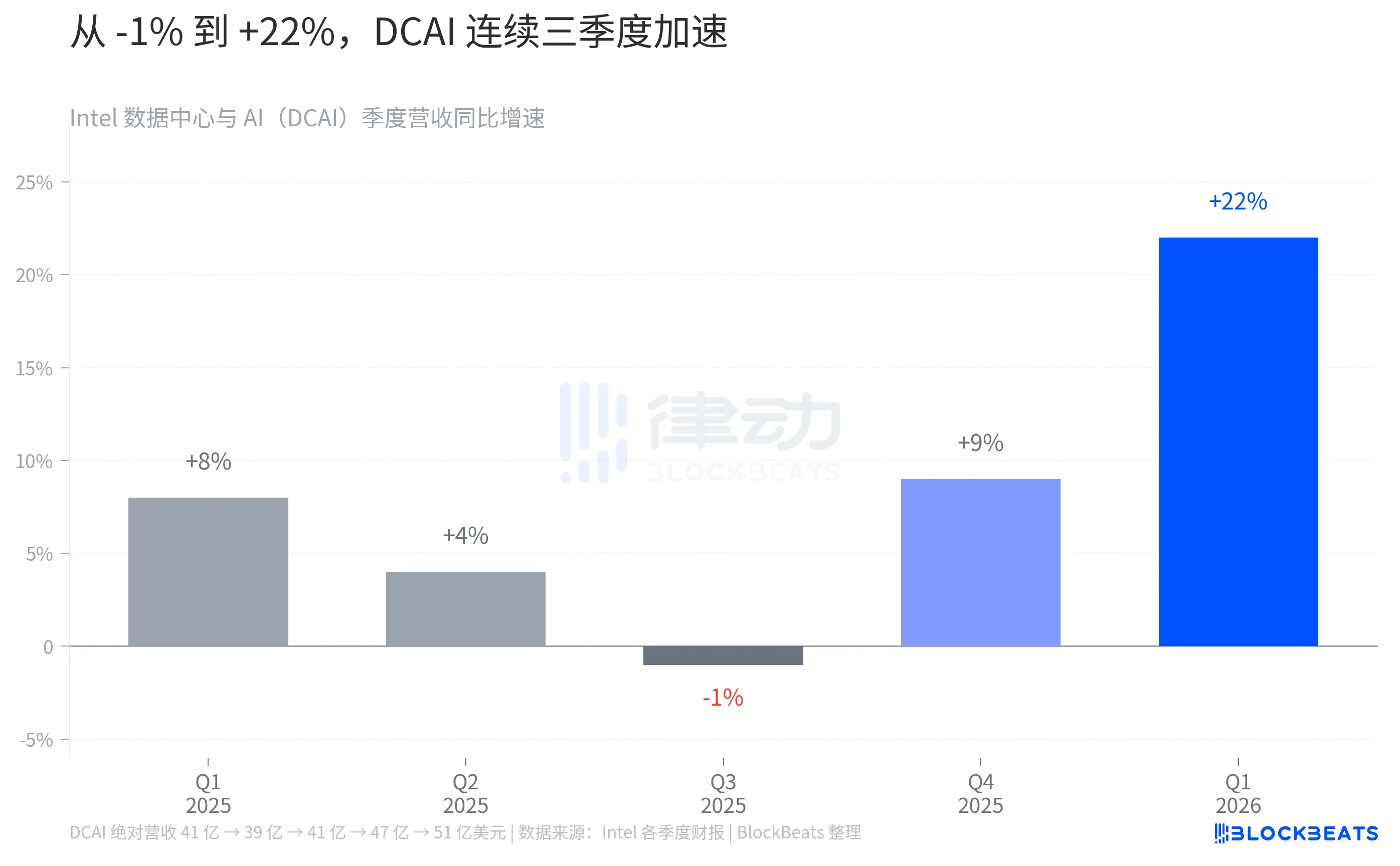

Breaking down Q1's $13.6 billion, the most significant change came from the Data Center and AI (DCAI) segment. According to Intel's earnings report, DCAI generated $5.1 billion in revenue for the quarter, a year-over-year increase of 22%, reaching an all-time high.

This is not a one-time surge. Looking back to 2025, DCAI's Q1 revenue was $4.1 billion, falling to $3.9 billion in Q2, and returning to $4.1 billion in Q3. This period of stagnation in mid-2025 led the market to doubt that the so-called "CPU recovery" was anything more than narrative. Then in Q4, according to Intel's disclosure compiled by Tom's Hardware, DCAI jumped from $4.1 billion in Q3 to $4.7 billion, a quarter-over-quarter increase of 15%, making it the fastest single-quarter growth rate for the company in a decade.

Entering Q1 2026, the $5.1 billion figure illustrated a clear U-shape curve, with the bottom reaching mid-2025 and the turning point established in Q4 2025, confirmed in Q1 2026. Management explained that the Xeon 6th generation "Granite Rapids" processors began to be produced at scale, combined with a refresh cycle in AI infrastructure. The company even voluntarily sacrificed some of its client CPU capacity, diverting wafers to the data center, thereby increasing the overall profitability of the DCAI segment. According to Intel's Q3 2025 earnings report, the operating profit margin for this segment rose from 9.2% in Q3 2024 to 23.4%, nearly a 2.5 times increase.

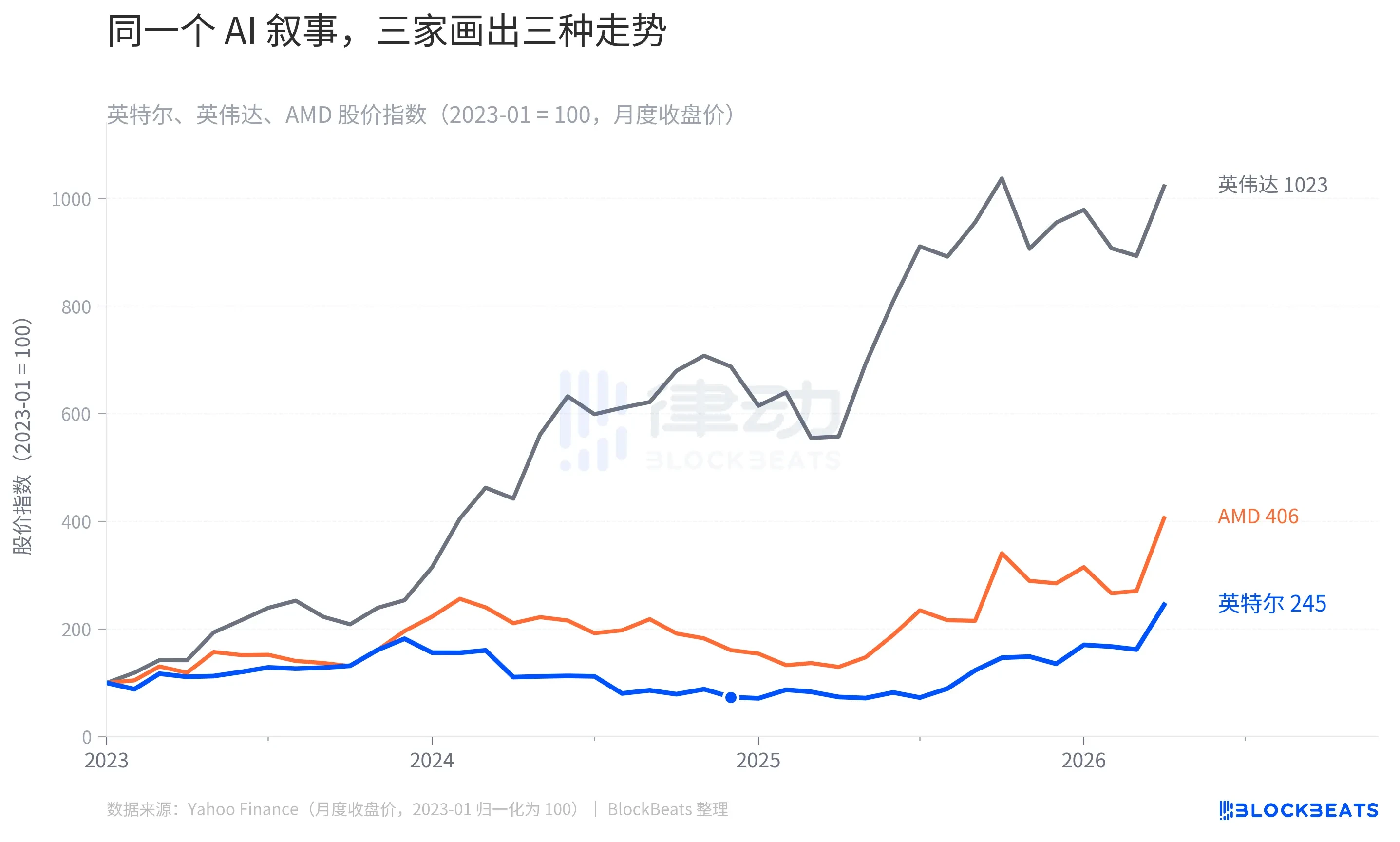

The Same AI Narrative, Three Companies Illustrate Three Trends

Comparing Intel's recent rebound with its peers reveals a more interesting picture than just price fluctuations.

Taking January 2023 as a benchmark, by April 2026, Nvidia's stock price index surged to 1023, AMD rose to 406, while Intel stood at 245. All three lines started from the same point, but the endpoint varied by nearly five times. What is more noteworthy is the shape of Intel’s blue line; it did not rise steadily but first dropped to 64 in September 2024 (a 36% decrease from the starting point), then formed a V-shaped rebound, finally catching up to 245 in early 2026.

This chart tells the story of the market's two pricing attempts regarding "who is actually making money in the AI capital cycle." From 2023 to 2024, funds flowed toward Nvidia because training required GPUs. AMD cashed in with its MI300 series and saw its stock rise accordingly. Intel, however, was systematically removed from the AI trade list due to disappointing Gaudi accelerator sales and delays in advanced process mass production. According to a third-party estimate cited by Fortune in January 2025, Nvidia's market share in AI chips rose from 25% in 2021 to 86% in 2024, while Intel dropped from 68% to 6%.

The second pricing took place from the second half of 2025 to early 2026, as the market began to reconsider a question: if AI moves from training to inference and agent phases, will the demand structure for computing power change? The answer to this question directly determines how far Intel's blue line can extend.

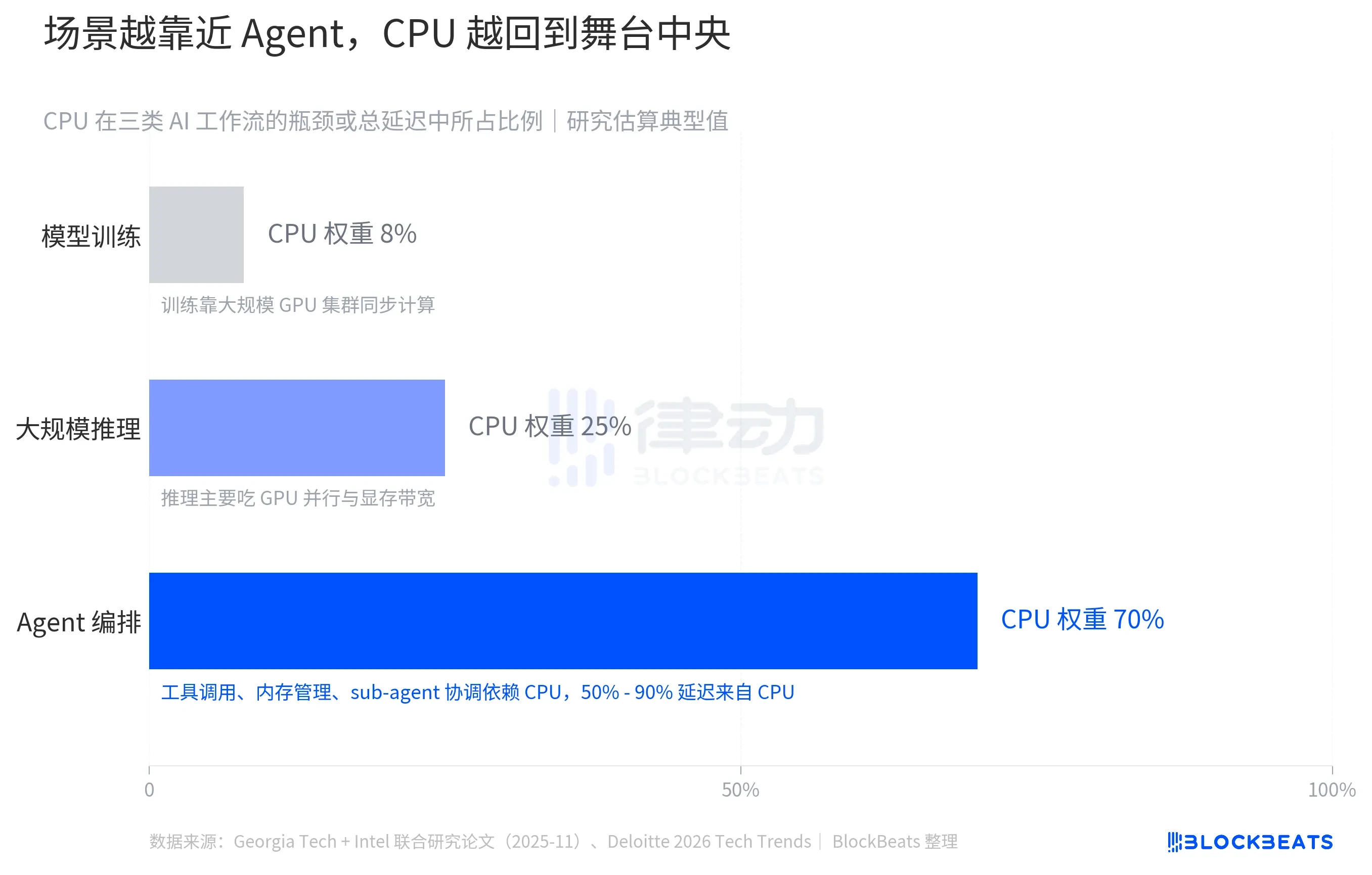

The Closer the Scenario to Agent, the More Central the CPU Returns

When breaking down AI workflows into three types of scenarios, the weight of CPUs within them varies significantly. According to Deloitte's 2026 Tech Trends report, during the large model training phase, the CPU accounts for only about 8% of the workflow bottleneck, with the remaining 92% of the computational load falling on parallel synchronization of GPU clusters, which is Nvidia's stronghold. As AI moves into large-scale inference, the CPU's weight rises to 25%, but the parallel throughput and memory bandwidth of GPUs remain bottlenecks.

Real change occurs in the agent orchestration scenario. A study co-published by Georgia Tech and Intel in November 2025 found that CPU processing for tool invocation in agent workflows accounted for 50% to 90% of the total delay in the entire process, with the specific ratio depending on the type of tool and the complexity of orchestration. In other words, when an AI agent is performing tasks such as "calling APIs, pulling data, coordinating subtasks, and managing context memory," the bottleneck is not in the GPU, but in the CPU.

This trend has measurable scale. Deloitte estimates that the proportion of inference workloads to total AI computational power is about 1/3 in 2023, approximately 1/2 in 2025, and expected to reach 2/3 by 2026. According to Futurum Group, the server CPU market size is projected to grow from $26 billion in 2025 to $60 billion by 2030, with a growth rate exceeding historical long-term averages. A more specific signal is the computational power roadmap disclosed by OpenAI, which plans to acquire "hundreds of thousands of cutting-edge Nvidia GPUs, as well as computing power scalable to tens of millions of CPUs to support agent workloads." GPUs remain dominant, but for the first time, the scale of CPUs is publicly placed on the same line.

The Rebound Did Not Start in Q1 2026

By overlaying Intel's stock price over the past five years with six key events, the 20% after-hours surge in Q1 is actually the culmination of a series of earlier decisions.

In February 2021, Pat Gelsinger returned to serve as CEO, unveiling the "IDM 2.0" strategy to transform Intel into both a chip designer and an external wafer foundry. In April 2024, when Gaudi 3 was launched, Intel set its AI accelerator sales target for 2024 at $500 million.

On August 2, 2024, the Q2 2024 earnings report bombshell revealed revenue of $12.8 billion, a year-over-year decline, with GAAP earnings per share at -$0.38, announcing a 15% layoff and suspending dividends, causing a single-day stock price drop of 26%, the worst single day since 1974. At that time, Intel disclosed that management later admitted the Gaudi 3 annual target could not reach $500 million, adjusting inventory downward by $300 million.

According to Intel's official announcement, on December 1, 2024, Gelsinger left, and the company entered a temporary co-CEO phase. In February 2025, the new management decided to cancel the independent GPU project "Falcon Shores," acknowledging that its self-developed AI accelerator path could not compete with Nvidia's ecosystem lock-in. On March 18, 2025, former Cadence CEO and semiconductor veteran Lip-Bu Tan officially became Intel's CEO. At that point, Intel's stock price was around $22, showing only a little over a 20% increase from its low of $18 in September 2024.

From Tan's appointment to the Q1 earnings report, Intel's stock price rose from $22 to $65 before the report, with the added 20% after hours meaning it just touched around $78. If the period from August 2024 to December 2024 was the darkest time for this company, then the real point of rebound did not start in Q1 2026 but at the moment of canceling Falcon Shores and appointing Tan as CEO. The company gave up the illusion of competing with Nvidia and returned to its true expertise in CPUs.

A 29 times EPS above expectations is a financial signal, but behind it, two things occurred simultaneously. The market began to reprice the CPU's position in the AI architecture, while Intel completed its leadership transition and product line adjustments. Both of these developments did not happen in Q1.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。