On April 21, Polymarket and Kalshi announced their entry into perpetual contracts on the same day. This synchrony is unlikely to be a coincidence.

The two platforms belong to different capital systems and user bases; Polymarket is backed by Peter Thiel and Silicon Valley venture capital, while Kalshi just completed its latest round of financing in March, achieving a valuation of $22 billion. Their usual competitive relationship cannot be described as harmonious. However, when the same external threat emerged, they almost simultaneously took identical defensive actions.

Polymarket's product went live on the announcement day, initially supporting BTC, NVDA, and gold, with a maximum leverage of 10 times. Kalshi will officially open on April 27, branding itself as "Timeless," relying on its CFTC DCM license and the margin trading permit obtained in March. Both are playing the same card: licensed compliance + a native user base in the prediction markets.

"Vertical Competition"

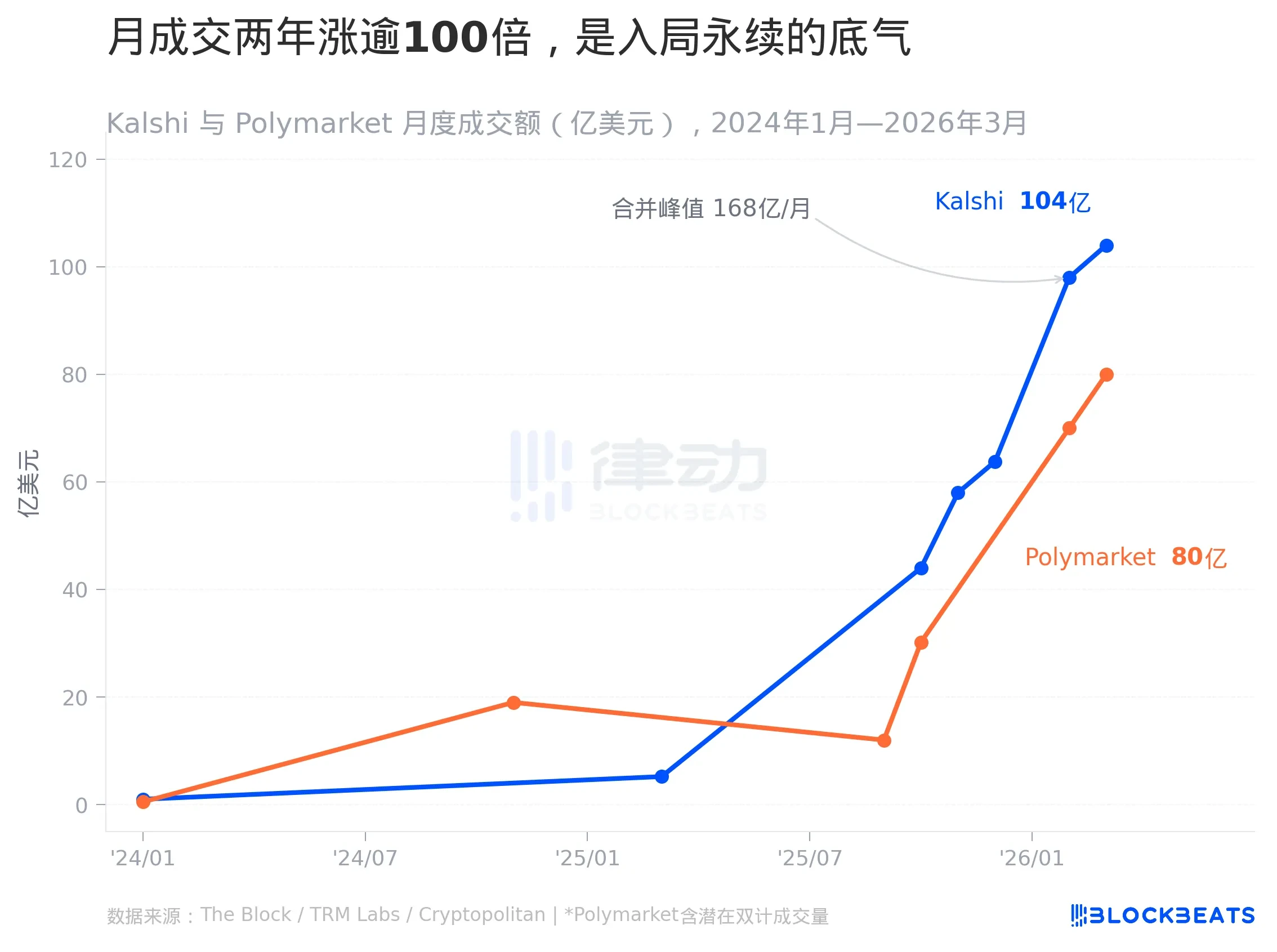

From early 2024 to March 2026, the monthly transaction volume growth curves for Kalshi and Polymarket are nearly vertical.

Kalshi’s monthly transaction volume in January 2024 was approximately $100 million. By March 2025, this number had risen to $521 million. By October 2025, it reached $4.4 billion. In March 2026, it exceeded $10.4 billion. In just over two years, it increased by more than 100 times.

Polymarket's pace is different but equally intense. During the November 2024 U.S. presidential election, its monthly transaction volume surged to around $1.9 billion, then receded after the election, but the platform subsequently found sustained vitality. In February 2026, Polymarket's monthly transaction volume reached $7 billion (according to The Block), and about $8 billion in March. Notably, Paradigm pointed out in its December 2025 report that Polymarket had issues with double-counting transaction volumes, indicating that the above figures should retain corresponding uncertainty.

The peak of combined transaction volume for the two platforms occurred in February 2026, totaling approximately $16.8 billion in monthly transactions.

This set of data gives Polymarket and Kalshi the confidence to enter the perpetual contract market. There is demand from users for such financial instruments, and the platforms have the capacity to maintain liquidity and user stickiness. This is a starting point that is difficult for any new entrant into the perpetual contract market to replicate.

The problem is that the time window is narrowing. The perpetual contract products from both platforms have some interesting differences in key dimensions.

Polymarket is following a crypto-native route. With 10 times leverage, initially supporting BTC, NVDA, and gold, its competitors directly target Coinbase and Hyperliquid. From the user structure perspective, Polymarket’s core users are crypto-native users who are not unfamiliar with perpetual contracts and have low migration costs.

Kalshi is leaning more towards compliance channels. It has already integrated with Robinhood, whose user base consists of U.S. retail investors accustomed to traditional financial products rather than crypto users operating on-chain every day. Kalshi's valuation has reached $22 billion, exceeding Polymarket’s $9 billion. Behind the higher valuation is greater market expectation, which requires opening up a market larger than the existing prediction market.

Both platforms hold the CFTC’s DCM (Designated Contract Market) license, which is a key qualification for legally providing leveraged derivatives in the United States. Compared to offshore exchanges, this license serves as their core barrier for U.S. users. Additionally, Kalshi obtained a margin trading permit in March this year, providing more complete regulatory conditions.

Is Hyperliquid the True Rival?

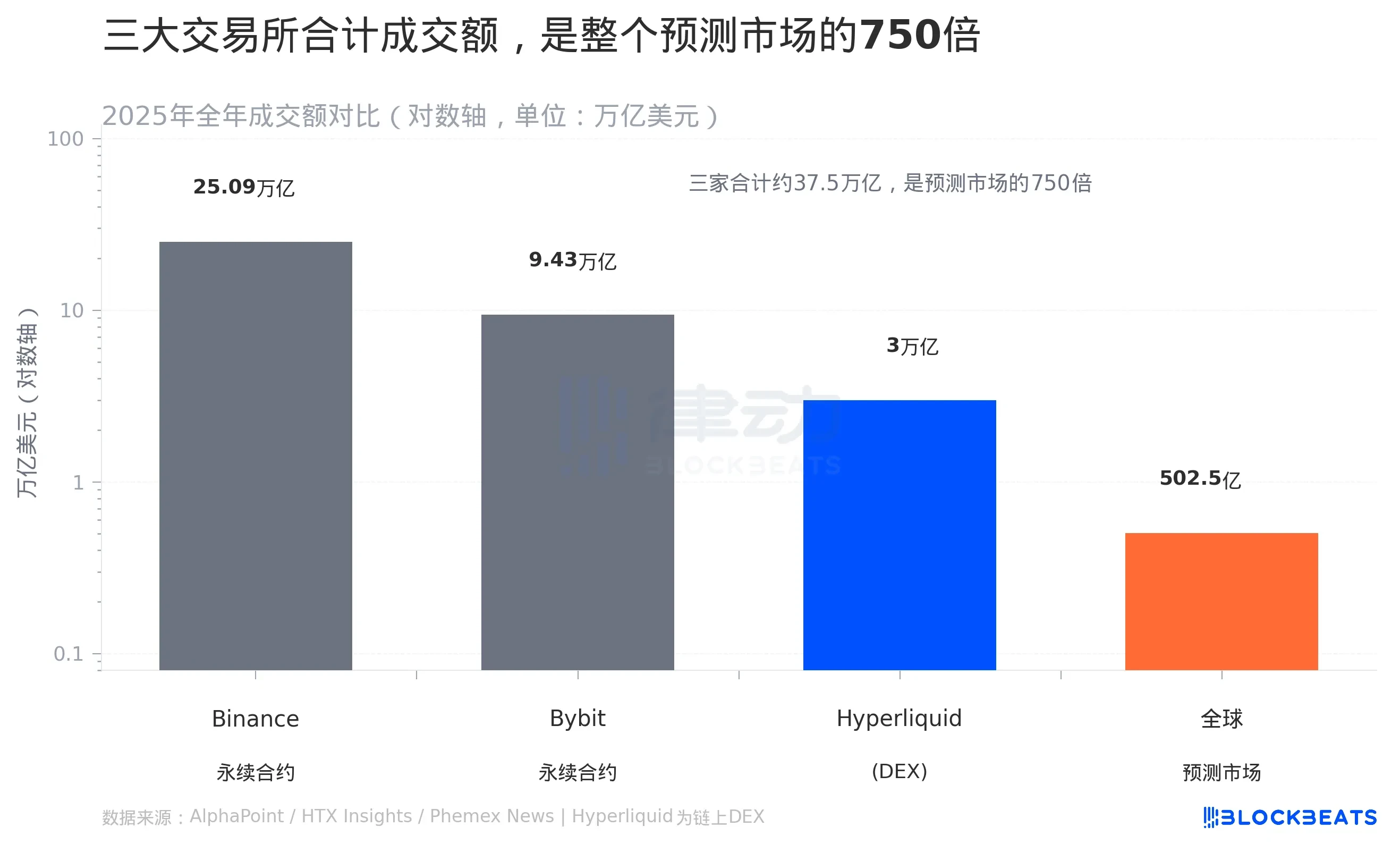

In 2025, the entire global prediction market's transaction volume was approximately $50.25 billion. This number seems substantial, but in the context of the perpetual contract market, it is merely background noise. Binance alone has an annual transaction volume of $25.09 trillion in perpetual contracts, Bybit has $9.43 trillion, and even on-chain DEX Hyperliquid recorded $3 trillion in 2025. Combined, these three make approximately $37.5 trillion, which is 750 times larger than the entire prediction market.

It’s not that the prediction market is insufficient; it’s that the two markets are currently not even in the same league. The market Polymarket and Kalshi aim to enter is three orders of magnitude larger than their current businesses.

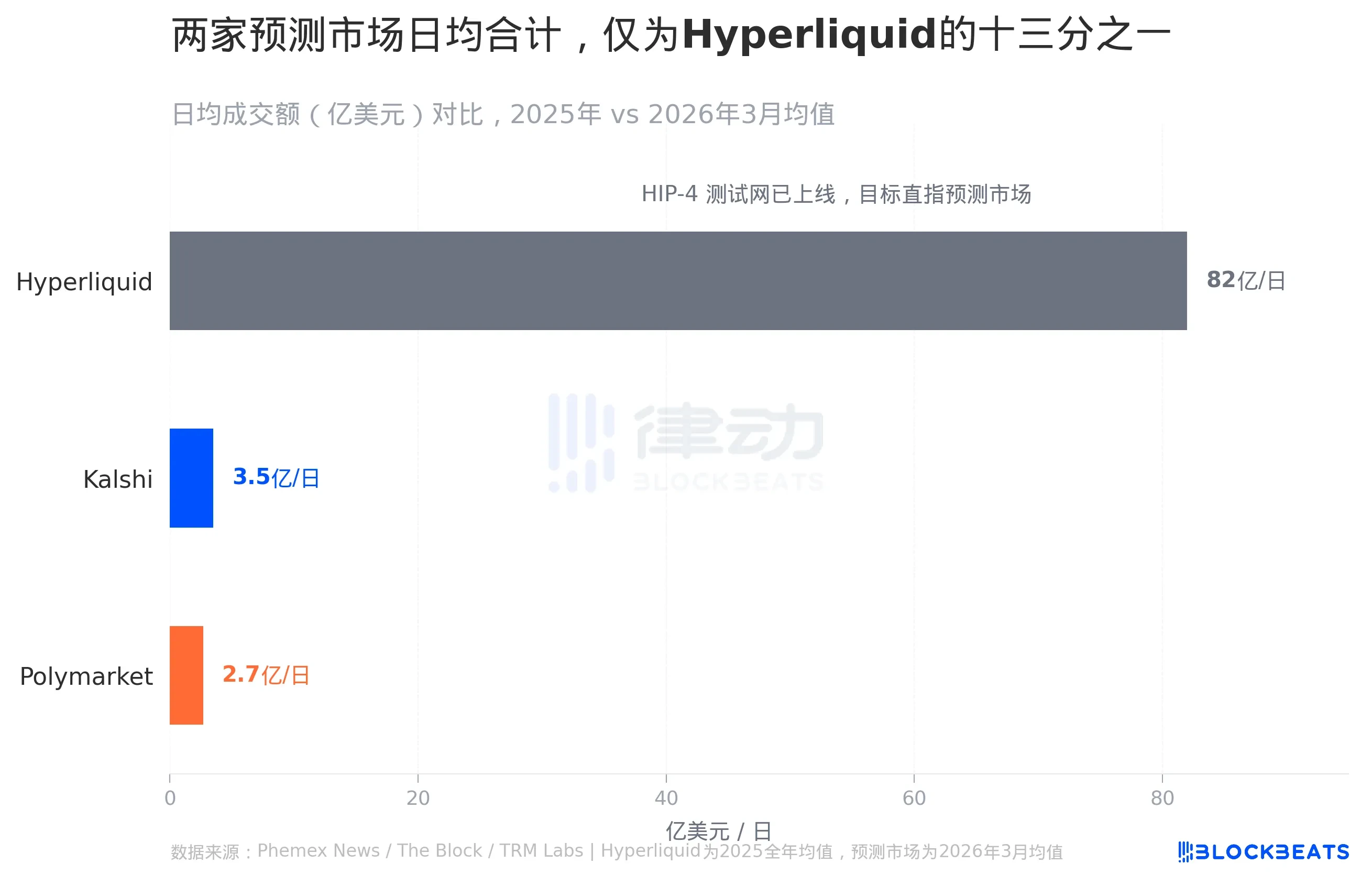

Furthermore, one detail underscores the issue: Hyperliquid’s daily average transaction volume is approximately $8.2 billion, equivalent to 80% of Kalshi’s entire monthly prediction market transaction volume in March 2026. In other words, Hyperliquid's daily volume nearly matches Kalshi's prediction market volume for an entire month.

They are well aware of this scale gap. They chose to enter perpetual contracts not out of a belief in going head-to-head with Binance but because another matter is unfolding.

Hyperliquid became the largest on-chain perpetual contract DEX in 2025 with a transaction volume of $3 trillion, holding about 38% market share in the decentralized derivatives space, with shares exceeding 70% at one point this year. This achievement has already put pressure on centralized exchanges. However, what makes prediction markets anxious is what Hyperliquid is doing additionally.

HIP-4, a protocol proposal from Hyperliquid, aims to allow anyone to issue perpetual contracts on Hyperliquid, including contracts based on prediction market events, such as election results, sports scores, and macroeconomic data. This directly targets the core user demands of Kalshi and Polymarket.

In numerical terms, the disparity is evident. Hyperliquid's daily average transaction volume is approximately $8.2 billion, while Kalshi’s prediction market daily average is about $350 million and Polymarket’s is about $270 million. Hyperliquid's volume is roughly 13 times the combined sum of the two.

However, transaction volume is not the only dimension. Hyperliquid’s users are crypto-native on-chain traders whose interest in prediction market events (elections, macro) is significantly lower than the policy-focused users of Kalshi or the gamblers of Polymarket. Whether Hyperliquid can build prediction market liquidity based on HIP-4 remains uncertain.

The current situation is that Hyperliquid wants to enter this prediction market domain, while Kalshi and Polymarket want to move into the perpetual contract space. Both sides have erected a sign at each other's gate.

Whoever can deepen liquidity first will have the voice. However, one thing is certain: before Hyperliquid HIP-4 is formally realized, Kalshi and Polymarket chose to take this step on the same day, not merely as a product launch but more like a positioning move. The combined monthly transaction volume of the two platforms has surpassed $18 billion, holding the only compliant leveraged derivatives brand license in the U.S., targeting U.S. retail users beyond the crypto-native circle. These conditions are temporarily unavailable to Hyperliquid.

The simultaneous launch of perpetual contracts by both prediction markets brings prediction market products into the same competitive arena as crypto derivatives for the first time, and the impetus for this timing has been a threat that has yet to fully materialize.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。