Written by: Prathik Desai

Translated by: Block unicorn

Stability may be an illusion. This is particularly common in finance. You bet on seemingly mundane financial instruments, believing they can provide stable and reliable returns. They may operate smoothly until their fundamentals start to falter. These seemingly safe investments are often more deceptive than speculative ones. People generally expect speculative investments to carry risks, but few anticipate that stable investments might do so as well.

About 75 years ago, we witnessed such a situation unfold.

In the 1940s, following the Great Depression and World War II, dollar-denominated deposits accumulated in European banks. This allowed account holders to place dollars in non-U.S. banks to hedge against local currency devaluation risks. These deposits offered attractive yields and led to innovative thinking. Some account holders, such as American companies, cleverly placed dollars offshore to evade domestic capital controls.

European banks welcomed all these deposits. They accepted these deposits and lent them out at higher rates. The excess of European deposits spawned the Eurodollar market, a parallel dollar system not regulated by the U.S. Federal Reserve. As the Cold War erupted in the late 1940s, the situation began to deteriorate. More and more people demanded to withdraw their dollars, but the banks lacked sufficient dollar reserves. The whole system collapsed.

We now see similar trades in the stablecoin market. However, it seems that digital dollar issuers have learned from history.

In today’s in-depth analysis, I will explain whether Ethena’s reliance on traditional stock markets can save its stablecoin reserve strategy.

Initial Behavior

At the beginning of 2024, Ethena launched USDe, a unique synthetic stablecoin. USDe is issued as an asset pegged to the dollar but does not actually hold dollar reserves. Instead, for every dollar of USDe issued, an equivalent amount of crypto assets like Bitcoin and Ethereum is held. At the same time, it shorts an equivalent amount of cryptocurrency futures.

These two positions offset each other. If the price of Bitcoin rises, the futures short position will lose the profits from the spot price increase. The reverse is also true. Ultimately, even if there are no actual dollars in the bank account, USDe always maintains a value of 1 dollar.

But why would people hold USDe instead of existing cryptocurrencies like USDT or USDC? Because holding USDe yields returns.

This incentive mechanism is specifically designed to adapt to how the cryptocurrency derivatives market operates. In bull markets, more traders bet on price increases. Exchanges charge these bullish bettors a small ongoing fee, known as the funding rate, and pay this fee to the other side of the trade. Ethena is always on the other side of the trade. It collects these fees and returns them as revenue to USDe holders.

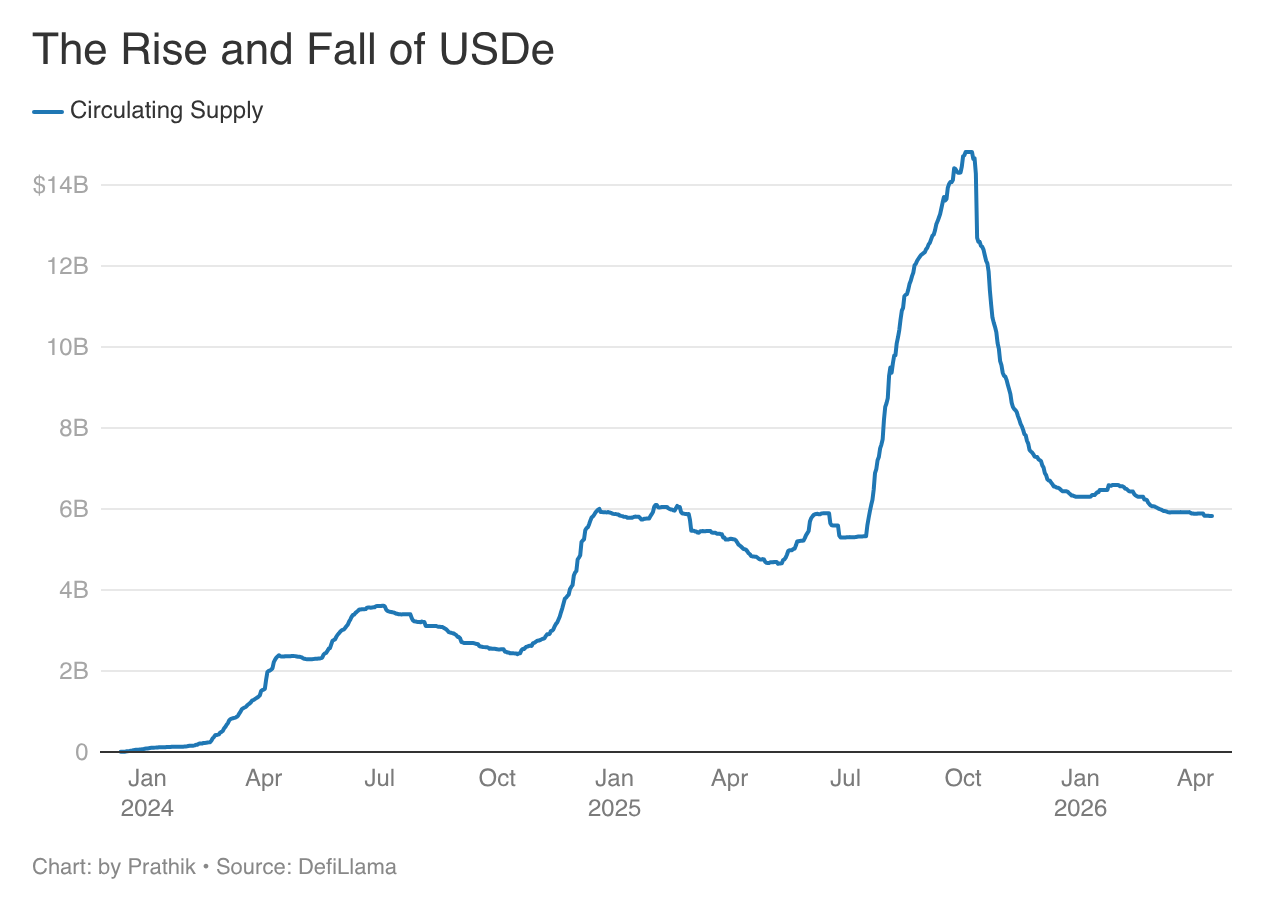

At its peak, the yield exceeded 20% annualized. Within just 18 months, USDe's circulation increased sevenfold, reaching about $15 billion, setting the record for the fastest growth ever of any stablecoin.

I like this design, but it relies heavily on the cryptocurrency market remaining stable. In a bull market, it is effective because the small number of investors holding short positions can profit, while the majority hold long positions. But markets change over time; this is inevitable. When the market changes, the cracks begin to appear. On October 11, the day after the largest liquidation in cryptocurrency history, which led to over $19 billion evaporating, USDe briefly lost its peg to the dollar. Ethena’s synthetic stablecoin fell to as low as $0.65 against the dollar on Binance.

Over the five months starting October 10, the circulation of U.S. foreign exchange reserves plummeted from around $15 billion to less than $6 billion.

A Lesson Learned Too Late?

Over $9 billion were redeemed. Perpetual futures once accounted for nearly 100% of the model's reserves but now constitute only 11%. Ironically, all of this could have been avoided. Ethena should have foreseen this scenario.

There are numerous signs that markets always cycle, and cryptocurrencies are no exception. We have witnessed this over the past 16 years. Relying on a single source of collateral (such as perpetual futures closely tied to market movements) is always a ticking time bomb.

Other stablecoin issuers have also begun to make adjustments. As the Federal Reserve started to cut interest rates, the top two stablecoin issuers increased their issuance to supplement their reserve income. Tether achieved reserve diversification by accumulating record levels of gold reserves. USDC issuer Circle is also actively building income sources through its Layer-1 network Arc and full-stack online payment system Circle Payments Network.

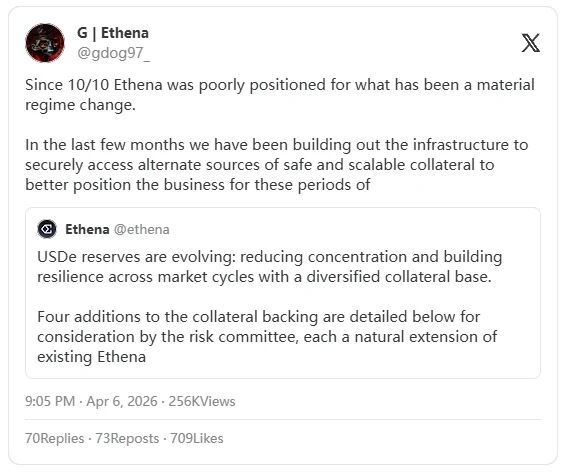

But Ethena has been slow to react. If it takes no action at all, the situation could worsen. This is not my personal view, but rather a statement acknowledged by its founder Guy Young in a post on X.

Guy also listed the measures Ethena is beginning to adopt to adapt to regime changes.

Traditional Financial Solutions

Ethena will expand its collateral base to include stock and commodity basis trading, over-collateralized institutional loans, prime brokerage services, and a broader array of real-world assets (RWA).

Ethena was originally conceived as a cryptocurrency-native synthetic dollar, unlike pioneers like Tether's USDT and Circle's USDC, which are backed by holding physical dollars or equivalent government bonds in their vaults.

For Ethena, fate seems to have come full circle. It is now reintegrating into the traditional financial system and continuing to generate returns for holders. Moreover, the sources of income are not just one but multiple.

Through stock basis trading, this strategy can earn the difference by going long in the S&P 500 spot while shorting its futures. This is similar to the strategy Ethena previously employed with BTC and ETH. The returns are modest but predictable and unaffected by cryptocurrency market volatility.

Now imagine Ethena performing similar trades across various asset classes: commodities such as gold, silver, wheat, and oil, indices, lending markets, and more. Each asset will have its price differentials, driven by supply and demand dynamics. Ethena can conduct Delta-neutral trading across all assets and earn spreads around the clock, without regard to retail sentiment towards cryptocurrency or Bitcoin.

While this reduces reliance on the cryptocurrency market, its current trajectory is still closely related to stock, commodity, or other asset markets. Each time these markets experience severe volatility or futures market liquidity dries up, these strategies may fail and further squeeze USDe's income.

But this pessimism equates to expecting a diversified portfolio of asset classes to also fail. Of course, that outcome remains possible but is extremely rare. However, that's how the financial world operates: it’s based on probabilities and mathematics. People do not expect to see breakeven points when the entire market is struggling. The purpose of diversification is to reduce the likelihood and extent of losses.

For Ethena, diversifying investments across uncorrelated sources of income can achieve the same effect. This will lower the risk of having its returns entirely squeezed when one or two categories of assets perform poorly.

The Liquidity Test

Ethena's diversification strategy is a reasonable solution to cope with market cycles. Spreading investment across stocks, commodities, credit, and cryptocurrency can enhance the stability of its income streams. This may be its only advantage compared to USDT and USDC, which are supported by government bonds since the latter do not pay any returns to holders.

But this new strategy still faces substantial resistance.

The liability portion of USDe has complete liquidity, meaning any holder can redeem at any time. However, assets that generate income may not have perfect liquidity during market pressure periods. Stock basis positions may take some time to close profitably. The terms of institutional loans are fixed. The liquidity of collateralized loan obligations (CLOs) is not always robust during market volatility. The gap between liquid liabilities and illiquid assets may pose a structural challenge for any yield-stablecoin. Even a diversified income strategy cannot close this gap.

In calmer markets, different asset classes may reflect different signals. Inflation concerns can drive up gold prices. Strong corporate earnings can boost stock markets. As we currently see, geopolitical crises involving oil-producing countries may elevate oil prices. With retail investors bullish on the cryptocurrency market, the financing rates for cryptocurrencies also remain high.

But under extreme stress conditions, their movements may not act as such. The correlation assumption may fail, offsetting the advantages of diversification. The commonality among all these assets is liquidity.

When the situation deteriorates across the board, everyone wants to cash out.

Harry Markowitz won the Nobel Prize for proving that diversification can reduce risk. However, the 2008 financial crisis provides sufficient evidence, without the need for a Nobel Prize, that there are exceptions to Harry's Modern Portfolio Theory (MPT). Nassim Taleb also presents a similar viewpoint in his work "The Black Swan." He points out that the correlations between assets are not constant but are a variable that changes with market conditions.

Despite these anomalies, it is important to recognize that these are inevitable and rare black swan events. Very few people can predict or control them. A diversified asset portfolio (covering multiple asset classes) can still outperform a concentrated investment in a single asset class. We saw this during the currency market collapse in 2008.

Due to more attractive spreads, reserve-level funds held short-term corporate bonds instead of government bonds. After Lehman Brothers collapsed, these bonds became worthless overnight.

Over-collateralization is one of Ethena’s measures to address this issue. If borrowers provide collateral exceeding the borrowing amount, theoretically, losses will be absorbed before affecting USDe holders. However, the over-collateralization rates are set based on historical volatility ranges. Stress events may surpass these ranges.

No strategy can completely evade risk. Ethena's mission is to inspire investor confidence, convincing them that its new diversification strategy is more advantageous than the previous model relying solely on cryptocurrency market dynamics.

That's it for today; see you in the next article.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。