Original author: Zhao Ying

Original source: Wall Street Watch

At 10 PM Beijing time on Tuesday night, the U.S. Senate Banking Committee will hold a hearing on Kevin Walsh's nomination as Federal Reserve Chair. This marks Walsh's first formal opportunity on Capitol Hill to systematically elaborate on his monetary policy propositions. Notably, Walsh has long criticized the enormous scale of the Federal Reserve's balance sheet, and this hearing may serve as an important platform for expressing his related views.

In fact, since the end of 2025, the trajectory of the Federal Reserve's balance sheet has been a core topic of great interest in the global financial markets. Against this background, Federal Reserve Governor Stephen Milan, along with three Federal Reserve economists, recently published a working paper titled "A User's Guide to Shrinking the Federal Reserve's Balance Sheet," providing a systematic explanation of the strategic logic and potential paths for the Fed's balance sheet reduction during a themed speech at the Miami Economic Club on March 26, 2026.

The core value of this paper lies in its ability to break common market perceptions. Previously, the market generally believed that "the ceiling for the Fed's balance sheet reduction is the exhaustion of reserves." However, the paper points out that the demand for reserves can be shaped by policy — through a series of regulatory and operational framework adjustments, the Federal Reserve can indeed achieve significant slimming of its balance sheet while maintaining a framework of "adequate reserves."

In response, the research team at Citic Securities subsequently conducted an in-depth interpretation. Their judgment is that relaxing LCR standards, reforming the SRP, and upgrading Fedwire are technically feasible options; however, proposals such as reserve tiering, reforming the TGA, and foreign reverse repo pools are relatively idealistic. Overall, the process of shrinking the balance sheet is unlikely to change the underlying logic of global central banks purchasing gold, and Citic Securities still maintains its prediction that the Federal Reserve will lower interest rates by 25 basis points in the second half of this year.

Why Reduce the Balance Sheet: Milan's List of Reasons

In his speech in Miami, Milan directly presented multiple reasons for reducing the Federal Reserve's balance sheet.

First, to reduce market distortions. An excessively large balance sheet creates unnecessary intervention in the funding markets, exacerbating the disintermediation problem in financial intermediation. Minimizing the Fed's "footprint" in the market is a basic requirement to maintain the market's price discovery function.

Second, to control financial risks. Large-scale asset holdings imply greater exposure to market value losses, while also increasing the volatility of Treasury profits (remittances). In recent years, the Federal Reserve has faced pressure from unrealized losses due to holding a significant amount of long-term securities, a problem that can no longer be ignored.

Third, to guard the boundary between monetary and fiscal policy. A huge balance sheet objectively leads the Federal Reserve to intervene in the allocation of credit resources, blurring the lines between monetary policy and fiscal policy. Furthermore, paying large interest on reserves to banks has been viewed by some members of Congress as a form of implicit subsidy to financial institutions.

Fourth, to retain policy ammunition. If the next zero lower bound crisis arrives, the Fed will need to expand its balance sheet to provide easing space. Currently compressing the balance sheet to a reasonable size is about preserving the necessary leeway for future policy maneuvering.

Milan candidly stated that many believe large-scale balance sheet reduction is "simply impossible." However, his judgment is starkly different: "Reducing the balance sheet is a manageable challenge; those who categorically deny it simply lack imagination."

Key Diagnosis: "Demand" Not "Supply" is the Constraint to Reducing the Balance Sheet

To understand this discussion, it is essential to clarify a long-misread logical structure.

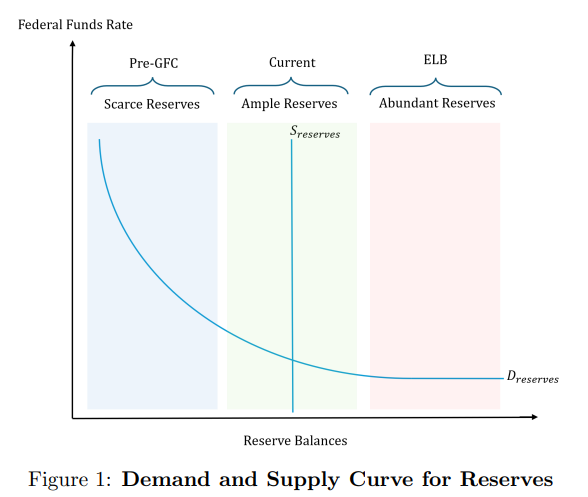

The traditional framework posits that the constraint on the Fed's balance sheet reduction arises when "the supply of reserves reaches the steep section of the demand curve" — once supply tightens to a critical point, overnight rates become uncontrollable. As a result, the Fed can only passively stop reducing the balance sheet when reserve levels drop to a "scarce" state. The "repo market shock" in September 2019 was a real-world manifestation of this logic.

The paper's breakthrough lies in shifting the focus from the "supply side" to the "demand side." It points out that demands for reserves are not externally determined constraints "naturally defined" by payment and settlement activities, but rather artificially elevated by regulatory rules, supervisory enforcement standards, and the Fed’s own operational framework — Milan calls this phenomenon "regulatory dominance" of the Fed's balance sheet.

Specifically, the following three mechanisms collectively raised the baseline demand for reserves:

1. Interest rate spreads turn reserves into "easy earn assets." Since the Federal Reserve began paying interest on reserves in 2008, reserves transformed from mere settlement necessities to assets that can compete with Treasury bills. Historically, there have been instances when the interest rate on reserves (IORB) exceeded the yield on 1-month/3-month Treasury securities, prompting banks to prefer hoarding reserves from a risk-return perspective.

2. Multiple liquidity regulations create a "ratchet effect." Rules such as LCR (Liquidity Coverage Ratio), ILST (Internal Liquidity Stress Test), disposition liquidity assumptions (RLEN), NSFR (Net Stable Funding Ratio), and SLR (Supplementary Leverage Ratio) are intertwined, creating a "robbing Peter to pay Paul" dilemma — changing one rule immediately makes another the new binding constraint.

3. Long-term "stigma" of the discount window. With high discount window rates linked historically to "troubled banks," and the risks of disclosure and regulatory scrutiny surrounding its usage, banks prefer to hoard reserves rather than utilize policy tools during periods of liquidity pressure. This same stigmatization logic extends to the Standing Repo Facility (SRP).

This diagnosis implies a fundamental policy path: there is no need to wait for reserves to return to a scarce state, but rather to lower the "scarcity-adequacy" dividing line, allowing the adequate reserves framework to operate normally under a smaller balance sheet.

How Much Can Be Reduced: A Quantitative Estimate of $1.2 Trillion to $2.1 Trillion

The paper uses data from the Fed's H.4.1 report on March 11, 2026, when the Fed's total assets were approximately $6.646 trillion. The breakdown of the liabilities side is as follows: reserves approximately $3.073 trillion, currency in circulation $2.390 trillion, the Treasury General Account (TGA) approximately $806 billion, and foreign reverse repo pool approximately $325 billion.

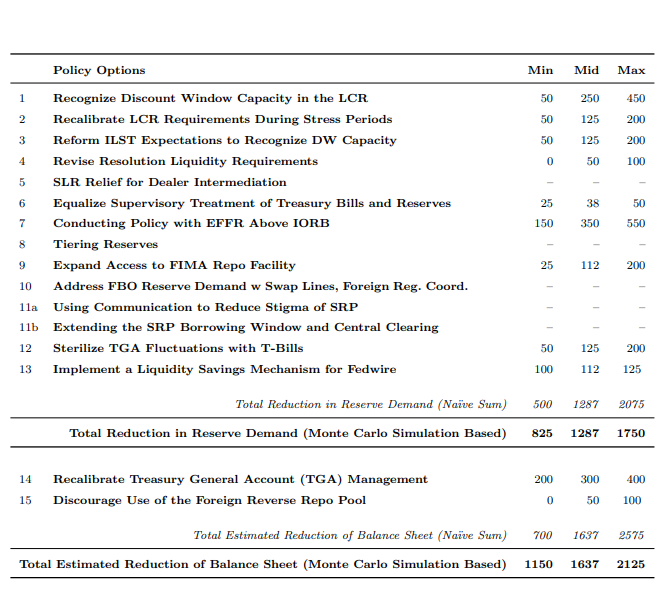

The paper conducts quantitative estimates around two main directions with a total of 15 policy options, but the key point is that it rejects simple summation. Due to the interrelatedness and substitutability of different policies, the paper employs a Monte Carlo aggregation method under the OMB A-4 framework to derive the following confidence intervals:

In his speech, Milan compared the above intervals with historical benchmarks:

- 15% of GDP: The level of the balance sheet after the end of the first round of QE in 2009, at which time the banking system could still operate normally;

- 18% of GDP (levels in 2012 or 2019): Reflecting the more clarified real liquidity demand of the banking system after the Basel reforms and the Dodd-Frank Act requirements became apparent.

The current Federal Reserve balance sheet is approximately 21% of GDP. According to the median estimate in the paper, if reforms progress smoothly, the balance sheet might fall to levels closer to those observed in 2012 or 2019. As for whether it can return to below 10% of GDP prior to the crisis — Milan clearly stated: "Unrealistic and unnecessary."

How to Reduce: A "Menu" Analysis of 15 Options

The paper categorizes the 15 policy tools into two main groups, providing estimates of effectiveness ranges and execution prerequisites for each.

First Category: Lowering Equilibrium Reserve Demand

(1) On the Regulatory Reform Level

LCR reform (Liquidity Coverage Ratio): The core measure is to allow banks to count the financing capacity corresponding to non-HQLA loans pre-collateralized at the discount window as HQLA, with certain limits set. The paper estimates the impact on reserve demand to be between $50 billion to $450 billion. The paper also cautions that if only the LCR is modified, the NSFR may immediately become the new binding constraint that needs to be addressed in a coordinated manner.

ILST and disposition liquidity assumption (RLEN): If regulators recognize the capabilities of the discount window and short-term liquidity sources, ILST reform could result in a decrease in reserve demand of $50 billion to $200 billion; extending the time window hypothesis for the discount window in the case of RLEN estimates a range of $0 to $100 billion.

(2) On the Supervisory Standards Level

If banks hold excess reserves to cater to examiner preferences (i.e., T-bills and reserves are not "equal" at the supervisory level), the adjustment magnitude is estimated to be $25 billion to $50 billion. This is a reform that does not require regulatory amendments, relying solely on a shift in supervisory culture; however, the difficulty of advancing it should not be underestimated.

(3) Reducing the Returns on Holding Reserves

Allowing the effective federal funds rate (EFFR) to exceed IORB, breaking the current state where EFFR has long been below IORB. The paper cites the Lopez-Salido and Vissing-Jorgensen (2025) framework to estimate that if "EFFR-IORB = +2bp" is taken as a reference (close to the levels seen during the pressure in September 2019), the corresponding decrease in reserve demand would range from $150 billion to $550 billion.

However, this path has obvious costs: the volatility of overnight rates and repo rates will significantly increase, and if the market responds by enhancing precautionary hoarding, the decline in demand might be partially offset. Pursuing this path requires supportive mechanisms, such as the SRP and temporary open market operations (TOMO).

(4) Enhancing the Attractiveness of Alternative Assets

Including upgrading the Fedwire system, enhancing liquidity in Treasury markets, and promoting central clearing, aiming to make Treasury bonds and other alternative assets attractive to banks, closer in appeal to reserves. These measures also assist in enhancing the capacity of the private sector to absorb the securities released during the Fed's balance sheet reduction.

(5) De-stigmatizing Fed Liquidity Tools

By alleviating concerns about using tools such as the discount window, standing repo facility, and intraday overdraft, banks' precautionary reserve requirements can be reduced. This requires systematic coordination from the Fed regarding transparency, pricing mechanisms, and regulatory communication.

Second Category: Directly Reducing Non-Reserve Liabilities

(1) TGA Management Readjustment

Reducing the Treasury’s cash buffer in the Fed's account from "about 5 days of operating funds" to "about 2 days," with the excess portion transferred back to the commercial banking system (similar to historical TT&L arrangements). The estimated reduction effect on the Fed's balance sheet is between $200 billion to $400 billion. The paper also acknowledges that the return of deposits to banks will correspondingly increase their demand for reserves, so the net effect is not straightforward.

(2) Reducing the Attractiveness of Foreign Reverse Repo Pools

By lowering interest payments and setting a size cap, directing foreign central banks and sovereign funds to shift funds from the Fed's reverse repo pool to the U.S. Treasury market. The estimated range is $0 to $100 billion, which is relatively limited in effect and depends on the willingness of external institutions to cooperate.

Walsh's Signals: From Technical Paper to Policy Expectations

Understanding this paper cannot disregard the personnel background at the Fed. The market widely expects that Walsh will take over as Federal Reserve Chair. Walsh has long criticized the Fed's balance sheet expansion policy since QE, repeatedly expressing a preference for reducing the balance sheet.

This working paper led by Milan has been viewed by the outside world as a forward-looking signal of the Federal Reserve's policy orientation in the future "Walsh era." The research team at Citic Securities points out that given Walsh's stance and the potential space revealed by this paper, there is indeed a possibility for the Federal Reserve in the "Walsh era" to gradually explore restarting balance sheet reduction.

However, both the paper and the speech repeatedly emphasize that the speed and rhythm are the most important constraints at the execution level. Milan concisely stated in his speech, "Once the preparatory work for the reforms starts, following the usual pace set by the government through the Administrative Procedure Act (APA), it is likely to take more than a year, or even several years." He referenced the SLR (Supplementary Leverage Ratio) reform, which took nearly six years from the temporary relaxation to the formal regulatory implementation.

This means that the Federal Reserve will not immediately restart balance sheet reduction due to the publication of this paper; the more likely path is to start research from less controversial, technically feasible options while providing the market with forward guidance on how new mechanisms will operate.

Citic Interpretation: What is Feasible and What is Idealistic

The research team at Citic Securities conducted a systematic evaluation of the 15 policy options from a practical feasibility perspective, yielding the following core judgments:

Options with Practical Feasibility:

- Relaxing LCR standards: This falls into the category of technical regulatory reform, with relatively controllable variables and a greater degree of initiative for the Fed;

- Reforming the Standing Repo Facility (SRP): De-stigmatization is more straightforward and does not involve external legislation;

- Upgrading payment systems like Fedwire: This constitutes a long-term infrastructure improvement with clear direction;

- Adjusting ILST supervisory standards: Some reforms require no legislative changes and can be advanced through shifts in supervisory culture.

Options that are More Aggressive or Require External Cooperation:

- Tiered interest on reserves: This may trigger non-linear responses in the banking system and is operationally complex;

- TGA management reform: This involves coordination mechanisms between the Treasury and the Fed, needing political consensus;

- Reducing the foreign reverse repo pool: Heavily reliant on the willingness of external institutions to cooperate, guaranteeing limited effectiveness.

Overall, Citic Securities considers this to be "a practical reform menu worth considering," but the actual implementation progress will be far slower than the potential upper limits represented in the paper and should be viewed as directional guidance rather than a commitment to near-term policy.

Market Impact: Increased Volatility, but No Change in Interest Rate Logic

Regarding the impact on the bond market, the essence of the Fed reducing the balance sheet is to decrease the issuance of base money, which will inevitably increase the scale of U.S. Treasuries that the private sector needs to absorb. Citic Securities believes this will amplify market volatility, resulting in greater tail risks — despite some regulatory easing measures (such as SLR relaxation) helping to broaden the capacity of dealers to absorb.

In terms of timing arrangements, the paper clearly opposes speeding up balance sheet reduction through direct sales of securities; a more feasible way would be to let maturing securities naturally roll off the balance sheet while providing dealers and the repo market with higher reserves of absorption capability. This objectively limits the short-term intensity of the balance sheet reduction's impact.

Citic Securities predicts that U.S. Treasuries are currently more suitable for trading opportunities, with short bonds likely outperforming long bonds.

As for the stock market, the impact of balance sheet reduction can produce a contraction effect on the real economy through both monetary supply and portfolio balance effects, but it can be offset by lowering the federal funds rate. Citic Securities believes that if balance sheet reform progresses, the necessity for adjustments in the interest rate path will increase, but this has limited direct connections to the current monetary policy pace. U.S. stocks may await a pullback window to look for thicker safety margins.

Regarding the gold market, balance sheet reduction reforms are unlikely to materially change the strategic logic of global central banks increasing their gold holdings, which are more driven by geopolitical restructuring and trends towards diversifying dollar reserves. Gold still holds medium-to-long-term allocation value.

Milan explicitly pointed out in his speech that the contraction effects generated by balance sheet reduction can be countered through interest rate cuts, and "reducing the balance sheet may expand the decline in the federal funds rate relative to benchmark scenarios." Citic Securities expects the U.S. CPI to oscillate within the range of 3.0% to 3.5% year-on-year this year, and continues to maintain its prediction that the Federal Reserve will cut rates by 25bps in the second half of this year, indicating no direct binding relationship between balance sheet reform and interest rate decisions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。