Original | Odaily Planet Daily (@OdailyChina)

Author | Wenser (@wenser 2010 )

Recently, the once-popular "internet-famous shoes" Allbirds announced it would sell its footwear business and raise $50 million to transform into an AI computing infrastructure company called NewBird AI. Upon the news, its stock price surged, reaching as high as $24.31, and has since fallen back to $16.99, with a daily increase still maintaining a terrifying 582.33%.

Upon reflection, $50 million is a drop in the bucket in the AI computing race, where orders often reach tens of billions of dollars. However, this move reminds me of the soaring stock prices of DAT companies (Digital Asset Treasuries) last year in Q3.

The era when a news of a transition to DAT could cause a listed company's stock price to skyrocket has ended, and we are entering a new era of "public companies transforming into AI computing sellers". The reason is simple, rooted in the "supply and demand" dynamics.

Behind the Shift from Internet-Famous Shoes: AI Computing Gap is a Major Problem

Recently, events like the decline of the Claude model's intelligence and tightening KYC policies have sparked extensive discussions, reflecting the structural gap in AI computing.

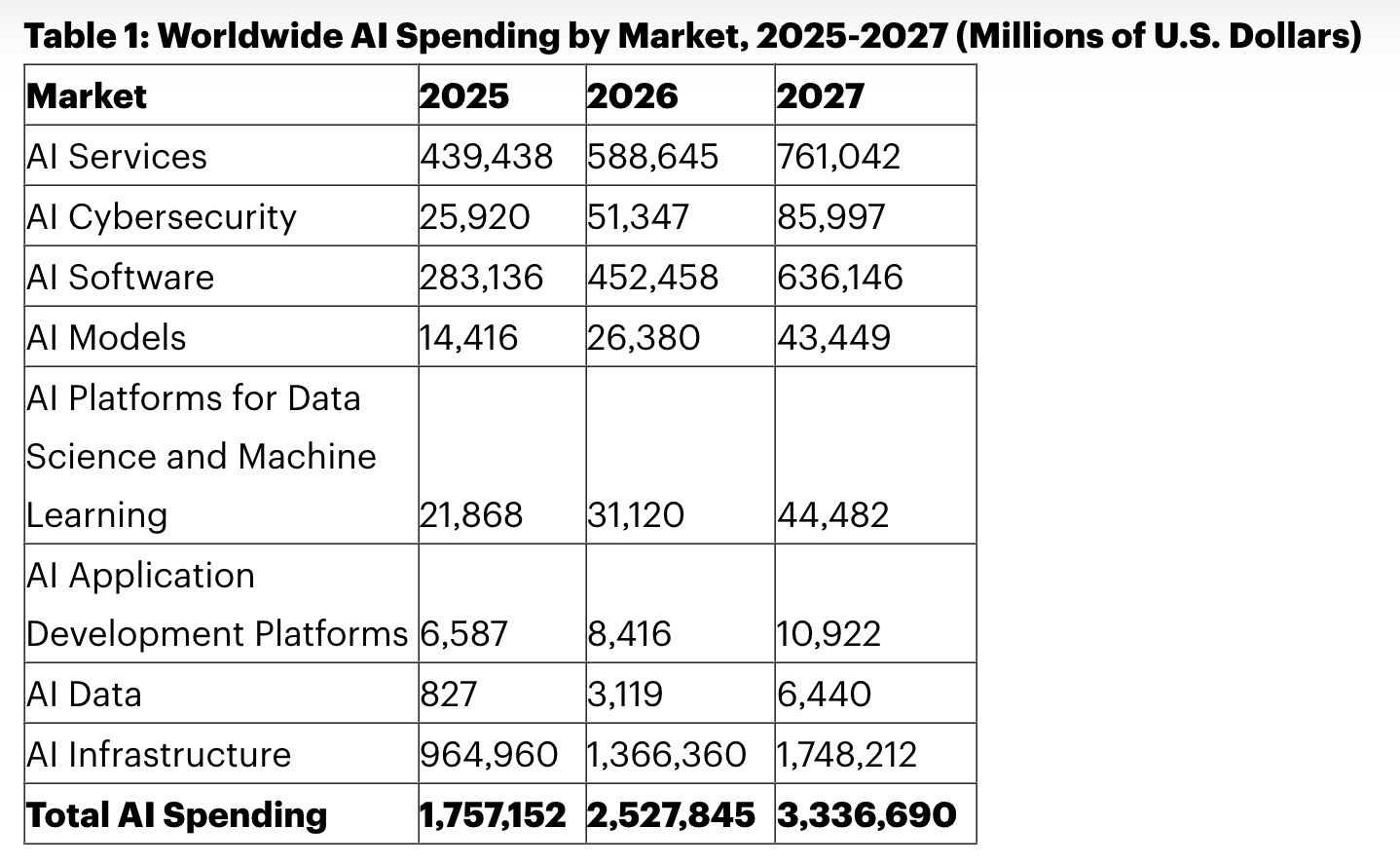

A report from US market research firm Gartner indicates that global AI spending will reach $2.52 trillion by 2026, a 44% year-on-year increase; of this, AI infrastructure (including servers, accelerators, storage, and data center platforms) is expected to consume about $1.37 trillion, exceeding half of total spending.

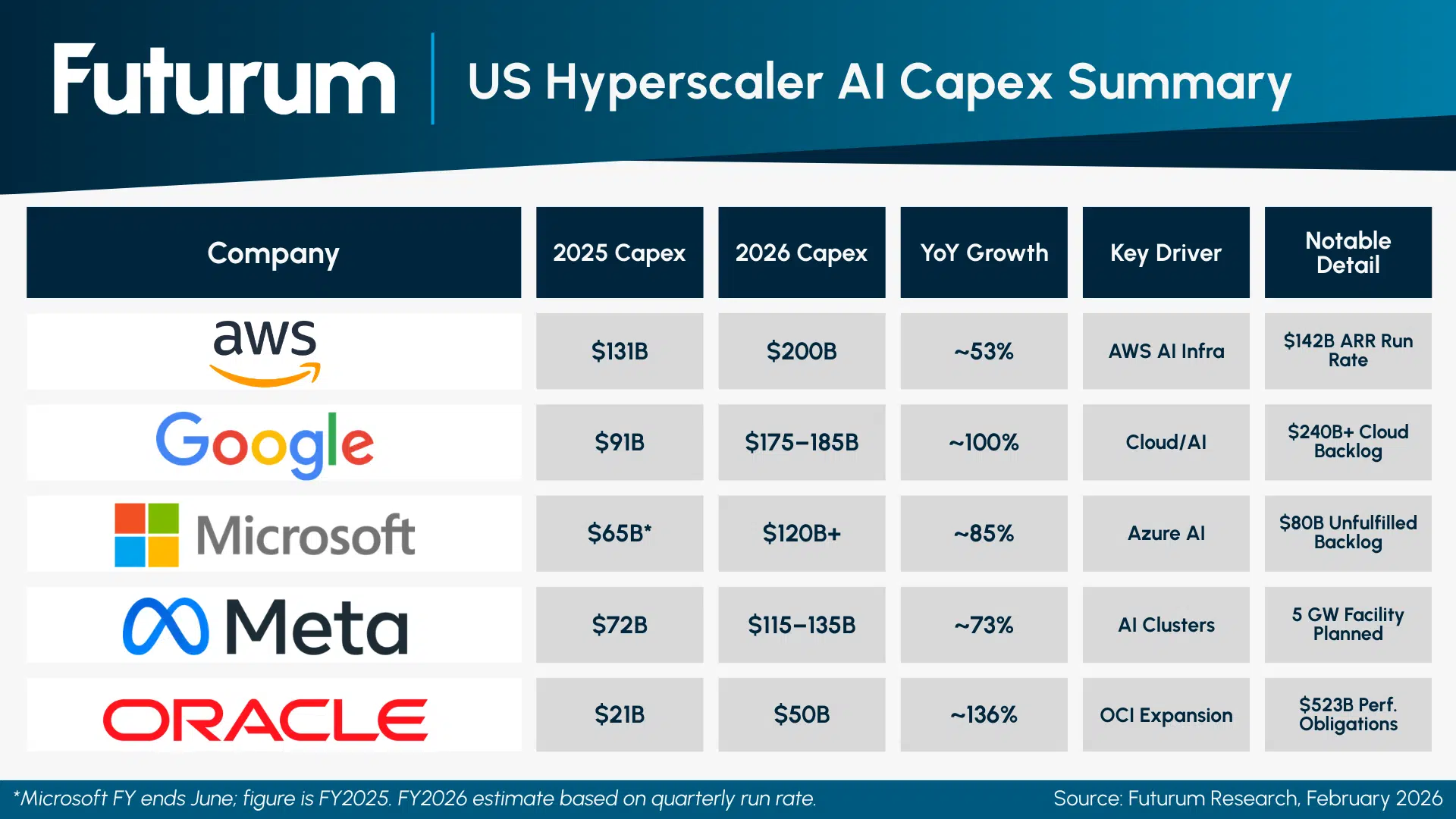

On the side of AI giants, Microsoft, Alphabet (Google's parent company), Amazon, Meta, and Oracle plan to spend a total of about $66 billion to $69 billion on infrastructure capital expenditures in 2026, about double that of 2025; the vast majority of this funding will go toward AI computing, data centers, and networks. All major cloud providers have indicated that their markets are experiencing a supply shortage.

Considering the delivery cycle for GPU data centers is about 36 to 52 weeks, the constraints on computing power and data supply are likely to last at least until Q3 of 2026.

It is worth mentioning that the current structural gap in computing power arises not only from the demand for training various models by large AI model vendors but also from the rapidly expanding demand for model deployment from billions of users worldwide. The gap in computing resources between B2B and B2C businesses contributes to the current situation of supply often falling short of demand in the computing power market. It's no wonder that NVIDIA founder Jensen Huang confidently stated at this year's CES: “(NVIDIA's) AI chip and infrastructure market might reach $1 trillion by 2027.”

Apart from the gap in computing resources, the alignment of many mining companies transforming into AI computing and data centers coincides with the competition for critical resources like electricity between AI and the cryptocurrency industry. According to a recent 2026 AI Index Report published by Stanford University, current AI systems' overall electricity demand is close to half that of Bitcoin mining, approaching the total electricity consumption of Switzerland or Austria.

There is no doubt that as AI becomes the only narrative driving US stocks and global tech companies, being "related to AI" has become a must for many listed companies.

When AI Computing Becomes the Next DAT Model: A Moment of Robustness Testing for AI Narrative

What Allbirds has sparked may be another wave similar to the surge of DAT companies last year.

This judgment stems from the overlapping areas between the DAT treasury model in the cryptocurrency industry and public companies transforming into AI, with several mature cases already existing.

Last July to September, with the emergence of Ethereum DAT companies like Bitmine and Sharplink, a large number of BTC DAT, ETH DAT, SOL DAT, BNB DAT, and various altcoin DAT listed companies became the "star stocks" of the time - many stocks doubled or even multiplied by several times within just a few days.

On the other side, there are also remarkable cases of transformation in the AI sector.

Last year, Axe Compute (formerly Predictive Oncology Inc.) performed a dramatic transition to AI computing, utilizing Aethir (ATH) as DAT reserve assets. Previously, the company’s main business was medical equipment, and it had explored services like a tumor drug response prediction platform and 3D cell culture models to support cancer treatment drug development. In September last year, the company initiated the ATH token DAT strategic transformation, and its stock price surged nearly 200%; after completing over $340 million in funding, it officially announced its transformation into a GPU computing infrastructure company, changing its stock code to AGPU.

Now, CoreWeave (CRWV), which has established partnerships with chip giants and AI leaders like NVIDIA and Anthropic, is also a participant in the "AI fast track." As an old mining company, CoreWeave's transformation over the past nearly three years of rapid AI development has been quite thorough: initially, it signed a $22.4 billion infrastructure contract with OpenAI; last year, it again signed an AI agreement worth $1.17 billion with Vast Data, which is funded by NVIDIA; recently, it reached a data center leasing agreement with Anthropic. According to financial reports, CoreWeave's revenue in 2025 is projected to be $5.13 billion, a 168% year-on-year increase; it plans capital expenditures exceeding $30 billion in 2026, and as of the time of writing, its market capitalization is about $62.4 billion. For more information, it is recommended to read “Analysis of CoreWeave: From Cryptocurrency Mining Company to AI Cloud Service Provider”. As for the AI transformation of other mining companies, there are numerous cases. See “The Great Migration of Mining Companies: Some Already Hold $12.8 Billion in AI Orders”.

Of course, compared to the tens of billions of dollars in orders for mining companies, Allbirds' financing amount is relatively small. Furthermore, from the perspective of actual purchasing power, compared to high-performance GPUs that cost $25,000 to $40,000 each, $50 million can barely acquire fewer than 2,000 GPUs; however, some analysts believe its positioning might be as an acquisition target for a large "alternative cloud" company to go public.

In other words, Allbirds' internet-famous shoes label has been torn away, while the "AI concept stock" label has become highly sought after. Its true value lies not in how many GPUs $50 million can buy, but in retaining a Nasdaq-listed company shell — which is attractive for AI infrastructure companies wanting to quickly enter the public market.

Finally, although from a capital operation perspective, the AI computing business model is quite similar to last year's DAT treasury model, there are still certain differences in the following aspects:

Firstly, the real business revenue in the AI industry compared to the cryptocurrency industry. According to a previous statement from Anthropic, its annualized revenue has exceeded $30 billion, while this figure was still $9 billion in 2025; moreover, as of February, OpenAI's annualized revenue has surpassed $25 billion. Although valuations reaching hundreds of billions of dollars are high, the true business revenue is a more stable data underpinning compared to the volatile token market capitalizations. Various large model companies are the best buyers in the AI computing business, as the shortage of computing power is an objective reality.

Secondly, the high operational threshold of the AI computing industry. Unlike the "hoarding coins" strategy of DAT treasury companies, the AI computing business is not merely about purchasing GPUs; it requires the establishment of an entire operational chain including data centers, electricity, cooling solutions, networking, operational teams, and client acquisition, thus the barriers to entry, sustained cycles, and team requirements are higher, making it relatively harder to "fake." At its core, the underlying assets of DAT are financial assets; while the underlying assets of AI computing companies are operational physical assets.

Thirdly, the sustained cash flow of the AI computing industry. For DAT treasury companies, whether it is BTC, ETH, or altcoins like SOL and BNB, their main revenue relies heavily on price fluctuations (staking income can be considered minimal), without any regular business revenue; the AI computing business can generate continual cash flows through long-term leasing agreements, providing actual cash inflow.

Of course, from the perspectives of financing structure, reverse mergers, and speculative sentiment, the two still exhibit high similarities; and regarding the potential for regulatory scrutiny and pressure, companies wishing to transform into AI computing firms will inevitably face various restrictions and ongoing attention.

Just like after Allbirds' stock price soared, industry insiders expressed their views:

- FifthVantage CEO Matt Domo believes that Allbirds' AI transformation is more of a means to boost its sluggish stock price, and investors should be wary of "AI washing," where some companies attempt to exaggerate or even fabricate their AI capabilities for marketing purposes. Additionally, companies attempting to grab onto hot trends through aggressive transformation is not without precedent; many companies tried to board the blockchain bandwagon from late 2017 to early 2018;

- Jason Schloetzer, an associate professor at Georgetown University's McDonough School of Business, pointed out that the initial $50 million in financing is "negligible compared to the actual investment required to become such a service provider," but from a more optimistic perspective, the influx of many new players into the AI field may reflect ongoing market enthusiasm for growth;

- Seaport Research analyst Jay Goldberg stated that it is hard to imagine a company like Allbirds, which has ventured into the field halfway, being able to offer competitive products or services.

In the current roaring train of the AI era, there are always those who are desperately trying to cling to the doors and fight for a chance. Whether they can stay on the train or be swept away by the whirlwind remains to be seen.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。