Core Summary (TL;DR)

- In this cycle, the arbitrage space for funding rates on mainstream crypto assets has been completely squeezed out by institutional futures and spot arbitrage funds.

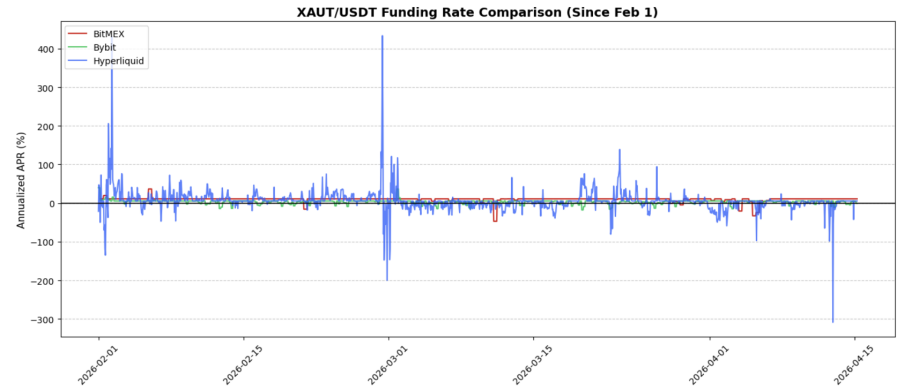

- On the XAUtUSDT trading pair, over the past 73 days, a simple "spot-perpetual contract" arbitrage on BitMEX achieved an annualized yield of about 9.67%, compared to 5.99% on Hyperliquid and 3.22% on Bybit.

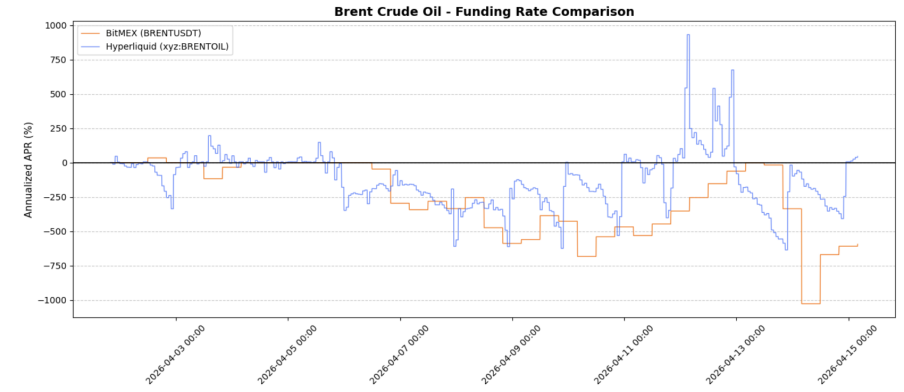

- The profit margins for Brent Oil are even richer: going long on BRENTUSDT on BitMEX and shorting Brent on Hyperliquid achieved an implied annualized yield of approximately 361.6% over 7 days, 220.7% over 14 days, and 103.0% over 30 days.

- Today, better opportunities lie within BitMEX's TradFi perpetual contracts—where asset updates, fund flows are still immature, and the dislocation in funding rates remains sufficiently large to be profitable.

Mainstream Crypto Arbitrage Is No Longer Attractive

For most of cryptocurrency history, funding rate arbitrage on mainstream perpetual contracts has been one of the purest trading opportunities in the market. The script is simple: buy spot, short perpetual contracts, maintain delta neutrality, then collect interest. This strategy worked because the long-term demand for leverage skewed towards the bulls, the funding rate mechanism itself structurally favored the long side, and market efficiency was still low enough to keep these spreads enticing for a long time.

But now the situation has changed. Since 2025, the drop in funding rates for mainstream coins has been extremely severe, most notably, larger market cap coins have been impacted more severely. This indicates that the old trading logic has not collapsed structurally; it has merely been "rolled over" by a wave of arbitrageurs. The easy profit opportunities have been devoured by hedge funds, basis desks, and large structured players, who now view crypto asset arbitrage entirely as a balance sheet business for big capital. Once funding rates rise to levels worth harvesting, large funds rush in and smooth them out. As a result, today's funding rate returns are no longer worth the effort for traders.

Advantage Has Shifted to TradFi Perpetual Contracts

What has changed is not the existence of funding rate arbitrage itself, but where it exists. More interesting opportunities have moved to TradFi perpetual contracts, where the market structure remains young, and the flow of funds is far from defined. These products occupy an unusually intermediary space: they are macro-financial instruments but are built on the infrastructure of cryptocurrency, traded 24/7, and face a user base still learning how to correctly price them.

This is crucial because the performance of TradFi perpetual contracts is starkly different from mature cryptocurrency contracts. They respond to macro news headlines, continue trading even when the underlying markets close, and are spread across platforms with diverse participant profiles. This creates a more chaotic funding rate environment, and chaotic markets are where traders can achieve excess returns. Particularly on BitMEX, this has opened a series of funding rate arbitrage opportunities that are far more attractive than the remaining spaces in mainstream crypto.

Trading Opportunities: XAUt (Tether Gold) and BRENT (Oil)

Trading Strategy 1: XAUtUSDT — A More Pure and Robust Arbitrage

The first opportunity is relatively direct: buy XAUt spot on BitMEX while shorting XAUtUSDT on BitMEX, earning funding fees in a delta-neutral structure. This is an extremely classic arbitrage trade, only applied to tokenized gold instead of mainstream crypto assets. Its appeal lies not only in the surface yield but in the "quality" of that yield.

In the past 1,759 hours (about 73 days), the average annualized funding rate for XAUtUSDT on BitMEX reached 9.67%, easily outpacing Hyperliquid's 5.99% and Bybit's 3.22%. More importantly, BitMEX's rate performance appears to be more stable. This point is crucial because only arbitrage trades that can be consistently maintained are truly useful. Traders often focus only on peak data, but the real value of funding rate strategies lies in whether their performance can allow traders to realize profits without persistent anxiety. Trades that appear tempting on paper but fluctuate wildly make it challenging to leverage positions and hold them confidently.

This is precisely why XAUtUSDT stands out. It may not be the most dramatic trade in the market, but it is more practical. In a time when most traditional crypto futures arbitrage spaces have been compressed to negligible, it offers a relatively clean and lower-cost version of arbitrage. For those seeking robust yield strategies rather than tactical speculation, this is a more "civilized" layout.

Trading Strategy 2: Brent Oil — A Higher Volatility Cross-Platform Spread

The second opportunity is much more aggressive and explosive. On the Brent Oil underlying, the funding rate difference between BitMEX and Hyperliquid has become one of the most visibly attractive cross-platform spreads in the current market. The structure is simple: go long on BRENTUSDT on BitMEX while shorting Brent on Hyperliquid.

The operational principle is equally straightforward. The funding rate for BRENTUSDT on BitMEX often exists in a state of extreme negativity, while Brent on Hyperliquid typically maintains a positive rate. This creates a rare structure: traders can often collect funding fees on both sides simultaneously. This is precisely the "dual funding rate capture" strategy that traders have long dreamed of in the crypto market, but such good days have essentially disappeared in the mature BTC and ETH ecosystems.

The data displays exceptionally strong performance. In the latest snapshot, the funding rate for Brent on BitMEX was annualized at -594.585%, while on Hyperliquid it was annualized at 40.792%. Over the past 7 days, the implied annualized yield of this spread was approximately 361.607%, with consistency reaching 80.5%. Over a 14-day period, its implied annualized yield still reached 220.740%, and 30 days yielded 103.012%. Within the 14-day and 30-day time windows, BitMEX had 65.4% of the time as the lower-cost platform. These are far from the normal data of a mature market, and that is precisely the key. Crude oil trading operating on a crypto base is still in its early stages, highly decentralized, and has not yet been completely filled by the army of arbitrageurs, which is why such levels of spreads exist.

Why Do These Trading Opportunities Still Exist?

The deeper story is that TradFi perpetual contracts are still in the early stages of price discovery. They attract a trading group that differs from mainstream crypto assets; their reactions to macro and geopolitical news are more direct, and they continue trading even when the underlying reference markets close. This combination of pricing distortions cannot survive for long in the crowded mainstream coin arbitrage pool.

BitMEX is particularly interesting here because its TradFi perpetual contract matrix is still young enough that these spread relationships have not yet been completely smoothed out by the balance sheets of mega-whales. This creates an excellent hunting ground for traders. In fact, the market is still rewarding those willing to step outside the obvious BTC/ETH funding rate trades to search for opportunities elsewhere.

Final Conclusion

The main battleground for traders seeking real advantages is no longer the old funding rate trades of mainstream crypto assets. That has become an extremely crowded institutional strategy, with competition compressing the returns to a point where they no longer make sense relative to the risks taken and the effort invested. Alpha has not disappeared; it has merely shifted to corners of the market where structural inefficiencies still exist.

Currently, BitMEX's TradFi perpetual contracts are one of the clearest places to find this Alpha. XAUtUSDT offers a more pure and stable arbitrage trade with an average annualized yield of about 9.67% over the past 73 days; whereas a comparison between BitMEX and Hyperliquid's Brent contracts shows that BRENTUSDT provides a more lucrative and tactical spread opportunity, with recent windows showing annualized yields reaching triple digits. Old arbitrage trades have not perished; they have simply moved away from the most crowded lanes in the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。