Original | Odaily Planet Daily (@OdailyChina)

Author|Azuma(@azuma_eth)

The market remains sluggish, funds are stagnating, agreements are shutting down, major players are silent, and retail investors are bleeding... It seems the industry is losing money from top to bottom. However, even in such a bleak market environment, there are still a very small number of projects with their money-making machines roaring.

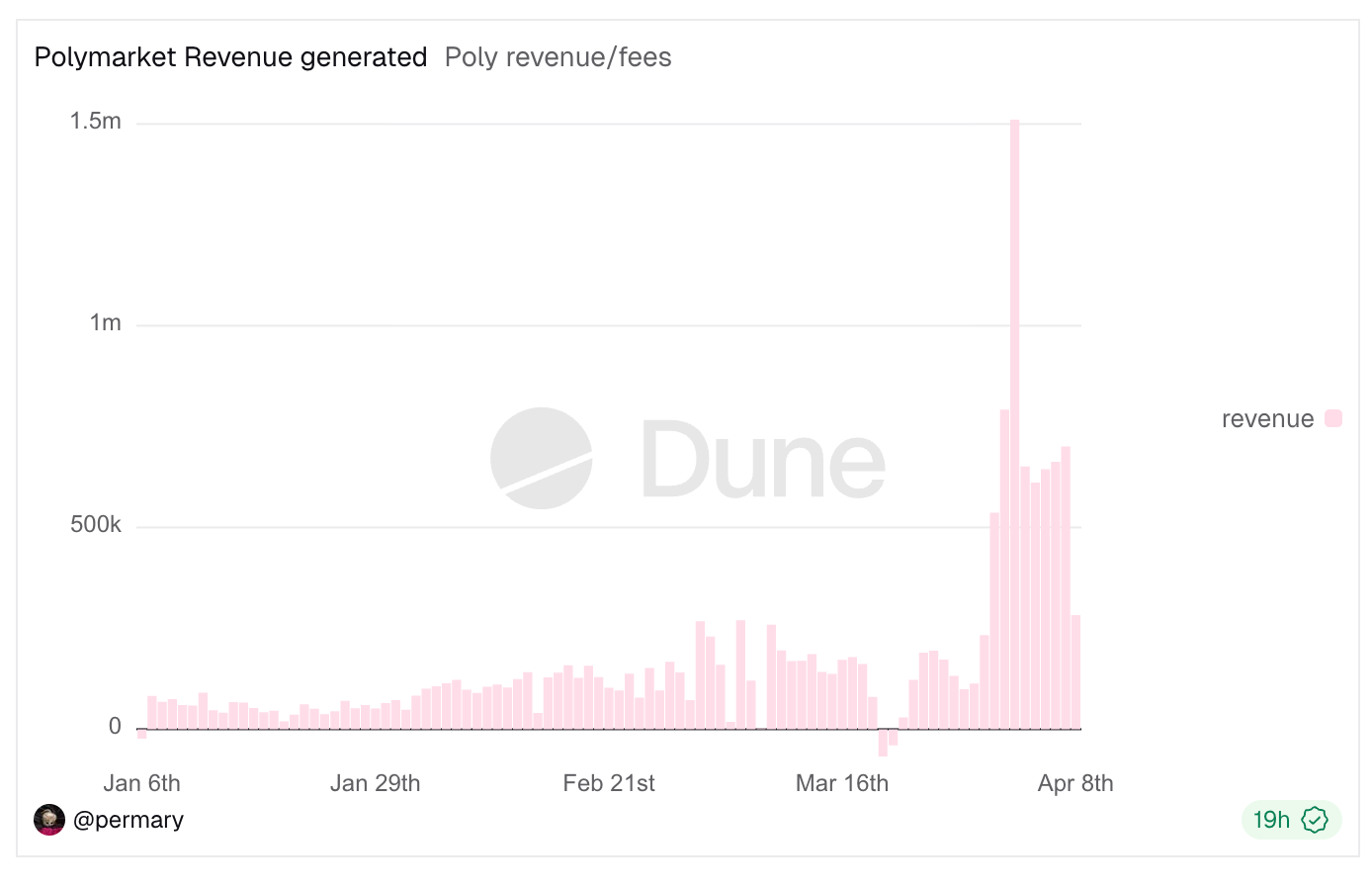

The latest case is Polymarket, which has completely opened the floodgates for fees. Since recently expanding the fee range and modifying the fee formula (recommended reading: “Hardcore Breakdown of Polymarket's Fee Formula: How did an Extreme Rate of 90+% Come About?”), Polymarket’s revenue capability has surged significantly; as of the time of writing, Polymarket's total fee revenue has exceeded 24 million USD, with April 2 setting a record of 1.5 million USD in daily revenue.

Taking this opportunity, I flipped through the revenue rankings on Defillama to see which businesses are still continuously making money during the bear market, and the results were quite surprising: the core businesses and revenue sources of the projects on the list are quite clear and could even be described as “simple.”

As shown in the above image, I believe that most players deeply entrenched in the crypto market could guess the majority of the names without looking at the answers and might even be quite clear about what they do. However, when these names are neatly laid out together, I suddenly realized that the main revenue sources of these profitable businesses are highly similar, and can essentially be summarized into two broad categories: one is interest spread, the other is transaction tax (fees).

First is the interest spread, which essentially acts as a “funds intermediary.” The core logic is to absorb funds at a relatively low cost while deploying them at a relatively high yield, gradually accumulating the difference between revenue and cost over time — the income of such businesses depends on the scale and duration of fund deposits; the larger the scale and the longer the duration, the higher the revenue.

Issuers of stablecoins like Tether and Circle belong to this category, with their main income coming from the interest generated after deploying reserves into assets such as U.S. Treasury bonds, while their costs mainly arise from the subsidies given to partners and users, with the difference constituting their profit; lending protocols like Aave also fall into this category, where the interest spread is the difference between a relatively high borrowing rate and a relatively low deposit rate; liquid staking services like Lido also follow suit, withholding a certain proportion from the native staking rewards of ETH as service fees, which similarly falls under interest spread.

Next is transaction tax, which is easier to understand; as long as there are trading-related activities (including token creation), the business entity can “tax” in the form of fees during each activity — the revenue of such businesses depends on the trading scale of single activities and the frequency of activities, where greater scale and higher frequency lead to higher revenue.

Whether it's Hyperliquid and EdgeX focusing on contract trading, Polymarket focusing on event trading, pump.fun, GMGN, Axiom, and four.meme focusing on meme trading, or Aerodrome, Jupiter, and Phantom (whose primary revenue comes from swap fees at the wallet front) focusing on spot trading, or even Courtyard and Fragment focusing on NFT trading (it’s quite surprising that this category can still make the list), their main revenue source is transaction tax.

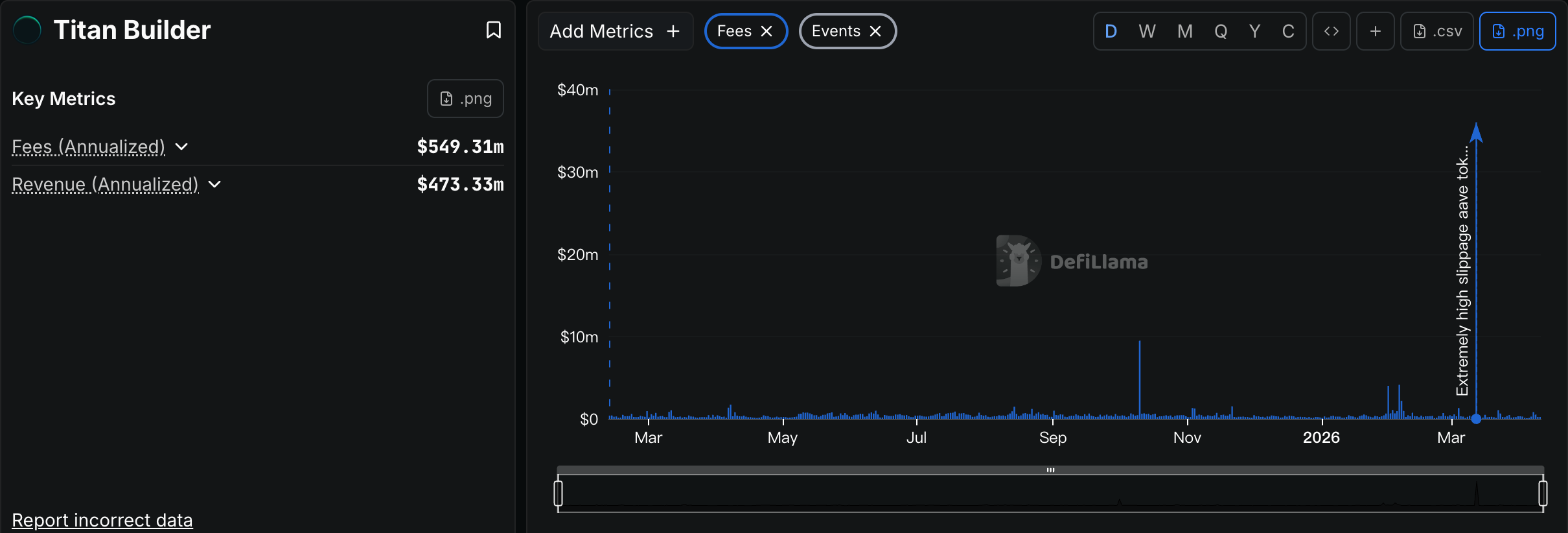

The only few special cases in the rankings are Grayscale, Chainlink, and Titan Builder. Grayscale is somewhat odd here, as its core revenue comes from management fees on ETFs and funds, essentially a traditional asset management business focused on the cryptocurrency market; Chainlink is noteworthy, with its main revenue coming from data service fees paid when projects call its oracle, resembling a To B on-chain SaaS business, but as you can see, the Matthew effect in this path is more significant than in other fields; Titan Builder is purely an exceptional phenomenon, serving as a block construction service provider which normally wouldn’t qualify as a lucrative business, but it made the list because it benefitted greatly from a massive AAVE trading incident last month (see “50 million USDT returned for 35,000 USD AAVE: How did the disaster happen?”).

Odaily Note: Look at what it means to be three years of no business, only to profit for three years once opened.

So the conclusion is already very clear. Projects that continue to make money during the bear market are not those chasing complex mechanisms and high-risk opportunities, but those capable of continuously operating with a simple and clear revenue model. In the still turbulent cryptocurrency market, simpler revenue models are showing stronger resilience, better withstanding the tests of market fluctuations.

However, a simpler revenue model does not mean these businesses themselves are “easier to operate.” On the contrary, behind these simple revenue models lies often more complex product services and refined operational management; this is where the leading players on the list have truly differentiated themselves. From interaction design to liquidity accumulation to risk management to user communication feedback… to stand out in the fiercely competitive existing market, more effort must be invested in the product and services.

The cryptocurrency winter is not yet over, and the projects that can truly survive or even profit are often those that flexibly combine simple revenue models with complex product services. Perhaps, this is the long-term key to navigating through bulls and bears.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。