The Strait of Hormuz is considered the "throat" of global energy: the global maritime transport of crude oil and a large amount of natural gas must pass through this narrow waterway to enter the international market from the Middle East. For a long time, it has been treated in public reports as a free international waterway, without charging for passing ships. Now, in the context of the U.S.-Iran ceasefire framework, the sudden implementation of a charging mechanism itself represents a historic institutional shift. The ceasefire arrangement and the charging mechanism appeared nearly simultaneously, indicating that geopolitical games have entered a new stage: shifting from "to fight or not to fight" to "who pays for peace and at what price." The real suspense lies not in the permit itself, but in how this additional cost layers into freight, insurance, and crude oil prices, ultimately altering the path of global inflation and reshaping the valuation logic of risk assets.

The Day of Ceasefire is also the Starting Point for Charges

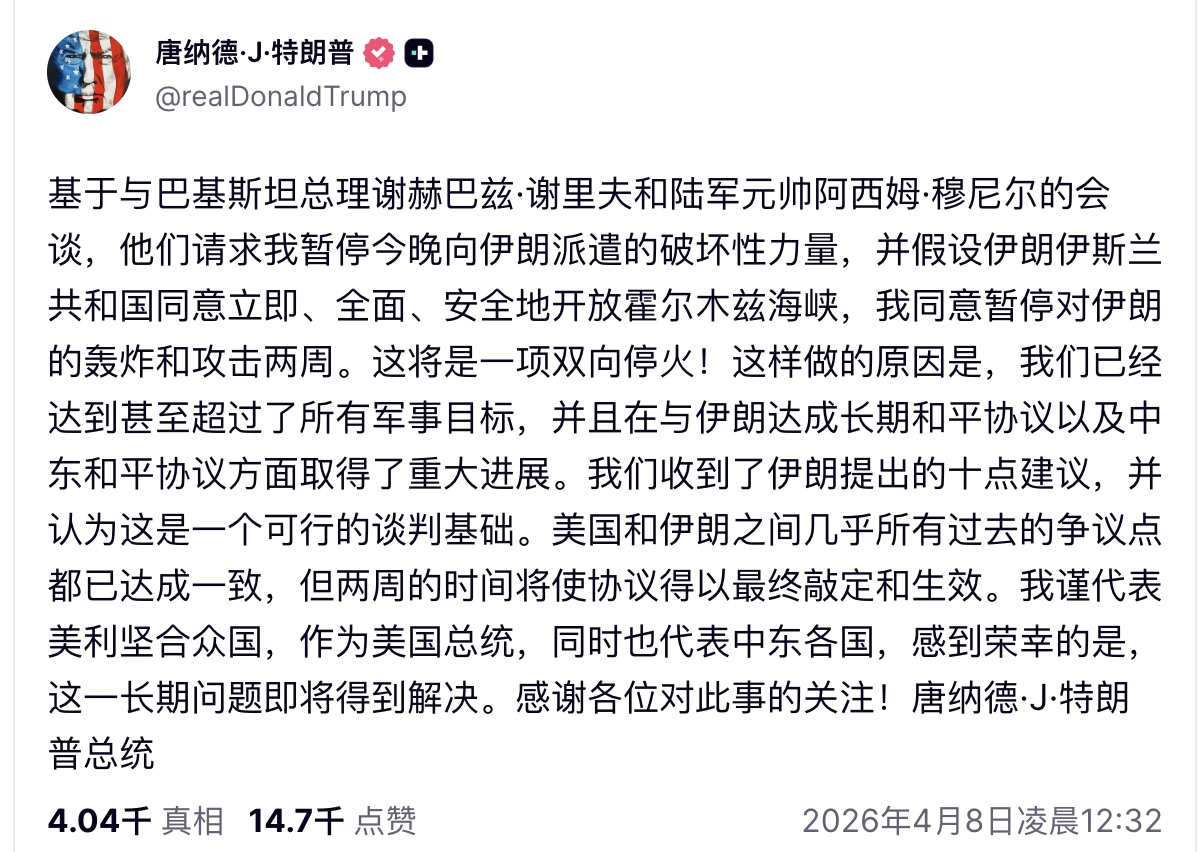

Under the U.S.-Iran ceasefire framework, Iran and Oman announced the start of tolls for ships passing through the Strait of Hormuz. This charging mechanism closely coincides with the ceasefire arrangement in timing: one side is the easing of war risk, while the other side is a rewriting of the navigation system. The simultaneous emergence of both releases signals far more complex than a simple "peace dividend." The ceasefire means a decrease in short-term bomb and blockade risks, while the charging indicates the introduction of a new, ongoing cost source on the same route, creating a new pricing dilemma for the market.

When the ceasefire news was initially absorbed by the market, mainstream expectations leaned towards optimism: the risk premium was expected to decline, concerns over crude oil supply interruptions eased, and there was downward potential for tanker insurance fees and freight costs. In this scenario, crude oil prices should have gently adjusted along the path of "de-escalation of conflict—decline of risk premium—decrease in freight," with some long positions ready to realize profits accumulated from geopolitical conflicts, allowing risk assets to breathe under the narrative of "the shadow of war dissipating."

Corresponding to these expectations is the emotional relaxation of market participants. The founder of Liquid Capital, Yili Hua, summarized this mindset with "the war has been confirmed to be over" (from a single source). Such statements reflect a hope to erase geopolitical risks in one fell swoop and return to "normal volatility." However, when the charging mechanism nearly simultaneously took effect, this feeling of "it's finally over" faced an immediate contrast: while the war risk premium was dissipating, the institutional cost premium began to rise, forcing a rewrite of the previously clear long-short logic.

A Rare Moment When International Waterways Start Charging

Publicly, the Strait of Hormuz has long been regarded as an international waterway without charges. This long-standing consensus forms the underlying assumption of the global energy shipping order: all cost calculations, long-term capacity allocations, and insurance pricing assumed that this Middle Eastern lifeline does not have a "toll" item. When a key bottleneck regarded as an international public channel officially begins charging as a sovereign entity, it means the premise of "free and open" in the old order is broken, and the market needs to reprice this waterway.

For international shipping companies and energy traders, this is not simply a matter of adding a cost to an Excel sheet, but rather a restructuring of the entire cost model and risk model. In the past, when companies calculated costs from the Gulf to major consuming countries, the focus was on fuel, capacity, insurance, and time value. Now, tolls will become a fixed expenditure with institutional stability and potential upward adjustment space. This will compel shipping companies to adjust their pricing logic, reassess fleet deployment, and some marginal capacities may even become unprofitable under the new cost structure.

Within the framework of international law and the principle of freedom of navigation, this charge also buries controversy and negotiation space. The long-standing perception of Hormuz as an international waterway clashes with the coastal states' assertion of the right to charge: on one hand, sovereign states have a realistic need to generate income through activities in their territorial seas and contiguous zones; on the other hand, major powers and key shipping countries may worry that "a precedent has been set," leading to future charges in other key straits or channels, raising global trade costs. Diplomatic negotiations around the legality of charges, scope of application, and discrimination issues may continue to ferment in the coming period, becoming a new battleground for geopolitical negotiations.

Post-war Reconstruction Chips: Tolls Becoming...

According to some sources, Iran plans to use the toll revenue from Hormuz for post-war reconstruction (the information source needs cross-validation). This adds a "politically correct" packaging to the charging mechanism—not merely fiscal exploitation, but financing for infrastructure and social restoration after the conflict. If this purpose is further confirmed, the charging mechanism will not just be a trade cost issue, but will also be included in discussions about post-war order and responsibility allocation: who pays for post-war restoration, the warring parties or global energy buyers relying on this channel?

From a macro fiscal perspective, tolls provide Iran with a potentially stable foreign exchange income channel, helping to ease foreign exchange tightness and enhance fiscal independence under a sanctions environment. Compared to relying on export channels that may be constrained by sanction intensity at any moment, tolls resemble a monetization of "geographic dividends," directly translating geographical advantages into recurring income. Once scaled, this revenue will partially hedge the fiscal pressure brought by traditional export restrictions, enhancing Iran's resilience in the face of external financial and energy sanctions.

More critically, pricing power itself will become a new bargaining chip in future geopolitical negotiations. The level of tolls, subjects for exemptions, and temporary adjustments can serve as exchange conditions among different negotiation topics: raising rates or hinting at adjustments during tense situations expands cost pressures on importing countries; offering certain discounts or stabilizing expectations during easing phases can exchange for political or economic concessions. Once the charging mechanism is embedded in the negotiation toolbox, its impact will go beyond simply "how much more was collected" and transform Hormuz from a physical channel into an adjustable geopolitical lever.

The Oil Price Chain is Rewritten: From Waterway to Gas Station

From the perspective of price transmission paths, the Hormuz toll will first reflect in the total costs of shipping companies, forming the comprehensive freight for each barrel of crude oil or each ton of goods alongside fuel, crew, and insurance. Once freight costs rise, insurance companies will also have the incentive to adjust premium structures when reassessing the geopolitical and operational risks of this route, especially in phases where charging triggers political friction and potential friction risks increase. The cumulative effect will be an upward adjustment in the landed cost at major consuming country ports, naturally leading crude oil spot trading to factor this new cost into pricing, in turn influencing crude oil futures prices through basis and expectation logic.

At the terminal level, the prices of refined products like gasoline and diesel are highly sensitive to this chain. U.S. polls show that about 70% of Americans express concern that military actions lead to rising oil prices (from a single source), indicating that in major consuming countries, oil prices themselves are highly politicized and emotional variables. Once the market reaches a consensus: that charging in Hormuz will elevate transport and supply costs within a visible timeframe, consumer sensitivities to rising oil prices will advance, and corporate pricing and union negotiations will lock this expectation into wage and commodity price discussions.

At the macro level, this will directly raise global inflation expectations, especially for low-income groups in emerging markets and developed economies that have a high energy weight. Central banks must weigh the risk easing brought by "de-escalation of conflict" against the tail risks of inflation from "the rigid increase in energy costs": if the market believes that oil price centrals will rise due to waterway charges, the pace of monetary easing may slow or even be postponed. Instead of entering a phase where post-ceasefire expectations of interest rate declines and risk asset valuation recovery spread, there will be pressure from "cost-push inflation" lingering, indirectly suppressing valuations of stocks, bonds, and cryptocurrencies.

From Whales Suffering Losses to the Chain Reaction for Cryptocurrencies

According to rumors, a whale in crude oil contracts faced a floating loss of about $3.41 million after the ceasefire news was announced due to unfavorable market conditions for long positions betting on sustained geopolitical risks elevating oil prices (from a single source anecdote). Such stories themselves are not sufficient to represent the entire market but are typical pendants of emotional turning points: when the conflict premium fades, excessively relying on narrative of "the war never ends" leveraged positions will be ruthlessly liquidated by the market, and prices will begin to revert to more detailed and structured supply-demand and cost logic.

In an environment where ceasefire and charging mechanisms run in parallel, positions in crude oil and related derivatives are being forced to reprice. The bubble of geopolitical risk premiums is squeezed out, but it is replaced by discounts on long-term institutional costs: traders need to include "Hormuz fees" as a new factor in their models to reevaluate the reasonable ranges of various term contracts. In the short term, long and short will repeatedly tussle over the question of whether "peace dividends outweigh rising costs," with the forces of macro CTAs, commodity funds, and physical hedges seeking a balance within the new price range.

For cryptocurrencies, fluctuations in oil prices and inflation expectations will reignite or weaken the narrative of assets like Bitcoin as an "inflation hedge." In times of rising inflation expectations and pressure on real interest rates, Bitcoin is often viewed by some funds as a target for "digital gold" allocation. Conversely, when the market expects that central banks may be forced into a dovish stance under high inflation due to growth pressures, liquidity games will push up interest in high-beta assets. If Hormuz charging is interpreted by the market as shifting the inflation central upward, it will emotionally support this narrative, driving some funds away from traditional safe-haven assets and credit markets toward cryptocurrencies; conversely, if charging is perceived as limited in impact, with ceasefire dividends prevailing, then the "inflation hedge" label may temporarily cool, with funds preferring short-duration, highly liquid cryptocurrency targets rather than long-term store of value narratives.

Normalization of Charges or a Window for Geopolitical Chips

In summary, the charging initiated in the context of the ceasefire in Hormuz releases a safety signal for "easing of conflict" in one hand, while elevating a long-term signal for "increasing energy costs" on the other. This duality makes it difficult for the market to interpret in a single direction: short-term explosive risks are decreasing, but structural cost pressures are on the rise. For risk assets, this means a downward trend in tail disaster probabilities, but the central discount rate and cost shocks may rise, with both positive and negative valuation factors being written into the new script simultaneously.

Moving forward, several key variables will determine the true impact of this mechanism: first is the charging level itself—whether it will remain within an acceptable range for the market or if there is a possibility of periodic elevation; second is the stability of implementation—whether policies will be consistent or vary with geopolitical friction, increasing uncertainty premiums; third is the political response from major buyers and shipping countries—whether major powers choose direct negotiation, seek exemptions, or hedge costs through other channels will determine whether this system is dulled, hedged, or further strengthened.

Under different scenarios, oil price and inflation paths will also show divergence: if charges are mild and execution is predictable, oil prices may simply rise one step higher within the original range, with inflation pressure more reflected structurally; if toll rates rise significantly and become frequently adjustable geopolitical tools, the fluctuation centers for oil prices and freight will be significantly raised, amplifying uncertainties in inflation and monetary policy. Current information regarding the use of charges and participating ceasefire parties still requires verification; subsequent official statements and cross-verification from multiple reports will be key in assessing the size of this "new powder keg" and the length of its fuse. For investors focused on crude oil, macro inflation, and cryptocurrencies, continuously tracking these factual updates is more important than betting on a single narrative at emotional turning points.

Join our community to discuss and grow stronger together!

Official Telegram community: https://t.me/aicoincn

AiCoin Chinese Twitter: https://x.com/AiCoinzh

OKX Benefits Group: https://aicoin.com/link/chat?cid=l61eM4owQ

Binance Benefits Group: https://aicoin.com/link/chat?cid=ynr7d1P6Z

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。