Original author: Pink Brains

Original translation: AididiaoJP, Foresight News

In the past 12 months, three major DeFi protocols have successively abandoned the ve token model.

Pendle, PancakeSwap, and Balancer have different triggers, but the conclusions drawn are highly consistent.

The ve token model was once regarded as the ultimate solution for DeFi token economics. Users lock tokens to gain governance rights, earn fees, and align incentives long-term, all without centralized governance. Curve proved the model's feasibility, and from 2021 to 2024, dozens of protocols followed suit.

But this situation has changed.

In the year 2025, three protocols with total locked values of several billion dollars identified that the mechanism's drawbacks outweigh its benefits. The reason is not theoretical errors, but failures at the execution level: low participation rates, governance capture, emissions flowing to unprofitable pools, and token prices plummeting even as usage increases.

Note: The ve token model (Vote-escrow Tokenomics) is one of the most representative token economic models in the DeFi field, first proposed and successfully implemented by Curve Finance in 2020. It achieves deep alignment of incentives among users, liquidity providers (LPs), and protocols by mandating long-term locking of governance tokens. In simple terms, users lock protocol tokens for a period (usually up to 4 years) in exchange for veToken, thus gaining the right to vote on how new tokens are distributed, enjoy higher yields, and receive protocol dividends, aiming for long-term protocol binding and reducing sell-offs.

Pendle: From vePENDLE to sPENDLE

The Issues

The Pendle team revealed that despite a 60-fold increase in revenue over two years, vePENDLE had the lowest participation rate among all veToken models—only 20% of the PENDLE supply was locked.

Originally intended to align incentives, the mechanism actually excluded 80% of holders. More decisively, the segmented data for each pool shows that over 60% of the pools receiving emissions are in a state of loss.

A few high-performance pools are subsidizing the majority of value-eroding pools. Voting rights are highly concentrated, resulting in emissions flowing to large holders' positions (usually to wrappers), which are then allocated to end users.

Source: https://x.com/pendle_fi/status/2013431342546157825?s=20

In contrast, Curve's veCRV locking rate is about 50% or higher. Aerodrome's veAERO locking rate is around 44%, with an average locking duration of about 3.7 years, while Pendle's 20% is significantly low. In the yield market, the opportunity cost of capital makes its locking incentives unattractive. Meanwhile, Aerodrome had distributed over $440 million to veAERO voters by March.

Alternative: sPENDLE

- 14-day withdrawal period, or pay a 5% fee for immediate withdrawal

- Algorithm-driven emissions, reduced by about 30%

- Passive rewards, voting only on key PPP matters

- Transferable, combinable, and restakable

- 80% of revenue used to buy back PENDLE

sPENDLE is a liquid staking token, pegged 1:1 to PENDLE. Rewards come from revenue-funded buybacks, rather than inflationary emissions.

The algorithm model reduces emissions by about 30%, while redirecting resources to profitable pools.

Existing vePENDLE holders receive loyalty boosts (up to 4x multiplier, decaying within two years from the January 29 snapshot).

An address associated with Arca accumulated over $8.3 million in PENDLE within six days.

However, not everyone agrees with this decision. Curve founder Michael Egorov believes that the ve token model is an extremely powerful mechanism for incentive alignment in DeFi.

PancakeSwap: From veCAKE to Tokenomics 3.0 (Burn + Direct Staking)

The Issues

PancakeSwap's veCAKE embodies a typical bribe-driven misallocation. The voting system has been caught by Convex-style aggregators, particularly Magpie Finance, which siphon emissions with almost no real liquidity brought to PancakeSwap.

Pre-closure data showed that pools receiving more than 40% of total emissions contributed less than 2% of CAKE burn. The ve model has created a bribe market where aggregators extract value, while the pools generating actual fees are inadequately incentivized.

Source: https://forum.pancakeswap.finance/t/cake-tokenomics-proposal-3-0-true-ownership-simplified-governance-and-sustainable-growth/1237

However, this closure was meticulously planned. Michael Egorov called it "a textbook governance attack," suggesting that insiders of CAKE wiped out the governance rights of existing veCAKE holders and could potentially forcibly unlock their own tokens after voting.

Cakepie DAO, as one of the largest CAKE holders, questioned the legality of the voting. PancakeSwap offered up to $1.5 million in CAKE compensation for Cakepie users.

Alternatives

- 100% of fee revenue used for CAKE burning

- Direct management of emissions by the team

- 1 CAKE = 1 vote (simple governance)

- Approximately 22,500 CAKE/day, targeted to reduce to 14,500

- 100% fee revenue used for CAKE burning, no revenue sharing

- Goal: annual deflation rate of 4%, total reduction of 20% by 2030

All locked CAKE/veCAKE positions can be unlocked without penalty during a 6-month 1:1 redemption window. Revenue sharing has been redirected to burning, and the burn rate for key pools has been increased from 10% to 15%. PancakeSwap Infinity was launched concurrently with a redesigned pool architecture.

Post-Transformation Results

- 2025 net supply reduction of 8.19%

- 29 consecutive months of deflation

- Permanent removal of 37.6 million CAKE since September 2023

- Burned over 3.4 million CAKE just in January 2026

- Cumulative trading volume of $35 trillion (projected $23.6 trillion for 2025)

While the deflation strategy performed well, the CAKE price remains around $1.60, down 92% from its all-time high.

Balancer: Gradual Phase-out of veBAL (DAO + Zero Emissions)

The Issues

Balancer's failure is a compound cascade of governance capture, security vulnerabilities, and economic bankruptcy.

The struggle with large holders erupted first. In 2022, a large holder named "Humpy" manipulated the veBAL system, directing $1.8 million worth of BAL to its controlled CREAM/WETH liquidity pool within six weeks. During the same period, this pool generated only $18,000 in revenue for Balancer.

Subsequently, a vulnerability attack occurred. A rounding issue in Balancer V2's exchange logic was exploited across multiple chains, resulting in approximately $128 million in losses. TVL dropped by $500 million within two weeks. Balancer Labs faced additional unbearable legal risks.

Alternatives

- 100% of fees allocated to the DAO treasury

- BAL emissions reduced to zero

- 100% of fees assigned to the DAO treasury

- Buy back BAL at a set price for exits

- Focus areas: reCLAMM, LBP, stable pools

- Streamline the team through Balancer OpCo

The old DeFi model centered around token rewards is gradually being phased out.

Despite the token economics issues, Martinelli pointed out that Balancer "is still generating real revenue," exceeding $1 million over the past three months:

"The problem isn't that Balancer can't operate, but that the economic mechanism surrounding Balancer is not functioning. These are fixable issues."

Whether a streamlined DAO can maintain a TVL of $158 million without incentives remains an open question. Notably, Balancer's market cap ($9.9 million) is currently lower than its treasury ($14.4 million).

Underlying Mechanism Analysis

The three exit cases above are surface-level signs; the structural issues are the root causes.

A recent analysis by Cube Exchange listed three scenarios in which the ve-token model might fail.

Source: https://www.cube.exchange/vi/what-is/vetokenomics

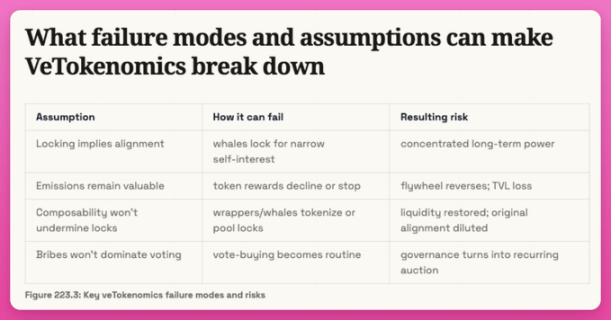

Assumption 1: Emissions must maintain value. If the token price crashes, the value of emissions declines → LP exits → liquidity, volume, fees drop → further sell-off. This forms a classic reverse flywheel (which has appeared with CRV, CAKE, and BAL).

Assumption 2: Locking must maintain reality. If locked tokens can be packaged into liquid versions (like Convex, Aura, Magpie), then "locking" loses practical significance and generates exploitable inefficiencies.

Assumption 3: A true allocation problem must exist. The ve model is effective when a protocol continuously needs to decide where to direct incentives (e.g., AMM). Without this demand, measuring votes becomes an unnecessary expense.

Diagnostic Test:

Does the protocol have a genuine and recurring allocation problem, allowing community-led emissions to create measurable greater economic value than team-led allocations?

If the answer is no, then the ve token model merely adds complexity without adding value.

Fee to Emission Ratio

The fee to emission ratio refers to the dollar value of fees generated by the protocol divided by the dollar value of emissions distributed.

When this ratio is above 1.0, the fees earned by the protocol from liquidity exceed the costs it pays to attract that liquidity. Below 1.0, it constitutes a loss-subsidized activity.

Pendle's exit reveals a nuance: the overall ratio obscures the true situation of individual pools.

Pendle's overall fee efficiency exceeds 1.0 (revenue greater than emissions). However, when the team segments by pool, over 60% of pools are in a state of loss themselves.

A few high-performance pools (likely large stablecoin yield markets) are subsidizing all other pools. Manual measurement voting directs emissions favorably towards large holders, rather than pools generating the most fees.

PancakeSwap also shows a similar situation, specifically reflected in CAKE burning.

The Liquidity Locking Paradox

The ve token model creates a problem: inefficient capital locking. Liquidity lockers attempt to solve this by packaging locked tokens into tradable derivatives. However, while addressing capital efficiency issues, they introduce governance centralization problems. This paradox exists at the core of every ve token model.

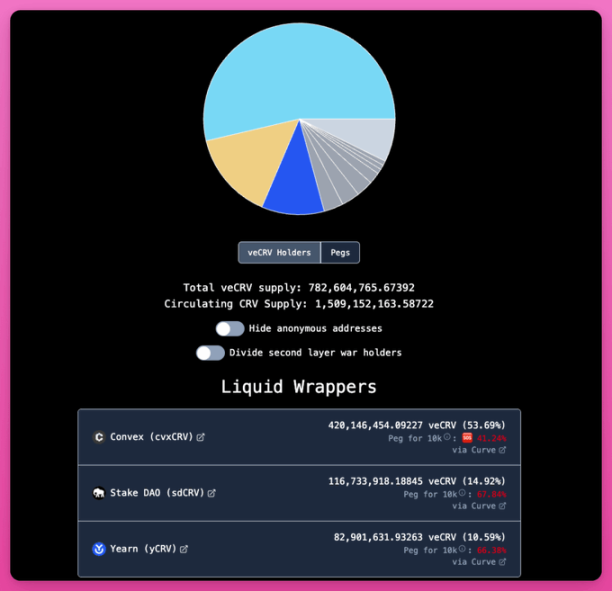

In Curve's case, this paradox has led to stable (if concentrated) outcomes. Convex holds 53% of all veCRV. StakeDAO and Yearn hold additional shares.

With Convex, individual governance is effectively mediated through vlCVX voting. But Convex's incentives are highly aligned with Curve's success, and its entire operation relies on Curve's good functioning. This centralization is structural rather than parasitic.

In Balancer's case, this paradox is destructive. Aura Finance became the largest holder of veBAL and the de facto governance layer. However, due to the lack of other strong competitors, a malicious large holder (Humpy) independently accumulated 35% of veBAL and extracted emissions by gaming the measurement constraints.

In PancakeSwap's case, Magpie Finance and its aggregators captured measurement votes through bribery and directed emissions towards pools that create extremely low value for PancakeSwap.

The ve token model requires locking capital to function, but the inefficiency of locked capital leads to mediators that unlock capital, and in the process, they concentrate governance power that should be dispersed. The model creates conditions for its own capture.

Curve's Rebuttal: Why the ve Token Model Remains Important

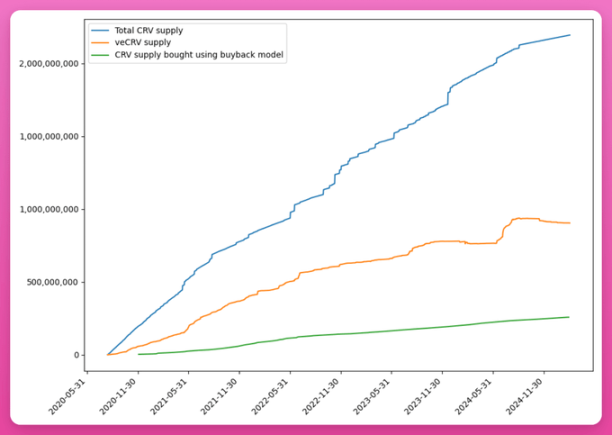

Curve concludes that the number of continuously locked tokens of veCRV is approximately three times the number of tokens that would have been removed by comparable burning mechanisms.

https://news.curve.finance/beyond-burn-why-vecrv-unlocks-sustainable-tokenomics-for-curve/

The scarcity based on locking is structurally more profound than the scarcity based on burning, as it simultaneously generates governance participation, fee distribution, and liquidity coordination, rather than merely a reduction in supply.

In 2025, Curve's DAO removed the veCRV whitelist, expanding participation rights in DAO governance. The protocol's metrics also performed excellently:

- Trading volume grew from $119 billion in 2024 to $126 billion in 2025

- Pool interactions more than doubled, reaching 25.2 million transactions

- Curve's share of fees from Ethereum DEX increased from 1.6% at the start of 2025 to 44% in December, a growth of 27.5 times

However, it is important to see the counterpoint: Curve occupies a unique position as the core pillar of stablecoin liquidity on Ethereum, and 2025 is a year of significant development for stablecoins. There exists a genuine, market-driven, organic demand for measures to guide liquidity. Stablecoin issuers like Ethena structurally need Curve pools. This creates a bribe market based on real economic value.

The three protocols that have moved away from the ve token model do not possess this condition. Pendle's value proposition is yield trading, not liquidity coordination. PancakeSwap is a multi-chain DEX. Balancer is a programmable pool. They lack structural reasons for external protocols to compete for their measurement emissions.

Conclusion

The ve token model is not universally failing. Curve's veCRV and Aerodrome's ve(3,3) are still thriving.

But the model only works where the measured-guided emissions can create genuine economic demand for liquidity. Meanwhile, other protocols are opting for revenue-supported buyback, deflationary supply mechanisms, or liquidity governance tokens as alternatives to the ve token model.

Perhaps DeFi has reached a point where a new incentive mechanism is needed, one that should benefit both the long-term interests of the protocols and the token holders.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。