Introduction: From Turmoil to Reconstruction

In the past few months, the Vaulta ecosystem has experienced a truly tumultuous period. Yves La Rose, the founder of the Vaulta Foundation, announced his resignation and disbanded the foundation. During the long transition, the price of the token $A continued to decline amid uncertainty, leading to a series of intensifying internal disputes. In terms of governance, Block Producers (BPs) as the highest governance authority faced reduced income—approaching shutdown prices—resulting in some BPs abandoning governance participation or showing severe lack of enthusiasm; in the community aspect, token holders experienced low information transparency, being unaware of both the transition progress of the former foundation and the development plans for the future network, leaving them to watch the token price fall helplessly; meanwhile, changes in the organizational structure led discussions about the overall network development to gradually deviate from narrative and technical development, ultimately focusing on the use of funds from the Vaulta Treasury (hereinafter referred to as Treasury), with network development evolving into a battle over fund distribution! It can be said that the dissolution of the foundation unveiled the failure of DPoS governance, highlighting that when you discover one cockroach, there are likely hundreds nearby.

This article, starting from the positions of Vaulta Labs and Treasury, will delve into the experiences and reflections of the Vaulta network regarding the adoption of the DPoS model and propose solutions. Additionally, this article will sound the horns for DPoS mechanism reform, serving as a commitment to the community and a starting point for the reconstruction of governance order in Vaulta.

The Commitment of DPoS: An Experiment in Democracy and Efficiency

Imagine a world without banks, no government, and no central authority—millions of people collectively maintain a ledger that cannot be tampered with, where no single entity has the final say. This is not a utopia; it is the core question blockchain attempts to solve: how can a group of strangers reach a consensus without a trusted intermediary?

Around this question, the blockchain world has delivered several distinctly different answers in just a few years. Bitcoin, using Proof of Work (PoW), was the first to break the ground—letting computing power do the talking. The more computing resources one contributes, the more authority one has to record transactions. It is secure and decentralized, but the costs are equally clear: slow, extremely high energy consumption, and almost no participation from the average person. Ethereum later introduced Proof of Stake (PoS), replacing the competition for computing power with the staking of tokens, improving efficiency, but ordinary token holders still lacked substantial influence on the network's direction.

In 2013, Dan Larimer first proposed the DPoS (Delegated Proof of Stake) mechanism, carving out a third path. Its logic directly addresses the core issue: instead of letting everyone compete for computing power or staked capital, why not let token holders vote directly to elect a group of community-recognized representatives to maintain the network? Efficiency comes from a streamlined representation; democracy comes from the votes of token holders. DPoS was first implemented on BitShares, then adopted by several well-known projects such as Steem, EOS (now Vaulta), and TRON, becoming a consensus mechanism that has been tested in real-world public chain competition.

In 2018, the EOS mainnet was officially activated and became one of the most-watched projects among new public chains at the time. The election of 21 BPs was referred to by many as "the first large-scale on-chain governance experiment in blockchain history"—node teams published white papers, committed to ecological construction, garnered community support, and token holders were truly deciding the network's direction with their votes. At that moment, the promise of DPoS appeared to be deliverable—democracy and efficiency could coexist.

However, good mechanisms require good governance to complement them. DPoS provides us with a framework, but how to operate within that framework remains an unanswered question.

The Structural Dilemma of DPoS Governance

Breakthrough in On-chain Governance

The first two years after the activation of the EOS mainnet were the closest DPoS governance came to its ideal state. BPs were vigorously campaigning, node teams came from all over the world, community discussions were lively, and ecological projects surged. On-chain transaction volumes once ranked among the top of global public chains, and token holders were full of hope for the network's future.

During this period, EOS's DPoS governance also exhibited its truly groundbreaking value—on-chain governance achieved real execution power for the first time.

Before this, most blockchain governance was limited to off-chain discussions—the community could debate but could not execute directly. EOS changed this: token holders could vote to replace underperforming BPs at any time; BPs could freeze stolen accounts, execute arbitration decisions, and drive protocol upgrades. Early EOS was able to freeze multiple stolen accounts through BP multi-signatures, a task almost impossible to accomplish on traditional public chains. For the first time, blockchain had a governance mechanism reminiscent of governmental execution power—rules were not just written in a white paper, but could genuinely be enforced.

However, this efficient execution power did not last long, as the development of voting led to another side—the centralization of power—resulting in the formation of vote banks.

The Triangle Dilemma and Vote Banks

In its early days, EOS attempted to constrain power through an on-chain constitution (EOS Constitution) and an arbitration organization (ECAF), but both failed due to a lack of enforcement mechanisms. This is not just a design flaw; it exposes a deeper structural dilemma within DPoS—efficiency, decentralization, and fair governance cannot all be maximized simultaneously.

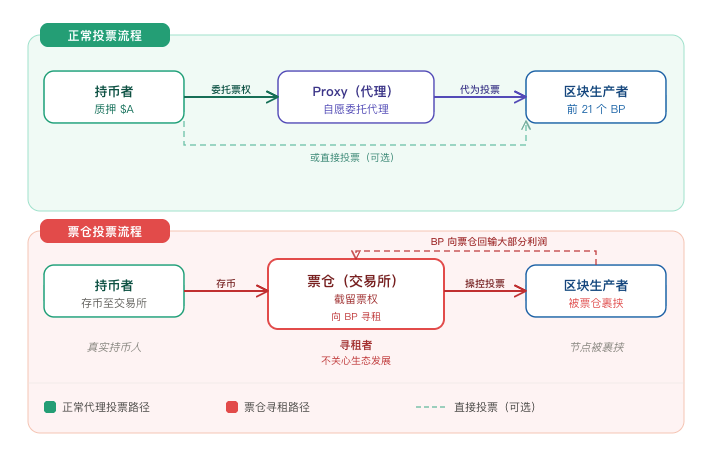

Currently, the first 21 nodes of the Vaulta network show a gradual decrease in enthusiasm among some nodes that had gained prominence early on in governance, yet they hold decision-making power, which is inherently contradictory. To achieve high efficiency, the number of nodes must be small, but the fewer nodes there are, the easier it is for power to concentrate; to ensure democracy, voting power is distributed based on token holdings, but the more tokens one holds, the greater their voting power, thus the vote banks have the most say; nowadays, nodes almost entirely rely on the votes from vote banks with little of their own holdings, which leads to nodes effectively becoming representatives of the vote banks rather than communicating the opinions of ordinary token holders.

To understand this problem, one must first grasp the proxy voting mechanism of DPoS. Under the DPoS system of Vaulta, token holders have two ways to participate in governance: one is to vote directly for the BPs they support; the other is through the Proxy mechanism, delegating their voting rights to a third-party proxy, who exercises them on their behalf. The design of proxy voting aims to lower the participation threshold for ordinary token holders—after all, not everyone has the time and energy to continually track the performance of the BPs.

However, in practice, this mechanism has given rise to "vote banks"—third-party institutions or individuals that aggregate a large number of proxy voting rights to extract benefits from BPs. Vote banks are not typical token holders but rather governance rent-seekers: they do not care about the technological development of the chain, nor the long-term health of the ecology; they only care about stable voting power income. To maintain their seats among the top 21, BPs must pay block rewards as returns to the vote banks. As a result, the primary service targets of nodes have thus transformed from the token-holding community to vote banks, leaving ordinary token holders entirely voiceless in governance.

On-chain Voting, Off-chain Decisions

A deeper issue lies in the fact that EOS's governance has had a fundamental break from the beginning—there are on-chain voting mechanisms, but real decision-making flows off-chain.

Major decisions are made through consensus in Telegram groups, private meetings, and informal channels, and then completed in the form of on-chain voting. Ordinary token holders only see the results, not the process—who exerted influence, how interests were exchanged, and what the basis for decisions was, all remain difficult to trace. On-chain records voting; off-chain governance occurs. The gap between the two has created an unbridgeable chasm between the so-called "decentralized governance" and its true vision.

This chasm was bridged during prosperous periods by soaring token prices and a vibrant ecology. But it never truly disappeared. And when prosperity wanes, what is laid bare before everyone is just chaos.

The DPoS practice on EOS has demonstrated that on-chain governance mechanisms can operate in reality, but under a voting system based on token weight, issues such as power concentration and interest alliances easily arise. This experience, alongside other factors, has influenced the design direction of subsequent public chains, making new generation projects like Solana, Aptos, and Sui more inclined to adopt PoS combined with Byzantine Fault Tolerance consensus structures to strengthen the security and determinism of the consensus layer, thereby reducing dependence on on-chain voting governance mechanisms.

These reflections are valuable to the entire industry, but for EOS, the problems have never remained theoretical—they have walked step by step to today's crossroads on their mainnet, with real communities, real assets, and real governance games.

After EOS was renamed Vaulta, the historical governance challenges will not automatically dissolve simply due to a brand renewal. To understand why we propose this plan today, we must first confront the real situation that Vaulta is currently in.

Power imbalances have never been a new issue. History has proven that the solution does not lie in overthrowing elite governance but in establishing real and effective checks and balances for it. This is the starting point for our proposed solutions.

Democracy First: Restructuring the New Order of Vaulta DPoS Network Governance

We have observed that during the turbulent period of the foundation transition, a group of community members who genuinely care about the development of the Vaulta ecosystem spontaneously formed the community governance organization ECF (EOS Community Foundation). Most of its members have been part of the network since the EOS era, representing the position of token holders. They now seek to consolidate the community's voice, finding a way forward for the ecology during this vacuum period without a central coordinator. After careful consideration and thorough observation of the ECF organization, Vaulta Labs and Treasury have decided to incorporate it into network governance as part of optimizing DPoS governance—accepting oversight and returning power to the community.

About Treasury

First, it is necessary to clarify the positioning of the Treasury. The Treasury is a public asset reserve independent of the BPs, Vaulta Labs, and the former Vaulta Foundation, with its core responsibility being to continuously create long-term value for the ecosystem while ensuring asset safety. During the foundation period, the primary function of the Treasury was to support strategic development for the network, ensuring that the network could operate normally even under adverse conditions while generating returns through proactive investment operations and using profits to continually repurchase $A.

Currently, the stance of the Treasury is: while prudently managing assets, it actively transforms them into tangible driving forces for promoting ecological governance and sustainable development, rather than letting money sit idly.

First Step: On-chain Staking, Sustaining Asset Growth

The Treasury will first address the funding issues for network development by swiftly pulling attention away from the mud pit of profit-sharing disputes. The assets currently held by the Treasury primarily originate from the specially established RAM Ecosystem Fund in the 2024 EOS new token economy program and additional tokens obtained through market-making buybacks. The total size has now exceeded 350 million $A, with a portion allocated according to the plan in the white paper for the $V (RAM) market, another part designated for market-making, custody, marketing, and exchange listing funds, and the remaining assets managed by the Treasury.

Currently, the Treasury plans to lock 220 million $A in REX. Locking means that selling tokens will become transparent, so this portion of locked assets can also be viewed as the entire ecosystem's confidence in $A.

REX (Resource Exchange) is the on-chain staking system on the Vaulta mainnet—token holders can deposit $A into REX to receive ongoing on-chain staking rewards, with the minimum lock-in period being 21 days, and returns coming from the network's pre-allocated staking reward pool.

Depositing 220 million $A into REX is the first step in obtaining development capital for the network without utilizing existing cash reserves.

Second Step: Introducing Democratic Oversight Mechanisms, Returning Power to the Community

The Treasury does not participate in network governance. We introduce the community governance organization ECF to supervise the existing BPs and rebuild the effectiveness of the DPoS governance mechanism.

The initial seven-member temporary committee of ECF comes from the Chinese, English, and Korean communities, entirely independent of other administrative organizations in the network, solely representing the community's voice. Members will rotate every six months, with a maximum consecutive term of 12 months to prevent the entrenchment of power. Formal committee elections will commence six months after the Treasury vote bank activates, with community members holding at least 10,000 $A eligible to participate, while heads of interest-related organizations cannot run for the ECF committee. Specific details will be disclosed by ECF over the next two weeks.

ECF represents the broad base of token users, conducting assessments and distributing voting rights for BPs through the Proxy voting mechanism—once the Treasury deposits into REX generate on-chain voting rights, they will be delegated to ECF, making it one of the largest single voting agents by voting power within the Vaulta network. ECF will produce transparent BP scoring standards through its independent communication channels, assigning varying weights to scores based on node rankings, and those with higher scores will receive more votes, directly linking voting power to actual contributions. This measure fundamentally addresses the dilemma of vote banks controlling nodes: on one hand, it relieves nodes from the cost pressure of sharing profits with vote banks, enhancing their earnings; on the other hand, nodes will need to actively participate in network governance to achieve higher voting. Simultaneously, the community will gain more voice in the network's development through assessing BPs. Centralizing power under decentralized management while simultaneously decentralizing authority is actually a more realistic exploration of the DPoS governance mechanism.

Third Step: Network Incentives, Revenue Reinvested in the Ecology

According to current yield estimates, funds deposited by the Treasury in REX are expected to generate about 20 million $A of on-chain revenue each year. This revenue will be used entirely to incentivize BPs that actively participate in governance and other ecological projects that contribute to the network, aiming to become positive incentives for sustainable ecological development.

The distribution of these funds will also introduce an oversight mechanism: ECF has the authority to review every application for on-chain funds within the network and has a veto right over Treasury's expenditure decisions.

A clear boundary of power is established among the three: the Treasury manages assets without participating in governance, ECF represents the community exercising oversight and vetoing rights, and BPs are responsible for network maintenance and governance; any resolution must gain majority support of 15/21—no single party can dominate the others.

Of course, whether this mechanism can truly take effect ultimately depends on the continued participation of the community and the support of the BPs. In this regard, the community has proposed a clear three-stage roadmap for governance reconstruction: the first stage is to break the chain of interests in BP vote buying and selling, purifying the governance environment while alleviating the profit dilemmas faced by BPs; the second stage is to activate the contribution incentive mechanism for BPs, ensuring that real contributions receive corresponding rewards; the third stage is to gradually reduce the nodes' dependency on the ECF vote bank, driving voting power back to decentralization. We encourage BPs to establish close communication with ECF, allowing the network to swiftly return to a healthy state.

Conclusion: Mechanism is Trust

To trust a person, one must judge their character. To trust a mechanism, one merely needs to verify its rules.

Every link in this plan—Treasury's on-chain staking, ECF's voting rights delegation, BP's scoring standards, the rules of incentive distribution, the conditions to trigger veto rights—can all be verified on-chain, overseen by the community, and held accountable publicly. It does not rely on anyone's moral self-awareness or any organization's unilateral promises.

This is Vaulta's monumental historical feat, the foundation for reconstructing market trust, and our responsibility to everyone still here.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。