Written by: Spinach Spinach

On March 5, 2026, the American Bankers Association (ABA) did something rare: it publicly rejected a compromise solution negotiated by the White House for several weeks. Just two days earlier, Trump had openly warned on Truth Social that banks were "hijacking legislation."

It is uncommon for an industry lobbying group to openly confront the president—this is not a frequent occurrence in American politics. Whatever led bankers to make such a decision must be significant.

What made them so anxious was a piece of legislation called the CLARITY Act (H.R. 3633, officially titled the Digital Asset Market Clarity Act).

Why are banks so fearful of this act? This article will break it down logically.

"A life-and-death struggle over $6.6 trillion in deposits."

Executive Summary

The essence of the CLARITY Act is not regulatory reform but a redistribution of intermediation rights: it grants non-bank institutions (cryptocurrency exchanges, DeFi protocols, crypto-native custodians) equal federal compliance status to banks, directly breaking the monopoly moat built by the banking industry over the past century based on licensing barriers.

The core fear of bank lobbying is "deposit migration." If stablecoins are allowed to pay yields, $6.6 trillion in deposits face the risk of transfer; deposits are the raw material for all bank operations—losing deposits would collapse banks' credit capacity, net interest margin models, and fee systems.

The CLARITY Act precisely targets the three layers of the banks' moat for dismantling. On the deposit side: the act grants stablecoins legal status and allows platforms to offer yields; on the clearing side: the act excludes decentralized activities from registration requirements, enabling DeFi to legally circumvent the banking clearing network; on the custody side: the act establishes a federal custodian framework, opening the $32.5 billion custody market to non-banks. With these three assaults combined, the monopoly moat of banks is being systematically dismantled.

I. What is the CLARITY Act—who's cheese is it moving?

The CLARITY Act (Digital Asset Market Clarity Act, H.R. 3633) is the most significant cryptocurrency regulatory legislation passed by the U.S. Congress to date. On July 17, 2025, it was passed in the House with a bipartisan majority of 294 votes to 134, and is currently stalled in Senate negotiations.

The core logic of the act can be summarized in one sentence: end the regulatory vacuum and clarify who regulates whom.

For a long time, the U.S. cryptocurrency industry has resided in a jurisdictional gray area between the SEC (Securities and Exchange Commission) and the CFTC (Commodity Futures Trading Commission), akin to playing in a game without referees.

The core provisions of the act are divided as follows:

CFTC Gains:

Exclusive regulatory authority over the spot market for "digital commodities," including registration oversight of digital commodity exchanges (DCEs), brokers, and dealers.

Assets like Bitcoin and Ethereum, recognized as "decentralized and mature," will fall under this framework.

SEC Retains:

Regulatory authority over digital assets that are classified as "investment contract assets," i.e., tokens that have not yet reached sufficient decentralization standards.

However, the act clearly outlines a "de-securitization" path—issuers can notify the SEC that the asset has achieved or will achieve "maturity" standards within four years, thus falling out of the securities framework.

Federal Access for Non-Bank Institutions:

This is the clause banks fear the most. The act allows financial holding companies and compliant banks to conduct digital commodity businesses while also permitting non-bank institutions to obtain registration as "qualified digital asset custodians," subject to federal or state oversight.

In other words, crypto-native entities such as Coinbase, Ripple, and BitGo will have the opportunity to obtain federal licenses equivalent to traditional banks for the first time.

While the CLARITY Act remains stalled, matters have accelerated from another front: within just 83 days, 11 crypto companies, including Circle, Ripple, BitGo, Paxos, and Fidelity Digital Assets, submitted applications for national trust bank licenses to the OCC (Office of the Comptroller of the Currency).

The banking industry has realized that even if legislation is stalled, competitors are completing the same layout through regulatory pathways.

This is a nightmare for the bank lobbying group:

If the act passes, they will no longer be facing "barbarians in the regulatory gray area," but formally licensed opponents competing under the same rules in the same arena.

II. The Triple Profit Moat of Banks: A Dissection of the Century-old Intermediation Tax Business Model

To understand why banks are so stubbornly holding on, one must first understand how banks make money.

The net profit of the U.S. banking industry in 2024 is projected to be $268.2 billion, and this money comes from three pillars:

Moat One: Deposit Monopoly—Earning Interest Spread

This is the foundation of the banking business model. Banks absorb residential deposits at near-zero cost (savings rates of 0.5%-2%) and then lend it out at much higher rates (mortgage rates of 6%-7%, consumer loan rates of 15%-25%), with the interest spread being the net interest margin (NIM).

The average NIM for the U.S. banking industry in 2024 is projected to be 3.22%, meaning a net profit of $3.22 for every $100 in assets annually. JPMorgan Chase is expected to have total revenue exceeding $177 billion in 2024, where the core driver is this sprawling deposit-and-loan interest spread machine.

The premise of this model is that deposits can only be placed in banks, as there are no alternatives.

Moat Two: Payment Clearing Licenses—Charging Tolls

Every bank transfer and every card swipe goes through a bank-led clearing network. The interchange fee is the most direct expression of this system—merchants pay banks a fee of 1%-3% for each card transaction, while consumers are completely unaware.

In 2024, the U.S. banking industry collected about $4.88 billion just in overdraft fees, which is just a visible fraction; the overall "toll" system of the payment network is much larger than this.

The premise of this model is that payments must go through the bank account system.

Moat Three: Custodial Qualification Barriers—Earning Service Fees

The global custody asset size is approximately $230 trillion, and the U.S. custody and securities services industry generated $32.5 billion in revenue in 2022.

Pension funds, sovereign wealth funds, and insurance companies are legally required to have their assets stored in institutions with specific regulatory qualifications—qualifications that only banks and a few licensed entities possess.

The custody business of State Street, BNY Mellon, and JPMorgan is a product of "institutional necessity": it is not because their services are the best, but because there are no other compliant options.

These three moats share a common characteristic: their core competitive advantage is not technology, nor efficiency, but regulatory barriers. Once these barriers disappear, the competitive advantage is lost.

III. How the CLARITY Act Precisely Attacks These Three Moats

Here is the most crucial causal chain of the entire story.

Each provision of the CLARITY Act precisely dismantles a layer of the banks' moat.

Attacking Moat One: Stablecoins Allow "Money" to Bypass Bank Accounts

Stablecoins are digital currencies pegged to the dollar at a 1:1 ratio, with a total circulation exceeding $230 billion and a daily trading volume of approximately $30 billion.

Under the current legal framework, stablecoins exist in a gray area, unable to pay interest or replace bank deposits. However, the CLARITY Act's legalization of stablecoins changes this equation.

The mechanism is conveyed as follows:

Step One (Trigger):

The CLARITY Act acknowledges the legal status of "permitted payment stablecoins" while allowing other intermediary platforms to provide yields or rewards for users holding stablecoins.

Step Two (Conduction):

This means users can convert bank deposits into stablecoins and earn yields on crypto platforms that exceed bank savings rates—which is precisely the "deposit migration" scenario banks fear the most.

Step Three (Quantifiable Consequences):

Empirical research from the New York Fed found that banks already participating in the stablecoin ecosystem (as reserve custodians) saw a decline of approximately 14 percentage points in their loan-to-asset ratios compared to similar banks—because these banks must hold more liquid reserves to meet stablecoin redemption demands, which in turn compresses the scale of available funds for lending.

Amplifier:

Standard Chartered analysts independently estimated that if yield provisions are implemented, $500 billion in deposits could migrate from traditional banks to stablecoin products by 2028.

The ABA further cited research predicting extreme scenarios could result in a loss of up to $6.6 trillion in deposits, equating to the elimination of approximately $1.5 trillion in credit capacity, with small business loans shrinking by $110 billion and agricultural loans by $62 billion.

The $6.6 trillion figure is an extreme scenario forecast commissioned by the ABA, not the baseline prediction; Standard Chartered's $500 billion is a more conservative estimate within the 2028 time window.

The two figures are based on different metrics, but the direction is consistent: deposit loss is a real structural threat, not mere bluster.

Attacking Moat Two: DeFi Turns Payment Clearing into Driverless Software

DeFi (Decentralized Finance) automatically executes financial transactions via smart contracts on the blockchain, without need for clearinghouses or bank intermediaries.

The total locked value (TVL) in DeFi is projected to be about $270 billion in 2025, with an annual growth rate of 31%. More crucially, the speed of cross-border remittances in DeFi is 4.3 times that of the traditional SWIFT system.

The CLARITY Act explicitly excludes decentralized activities like "verification nodes" from registration requirements but retains oversight for anti-fraud and anti-manipulation.

This means DeFi protocols can operate within a legal framework without having to pay tolls to the existing banking clearing network.

Attacking Moat Three: Crypto-native Custodians Will Hold Federal Licenses for the First Time

The most direct dismantling of the moat occurs in the custody segment.

The CLARITY Act establishes a framework for "qualified digital asset custodians," allowing non-bank entities to obtain compliant status through registration. Coinbase, BitGo, and Fidelity Digital Assets are accelerating this process through OCC license applications.

Once these entities hold federal licenses equivalent to banks, institutional clients (pension funds, sovereign wealth funds) will no longer have a compelling reason to choose traditional banks for custody of their digital assets.

The $32.5 billion U.S. custody market will open up to non-bank entities.

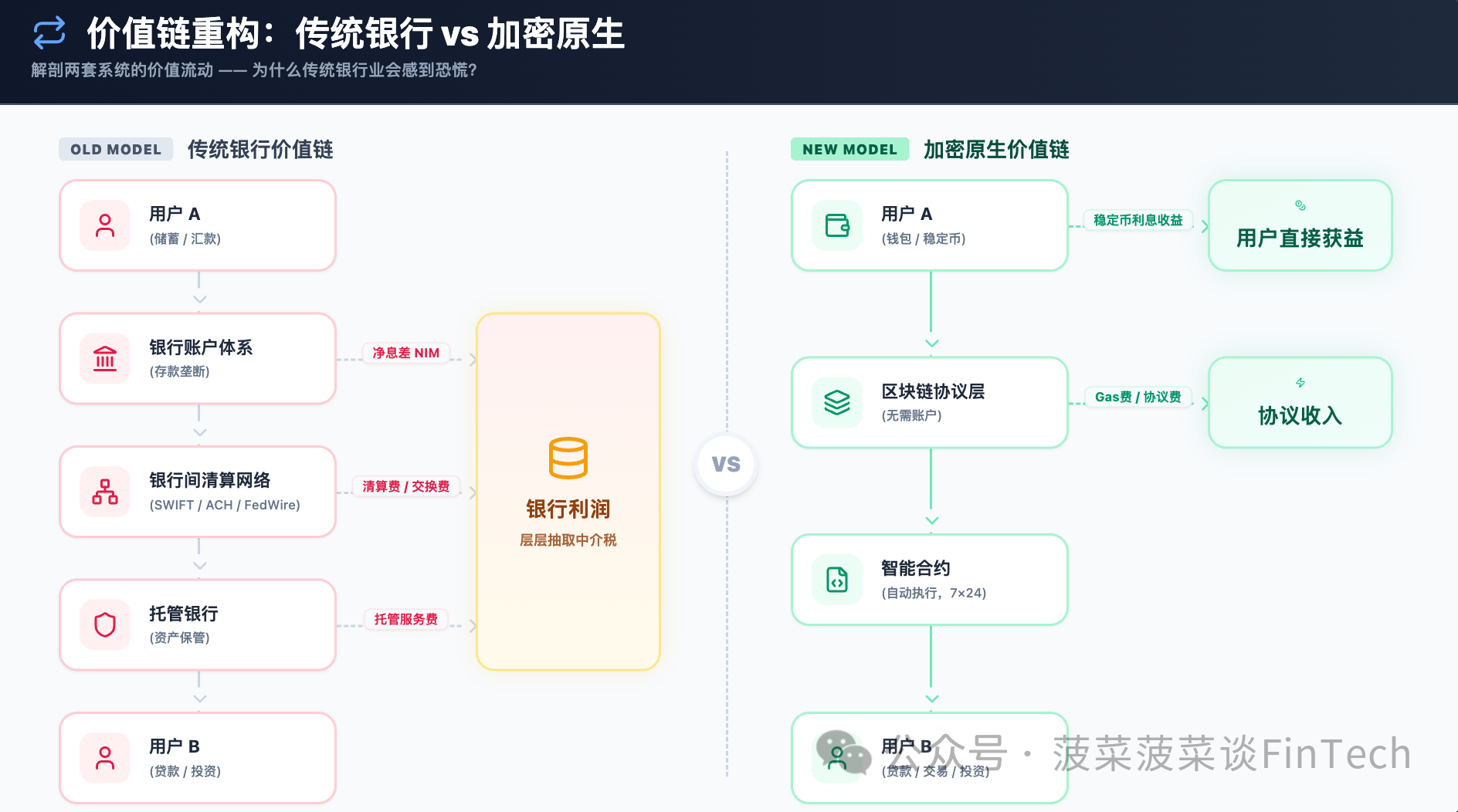

IV. Old Business Model vs New Business Model: Fundamental Differences in Value Chain Structure

The core difference between the two financial systems lies not in products, but in the necessity of the intermediary layer.

In the old model, each layer is a checkpoint, and each checkpoint incurs a fee.

When a user transfers money from A to B, it passes through three nodes: "account-opening bank → clearing network → receiving bank," with each node charging fees, and each transaction is subject to a T+1 or T+2 settlement period.

In the new model, A and B interact directly through wallet addresses, with blockchain protocols replacing the intermediate three-layer structure, compressing settlement time from "business days" to "seconds," and reducing cross-border remittance costs from 3%-7% to less than 1%.

The value chain structure difference between the two models fundamentally represents whether the "intermediary layer exists":

- In the old model, banks are an indispensable trust machine.

- In the new model, trust is coded and outsourced to cryptography via a blockchain consensus mechanism.

The banking business model has not been overturned; it has been circumvented.

Core Conclusions

Having read up to this point, we can connect all the dots into a single line.

The story begins with the banking industry's business model; for a century, the core profit formula of American banking has never changed:

Monopolize deposit raw materials → Charge tolls via a regulated clearing network → Lock in institutional clients with exclusive custodial qualifications.

The industry-wide net profit of $268.2 billion in 2024 essentially represents the output of this monopolistic intermediation system over the course of a year.

The emergence of cryptocurrency technology represents the first true threat on a technological level:

- Stablecoins allow "money" to exist outside of bank accounts;

- DeFi enables payment clearing without a bank intermediary;

- Crypto-native custodians allow institutional assets to be held outside traditional banks.

These three points directly attack the three core payment nodes of the bank's value chain.

The danger of the CLARITY Act lies in:

It legally legitimizes all three of these threats. Once crypto-native institutions obtain federal licenses, the technological threat escalates to an institutional threat—banks will lose their last line of defense, the moat built from regulatory barriers.

In this battle for city defense, the bank lobbying group wins time but loses the long-term game.

They can slow down legislation but cannot stop the permeation of technology; they can block one law but cannot prevent 11 competitors from applying for licenses with regulators simultaneously.

The real issue has never been whether the CLARITY Act passes, but whether traditional banks can maintain irreplaceability at any node once the value chain of digital-native finance ultimately becomes infrastructure.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。