Author: Eric, Foresight News

On the evening of March 26, Beijing time, The Wall Street Journal reported that the American mortgage finance giant Freddie Mac will accept cryptocurrency mortgages for the first time, in collaboration with Coinbase and the mortgage company Better Home & Finance Holding Co. approved by Freddie Mac.

This move, seen in the Web3 space as another recognition by traditional financial institutions, has been almost drowned out by the skepticism of a vast number of internet users...

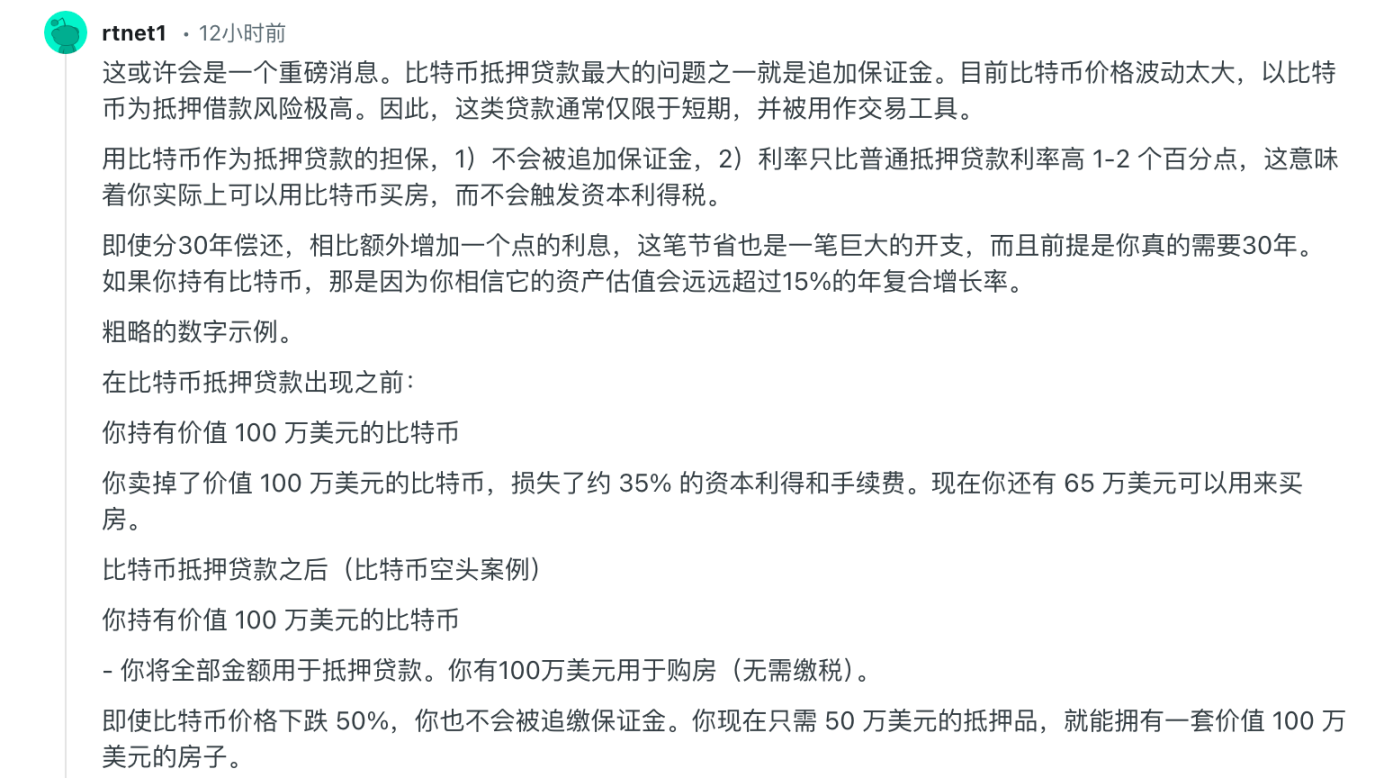

According to relevant reports and an announcement from Better, this loan is only for the "down payment" and aims to solve the trouble that homebuyers face when they need to sell assets for the down payment and the associated tax issues. Currently, the supported cryptocurrencies are only Bitcoin and USDC, requiring borrowers to transfer the coins to Coinbase's custody address, with collateralization rates of only 40% and 80%, respectively. Additionally, the interest rates for cryptocurrency mortgages are 0.5% to 1.5% higher than typical home mortgage interest rates.

However, the good news is that borrowers do not need to supplement their collateral due to a drop in Bitcoin prices, as liquidation of collateral only occurs after 60 days of delinquency. But the use of USDC as collateral with an 80% collateralization rate is somewhat concerning.

This loan product is not designed for mortgages but for down payments. In other words, it gives you the "opportunity" to mortgage Bitcoin to borrow money for the down payment and then mortgage the purchased house to borrow money for the remaining amount, thereby taking on two loans.

Let’s do a simple calculation. Suppose you want to purchase a property priced at $400,000, with a down payment ratio of 20%, which is $80,000. If you mortgage Bitcoin for this $80,000, you will need to mortgage $200,000 worth of Bitcoin. As of March 26, the average rate for a typical 30-year fixed-rate mortgage in the U.S. is about 6.38%, while the rate for borrowing against Bitcoin could be as high as nearly 8%.

On Reddit, many Americans find this baffling: If I have $200,000 worth of Bitcoin in my portfolio, how can I not come up with $80,000 for the down payment? If I can’t afford the down payment, how could I possibly have money to buy Bitcoin?

Of course, there are also supportive voices; some netizens express that high capital gains taxes mean that if you sell $1 million worth of Bitcoin, you may only net $650,000. However, through this method, it is possible to leverage your position to buy property while continuing to hold Bitcoin, providing another option for many people.

Although there are many supporters, their descriptions suggest that they are at least of middle-class standing and have a comparatively deep understanding of finance and taxation. This has sparked discussions about whether the system is "helping the rich and not the poor."

Axios also mentioned in its report that this product is "not a broad-based first-time homebuyer product," implying that it may provide additional help to those with some economic capacity but does not address a more pressing issue:

The mortgage delinquency rates for low-income populations have risen sharply since the end of last year.

Many ordinary people on Reddit also have strong opinions on this. According to the latest report released by Cotality in February 2026, the national mortgage delinquency rate (30 days overdue or more) as of December 2025 is flat compared to December 2024, remaining at 3.2%. The Federal Reserve data shows that the single-family mortgage delinquency rate in the fourth quarter of 2025 is 1.78%.

However, the data for FHA loans (a government-backed loan program designed to help low- and moderate-income people and first-time homebuyers) is starkly different. In the third quarter of 2025, the FHA loan delinquency rate reached 10.78%, up 21 basis points from the previous quarter, with serious delinquency rates increasing by nearly 50 basis points year-on-year. Additionally, the FHA loan overdue rate has exceeded 11%, accounting for 52% of all seriously delinquent loans.

The skepticism centers on whether Freddie Mac is using a bigger risk to attempt to cover up an already spreading risk?

As early as mid-2025, the Federal Housing Finance Agency directed Freddie Mac and Fannie Mae to study whether cryptocurrency assets should be considered in loan approval assessments. At that time, many scholars in the financial industry expressed opposition, with the core concern being that relaxing standards seems reminiscent of the conditions leading up to the 2008 subprime mortgage crisis.

In the U.S., paying off a mortgage early incurs a significant prepayment penalty, meaning that in order to take out a loan, you must lock up your Bitcoin for a long time. If you only have 5 Bitcoins and you mortgage all of them to buy a house, you can’t access them for 30 years; it’s likely you wouldn’t want to do that. However, if you have 200 Bitcoins, mortgaging 50 or even 100 Bitcoins to improve your living situation seems much more reasonable, after all, you are certainly in for the long haul and will not sell regardless.

For wealthier individuals with better cash flow, being able to mortgage Bitcoin for home purchasing provides a means to leverage that doesn't disrupt their investment portfolio, allowing them to continue investing in other assets or simply providing asset substitution capability. But what poorer individuals do not understand is why you think I cannot afford to buy a house because I bought Bitcoin?

Embedding Bitcoin into the intricate traditional financial system is a field worth exploring but fraught with unknown risks. To borrow a playful comment from a Reddit user, when Bitcoin really becomes "too big to fail," will it also become the trigger for the next explosion?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。