Original Author: Sanqing, Foresight News

On March 24 (Eastern Time), the closing price of stablecoin issuer Circle (CRCL) on the New York Stock Exchange was reported at $101.17, with a daily drop of over 20%, marking the largest single-day decline since its listing. Its largest distribution partner, Coinbase (COIN), also fell nearly 10%, with a Nasdaq closing price of $181.04.

The trigger for the sell-off was the leak of details from the latest draft of the Clarity Act, which proposes to prohibit digital asset service providers from "directly or indirectly" paying interest on stablecoin balances and forbids any structures that are "economically or functionally equivalent to interest."

Image source: Tweet by Eleanor Terrett, host of Crypto in America and former Fox Business reporter

On the same day, its competitor Tether announced that it has hired one of the Big Four accounting firms to conduct its first complete financial audit (including USDT reserves).

"Directly or indirectly," which five words block whom

The draft text was submitted for review by representatives of the cryptocurrency industry during a closed-door meeting on March 24, with banking representatives following up for review the next day. Reporter Eleanor Terrett disclosed the details of the draft in a related email on X.

USDC itself has never paid interest, and Circle, as the issuer, has never paid any earnings to coin holders. So, how does the draft prohibiting interest payments by issuers relate to Circle?

The draft's "range" goes beyond just issuers. The real entity paying users interest is Coinbase.

According to the profit-sharing structure disclosed in Circle's prospectus, 100% of the reserve interest from USDC held by users on the Coinbase platform belongs to Coinbase; for USDC circulating outside the platform, 50% of the reserve interest belongs to Coinbase.

Coinbase distributes the vast majority of the reserve profits obtained within the platform to users in the form of "USDC Rewards." According to an analysis by Columbia Law School, Coinbase's profits from USDC Rewards are very thin, retaining only about 20 to 25 basis points of the interest margin.

The "directly or indirectly" and "economically or functionally equivalent to interest" clauses in the Clarity Act draft are specifically designed to close this loophole.

This ban may have a limited financial impact on Coinbase, and it might even be positive. Coinbase is both a shareholder of Circle and also retains pure profit-sharing of 50% of reserve income outside the platform, so its incentive to promote USDC will not disappear as a result.

However, USDC's competitors include not only USDT but also the US dollar itself.

USDC Rewards allow USDC to effectively play the role of a "high-yield digital savings account." This is also one of the driving factors for USDC's growth rate outperforming USDT for two consecutive years. Once this channel is closed, if the earnings from holding USDC drop to zero, the willingness to hold it will weaken.

The transmission path of shrinking demand points to Circle. With weakened holding motivation from the retail side, the growth rate of the total circulation of USDC will slow down, and the speed of reserve pool accumulation will decrease, thereby beginning to destabilize Circle's income growth narrative based on scale expansion expectations.

The draft also retains an exemption for "activity-based rewards," allowing rewards linked to payments, transfers, or platform usage. However, this is a completely different product from the current “hold and earn” model.

Moreover, the expression "economically or functionally equivalent to interest" is too vague, leaving significant room for interpretation by future regulatory agencies, and there is also a risk of tightening the boundaries of activity-based rewards.

Another pressure on the same day

If the Clarity Act draft aims to dismantle Circle's growth flywheel, then Tether's audit announcement on the same day points to another competitive advantage for Circle.

The long-standing differentiated narrative of USDC has largely been built on compliance.

Circle regularly receives reserve proofs issued by top accounting firms, and during the years when regulatory uncertainty suppressed Tether, "we are the transparent and compliant one" was a very effective card for institutional clients and compliance-sensitive exchanges.

On the other hand, Tether has responded to external concerns with quarterly proof rather than genuine audits; S&P Global once labeled USDT's credit rating as "weak" in 2025 and warned of the risk of under-collateralization as Bitcoin prices decline further.

Additionally, the GENIUS Act requires large stablecoin issuers to undergo annual independent audits, and Tether's hiring of the Big Four seems more like a response to this legal obligation. Regardless of the motivation, the timing of this signal is enough to compound negative sentiment in the market.

USDC has outpaced USDT at a higher growth rate for the past two years. The narrative of compliance and transparency is one of the most important driving forces behind this round of growth. Tether's hiring of the Big Four for audits has not yet commenced, and the outcome is far from certain. However, if the audit is successfully completed, it is obvious that the compliance premium on which Circle relies to maintain its growth advantage will be compressed.

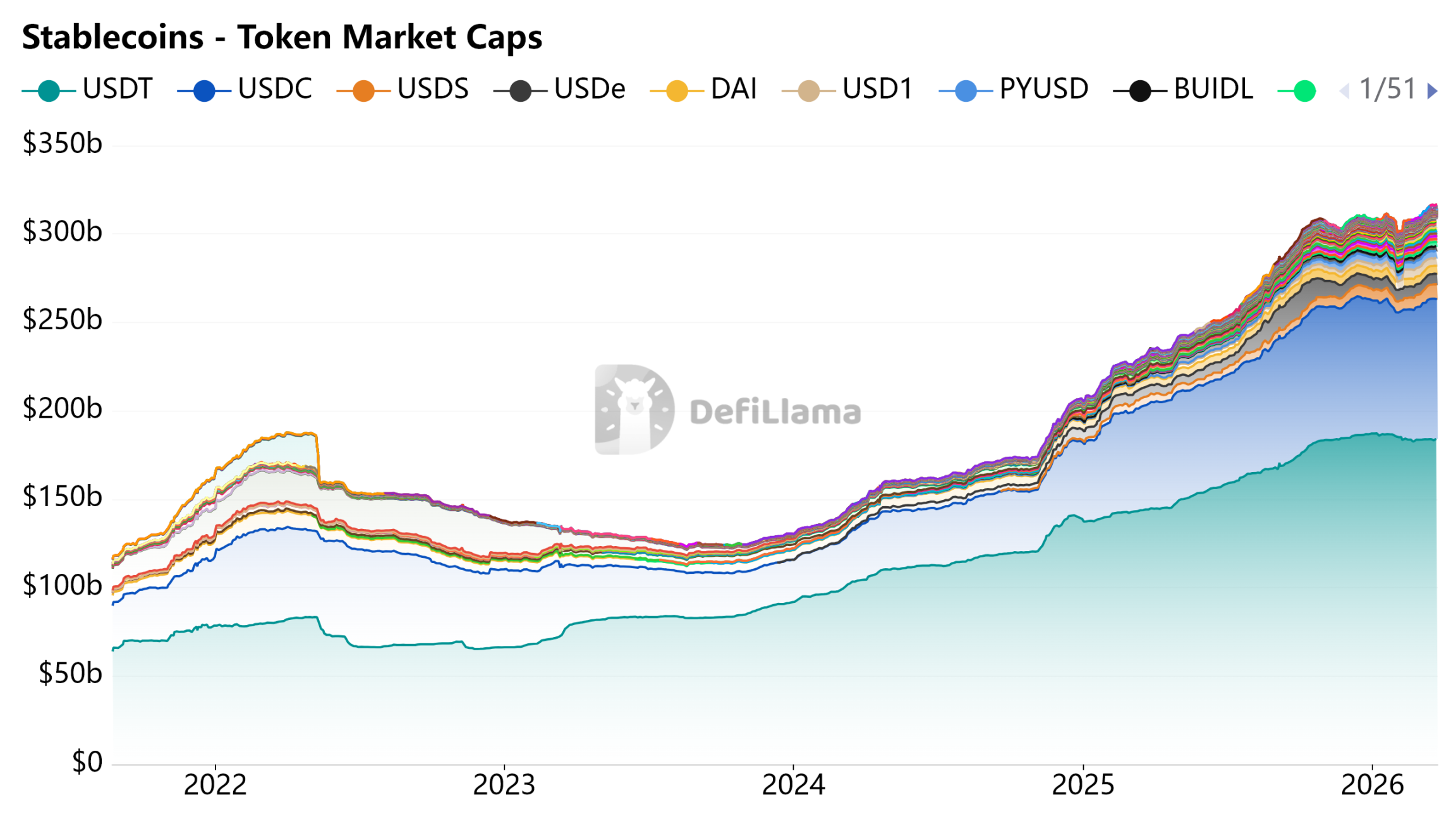

Image source: DeFiLlama - Stablecoins

Payment tool, not a savings account

Circle's value benefits from a growth model where income incentives drive users to hold USDC, scale expansion thickens the reserve pool, and reserve interest supports income growth. This model can work only if stablecoins are allowed to play the role of income-generating assets or savings deposits.

The Clarity Act draft negates this premise at the legislative level.

Without income incentives, the growth of USDC's scale must rely on the natural penetration of real payment scenarios. This path is not unfeasible, but it is much slower and more uncertain than being driven by income.

Compliance has secured Circle's license, but it cannot sustain its growth model. The answers provided by bankers are very clear: stablecoins can exist, but they cannot earn interest.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。