Compiled by: Block unicorn

In the past few months and weeks, RWA cycles have become one of the hottest topics in the cryptocurrency space.

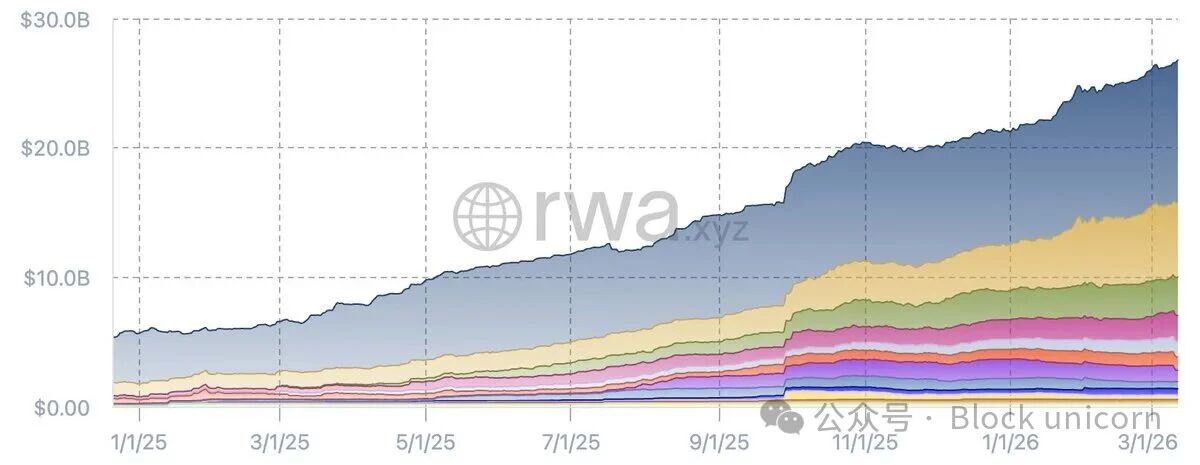

Why It Matters

The total value of RWAs has grown about five times in the past 12 months, reaching an all-time high of $26.7 billion.

Strong upward momentum

Thanks to tokenization platforms like Centrifuge and Securitize, top asset management firms like BlackRock, Franklin Templeton, and Apollo have been able to tokenize their products and put them on-chain—primarily to meet cryptocurrency users' demand for diversified investments beyond crypto assets.

As a result, the supply side of RWAs seems to have been largely addressed, and attention has shifted to the next challenge: finding new buyers who can drive the next phase of market growth.

Compelling Reasons

RWA cycles are increasingly seen as one of the most reliable ways to drive this demand. By unlocking leverages from low-correlated yield sources, RWAs provide advantages that traditional finance (TradFi) cannot offer:

Rapid, accessible, programmable leverage on alternative assets, which typically requires lengthy negotiations in traditional markets and is limited to large institutions.

Behind the Scenes

To better understand the infrastructure and applications of RWA cycles, we spoke with the following people at Blockstories:

LUKE CHMIEL from Morpho, whose modular lending infrastructure is the cornerstone of many leveraged RWA strategies.

Marcin Kazmierczak, co-founder of RedStone, which is developing price oracles, ratings, and liquidation systems tailored for tokenized RWAs.

Senior protocol strategist Anlin Zhang from Gauntlet, one of the leading risk management firms in the cryptocurrency space, responsible for overseeing leveraged RWA strategies with tens of millions of dollars in capital.

Co-founder Sonya Kim from 3F, a platform that allows investors to create leveraged RWA positions covering various RWAs with a single click.

David Vatchev, head of RWA tokenization at Fasanara Capital, a leading institutional asset management firm managing over $5 billion in assets and operating a tokenized private credit fund, mF-ONE.

Nuno Cortesão, co-founder and CEO of Zharta Finance, a loan infrastructure provider that recently partnered with Securitize to announce the first on-chain asynchronous redemption feature for tokenized security leveraged positions.

Here are the key points we summarized.

1/ Why is the RWA cycle becoming increasingly popular now?

Two things have happened in the past year that made it feasible.

First, on-chain interest rates have plummeted. With reduced speculative activity and fewer participants seeking leverage on crypto assets, the yields from crypto-native lending strategies have decreased, in some cases even falling below traditional money market rates. This has led to more on-chain stablecoin funds seeking effective sources of yield.

“As the speculative frenzy has faded, cryptocurrency prices have fallen, and arbitrage opportunities have diminished, many traditional cryptocurrency yield sources have shrunk. This has prompted DeFi to look for new sources of yield, and RWAs are appealing because they introduce real yields unrelated to the cryptocurrency market and can amplify returns through cycling strategies.

A very simple example of RWA cycle economics

2/ Is yield the only reason investors are interested in RWA cycles?

Yield is just one part of it. The bigger breakthrough of the RWA cycle mechanism lies in its creation of a whole new way to leverage assets that have historically been difficult to finance in traditional markets.

Private credit is a great example. Financing such instruments often requires signing bilateral agreements with banks or specialized lending institutions, extensive underwriting, and slow, fragmented operational processes.

Tokenized private credit is vastly different. Once integrated into lending markets, investors can lend programmatically using their tokenized positions without permission and enhance returns through cycling strategies.

This means that investment strategies previously limited to a handful of institutional investors can benefit a wider array of participants by putting the underlying assets on-chain.

“Ethena demonstrates the power of bringing strategies like basis trading, once limited to hedge funds and institutions, to benefit global investors through on-chain integration. At 3F, we aim to bring similar transformation to leveraged arbitrage trading by building the infrastructure that enables users to cycle through various RWAs.”

—— Sonya Kim, Co-founder of 3F

3/ What is the current state of the RWA trading market?

The market size is still relatively small. According to our conversations, the estimated leverage of RWAs on major lending platforms like Aave, Morpho, and Kamino is about $700 million. For reference, this is a small fraction of the approximately $20 billion in outstanding loans from these lending markets.

In terms of assets, most activity is concentrated on leverage strategies involving tokenized US Treasuries and private credit funds from companies like Apollo Global, FalconX, or Fasanara Capital.

On the demand side, the market is still primarily driven by crypto-native applications.

“Currently, we see demand for on-chain RWAs coming mainly from three areas. First, DeFi native hedge funds, whose use case is leveraged cycles and improved capital efficiency. Second, funds management from L1 foundations and DAOs, seeking diversified yields. A third emerging driver is yield stablecoins, which use RWAs as reserve assets to increase diverse, real-world yield-supported sources.”

——David Vatchev from Fasanara Capital

4/ What is still hindering RWA cycles?

The core limitation is the mismatch between the speed of DeFi and the actual settlement of RWAs. While crypto-native lending markets assume collateral can be priced, liquidated, and sold in a matter of seconds, most RWAs do not operate that way. The settlement cycle for government bonds is T+1. Private credit funds may have 90-day lock-ups or quarterly redemption windows. Moreover, most RWA tokens cannot be freely traded by any liquidator.

“A major bottleneck for RWA cycles is that DeFi is built on atomicity: transactions either execute in a single block or revert. ——Nuno Cortesão, co-founder and CEO of Zharta

Today, asset management firms are addressing this issue by adjusting RWA designs.

“The core design principle of bringing real-world credit on-chain is to align the asset cash flow with the liquidity expectations of the DeFi market. limits, diversified exposures, and integrating characteristics like liquidity arbitrage or enhanced redemption cycles. These measures help bridge the mismatch between RWAs and on-chain lending markets.”

—— David Vatchev, head of RWA tokenization at Fasanara Capital

Nevertheless, other challenges remain. Most DeFi lending markets currently rely on floating interest rates. Since cycling strategies depend on the yield spread between the underlying asset's yield and borrowing cost, any spike in borrowing rates can compress or even completely eliminate this spread, making yields unpredictable and some strategies unfeasible. This is also why an increasing number of lending protocols have begun exploring fixed-rate lending infrastructure.

In addition, the broader framework for integrating RWAs into DeFi is still developing. Lending markets, risk management firms, and infrastructure providers are just starting to develop the models and tools needed to handle RWA cycles at scale.

“Protocols that accept RWAs as collateral typically price risk based on net asset value (NAV) data without fully understanding the underlying credit quality, redemption restrictions, or concentration risks of the collateral pool.”

—— Marcin Kaźmierczak, co-founder of RedStone

Ultimately, no single protocol can solve all these problems alone. To make RWA cycles viable at scale, coordination among various infrastructure providers is necessary.

“To make RWA cycles operate effectively, you need to build a complete tech stack around the asset: a lending market where the asset can be used as collateral, custodians or risk managers capable of adequately underwriting the asset, reliable price oracles, bridge financing from third-party liquidity providers to build leveraged positions in one go, and settlement infrastructure that can actually handle these assets. If these components are not mature and able to work together, the market cannot truly scale.”

—— Sonya Kim, co-founder of 3F

5/ If these challenges are resolved, how will the RWA cycle market evolve?

On the demand side, RWA cycles can broaden institutional participation by allowing institutional investors to increase exposure to their existing assets more efficiently.

“We are actively talking to asset issuers and institutional capital allocators, both of whom are interested in our leveraged RWA strategies. The former want to expand the composability and utility of their tokens on efficient DeFi platforms, while the latter wish to enhance their exposure to existing positions in underlying RWAs.”

——Anlin Zhang, senior protocol strategist at Gauntlet

On the supply side, the range of recyclable assets is expected to expand, but it will not develop uniformly. Duration risk is a decisive constraining factor: the assets that achieve scalability first will be those that can settle quickly and have reliable clearing paths, not necessarily the assets with the highest yields.

“Assets that can thrive are those with short durations and established clearing and secondary market partner ecosystems. This makes tokenized money market funds and short-term treasury products natural frontrunners, as they already have T+1 settlement, daily liquidity, and strong relationships with market makers.”

—— Marcin Kaźmierczak, co-founder of RedStone

Summary of Key Points

As crypto-native yields compress, RWA cycles are gradually gaining market recognition. With arbitrage opportunities diminishing and speculative demand waning, DeFi capital is turning to tokenized RWAs to seek non-correlated yields that can be amplified through leverage.

The market is still in its early stages, but it has begun to take shape. It is estimated that the leverage supported by RWAs on leading DeFi lending platforms like Aave, Morpho, and Kamino is around $700 million, with demand mainly coming from crypto-native participants like DeFi hedge funds and DAO treasuries.

Infrastructure remains a major bottleneck. DeFi lending systems assume instant pricing, liquidation, and settlement, while RWAs have slower redemption cycles, requiring new oracle systems, risk frameworks, and liquidation mechanisms.

If infrastructure challenges are resolved, market size is expected to expand rapidly. By then, tokenized government bonds and money market funds will likely be among the first to be adopted. They settle quickly and have reliable clearing paths.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。