Text | Kaori

Editor | Sleepy.md

In the first three months of 2026, players in the payment sector had a fulfilling time.

On January 11, Google announced the Universal Commerce Protocol (UCP) at the National Retail Federation's annual conference in the United States, aiming to define a universal language for AI Agent commerce. In the same week, Revolut announced it would be one of the first European payment methods compatible with Google AP2, PayPal announced the acquisition of the merchant directory synchronization company Cymbio, and Mastercard launched the Agent Suite package.

In February, Coinbase officially released Agentic Wallets, allowing AI Agents to have their own wallets to autonomously spend, earn, and trade cryptocurrencies. The x402 protocol is deeply integrated with the Google system, having processed over 50 million transactions.

March saw further intense developments. Circle launched Nanopayments, Ramp introduced Agent Cards, Mastercard officially announced an acquisition of the stablecoin infrastructure company BVNK for up to $1.8 billion, and the Tempo mainnet incubated by Stripe and Paradigm went live, simultaneously releasing the Machine Payments Protocol (MPP).

In three months, there were more than a dozen significant actions, both promising and concerning. These events seem scattered but point to the same structural change: as the cost of transactions between machines approaches zero, the real enemy of payment giants is no longer each other, but the concept of zero cost itself.

Key Event Review

In the Zero Cost Era, There Are No Winners Take All

Six months ago, we were still discussing who would legislate for AI Agents. Stripe's ACP, Google's AP2, and Mastercard's Agent Pay each pursue their own interests while vying for the defining rights of the same proposition.

Now this battle is essentially over, not because one side won, but because everyone has realized that a winner-takes-all scenario will not occur.

The UCP introduced by Google at the beginning of the year includes all mainstream standards and is responsible for business transactions within the search and Gemini ecosystem. The MPP launched alongside Tempo by Stripe also supports integration with Mastercard and Visa systems, handling autonomous payments between machines. Mastercard's Agent Pay is responsible for audit-capable authorization of high-value transactions.

What was once a territory dispute is now a matter of delineating territory. The status quo of the protocol layer indicates that decisive competition has shifted elsewhere.

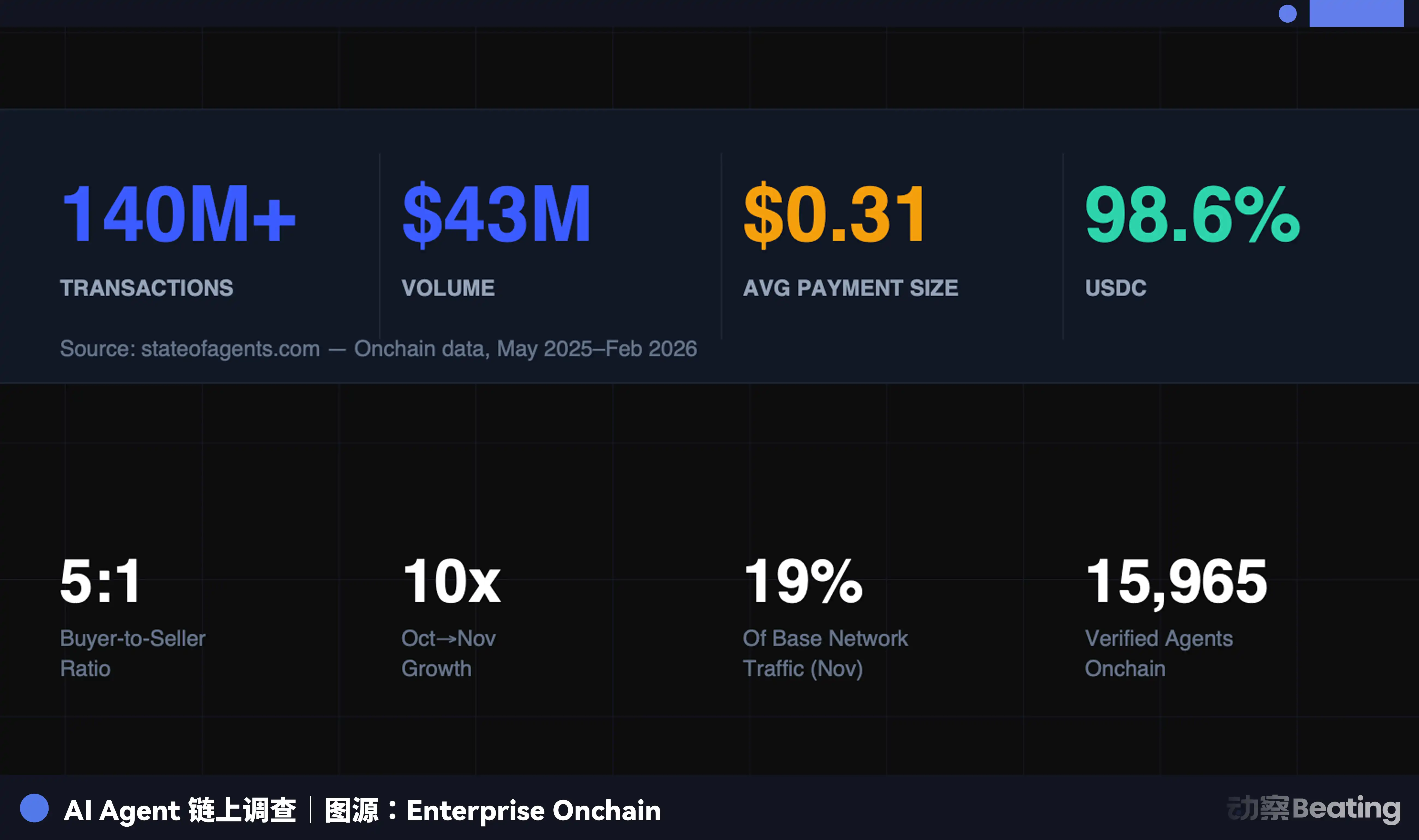

Looking at data released by Enterprise Onchain, in the past nine months, AI Agents completed 140 million payments, totaling $43 million, with 98.6% using USDC, averaging $0.31 per transaction. The number of AI Agents with purchasing power has exceeded 400,000.

Let's analyze the significance of these numbers.

First, autonomous machine transactions. 140 million payments occurred without human intervention, bank approvals, or credit card validations. Between code and code, between protocol and protocol, processes that once required human signatures, reconciliations, and settlements are now completed autonomously by machines.

Second, the individual amounts are very small. An average transaction amount of $0.31 means that most of these payments are microtransactions for API calls, computing power purchases, data access, and other scenarios. Under traditional payment systems, such transactions would be impossible, as any card network's minimum fee would exceed the value of the transaction itself.

Third, costs approach zero. Coupled with the x402 protocol, payments are directly embedded in HTTP requests, and Circle's Nanopayments reduces the gas fees for single transactions to zero by pooling thousands of small payments off-chain and periodically packaging them for on-chain settlement. The costs of on-chain settlement are borne by Circle at the batch settlement layer.

Transactions between machines have no checkout pages, no payment gateways, no intermediaries—this is the source of concern.

Of course, zero cost currently only applies to this specific scenario of micropayments between machines. Stablecoins are not truly free; on the Ethereum mainnet, the gas fee for a small stablecoin transaction can exceed 20% of the transaction amount, which is exactly why Stripe is establishing Tempo to address this issue.

At the consumer payment level, card networks still have advantages that stablecoins cannot replicate, such as unified consumer protection, consistent user experience, and the flexible routing capabilities of cards as an abstraction layer at the base level.

However, this does not change the essence of the concern. In the scenario of high-frequency microtransactions between machines, zero cost has become a reality, and this gap is rapidly widening. Deloitte predicts that the global Agent market size will reach $45 billion by 2030. This is a completely new transaction world, opening a massive gap on the edge of traditional payments.

Giants' Responses: From Tolls to Bridges

Faced with the threat of zero cost, traditional payment giants have varied response strategies, but they share a common underlying logic: since it is impossible to charge fees for microtransactions between machines, the focus should be on controlling the bridge between the old and new systems, where fees can be charged.

Visa's strategy is absorption rather than confrontation. USDC settlement was officially launched in the United States, and crypto-friendly banks like Cross River Bank and Lead Bank have started using it. Visa Direct supports stablecoin pre-loading and direct payments.

In other words, you can use stablecoins, but please go through my pipeline. Visa has also participated in the drafting of the MPP, extending the protocol to card payment scenarios, a move typical of joining forces when one cannot win.

Mastercard acquired BVNK for $1.8 billion, securing the bridge between fiat and stablecoins. BVNK supports fiat-to-stablecoin conversions across over 130 countries and all mainstream blockchain networks, which is the most critical infrastructure for the era of AI Agent payments.

Mastercard’s Chief Product Officer Jorn Lambert's response to the notion that stablecoins threaten card business was straightforward: the card business is fine; the acquisition was aimed at expanding into new fields like remittances. But the deeper logic is that when stablecoin transaction volumes grow rapidly, controlling the clearing bridge between fiat and stablecoins means controlling the lifeline of value flow.

Stripe has the highest ambition. It owns its blockchain Tempo, its protocol MPP, and a platform called Open Issuance that allows businesses to issue their own stablecoins and share reserve earnings, representing the pinnacle of vertical integration.

The combination of Tempo + MPP + Open Issuance means that Stripe is no longer just a payment processor; it is becoming the infrastructure operator for the era of AI Agent payments.

PayPal has taken a different path. The acquisition of Cymbio was not to control the payment pipeline but to control the distribution of the merchant directory. Cymbio's core capability is Store Sync technology, which enables merchants' product catalogs to be synchronized to multiple AI shopping surfaces with one click, meaning small and medium-sized merchants no longer need to adapt to each AI platform separately.

When AI Agents replace humans in discovering products, whether a merchant's product catalog can be seen by AI becomes a life-and-death question. PayPal is betting that in the era of Agent Commerce, being discovered by Agents itself holds value.

An interesting intermediate state is Ramp's Agent Cards, which provide AI Agents with virtual cards, still operating on the Visa card network, but with dynamic authorization for each transaction, not exposing real card information; essentially transforming business expense cards into Agent wallets.

Whether this is a continuation of traditional payments or a stopgap measure in a transitional period remains unclear. If the mainstream form of machine-to-machine transactions ultimately follows a stablecoin-native path, then Agent Cards might represent the last opportunity for traditional card networks to be needed in the new era.

In the New Era, How to Make Money?

There is a question that has not been directly answered. On the zero-cost track, transactions themselves do not generate fees. So, who will make money?

Circle's Nanopayments rely on infrastructure service fees, Stripe's Open Issuance relies on reserve earnings, and Mastercard profits from the conversion services between fiat and stablecoins after acquiring BVNK.

These three charging methods share a common characteristic: the charging point has shifted from the transaction itself to the conditions that enable the transaction. Essentially, they are closer to infrastructure rent than transaction taxes.

This represents a fundamental shift in the business model. For the past fifty years, the moat of payment networks has been the network effect. More merchants lead to more consumer willingness to transact; more consumers mean merchants need to connect, and this flywheel profits from the commission rights brought by scale.

In the world of machine-to-machine transactions, this flywheel is ineffective. Machines only need a stable, programmable, low-cost settlement layer—whoever can provide that becomes the new infrastructure provider.

It is not a big issue for payment giants to survive. The real question is, in an industry that maintains power through commissions, where does power go when commissions lose their significance?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。