Translated by: Block unicorn

Foreword

In 1719, Scottish gambler and monetary theorist John Law persuaded the French regent to allow him to establish a system that packaged the non-liquid assets of colonies into highly liquid paper financial instruments. He created the Mississippi Company, which monopolized trade with French Louisiana, a vast territory mostly made up of swamps.

John Law transformed these illiquid colonial assets into company shares redeemable for gold. Ordinary Parisians flocked in. A year later, this scheme made him the richest man in Europe and the French Comptroller General. Though it was only temporary.

What happens when you hold stocks redeemable for gold? You wait for the stock price to rise, then request to redeem the gold. Investors did just that. A tide of redemptions began as they wanted their gold back. However, the gold supply was insufficient. John Law's response was to modify the rules. He restricted the amount of gold anyone could hold. He devalued the paper currency by decree and mandated that stocks could only be sold through his bank at prices he set. Each intervention bought him a few weeks of time, but it destroyed trust. By 1720, investors' redemption receipts had become worthless. John Law fled France after leading it into the Mississippi Bubble.

Three centuries later, the world's largest private credit funds are responding to a surge in redemption requests from investors in a similar way. They are modifying redemption rules to control losses. But is this a solution, or merely a stopgap? Can on-chain private credit help? In today’s deep dive, I will explore this question. Let's begin.

From Origins to Redemption

Private credit refers to lending activities that occur outside of banks and public markets. Companies borrow directly from specialized funds like Blackstone, Apollo Global Management, or Blue Owl rather than borrowing from banks or issuing bonds. Borrowers are typically mid-sized enterprises that are currently unable to go public.

Twenty years ago, this market barely existed. Today, it has grown to over $3 trillion and is expected to reach $5 trillion by 2029. The industry filled the market gap left by the 2008 financial crisis when the cost of holding high-risk loans became prohibitively high due to regulatory and capital requirements.

Private credit attracts investors with higher returns than public markets (8-10%) but at the cost of poor liquidity. Investors' capital can be locked up for several years. This is the essence of private credit. Compared to traditional loans obtained via syndicated loans, private credit provides companies with greater flexibility and convenience in managing their business. In return, investors earn a liquidity premium due to their funds being tied up for the long term.

Subsequently, the industry decided to change the rules. They sought to attract retail investors, either to provide more attractive returns or to develop the private credit market. To this end, the US Congress established Business Development Companies (BDCs) in 1980 under the Investment Company Act. BDCs remained niche products for decades, but with companies like Ares, Blackstone, and Blue Owl launching non-listed BDC products targeting retail and high-net-worth individuals, they began to gain popularity. These products bundle illiquid corporate loans and set quarterly redemption windows to appease retail investors.

Retail investors participated in these deals but overlooked a significant structural flaw: the private credit industry promised to provide liquidity while the liquidity of the underlying loans was very poor. If the credit cycle bubbles burst, retail investors would rush to redeem, and the private credit funds issuing these retail investment products would find themselves in trouble. Thus, they set redemption limits at 5%. This seemed to solve the problem for fund managers. But what happens if a market crash forces redemption demands beyond the 5% limit? Ultimately, the inevitable happened.

In September 2025, two major collapses completely destroyed retail investor confidence in private credit.

First, the auto parts supplier Brands Group filed for bankruptcy after failing to discover and disclose hidden off-balance-sheet liabilities in its loan agreement. The lender underwrote the deal believing it was a 5x leveraged buyout, when in fact the leverage was close to 20x. Second, the subprime auto lender Tricolor Holdings reportedly used the same collateral for multiple loans. Once the truth was revealed, redemption demands skyrocketed.

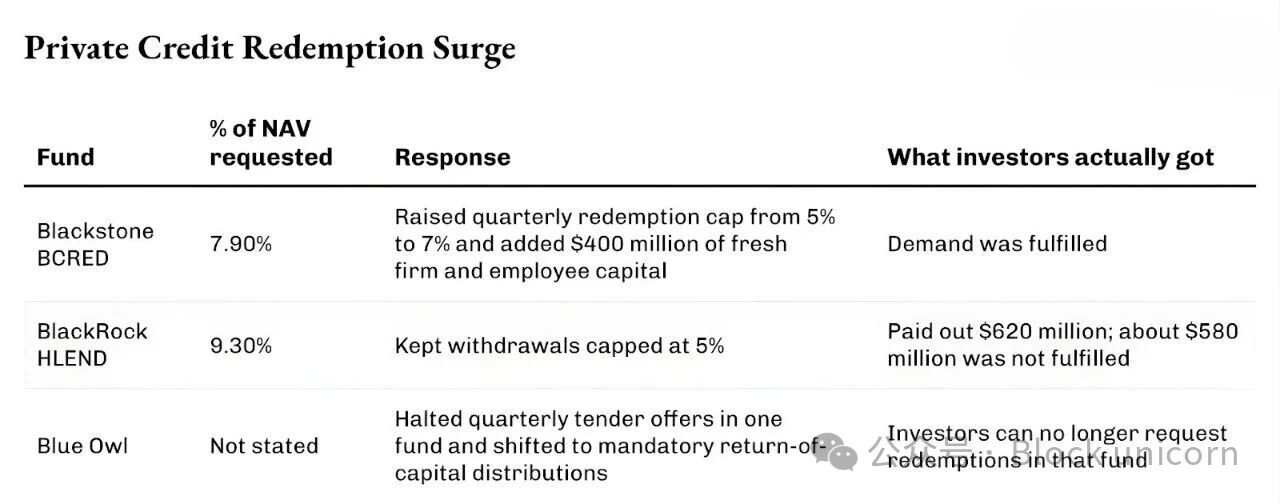

This led top private credit fund managers to either take discretionary measures to modify rules or limit redemptions.

These responses carry a touch of the John Law style. Some directly restrict redemptions while others modify rules during the crisis.

These responses all have a John Law-like quality. Some measures limit redemption opportunities, while others change the rules when a crisis arises.

What worries me is that this kind of gatekeeping and arbitrary rule changes is a double-edged sword. For investors, it conveys the message that the terms they previously agreed upon are negotiable and can only be negotiated in one direction. Investors can only be subjected to the whims of fund managers, who can tighten redemption restrictions or, worse, completely halt redemptions and adjust profit distributions. Even more unfairly, these changes occur only after the funds have been invested. This undermines the spirit of any contract signed by both parties.

On the fund manager side, they start to become conservative. Funds under continuous redemption pressure won’t confidently deploy capital. Rather, they will choose to hold cash instead of lending it out.

Is On-Chain Private Credit the Solution?

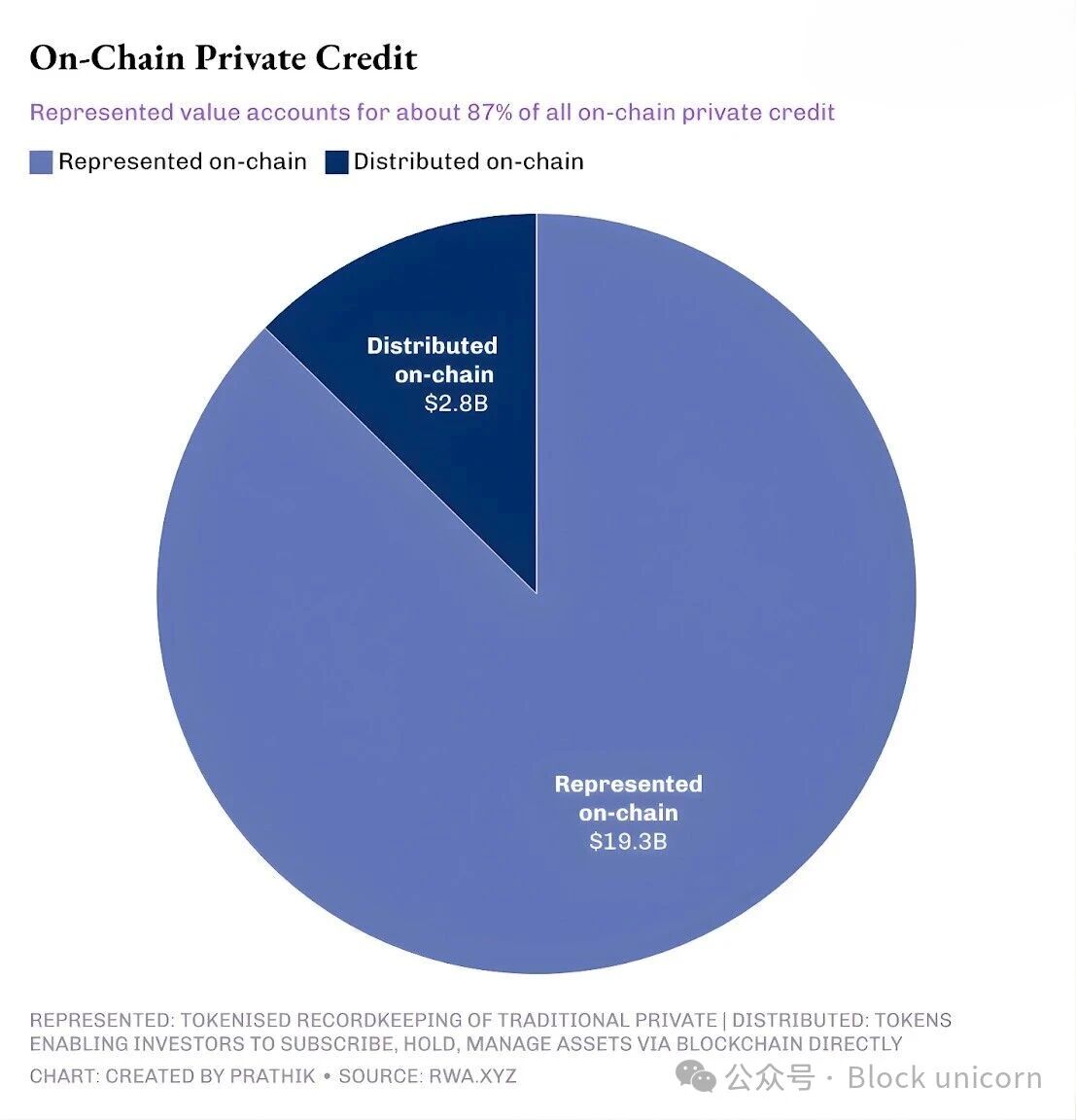

People may boast about the various advantages of on-chain private credit. They will showcase the various data on their tokenized dashboards and the total value locked in private credit agreements. But in reality, most of these are merely repackaged existing traditional private credit industries. Why do I say this? The facts are as follows:

The core unique selling proposition (USP) of on-chain private credit lies in its ability to execute smart contracts on any financial underlying. These contracts can set withdrawal limits, collateral ratios, and allocation rules in code. While on-chain private credit funds cannot guarantee higher liquidity than traditional funds, they can ensure that once capital is invested, no fund manager can unilaterally modify the contract terms. No board votes can expand the offer size or convert quarterly redemptions into capital return allocations like Blue Owl.

Regardless of the manager’s intentions or market conditions, the code will continue to operate as originally intended.

Smart contract-based private credit funds can also address the problem of repeated collateralization. Tricolor's collapse involved using the same collateral for multiple loans. Tokenized collateral creates a single, auditable record, with each debt corresponding to a set of tokens. This structurally increases the difficulty of re-pledging collateral.

In the months leading up to First Brands' bankruptcy, its valuation was still maintained at par by private credit funds. On-chain, every transaction and repayment is visible in real-time. Any self-reported valuation cannot mislead investors. If the on-chain market values an asset at 60 cents, then it cannot be priced at 100 cents.

If on-chain credit tokens could trade in the secondary market, better price discovery could be achieved. This resolves the pricing mismatch between non-traded Business Development Companies (BDCs) and their underlying loans. We saw this in the case of hedge funds Saba Capital and Cox Capital acquiring Blue Owl shares at prices 20-35% below the net asset value.

Various protocols are already building this infrastructure. Maple Finance operates a pool of institutional credit managing $3 billion in assets. Apollo has partnered with Securitize to launch tokenized sub-funds. WisdomTree has introduced on-chain net asset value data for its private credit fund through Chainlink oracles. The infrastructure is ready.

However, all this infrastructure cannot solve one problem: they cannot assess whether a borrower will repay a loan or determine whether a mid-sized software company can survive in the transformative wave of artificial intelligence.

As the cases of First Brands and Tricolor demonstrate, underwriting issues caused by human judgment errors can be minimized but not entirely eliminated through on-chain records. However, another larger issue is that most business processes, including maintaining financial statements, vendor contract records, balance sheets, etc., exist entirely off-chain. Smart contracts cannot check a borrower's books or verify their financial statements. Even if there were some agreement to get this data on-chain for validation, companies would not agree to expose their financial and other sensitive business details on a public blockchain. Thus, under the current infrastructure, fully on-chain underwriting is simply not feasible.

Blockchain currently offers a series of different trade-offs. But failures in private credit conducted via decentralized finance (DeFi) channels could be more severe than failures in traditional private credit industries.

Imagine a fund whose assets are continuously devaluing while redemption amounts are continuously climbing. For this fund, a decentralized finance (DeFi) ecosystem eager for high returns from real-world assets is undoubtedly an ideal target. Investors are highly motivated to redeem and fund managers are equally motivated to seek new sources of funding to tokenize and sell these loans to on-chain capital pools. DeFi can easily become a dumping ground for illiquid, problematic products from traditional markets.

We have seen this in the case of on-chain lending pioneer Goldfinch: a borrower unauthorizedly made a substantial inter-company transfer that jeopardized the whole company’s operations. Tokenization can only reveal the consequences of the event but cannot prevent the occurrence of fraudulent activities.

There are counterarguments as well. On-chain secondary markets can also provide liquidity for distressed assets and help achieve more reasonable pricing. However, the line between market functionality and exit liquidity can be quite blurred, and collapse can occur easily.

As long as critical information such as borrower qualifications, covenant effectiveness, financial reporting, etc., remains off-chain, on-chain credit cannot resolve the issues of the traditional industry and will only bring a series of new problems.

If mainstream on-chain protocols direct hundreds of millions in DeFi deposits toward loans that are in default or have weak underlying assets, the damage will ripple across multiple protocols. On-chain private lending is still in its infancy. The total amount of active blockchain-native loans across all protocols is only $3 billion, while the scale of the traditional private credit industry reaches up to $3 trillion. A highly publicized default event could set back the entire concept of lending based on real-world assets (RWA) by several years.

If on-chain private credit wants to transcend the glamorous facade of traditional private credit, it must first resolve the trust issue to address the yield issue. This includes third-party verification of underlying collateral instead of relying on self-reported information from originators. Additionally, a standardized risk disclosure mechanism could convert duration and credit risks into terms that DeFi participants can understand and value.

It should even include credit ratings of on-chain tools from traditional institutions, which Maple Finance CEO Sidney Powell anticipates will be achieved by the end of 2026. It should also contain frameworks capable of detecting and preventing originators from dumping distressed assets into on-chain capital pools. Without these measures, the fusion of traditional finance and decentralized finance risks will turn into exploitation rather than enhancement.

That’s all for today; see you in the next article.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。