Written by: FinTax

1 Introduction

In scenarios of cross-border payments, asset preservation, and capital flows, the applicability of different financial instruments and institutional arrangements shows more significant differences in an environment of high uncertainty. Compared to traditional settlement systems that rely on centralized intermediaries, on-chain assets possess the technical characteristics of cross-border transfer, self-custody, and not fully depending on a single institution. Therefore, in situations of sanctions, high inflation, or restricted capital flows, they are more easily used for value transfer, risk buffering, and asset allocation.

Taking Iran as an example, under extreme external pressure, the exchange rate of the Iranian rial to the dollar in the open market plummeted by 30 times. Under extreme macro shocks, on-chain assets with characteristics of cross-border transferability, self-custody, and resistance to single-point freezes were quickly utilized by multinational trade participants and local residents as channels for risk buffering and capital substitution. Research by Chainalysis shows that the scale of Iran's crypto ecosystem reached approximately $7.78 billion by 2025, with on-chain activities showing a high correlation with significant macro events. However, the cross-border flow of these assets also carries significant compliance risks. While their resistance to censorship provides autonomy for users, it may also create opportunities for illicit capital flows. Balancing innovation and regulation has become a common challenge for global policymakers.

The short-term "channel value" under macroeconomic fluctuations cannot obscure the profound value differentiation in the crypto asset market. The long-term blind expansion of token supply contrasts sharply with the rapid demise of numerous projects: Data from CoinGecko Research indicates that over 13.4 million previously listed crypto projects ended trading and were deemed failures. This large "death list" profoundly demonstrates that assets driven solely by "issuance—financing—narrative," lacking foundational support, are unable to maintain consensus over the long term. Market funds and liquidity will inevitably converge towards a few assets with sustainable value mechanisms.

Against this backdrop, this article centers on "value mechanisms," first exploring which tokens possess sustainable value beyond cycles under the tests of economic policy uncertainty and cross-border economic activities. Second, it deeply analyzes why the regulatory system must evolve from managing financing chaos to governing market infrastructure and then to classification details and data reporting in the evolution of global digital finance.

2 Theoretical Basis

2.1 Theoretical Definition of Tokenization and Three Fundamental Proofs

The World Economic Forum (WEF) defines "tokenization" in its 2025 report as: the process of representing asset ownership in a transferable digital format using programmable ledgers. Unlike traditional financial systems that rely on fragmented external messaging (such as the SWIFT system), tokenization theoretically constructs a shared system of record, which, together with smart contracts, enables a unified record system, flexible custody models, and on-chain governance.

The Bank for International Settlements (BIS) further points out in its Unified Ledger framework blueprint that tokenization integrates information transmission, reconciliation, and settlement into a single seamless operation. This underlying architecture significantly reduces trust friction and compliance costs in multinational commercial collaboration. Its theoretical framework is based on three fundamental proofs: first, Proof of Value. That is, asset issuance must have a verifiable value basis—either supported by cash flow from the real economy or widespread network consensus. This ensures that on-chain assets are not merely fictitious "narrative bubbles"; second, Proof of Ownership. That is, property rights must be clear, assigning asset disposal rights directly to legal holders. Distributed ledgers use cryptographic means for exclusive confirmation of rights, severing reliance on centralized intermediaries, thus technically avoiding the tail risks of assets being single-point frozen or misappropriated; third, Proof of Transaction. This means producing an immutable, verifiable transaction history and evidence of settlement and clearing. This implies that every cross-border capital flow has complete traceability, providing a data foundation for post-compliance audits and penetrative supervision.

These three proofs together constitute the logical starting point for tokenization's reconstruction of financial infrastructure: Proof of Value establishes the basis for asset issuance, Proof of Ownership reconfigures the realization form of property rights, and Proof of Transaction reshapes the trust mechanism of clearing and settlement.

2.2 Two Core Token Models: Native and Backed

Current tokenization models can essentially be divided into two basic categories based on their value capture mechanisms: Native Tokens and Backed Tokens. Their ability to navigate macro cycles shows significant differences, rooted in their differing value anchors.

Native Tokens are assets issued directly on-chain, possessing embedded issuance, trading, and ownership records. These assets (such as native assets of public chains like Ethereum) are generally not anchored to external physical assets; their core function is to serve as a settlement medium within the network and maintain the operational "security budget" of decentralized systems. Specifically, native tokens attract nodes to maintain network consensus through economic incentive models (like Proof of Stake), acting as network fuel (Gas Fee) when users engage smart contracts and execute complex business logic. The sustainable value of native tokens is deeply tied to whether the public chain network can continuously lower friction costs for real economic activities—their value accumulation stems from the prosperity of the network ecosystem and actual usage frequency. In short, the value anchor of native tokens is network utility.

Backed Tokens are also issued and circulated on-chain, but their value is strictly anchored to off-chain assets. The core mission of backed tokens is to bring true returns from traditional financial markets onto the chain. In the current climate of increasing economic policy uncertainty, backed tokens exhibit strong practical value. For instance, tokenizing high-quality liquid assets like U.S. Treasuries not only grants these traditional assets 24/7, divisible global liquidity but also provides on-chain funds with a risk-free yield benchmark that is independent of the high volatility of the crypto market. For enterprises looking to expand internationally, this represents a tool for efficient liquidity management, hedging against currency depreciation, and reducing cross-border friction costs. The value anchor of backed tokens is off-chain asset value.

The essential difference between these two types of tokens is that the value of native tokens arises from the network itself, and their sustainability depends on the ecosystem's ability to continuously create value that reduces costs and increases efficiency; the value of backed tokens comes from their reference to off-chain assets, and their sustainability relies on the credit quality and repayment capability of the anchored assets.

3 Economic Analysis of Sustainable Token Value

After several rounds of bull and bear market transitions, the crypto asset market is undergoing a profound value correction. Data from CoinGecko Research shows that over 13.4 million crypto projects driven merely by "issuance—financing—narrative" ultimately ceased trading and were eliminated from the market. This massive "death list" reveals a fundamental principle: speculative products lacking underlying asset support and real application scenarios are doomed to be unable to sustain market consensus when macro liquidity recedes.

From the perspective of institutional economics, for a token to possess sustainable value that traverses cycles and withstands external macro shocks, it must substantially reduce friction costs in the operation of the real economy and establish a solid rights structure. This sustainable value can be analyzed from the following three dimensions.

3.1 Macro Hedging

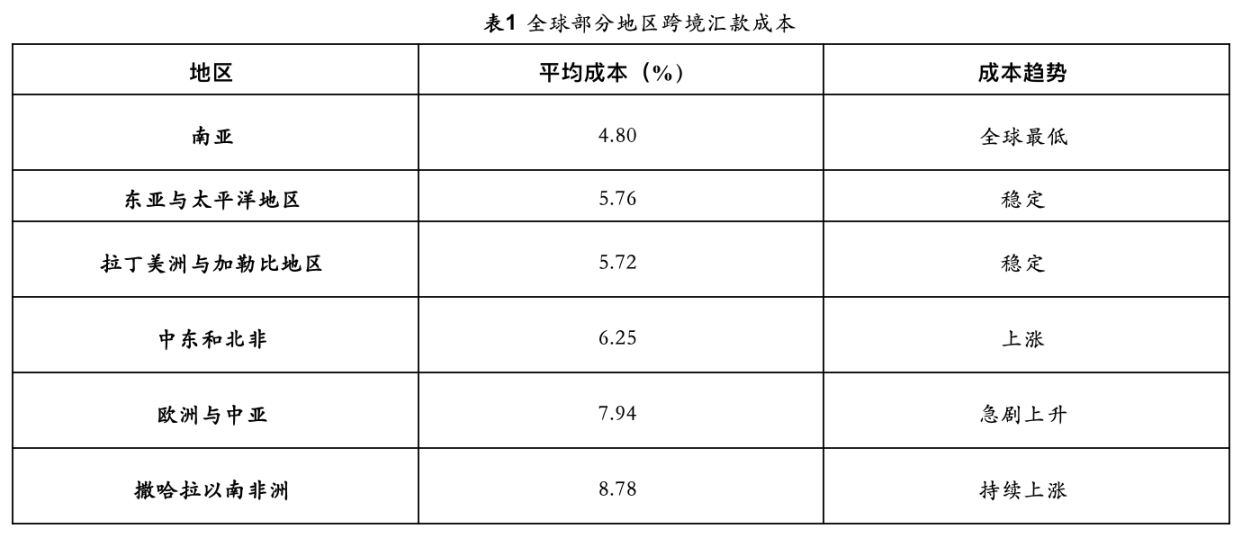

In international layout and cross-border trade, enterprises rely heavily on stable, low-friction cross-border payment networks. However, the traditional correspondent banking model has significant institutional friction due to lengthy clearing chains and complex compliance nodes. As of the first quarter of 2025, World Bank data shows that the average cost of global cross-border remittances remains as high as 6.49%, with explicit fees through traditional banking channels averaging 12% to 13%. Cross-border remittance costs across different regions of the world can be seen in Table 1. Moreover, due to the instability of the macroeconomic environment, cross-border remittance costs in certain areas are also on the rise. The Bank for International Settlements in its Agorá project study pointed out that the current cross-border payment system is fraught with challenges, while tokenization technology can integrate information transmission, reconciliation, and settlement into a single seamless operation.

Data source: RemitBee

When economic policy uncertainty escalates sharply—such as extreme capital controls or sanctions due to geopolitical struggles, or when the SWIFT network connection is severed during a macro crisis—traditional cross-border capital flows face both high implicit and explicit costs, as well as an availability crisis where funds can be frozen at any time. At this point, the value of tokens primarily manifests as their macro hedging capability as independent, censorship-resistant channels.

Global macro data from Chainalysis validates this logic: in regions under extreme pressure from uncontrolled inflation or escalating geopolitical conflicts, retail and corporate users tend to convert substantial amounts of funds into stablecoins like USDT and USDC to maintain operations of cross-border supply chains and hedge against rapid depreciation of their local currency. These on-chain assets issued based on programmable ledgers empower end-users with asset control through self-custody mechanisms, severing reliance on single centralized financial intermediaries. For multinational economic entities, this on-chain value network with global liquidity has become a capital buffer against the tail risk of macro policies.

3.2 Anchoring Real Returns

The demise of countless "air coins" proves that a token economy reliant solely on community sentiment and Ponzi-like liquidity is unsustainable. The World Economic Forum points out that tokens with sustainable viability must possess clear "Embedded Rights," meaning that it grants holders legitimate economic and governance rights in an unalterable manner at the underlying code level.

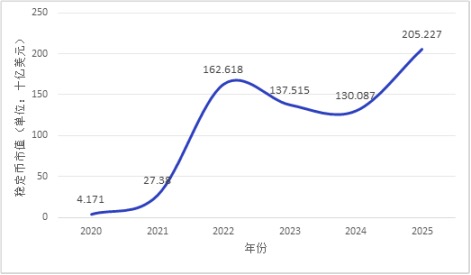

Market funds are undergoing a clear structural migration: accelerating towards assets with "real returns." Reports from the World Economic Forum show that the total transaction volume of backed tokens like stablecoins reached $27.6 trillion in 2024, exceeding the combined transaction volume of Visa and Mastercard. The market capitalization of stablecoins has demonstrated a continuous upward trend since 2020. From the perspective of macro capital efficiency, there exists an estimated potential collateral pool of about $230 trillion globally, but due to the inefficiencies and time friction of physical circulation in the traditional financial system, only about $25 trillion in securities have been actively activated as collateral.

Tokenizing high-quality liquid assets (HQLA, such as U.S. Treasuries) not only endows traditional assets with 24/7, infinitely divisible global transfer capabilities but also directly introduces the risk-free return rates of the real economy onto the chain. This mechanism constructs a valuation anchor detached from pure crypto speculation, aligning the value logic of backed tokens with classic valuation models in modern finance, providing new liquidity tools for enterprise treasury management. Market performance validates this: during periods of heightened macro volatility, the circulation scale and trading activity of compliance-focused stablecoins have both shown significant increases, reflecting the market's substantive demand for "verifiable value anchoring." Research by the International Monetary Fund (2025) indicates that tokenizing central bank reserves is a key path to maintaining the crucial settlement function of central bank currencies within the digital asset ecosystem, essentially being a technical migration of the existing reserve system rather than creating new central bank liabilities.

Figure 1 Evolution of Total Market Capitalization of Stablecoins (2020-2025)

Data source: CoinLedger

3.3 Reducing Friction and Costs

In the micro lifecycle of enterprise operations and financial settlement, the core value of sustainable tokens stems from their reconstruction of contract execution efficiency. In traditional capital markets, corporate actions such as dividend payments, stock splits, and voting are not only time-consuming but also prone to information asymmetry and accounting errors due to their unstructured data characteristics.

The programmability of smart contracts provides a new paradigm for addressing this issue: the immutable code mechanism effectively prevents unilateral changes to rules and reshapes business trust through standardized operations. Cross-border compliance checks (KYC/AML), complex asset service flows, and automated profit distribution can all be transformed into executable program codes. Furthermore, smart contracts achieve "atomic settlement" (i.e., delivery versus payment, DvP), fundamentally eliminating reconciliation frictions and counterparty risks in cross-border collaborations.

As a result, the sustainable value of native tokens is established: they serve as the "system security budget" and network fuel (Gas Fee) for maintaining the efficient and secure operation of decentralized underlying ledgers. This value logic has been validated by the market—on public chains like Ethereum, network activity shows a high positive correlation with native token consumption, and the prosperity of the application ecosystem directly translates into the value capture of tokens. As long as the underlying public chain can continuously reduce costs and improve efficiency for real-world cross-border payments, supply chain finance, and clearing systems, the value cycle of its native tokens can establish a self-reinforcing flywheel effect.

4 Governance of Chaos and Infrastructure Construction

If the underlying programmable mechanism of tokens determines their intrinsic value that transcends cycles, the evolving regulatory framework delineates their survival boundaries and compliance costs in the modern macroeconomic system. PwC’s annual regulatory report also states that regulation is no longer a constraint but is actively reshaping the market, allowing digital assets to expand responsibly. Globally, the regulation of crypto assets shows a clear evolutionary path from "managing financing chaos" to "governing market infrastructure," and finally to "classification details and data reporting." The core driving force lies in: as the scale of the crypto market expands and the complexity of assets increases, the transmission path of financial risk has fundamentally shifted from isolated crypto ecosystems to traditional cross-border capital flows and macro-financial stability systems.

4.1 Temporal Dimension Evolution of Regulatory Pathways

From the lifecycle of cross-border capital flows, the evolution of regulatory pathways is a passive response and proactive prevention of prominent risks at different stages, which can be divided into three phases:

4.1.1 Phase One: Managing Financing Chaos

In the early stages of the crypto market, the market was inundated with projects driven solely by narratives. Due to fuzzy asset definitions and a lack of cash flow support from the real economy, financial risks predominantly manifested as regulatory arbitrage, illegal fundraising, and resulting damage to investor rights. A large number of projects failed after brief trading. In response to such chaos, the defensive focus of regulation has been to cut off the disorderly exchange channels between traditional fiat currencies and rootless tokens, aiming to prevent illegal outflows of cross-border capital and their systemic disturbances to macro-financial order. The core characteristic of this phase is "containment regulation"—with the primary goal of curbing risk spillover.

4.1.2 Phase Two: Market Infrastructure Governance

As the crypto ecosystem evolved, centralized exchanges (CEX) and custodians expanded rapidly, leading to extreme concentration risk in the market. However, in the absence of regulation, these institutions often faced issues of fund commingling and internal control deficiencies. When encountering tightening macro liquidity or shocks from economic policy uncertainty, these centralized nodes, lacking risk buffering capabilities, are prone to trigger "bank runs" similar to traditional banks, creating strong procyclical effects. Thus, regulatory focus shifted towards building the resilience of underlying infrastructures. Policymakers began to mandate the implementation of asset segregation (Bankruptcy Remoteness) and independent third-party custody to ensure the integrity of customer assets in the event of institutional bankruptcy, thus severing the chain of systemic risk transmission triggered by single-point failures. The hallmark of this phase is "structure-based regulation"—introducing traditional financial infrastructure safety standards into the crypto ecosystem.

4.1.3 Phase Three: Classification Details and Data Reporting

As blockchain technology is gradually adopted by mainstream financial systems to reduce cross-border transaction friction, regulation enters a deeper phase. Regulators recognize that a "one size fits all" approach is no longer sufficient to accommodate complex asset forms. Cutting-edge regulations represented by the EU's Markets in Crypto-Assets Regulation (MiCA) and Liechtenstein's Token and Trusted Technology Service Provider Act (TVTG) define tokens as "containers of rights" and implement classification regulation strictly based on their underlying economic characteristics. Simultaneously, regulatory tools are accelerating towards digitization and API-based frameworks, requiring unified data reporting interfaces to achieve all-weather penetrative monitoring of on-chain liquidity and cross-border capital movements. The core characteristic of this phase is "embedded regulation"—incorporating compliance requirements into the technological infrastructure.

4.2 Differentiated Regulation Based on Token Value Types

Regulators adopt differentiated compliance requirements and policy tools for tokens with different value anchors.

The regulatory logic for native tokens focuses on enhancing network resilience and anti-money laundering penetration. Non-anonymous crypto assets, given their potential compliance advantages, have average market values significantly higher than their anonymous counterparts. Native tokens exhibit characteristics of decentralization similar to unregistered assets, with issuance and settlement completed in a closed loop on the chain. In a complex macro environment, this anonymity provides autonomy to users but can also be misused to circumvent compliance requirements. The international anti-money laundering regulatory bodies (like FATF) have designated the anti-money laundering penetration of virtual asset service providers (VASPs) as a priority in their frequently updated guidelines. Regulators' tools for native tokens and their service providers heavily rely on on-chain data analytics and the mandatory enforcement of FATF's "Travel Rule," requiring the penetration and recording of the real identity information of both transaction sides, achieving compliance penetration through service provider layers without disrupting the decentralized network architecture.

The regulatory logic for backed tokens focuses on auditing and liquidity management of off-chain assets. The foundational value of backed tokens lies in their rigid repayment commitments to off-chain assets. Their core vulnerability stems from potential mismatches in terms between the on-chain ledger proof and off-chain real reserves, as well as possible value disconnections. In the face of macro shocks, regulators strictly focus on preventing "de-pegging" risks. In February 2026, the Office of the Comptroller of the Currency explicitly required issuers of stablecoins to maintain 100% reserves of high-quality liquid assets, accept monthly reporting and annual audits, and introduce traditional financial asset auditing standards in a more refined manner onto the chain. Modern regulatory frameworks compel issuers to engage high-frequency third-party independent audits, strictly limit investment ratios in high-risk assets, and establish dual liquidity pools to ensure full coverage of 100% or even excess high-quality liquid assets (HQLA) for the circulating supply, thus providing credit support for on-chain value anchoring using traditional financial asset auditing standards.

4.3 "Codification" of Compliance Rules

In handling high-frequency and complex multinational enterprise transactions, traditional ex-post accountability regulatory frameworks face exorbitant cross-border enforcement costs and information latency. In striving for a balance between promoting capital flow efficiency and maintaining financial security, many national regulatory bodies are actively advocating for foundational innovations in "compliance rule codification."

By introducing token standards specifically designed for compliance (such as ERC-3643, or the T-REX protocol), digital identity verification (KYC/AML), thresholds for anti-money laundering travel rules, and capital transfer restrictions in specific jurisdictions are directly hard coded into the underlying smart contracts. This means that if a tokenized asset transfer initiated by a multinational enterprise fails to meet the predefined compliance whitelist conditions or triggers a dynamically updated sanctions blacklist, that transaction will be automatically blocked at the blockchain protocol level. This innovation in regulatory infrastructure, which transforms legal logic into immutable code logic, significantly reduces the compliance verification costs for cross-border commerce and provides foundational infrastructure support for legitimate capital flows under extreme macro shocks. It marks a fundamental shift in regulatory paradigms from "ex-post accountability" to "ex-ante embedding." Estimates in the DFCRC report suggest that if the regulatory framework is clear, the tokenized financial market could generate tens of billions of Australian dollars in economic benefits for Australia, highlighting the reliance of digital asset potential releases on properly constructed regulatory infrastructure.

5 Conclusion and Outlook

Tokenization technology is driving a fundamental reconstruction of global financial infrastructure, while macro geopolitical conflicts and persistently high economic policy uncertainty are stress tests for this emerging value bearer. Amidst intense volatility, the purely "narrative bubbles" and rootless assets in the crypto market are gradually being peeled away, with market attention and liquidity accelerating towards tokens backed by real value.

This research indicates that truly sustainable tokens capable of traversing cycles typically exhibit several distinct traits: first, they can provide real yield anchoring, bringing off-chain asset credit onto the chain; second, they can substantially reduce execution costs in cross-border transaction contracts, reshaping business trust through programmability; third, they act as a security budget for decentralized networks, with their value grounded in the actual usage frequency and efficiency gains of the ecosystem. These tokens are not speculative symbols detached from real foundations, but value carriers embedded in real economic activities, capable of bearing specific functions, yield relationships, or rights arrangements.

Currently, global regulatory frameworks have shifted from early passive containment to proactive embedded rule-making. Through classification details and compliance codification, regulatory bodies are cautiously integrating high-quality digital assets into mainstream clearing and settlement systems.

In the face of this irreversible trend in financial evolution, this article offers the following recommendations for various market participants:

- For enterprises, they should regard on-chain assets as tools for enhancing the efficiency of global capital turnover. In cross-border settlement scenarios, prioritize the use of compliant stablecoins to hedge against fiat currency exchange rate volatility and reduce institutional frictions; simultaneously, strictly distinguish between highly volatile native tokens and rigorously regulated backed tokens, implementing differentiated fund management strategies.

- For issuers and financial institutions, they must completely abandon the outdated logic of "issuing tokens equals financing." The focus of digital asset design should fully shift to "embedded rights"—clearly and immutably defining asset attributes in underlying smart contracts and actively employing compliant-oriented token standards like ERC-3643 to provide the market with transparent, real-time audit capabilities and genuine reserve backing.

- For policymakers, it is recommended to uphold a principle of technological neutrality while promoting innovations in the regulatory paradigm of "compliance as code." While adhering to the bottom line of preventing cross-border money laundering and systemic financial risks, they should guide the construction of unified ledgers based on multilateral consensus and deeply integrate national sovereign credit with programmable technology, building next-generation financial infrastructure suitable for the digital economy era.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。