Written by: Will 阿望

Just seven weeks before the acquisition was announced, Mastercard’s Chief Product Officer Jorn Lambert said during an analyst call that stablecoins "are currently not a universal payment tool." Seven weeks later, Mastercard announced it would acquire one of the world's largest stablecoin payment infrastructure companies for up to $1.8B.

Not because the judgment changed, but because they could not wait any longer—Stripe bought Bridge, Visa locked in Rain and Reap, and after negotiations with Coinbase fell through, there was still Circle. The independently purchasable targets at the stablecoin infrastructure layer are disappearing, and Mastercard had to make a choice before the window completely closed.

This is a follow-up situation. The first mover can cooperate because the first mover advantage is already there; the follower can only acquire because the pace of cooperation cannot catch up with the gap.

The numbers illustrate how large the gap is: the total on-chain transfer volume of stablecoins over the past 12 months was $46 trillion, with an adjusted actual payment scale of about $9 trillion, which is close to Mastercard's annual payment volume of $10.6 trillion in 2025— and this $9 trillion did not go through any card. In this most direct consumption scenario of stablecoin payment cards, Visa accounts for over 90% of transaction volume. Mastercard lost the first mover position; the $1.8B is a cost to make up for it.

1. Who is BVNK

BVNK does not issue stablecoins and does not make consumer wallets. What it does is a boring, yet critical task—stablecoin infrastructure.

What does this mean specifically? Worldpay wants contractors in 180 global markets to receive stablecoins, but Worldpay’s team does not understand blockchain, does not want to hold crypto assets, and does not have regulatory licenses across 130 countries. BVNK wraps these three layers into one API—dollars in Worldpay’s account go in, stablecoins out to the target wallet, and the target address can also be automatically converted to local fiat. Worldpay's system does not "encounter" any on-chain assets throughout this process. This is an infrastructure business, not a product business.

BVNK's value proposition can be summarized in one sentence: make stablecoins completely invisible to end users. The best infrastructure is that which disappears.

Who is using it is more convincing than any self-description. In 2025, BVNK added 226 customers, including: Worldpay, Deel, Flywire, Rapyd, Thunes, Bitso, LianLian Global, dLocal, Highnote, IC Markets, Equals Money, etc.

This is not a crypto-native customer list, but a global payment infrastructure customer list. Worldpay and Rapyd are top payment processors, Deel is a global payroll platform, dLocal is a leader in emerging market payments, and Thunes is a cross-border B2B remittance network. The traditional payment system is already using BVNK to run production traffic. This fact is more important than any valuation number.

The financing path itself is a judgment: this company is destined to be acquired. In December 2024, Haun Ventures led a $50M Series B; in May 2025, Visa Ventures made a strategic investment; in October 2025, Citi Ventures followed. In less than a year, the valuation rose from $750 million to the acquisition price of $1.8B. Visa invested in it, Citi invested in it, and in the end, it was bought by Mastercard—every round of investors coming in is conducting due diligence for the next buyer.

The Best Infrastructure Gets Acquired, Not Copied

BVNK has never claimed to disrupt anyone; it has quietly solved a problem that institutions cannot avoid: compliant access to stablecoin payments. 25 licenses and five years of accumulated regulatory relationships are harder to replicate than any technological advantage. The ultimate fate of these types of companies is never an IPO; it is acquisition.

2. BVNK's Position in the Stablecoin Payment Chain

BVNK sits at the most difficult to replicate layer of the stablecoin payment chain.

The complete chain from top to bottom: end users/merchants → payment products (wallets/gateways) → infrastructure (settlement, compliance, liquidity) → blockchain → fiat withdrawal. This layer requires three capabilities simultaneously: technology (cross-chain settlement), compliance (25+ licenses, regulatory adaptation in 130 countries), and liquidity (real-time exchanges for USD/EUR/GBP). None of the three can be lacking; each requires years of accumulation. If a bank wants to build a BVNK, just obtaining the licenses takes four to five years.

There are two delivery models for the product, serving two types of customers:

- Managed Payments: BVNK is responsible for compliance, custody, and payment execution, while the customer only calls the API. This is suitable for large payment institutions that do not want to face on-chain compliance directly, like Worldpay’s model—customers hold dollars in their own accounts, while BVNK completes all stablecoin conversions and settlements in the backend.

- Layer1: Customers have their own licenses, and BVNK only provides the technical pipes. Customers connect with their own on-ramp/off-ramp partners and liquidity providers, while BVNK orchestrates. This is suitable for fintechs that already have compliance capabilities and wish to fully control their risk exposure, like the way dLocal connects.

Supported rails cover Swift, ACH, Fedwire, SEPA, CHAPS, Faster Payments, and all mainstream chains such as Ethereum, Solana, Tron, Base. One API connects fiat rails and on-chain rails simultaneously. Once connected, all settlement paths are covered. What this means for the IT departments of enterprise clients needs no explanation.

A typical scenario: Deel tops up its BVNK account with dollars, issues an instruction—freelancers in 100 countries receive USDC or automatic conversion to local fiat within minutes. Deel never holds any crypto assets throughout the process and never directly interacts with any blockchain. Stablecoins are settlement tools in the entire transaction, not Deel’s product.

Stablecoin Tech Is Reproducible. Regulated Distribution Is Not.

Any engineering team can build a cross-chain settlement system within six months. But 25 licenses, regulatory relationships in 130 countries, and Worldpay and Deel willing to let you run production traffic—these three items have no shortcuts. Mastercard is not acquiring BVNK's code, but the regulatory distribution capability. This is the truly scarce thing in stablecoin infrastructure.

3. Mastercard vs Visa: Same Track, Two Different Bets

The core assets of V/M are not technology, but trust networks.

Issuing banks, acquiring banks, merchants, consumers—in the four-party model, every node relies on V/M as the intermediary trust layer: dispute resolution, fraud backing, compliance endorsements, global merchant acceptance. The value of this network lies not in its speed, but in its ubiquity. Any payment method that connects to this network automatically gains access to this trust infrastructure. This is what V/M is truly selling—not card swiping, but the distribution of trust.

Stablecoins have changed the settlement layer but have not solved the trust layer. Blockchains excel at transferring funds within seconds, but on-chain/off-chain conversions, compliance checks, and reconciliations cannot be answered with “a faster blockchain.” Stablecoins can bypass four-party models for peer-to-peer settlement, but what they lack is exactly what V/M has: global merchant acceptance, consumer protection, regulatory compliance.

The real question is not "Will stablecoins replace card organizations," but rather: Who will be the trust layer for stablecoins?

Visa provided its answer early on: I will be the trust layer. The layout is systematic—starting to test USDC settlement in 2021; officially launching in the United States in December 2025, and VisaNet will be obligated to settle USDC on Solana, with an annual settlement volume of $4.5 billion (according to Visa, Artemis/McKinsey's corresponding figure is about $3 billion, increasing from $1 billion to $3 billion in a single year, tripling); collaborating with Bridge to push stablecoin Visa cards to 18 countries; connecting with Phantom and MetaMask, allowing chain balances to be spent directly with cards. In January 2026, BVNK became a stablecoin infrastructure partner of Visa Direct.

Visa chooses cooperation rather than acquisition, and its revenue structure gives it the space for this choice. Visa collects network assessment fees itself—about 0.13-0.14% per transaction; the real big portion of interchange is the transfer payment from acquiring banks to issuing banks, which Visa does not touch. This means Visa's business model is essentially about "facilitating transactions," rather than "controlling the flow of funds." In the context of stablecoins, Visa only needs to connect the stablecoin rails to the network and let issuing and acquiring banks use them on their own—there is no need to own the infrastructure to still collect assessment fees. Cooperation is sufficient.

Mastercard's revenue structure is nearly identical to Visa’s. But Mastercard still acquired because it had no other choice. First movers can maintain their lead through cooperation, whereas followers can only buy time through acquisition—in the most direct consumption scenario of stablecoin payment cards, Mastercard's share is already very small, with Visa occupying over 90%. For a network that has already fallen behind, "staying open and waiting for banks to connect" is an empty statement. No one will proactively connect to a network with a smaller share. Mastercard needs to catch up; the speed of cooperation is insufficient, so it can only buy.

The root of the lag is the wrong level of focus. Mastercard early on focused on "exchange users"—Revolut, Bybit, Gemini, Binance all operate Mastercard card projects. Exchange cards follow market sentiment, active in bull markets and quiet in bear markets, making them cyclical. Visa linked earlier with full-stack stablecoin issuers like Rain and Reap, not relying on any exchanges, directly serving consumption scenarios—leading to structural growth. As a result, both sides have 130+ card issuance projects, but Visa bears over 90% of the transaction volume for stablecoin payment cards. The number of projects is similar, but the share is vastly different. The first mover chose the right layer and consumed the ecosystem.

Mastercard's statement makes this acquisition seem more like a forced pivot. Mastercard is compelled to answer a more urgent question: If competitors are rushing to buy out infrastructure, what independent targets will be available by the time it figures things out? The pressure does not come from the data, but from the speed of competitor actions.

First movers can cooperate. Followers can only buy.

4. Mastercard's Acquisition Logic

Mastercard has a trust layer but lacks the stablecoin layer—on-chain settlement, cross-chain compliance, and fiat entry and exit pipes. This is the part that cannot be built quickly and cannot wait.

Mastercard's acquisition is not a premature layout; it is a precise timing. BVNK co-founder Chris Harmse said before the acquisition: "If 2025 is the RFP year, then 2026 is the year for going live and scaling." The enterprise customer pipeline has grown 5-10 times, and large institutions are transitioning from "studying stablecoins" to "actually launching stablecoins." At the moment when the demand shifts from research to deployment, locking in the most critical infrastructure layer into its own network—this timing is neither too early nor too late.

4.1 BVNK is the Anchor Point That Mastercard Has Always Been Searching For

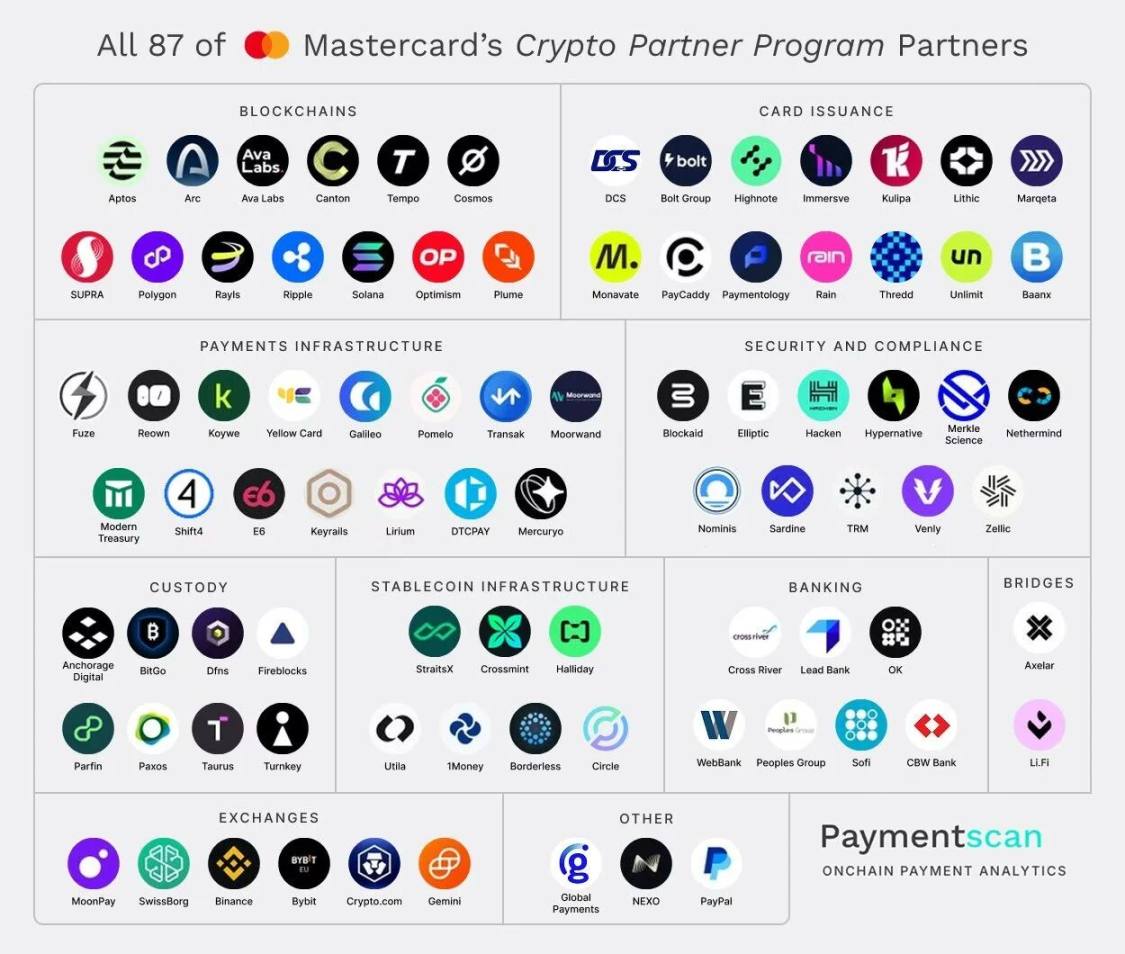

Six days before the acquisition was announced, Mastercard launched the Crypto Partner Program, uniting with over 85 partners including Circle, Ripple, Fireblocks, declaring its intent to directly connect the digital asset ecosystem with global payment infrastructure. A statement of such scale without a substantial technological foundation is hollow. BVNK is that foundation—not because the concept is good, but because it has already validated the stablecoin infrastructure layer, making BVNK the market’s closest thing to a "turnkey" option.

4.2 BVNK Also Needs Mastercard's Distribution Layer

BVNK’s customer scenarios are concentrated in B2B—corporate cross-border settlements, payroll withdrawals, payment processing channels. End users are unaware of its existence, while the C-side is almost vacant. Mastercard’s 350 million issued cards and 150 million merchant network precisely fill this gap. The highway is built; Mastercard is responsible for driving the cars onto it.

The numbers show why this path is correct. The annual volume of stablecoin payment cards is $18 billion, with a CAGR of 106% (Artemis); meanwhile, P2P stablecoin transfers only grew by 5% over the same period. Cards are experiencing an explosion while P2P is stagnating.

The reason is simple: Cards do not require anyone to change their spending habits.

Users swipe their cards, merchants receive fiat, and stablecoin settlements happen quietly in the backend. This is the path with the least friction to enter daily consumption scenarios, and it's also the reason card organizations are hardest to bypass. After stablecoins, tokenized deposits will be the next layer—tokenized deposits issued by banks also require this compliance settlement pipeline, and BVNK's infrastructure is naturally compatible.

Users do not lack willingness; they lack access points. A joint report by BVNK, Artemis, and Coinbase covering nearly 5,000 users across 15 countries found that 77% indicated they would use a stablecoin wallet if offered by banks or fintech. The trust is already there; the product is not. The integration gap further illustrates the issue—42% want to use stablecoins for large purchases, but only 28% are actually doing so; even for everyday subscriptions (Netflix, Google), 34% want to use stablecoin, while 27% currently do. The demand is not theoretical, but hindered by availability.

52% of stablecoin users have specifically gone to a merchant that accepts stablecoins for the sake of making a purchase. This isn't retention; it's new customer flow. The acceptance of stablecoins serves as a customer acquisition tool, not just a service tool. Mastercard connects 150 million merchants globally—after merging with BVNK, every merchant joining the Mastercard network has the opportunity to open this access point without having to build any stablecoin infrastructure themselves.

4.3 After the Merger, the Business Model Itself Will Also Upgrade

BVNK charges fees based on basis points when independent—it has weak pricing power—the customers are always price comparing, and BVNK itself is teetering at the break-even line. After merging with Mastercard, what changes is not the pipeline but the pricing system above the pipeline: stablecoin settlements are bundled into enterprise packages, new digital asset settlement fees are added, and C-side cardholder service fees are introduced. Three layers of income that BVNK could never reach on its own. The infrastructure remains, but the pricing power has changed. This is the real reason the $1.8B valuation can be supported.

4.4 The Window for Independent Targets is Closing

The stablecoin infrastructure layer once raced with three horses: Bridge went to Stripe, BVNK went to Mastercard, and only Zero Hash remains independently operated. Coinbase attempted to acquire BVNK for about $2 billion in November 2025, but negotiations fell through—they wanted near-term revenue, while BVNK's end-of-2024 revenue is about $40 million, making the return period too long. Mastercard is looking for technology and licenses; $40 million in revenue isn’t a consideration. Same target, but two buyers’ logic is completely different.

Reports indicate that Mastercard was also negotiating to acquire Zero Hash for $1.5-2 billion at the same time—multiple targets were in talks, indicating this is systematic catch-up, not opportunism. If not acquired now, prices will only go higher. $1.8B might already be at a discount price.

4.5 The Last Motivation is Defense

Lambert's statement is worth unpacking: "We expect most financial institutions will eventually offer digital currency services—whether stablecoins or tokenized deposits."

This is not a slogan. Research from American Banker shows that 54% of national banks and 47% of all banks expect to issue publicly available stablecoins within the next decade. The penetration rate is currently less than 1%; "most financial institutions" means this game has only just begun.

Mastercard's layout is the infrastructure layer required to serve these institutions—stablecoins are the entry point, while tokenized deposits are what banks genuinely desire. Allowing each bank to access this capability through the already trusted Mastercard network eliminates the need to find independent infrastructures. It’s not about the inability to bypass but rather the unnecessary nature of it.

The goal isn't to block the bypass. It's to make the bypass pointless.

Mastercard's defense logic isn't about "preventing institutions from bypassing me," but rather about "making bypassing unnecessary"—by embedding stablecoin settlement capabilities into the already trusted Mastercard network used by banks and enterprises, they have no reason to look for independent on-chain infrastructure. The $1.8B buys this reason of "no need for detours."

4.6 Opposing Viewpoints

After merging into Mastercard, BVNK may lose the value of "neutral infrastructure."

Part of BVNK's current value comes from its neutrality—Visa, Coinbase, and various fintechs can all be its clients. Once it belongs to Mastercard, how will the existing Visa Direct collaboration continue? Will those institutional clients who do not want to tie stablecoin settlement capabilities to a single card network seek alternative options? Once neutrality is lost, it’s difficult to regain.

Another discrepancy worth addressing is that William Blair noted in their analysis report on the day of the acquisition, "We believe this acquisition further validates the value of stablecoins in cross-border commercial scenarios, rather than B2C payments— the latter is already well served by card payments."

In other words, the main battlefield for stablecoins may be B2B and cross-border, rather than the consumer card payment scenarios emphasized in this article. If this judgment is correct, Mastercard’s C-side distribution advantage may not be as critical, and the acquisition logic leans more towards defense rather than offense.

If you can't win, just buy it. $1.8B is the current price—wait another year, and there may be no targets left to acquire. The follower cannot afford to be patient.

5. Follow-up Worth Observing

The questions raised by this acquisition are more than those it answers.

Fedwire has opened a crack. The OCC has conditionally approved a national trust bank charter for five institutions, including Circle and Paxos. A more specific case is Kraken—by the end of 2025, it will gain direct access qualifications to Fedwire, becoming one of the first crypto-native institutions to participate directly in the Federal Reserve clearing network.

Once the "skinny master account" being discussed by the Federal Reserve is implemented, stablecoins will no longer just be an alternative to the banking system but will directly participate in America's core clearing infrastructure. After merging with BVNK, Mastercard's credibility for pursuing this pathway will significantly improve.

Visa has not acquired anyone—this itself is a judgment. The BVNK equity held by Visa Ventures will belong to Mastercard following the acquisition, turning a strategic partner into a competitor's asset. However, Visa's response is not to acquire, but to continue expanding its network of partnerships: collaborating with Stripe/Bridge to push stablecoin Visa cards to more markets; deepening USDC settlement integration with Circle—Circle is essentially doing the same thing as BVNK, but from the issuer's perspective.

Visa's logic remains "let transactions happen" rather than "control infrastructure." First movers do not need to buy out, as open networks are inherently defensible.

The distribution layer of stablecoin payments is rapidly being consolidated. The endgame of this track is not diversification; it is that card organizations, banks, and major fintechs gradually acquire compliance distribution capabilities—whoever controls this layer controls the entrance for stablecoins into daily consumption. Stripe buying Bridge was the first domino; Mastercard buying BVNK is the second. How many independent targets remain in the infrastructure layer? For each one that disappears, the remaining ones become more expensive.

BVNK's path is a forecast: you don’t need to become Stripe, you only need to be irreplaceable at a certain layer. Focus on accumulating licenses and building trust with enterprise clients, allowing giants to calculate their in-house costs and come knocking. From $750 million to $1.8B in less than a year. This is not luck. The next to be acquired is repeating the same process in some market.

Of course, the ultimate fate of stablecoins may contradict the narrative of stablecoins themselves—they may disappear from the public eye. Everyday customers do not need to know what "stablecoins" are; they are already using them. This may seem boring, but it means they have already won. They are everywhere.

Stripe bought Bridge, Mastercard bought BVNK.

Visa has not yet acquired anyone—but maybe it does not need to at all.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。