Just as the entire market eagerly awaits the Federal Reserve's interest rate meeting this week, a ghost that no one wants to face is once again hovering over Jackson Hole—the war in the Middle East has once again pushed central banks around the world to the brink of stagflation.

For the fifth consecutive year, whenever Federal Reserve officials are filled with hope that inflation is about to return to the "gentle haven" of 2%, reality always slaps them hard in the face. From the aftermath of the pandemic to the Russia-Ukraine conflict, from the comprehensive tariff plans of two years ago to the current flames of war in the Persian Gulf, the battle against inflation seems trapped in an endless cycle.

Now, the skies above the Strait of Hormuz are thick with clouds of war, international oil prices have aggressively broken the $100 per barrel mark, and gasoline prices in the US have surged by 18%-25% since late February. What lies ahead for the Federal Reserve is no longer the easy question of when to cut rates, but rather a soul-searching inquiry that could rewrite the history of monetary policy: This year, can rates still be cut?

1. From "When to Cut" to "Can We Cut", a Matter of Life and Death for Expectation Management

● Timiraos points out that the core question among officials has undergone a qualitative change at this week’s meeting. The question now is not when the next rate cut will be, but whether these decision-makers, who control the global cost of capital, can still confidently allow the market to hold expectations for rate cuts.

● This war is almost certain to strengthen the consensus among officials to "keep interest rates unchanged." But more tricky than remaining inactive is what signals they should send months later. The market is like a crying baby; if they feed it the wrong milk, it might trigger severe vomiting of global risk assets.

● If you think this is just another old cliché of "the wolf is coming," then you are sorely mistaken. This time, the script is compounded by high oil prices, high inflation, cracks in the labor market, and the transition of the Federal Reserve chair.

2. Three Traffic Lights, Tonight’s Market Nuclear Button

Combining the guidance of the "trombone" and the data from global prediction platforms, tonight's interest rate meeting is not merely a formality, but has three nuclear-level highlights, each of which could ignite a new round of global asset pricing reset:

● Signal 1: To Delete or Not to Delete the Words "Rate Cut" in the Policy Statement?

In the January meeting of this year, a few hawkish officials attempted to delete terms implying "the next action will be a rate cut" from the statement, but were unsuccessful. Timiraos analyzes that if this meeting ultimately makes this modification, it would be the first official acknowledgment that "the easing cycle may have ended." This is not just wordplay; it is the "obituary" of a shift in monetary policy.

● Signal 2: The "Bloody Face Change" of the Dot Plot.

This is the most gruesome and direct highlight. In December last year, 12 of 19 officials expected at least one rate cut this year. But now, in this situation, as long as three of them change their minds, the much-watched "median" expectation for rate cuts will directly fall to zero.

The market has already voted with its feet. According to the options prices calculated by the Atlanta Fed, traders last weekend believed that the probability of at least one rate cut by December of this year has plummeted to 47%, while before the outbreak of the Iran war last month, this probability was as high as 74%. Even more alarming, during the same period, the probability of raising rates by the end of the year surged from 8% to 35%.

● Signal 3: Powell's "Last Dance".

This might be the most tortured press conference for Powell as his term countdown begins. His chairmanship will end in May this year, which means that any policy set this week will become the baseline for his successor. Will he respond strongly to inflation during the press conference and leave a “hawkish” foundation for his successor? Or will he be ambiguous and pass the buck to the next one? Every word will be interpreted by the market under a magnifying glass.

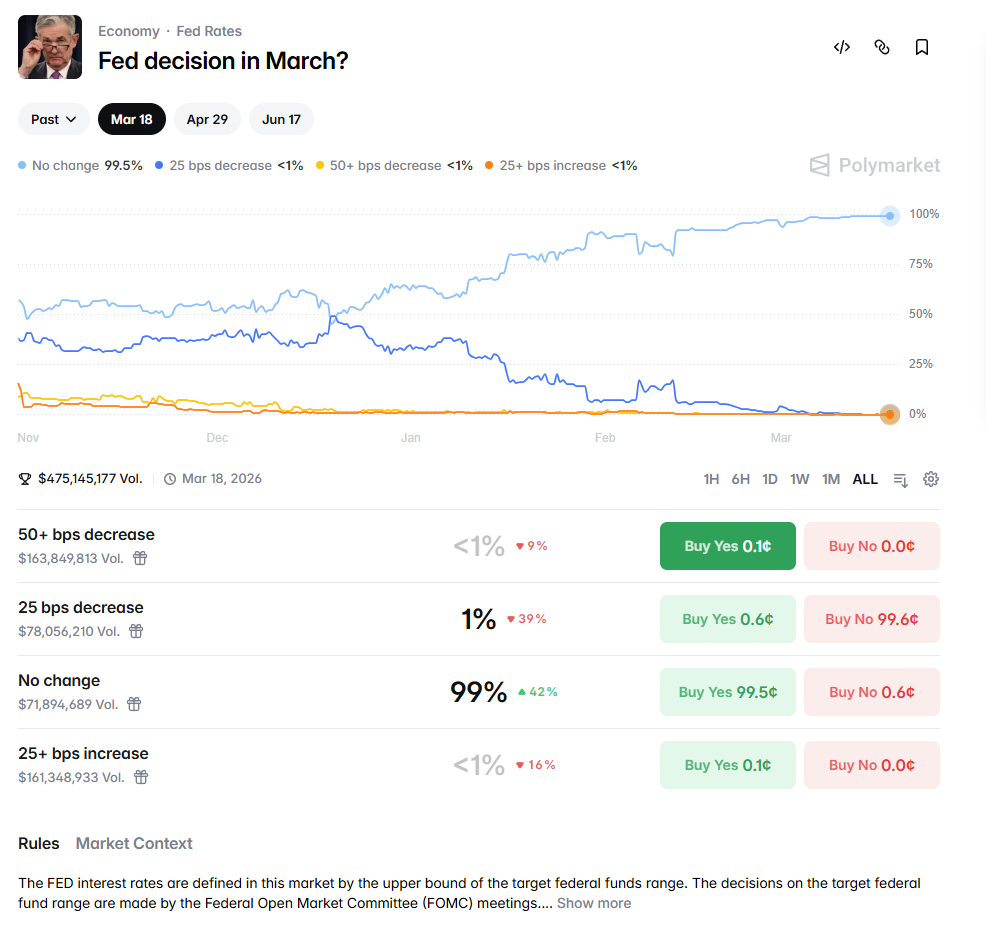

3. Polymarket's "Prediction": Traders Bet Real Money on "Not Cutting Rates"

● On the decentralized prediction platform Polymarket, contract trading regarding this Federal Reserve's decision has long been filled with smoke. As an "alternative data source" outside traditional financial markets, Polymarket's pricing often sensitively captures the true thoughts of smart money.

● Data shows that as of March 18, traders bet that the probability of the Federal Reserve keeping rates unchanged at this meeting is as high as 99%, while the probability of a 25 basis point rate cut is only about 1%, and the probability of a rate increase can be virtually ignored.

● More interesting is the yearly prediction. A contract on Polymarket about "the number of rate cuts by the Federal Reserve in 2026" shows that the probability of believing there will be no rate cuts this year has risen to 23%, while the probability of expecting at least three rate cuts has fallen from a pre-conflict peak to just 12%. This data starkly reveals a cruel reality: global traders are rapidly digesting the expectation of "longer-term higher rates."

4. The "Nightmare Cycle" of Inflation: Is This Time Really Different?

● In the face of an oil shock, traditional central bank textbooks tell you to "think longer term," because the impact of rising oil prices on economic growth and the push of inflation will roughly offset each other. But now things are different; this advice assumes that the public has to believe inflation will eventually come down.

● However, the reality is that the American public has experienced five consecutive years of inflation above target, along with a series of reminders about rising prices; this "trust" has long been a luxury. Minneapolis Fed President Kashkari questioned in an interview this month: "Do we really want to do 'transitory inflation 2.0' again?"

● The core PCE price index, favored by the Federal Reserve, accelerated to 3.1% in January, up from a low of 2.6% in April last year. Inflation is not dead; it is being revived by the winds of geopolitical conflict.

● Former St. Louis Fed President Bullard's remarks are even more direct: had it been last year, he would still have included a rate cut in the plans, but now he would cross out that plan. Facing core inflation exceeding 3% and trending upwards, "you definitely don't want to commit to rate cuts at this juncture."

5. Who Can Reopen the Strait of Hormuz?

Pradeep Philip, head of economic research at Deloitte, pointedly remarked: "Central banks can set interest rates, but they cannot reopen the Strait of Hormuz."

Tonight, no matter how Powell words things, no matter how the dot plot fluctuates, an undeniable fact has already been laid on the table: the "stagflation" risk of the global economy is being re-priced due to the conflict in the Middle East. For investors, the narrative of "buying on dips" related to rate cuts has gone bankrupt, and what awaits us may be a "purgatory mode" that struggles to survive between inflation and recession.

The only certainty is that the script of history has never seemed so similar, and this time, the cards held by the Federal Reserve are worse than at any previous time.

Join our community to discuss and become stronger together!

Official Telegram community: https://t.me/aicoincn

AiCoin Chinese Twitter: https://x.com/AiCoinzh

OKX Benefits Group: https://aicoin.com/link/chat?cid=l61eM4owQ

Binance Benefits Group: https://aicoin.com/link/chat?cid=ynr7d1P6Z

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。